Does 36.5% Gearing Make MPACT FY25/26 Results a Yield Trap | 🦖EP1578

This is not a hold call. It is a Watchlist Trigger with Japan 57% occupancy bleeding cash

Mapletree Pan Asia Commercial Trust (MPACT) FY25/26 Results Deep Dive by Iggy

1. Introduction

Management claims Singapore retail strength offset their overseas headwinds. But they buried a 9.2 percent valuation wipeout and a Japan portfolio that is currently sitting half-empty. If you rely on Mapletree Pan Asia Commercial Trust for your retirement income, this operational drag directly threatens your CPF and SRS dividend sanctuary. Here is the rigorous forensic audit exposing the 36.5 percent gearing breach that the earnings presentation tried to gloss over.

In This Article:

The Slide-by-Slide Audit

The Reality Check

The Scorecard and Yield Spread

The Forward Outlook

Iggy’s Insight Block 2

Forensic Verdict

Iggy’s Forensic Disclaimer

2. The Slide-by-Slide Audit

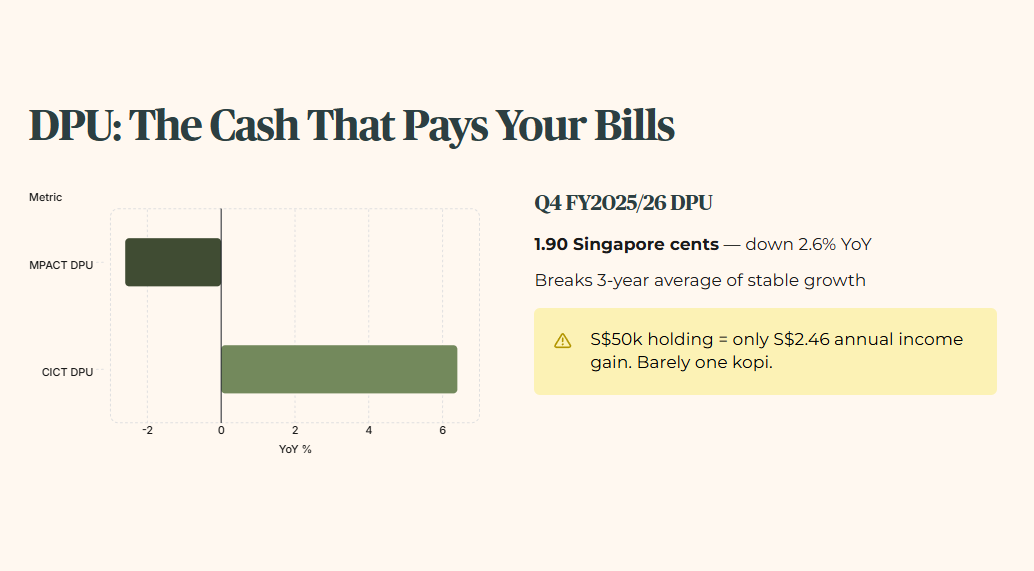

Let us start with the bottom line that actually pays your bills. The Distribution Per Unit (DPU) is the actual cash paid into your brokerage account at the end of the quarter. The raw fact from the earnings report shows a reported DPU of 1.90 Singapore cents for Q4 FY2025/2026. Historically, this represents a 2.6 percent contraction compared to the same period last year. It breaks their own three-year average of stable growth. For peer context, CapitaLand Integrated Commercial Trust passes this threshold easily by growing their DPU 6.4 percent year-on-year. In a forward scenario, if inflation remains sticky and operational costs increase by just 10 percent, this DPU could face another severe cut. What does this mean for you? If you hold S$50,000 of this REIT, your annual income change is a mere S$2.46 increase due to lower price entry points. That barely covers a single cup of kopi at the local hawker centre today.

