EXCLUSIVE: Seatrium (5E2) Saves the Deal but Becomes a $250M Bank

Everyone is cheering the “settlement” with Maersk today. It sounds like good news: the massive Wind Turbine Vessel (Phoenix II) isn’t getting cancelled.

But let’s look at the fine print.

The “Signal”

Seatrium didn’t just win a contract; they had to buy their way out of a problem. To ensure this vessel actually leaves the shipyard by Feb 2026, Seatrium is lending its own client US$250 million (S$330M+) for 10 years.

Think about that. Seatrium is supposed to be a shipbuilder. Now, they are a bank. They are locking up S$330M of liquidity—money that could have paid down debt or paid us dividends—just to save face and keep the order book moving.

Combine this with the US government pausing major offshore wind projects, and the “Green Pivot” suddenly looks a lot riskier than it did last week.

The “Data Check” (InvestingPro Integration)

The Divergence: The math is confusing right now, which is why we need to be careful.

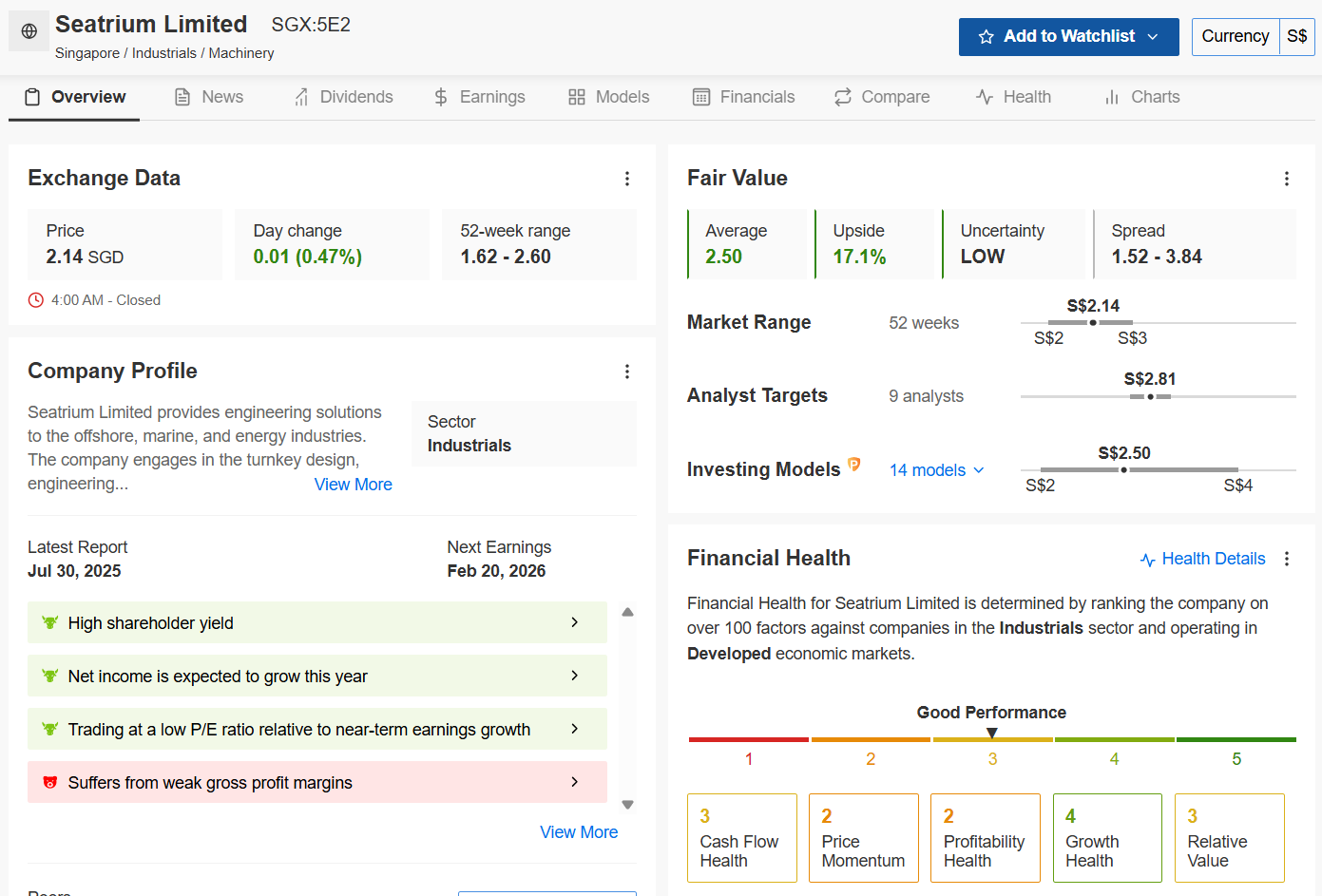

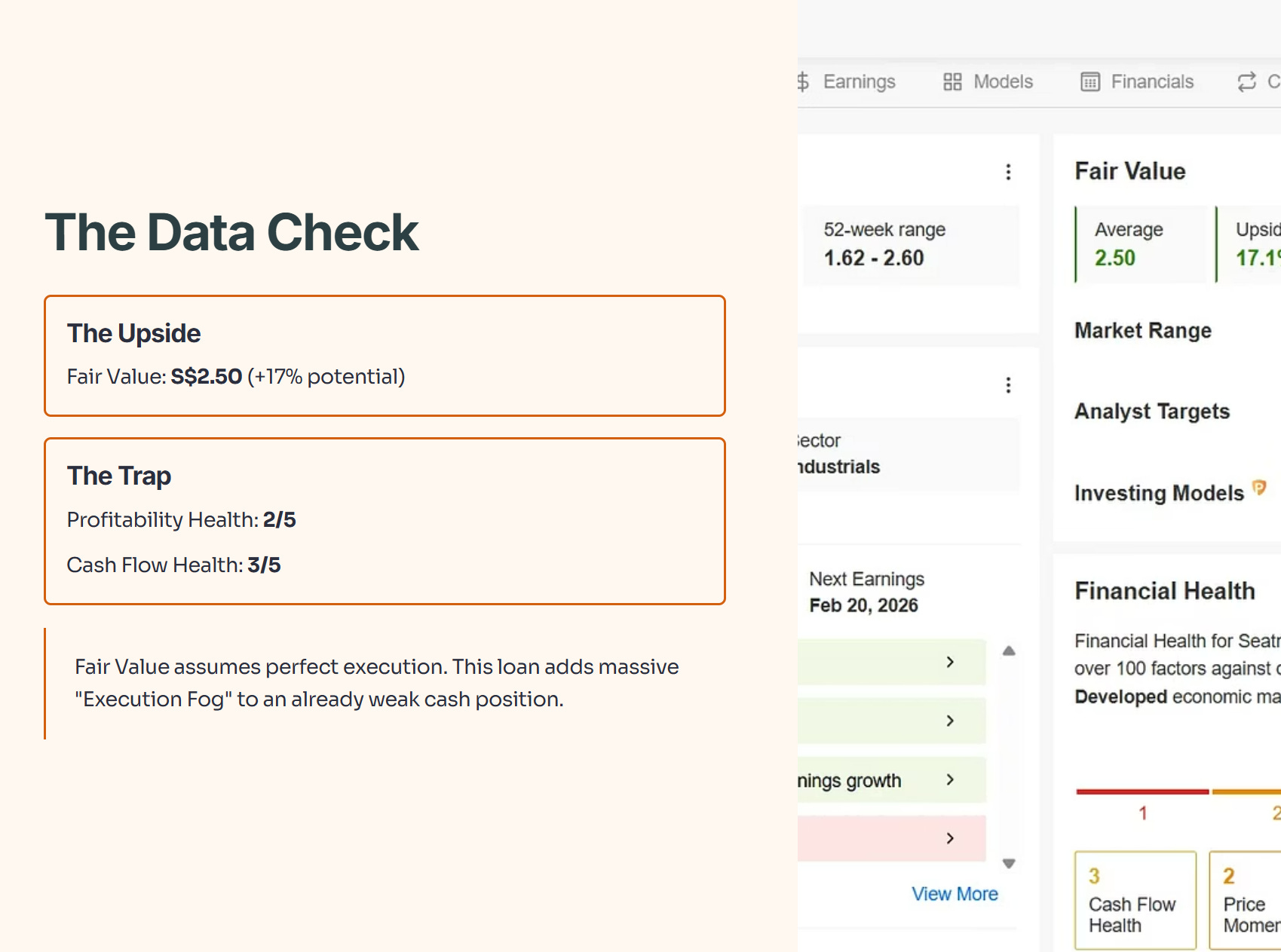

The Upside: The Fair Value model actually sees a target of S$2.50 (+17% upside).

The Trap: Look at the Profitability Health (2/5) and Cash Flow Health (3/5).

The Fair Value assumes Seatrium executes perfectly. But this new loan adds a massive layer of “Execution Fog.” A company with weak cash flow shouldn’t be lending hundreds of millions to customers in a slowing sector.

Iggy’s Verdict (Actionable)