Don’t Chase Yield. Use This 5-Factor Score to Find Resilient DPUs Through 2026’s Refi Hump

Many Singaporean investors think high yields alone guarantee REIT safety. But in a new rate cycle, the old playbook falls short. Here’s how to see through surface-level noise.

Many Singaporean investors think high yields alone guarantee REIT safety. But in a new rate cycle, the old playbook falls short. Here’s how to see through surface-level noise and use a disciplined 5-factor score to identify the few trusts that can keep incomes resilient—even with refinancing risks and market headwinds on the horizon.

Setting the Scene: Singapore’s REITs in 2025—Why Surface Numbers Aren’t Enough

It’s tempting to just hunt for the highest yields. But after two years of rate hikes, quick “easy income” REITs aren’t what they seem. Maybe some blue-chips sit in the portfolio. Maybe DPU looks flat and hope is for a bounce as rates edge down. Yet payouts are not rebounding in a straight line.

Most REITs face a refinancing wall through 2026. Some locked in higher-cost debt in 2023–2024. Others raced to hedge at fixed rates. DPUs can look steady while balance sheets either heal or strain beneath the surface.

This is where many get tripped up: they stop at the headline yield. To build a REIT sleeve that can ride the 2026 refi cycle, look deeper. Use a scorecard that weighs debt, coverage, and tenant strength. That is the edge institutions use. In this piece, we’ll walk through the 5-factor score, then apply it to three archetypes—Anchor, Growth, Disruptor—so allocation and risk controls become clear and repeatable.

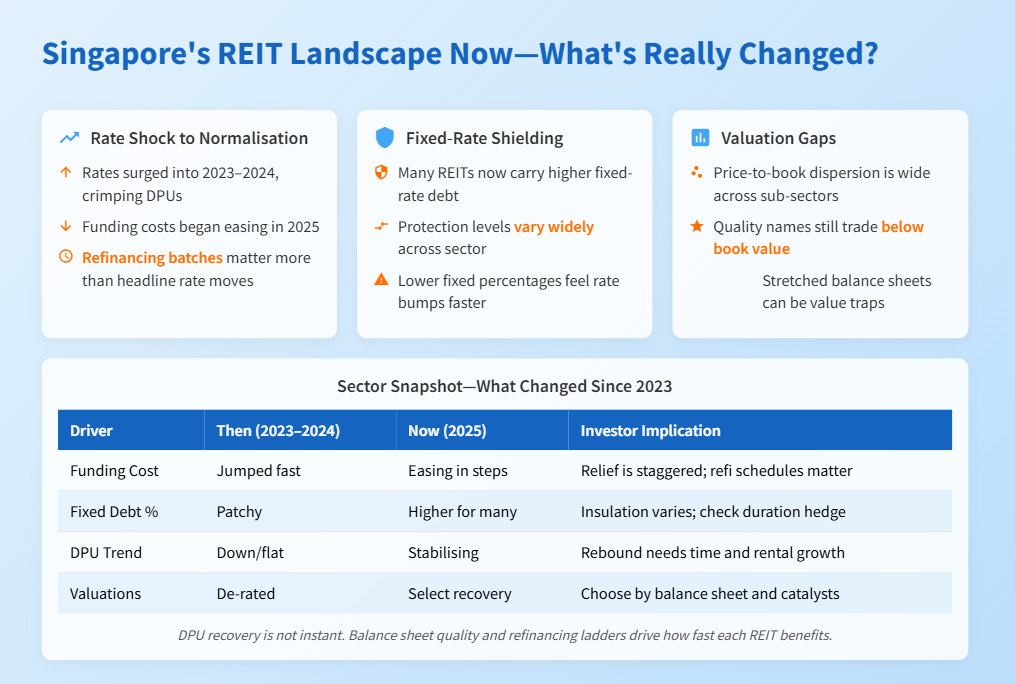

Section 1: Singapore’s REIT Landscape Now—What’s Really Changed?

Rate Shock to Normalisation

Rates surged into 2023–2024, crimping DPUs and pushing leverage higher.

In 2025, funding costs began to ease, but the benefit lands with a lag.

Refinancing batches matter more than the headline rate move.

Explanation: Think of rates like a tide that fell fast, then rises slowly. REITs refinance on set dates, not every day. So even if base rates ease now, the full relief only shows when older, expensive loans roll over. That is why DPUs feel “stuck” before they improve.

Fixed-Rate Shielding and Dispersion

Many REITs now carry higher fixed-rate debt protection.

Protection levels vary widely across the sector.

Lower fixed percentages feel rate bumps faster and harder.

Explanation: Fixed-rate debt is like an umbrella in a drizzle. If a REIT fixed 80% of debt for two to three years, it stays dry while showers pass. If it fixed only 55–60%, more of its debt gets wet when rates blip. Two REITs can face the same weather but have very different outcomes.

Valuation Gaps

Price-to-book dispersion is wide across sub-sectors.

Some quality names still trade below book value.

Others with stretched balance sheets are value traps.

Explanation: A low valuation is not always a bargain. If assets are good, debt is moderate, and cash flow is solid, a discount can be attractive. If leverage is high and coverage thin, a cheap price can mask risk. The 5-factor score separates the two.