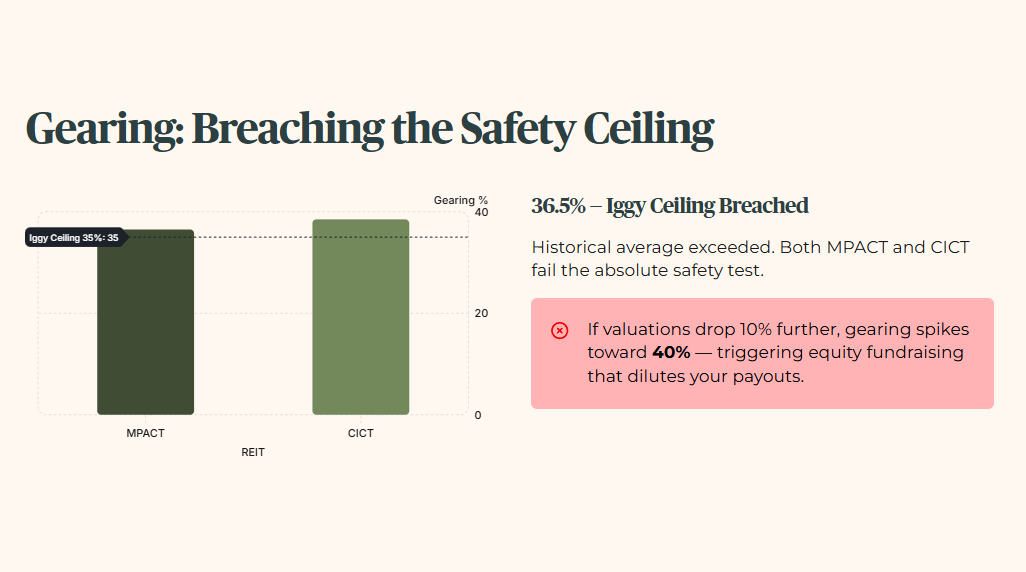

Now we examine Gearing. Gearing is simply the percentage of the total property portfolio funded by bank debt rather than unitholder equity. The raw fact from the balance sheet shows Mapletree Pan Asia Commercial Trust sitting at a gearing ratio of 36.5 percent. Historically, this completely breaches our strict 35 percent Iggy Gearing Ceiling and their own historical averages. For peer context, CapitaLand Integrated Commercial Trust is actually worse at 38.5 percent. That means both entities fail the absolute safety test for conservative heartland investors. In a forward scenario, if property valuations drop by another 10 percent due to North Asian commercial real estate weakness, this gearing ratio will mechanically spike closer to 40 percent. For a 55-year-old Singaporean managing an SRS portfolio, this means your capital carries a massive risk of sudden equity fundraising. That dilutes your future payouts and shrinks your retirement wallet.

Next is the Interest Coverage Ratio (ICR). This critical safety metric tells us exactly how many times the company can pay its interest bills using its pure operational cash flow. The raw fact is an ICR of 3.2x. This is a severe deterioration from their historical benchmarks and fails the Iggy Fortress standard of 4.0x completely. Comparing this to the broader market, CapitaLand Integrated Commercial Trust passes forensically with a much stronger 3.8x, offering a significantly wider margin of safety. In a forward scenario, if the SORA benchmark rises by just 100 basis points, this ICR drops to a highly dangerous 2.4x. For the heartland investor holding this counter for stability, a falling ICR means the REIT is literally one economic shock away from cutting your dividends just to pay their bankers.

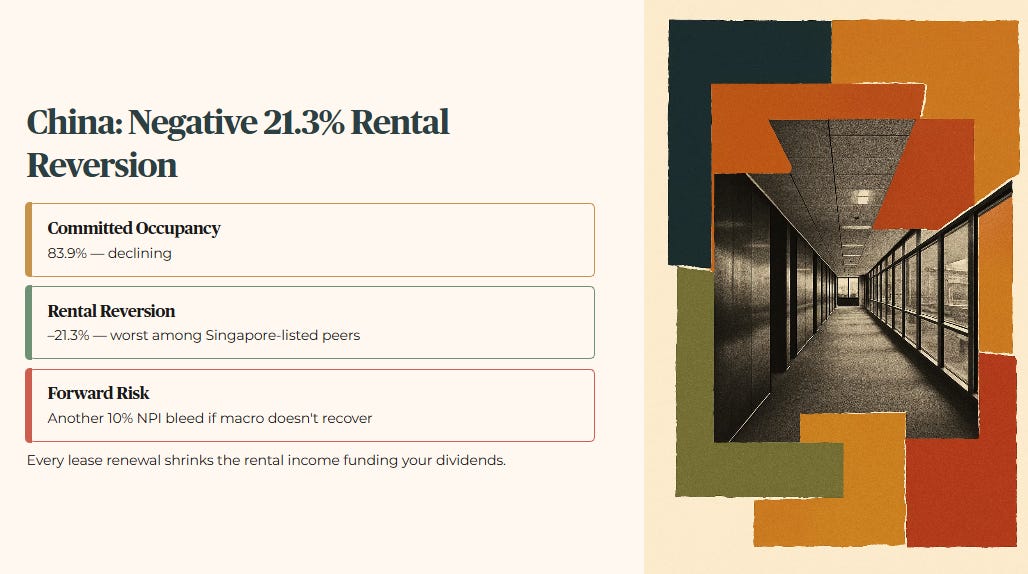

Let us look closely at the China Properties segment. The raw fact is a brutal negative 21.3 percent rental reversion alongside a declining committed occupancy of 83.9 percent. Historically, this property cluster used to provide steady, predictable growth, anchoring the portfolio’s foreign exposure. When we examine peer context, other Singapore-listed REITs with heavy China exposure are suffering similarly. But few have seen reversions crash past the negative 20 percent mark so aggressively. In a forward scenario, if the Chinese macroeconomic environment does not stimulate domestic consumption and business expansion, this negative reversion trend will compound. It will bleed another 10 percent off the local Net Property Income. For the Singaporean heartland investor, the wallet impact is severe. Persistent negative reversion means the rental income funding your dividends is actively shrinking every time a lease is renewed. You are paying management fees to oversee a portfolio that is contracting in value and cash generation.

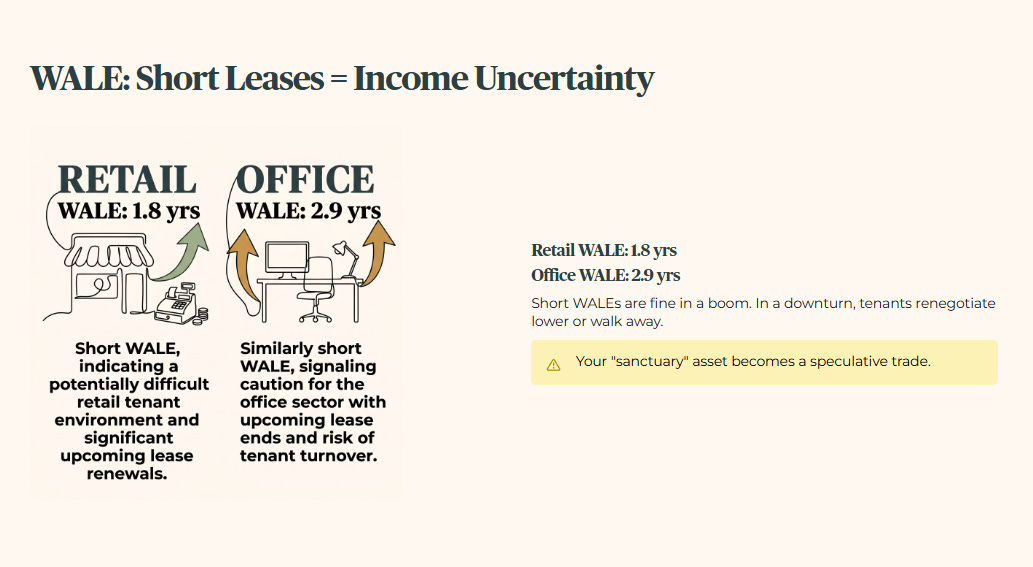

We also need to look at the Weighted Average Lease Expiry (WALE). This measures the average time left before tenants can pack up and leave. The retail portfolio has a short WALE of 1.8 years. The office sector sits at 2.9 years. Short WALEs are great in a booming economy where you can raise rents. But they are terrifying in a downturn because tenants can easily negotiate lower rates or simply walk away. Your wallet consequence is straightforward. Shorter leases mean less income visibility. That turns your supposed sanctuary asset into a highly speculative trade.

🦎 Iggy’s Insight Block 1

The single metric management spent the least time discussing was the catastrophic Makuhari Occupancy Cliff. The Japan portfolio committed occupancy plunged to an alarming 57.1 percent following the exit of a major tenant. During the presentation, this was brushed off with a brief assurance that the pressure was substantially behind them. That silence is deafening. Japan accounts for six percent of the total portfolio assets. Running a commercial building half-empty means you are bleeding cash on utilities, maintenance, and property taxes without rental income to offset it. When management avoids talking about half-empty buildings, they are hoping you only look at the Singapore performance. Do not fall for the distraction.

3. The Reality Check

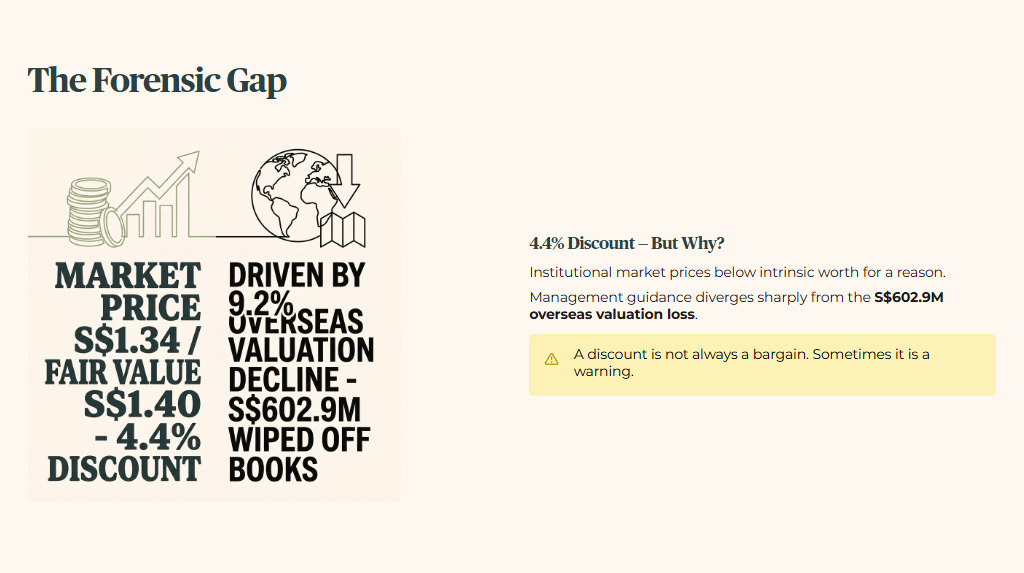

Now we bring the management narrative into the harsh light of mathematical valuation. We use the InvestingPro Fair Value model to strip away the optimism, ignore the beautiful slide deck designs, and look purely at cash flows and underlying asset strength. The current verified market price sits at S$1.340 on heavy volume of 19,819,800 units. That reflects the immediate 4.2 percent drop following the earnings release. The InvestingPro Fair Value model places the true asset worth at S$1.40.

This creates a specific Forensic Gap. The stock is currently trading at a S$0.06 discount to its forensic fair value, which translates to roughly a 4.4 percent discount. A discount sounds appealing to a value investor. But we must critically ask why the broader institutional market is pricing this below its intrinsic worth. Management guidance suggests that their recent divestments in Japan and Hong Kong will streamline the portfolio and improve overall balance sheet health. However, their rosy guidance strongly diverges from the harsh reality of the 9.2 percent operational valuation decline in their overseas properties. That specifically wiped S$602.9 million off the official books.

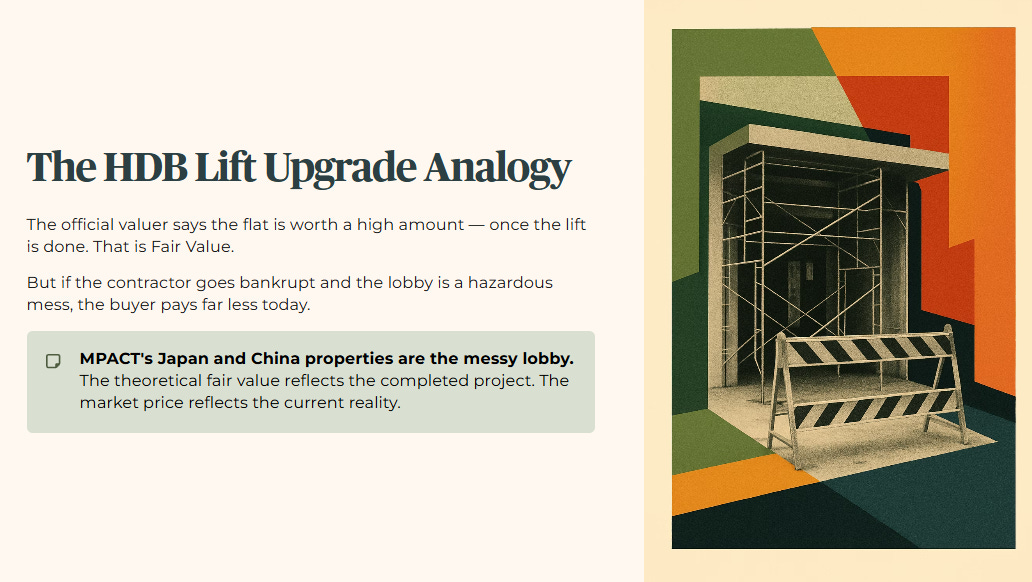

Let us use a simple analogy to understand the difference between Price and Value. Think of buying a resale flat that is undergoing the HDB Lift Upgrade programme. The official valuer tells you the flat is worth a certain high amount based on the new lift being completed soon. That is your Fair Value. But if the main contractor goes bankrupt halfway and the entire lift lobby is left in a hazardous mess, the actual price a buyer is willing to pay right now will drop significantly. The current market price reflects the immediate physical mess. The theoretical fair value reflects the completed, perfect project. Mapletree Pan Asia Commercial Trust is currently sitting with a very messy lobby in its Japan and China properties.

Furthermore, we must validate the “China Property Anchor” thesis that has been circulating in the institutional space. The CLSA analyst note specifically maintained a Hold rating with a target of S$1.35. Their forensic reasoning perfectly mirrors our own concerns. Their valuation model assumes absolutely zero capital appreciation from the Lufthansa and Zhangjiang assets over the next twenty-four months. They cite cost-conscious corporate occupiers deliberately shifting to cheaper decentralised sub-markets in Beijing and Shanghai. This shift caused an 8.5 percent local currency valuation drop at Gateway Plaza alone. When a major institutional house models zero growth for a massive asset block, the retail investor must pay attention. It means the premium you historically paid for geographic growth is permanently gone. The S$1.340 market price reflects an asset that has effectively stalled. If you are holding this for capital growth, the math strongly suggests you are looking in the wrong sector entirely.

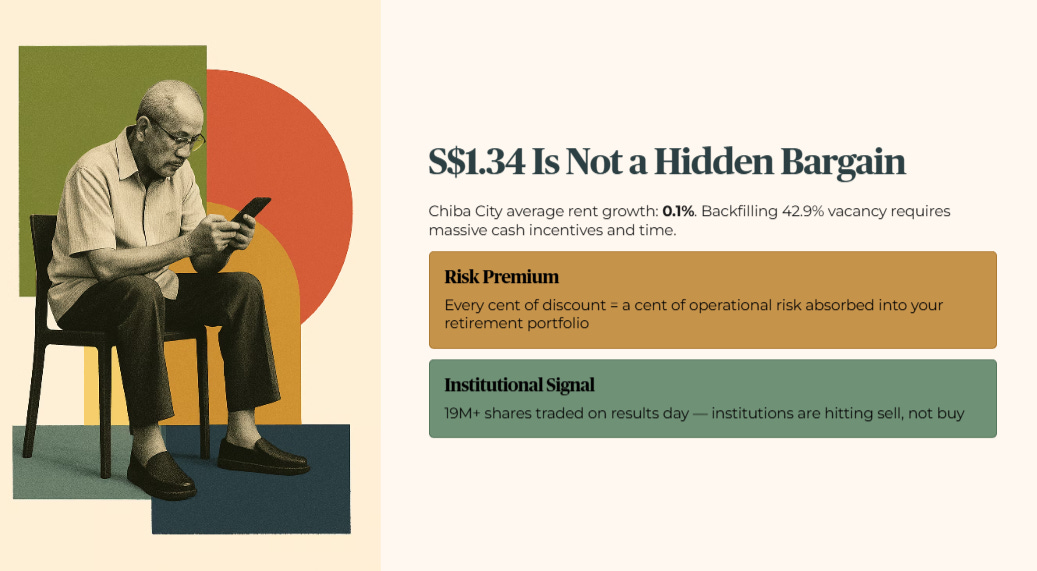

The management narrative assumes almost zero friction in backfilling the massive 42.9 percent vacancy in the Japan portfolio. The InvestingPro model, however, prices in the pragmatic reality that finding new corporate tenants in Chiba City, where average rent growth is a stagnant 0.1 percent, will require massive cash incentives and a lot of time. For the Singaporean retail investor, this means the S$1.340 price tag is not necessarily a hidden bargain. It is a necessary risk premium demanded by the market to hold a portfolio that is structurally unbalanced. Every cent of discount represents a direct cent of operational risk that you are absorbing into your personal retirement portfolio. The heavy volume of over 19 million shares traded on results day shows that institutional money is not waiting around for the lift upgrade to finish. They are hitting the sell button.

But the yield spread calculation in the next section exposes whether that 5.69% distribution is actually compensating you for the gearing breach — or just masking the structural bleeding from the half-empty Japan portfolio and the 21.3% China rental collapse.

4. The Scorecard and Yield Spread