EXCLUSIVE: The BBCA Valuation Trap: Why This "Buy Signal" is Dangerous

Here is the setup. You look at the charts, and the algorithms are screaming “BUY.” The models are promising you a +28.5% Upside. It looks like free money lying on the floor.

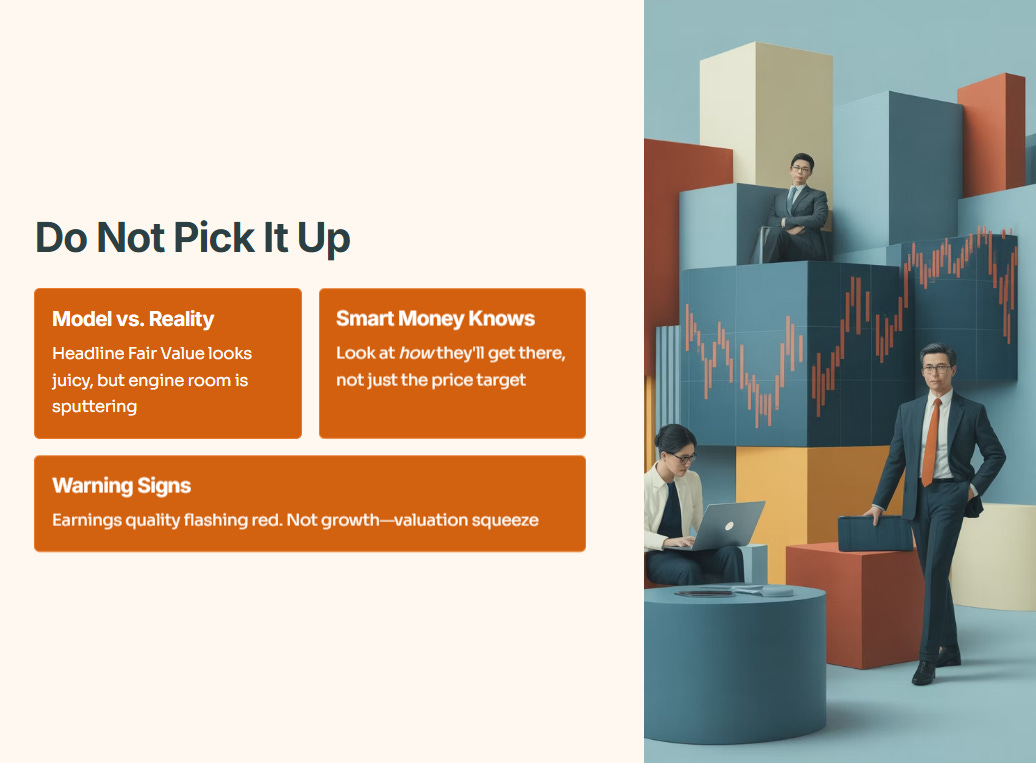

Do not pick it up.

This is a classic “Model vs. Reality” trap. While the headline Fair Value looks juicy, the engine room is sputtering. The “Smart Money” doesn’t just look at the potential price target; we look at how they are going to get there. And right now, the quality of the earnings is flashing red warnings. This is not a “growth story” anymore; it’s a “valuation squeeze.”

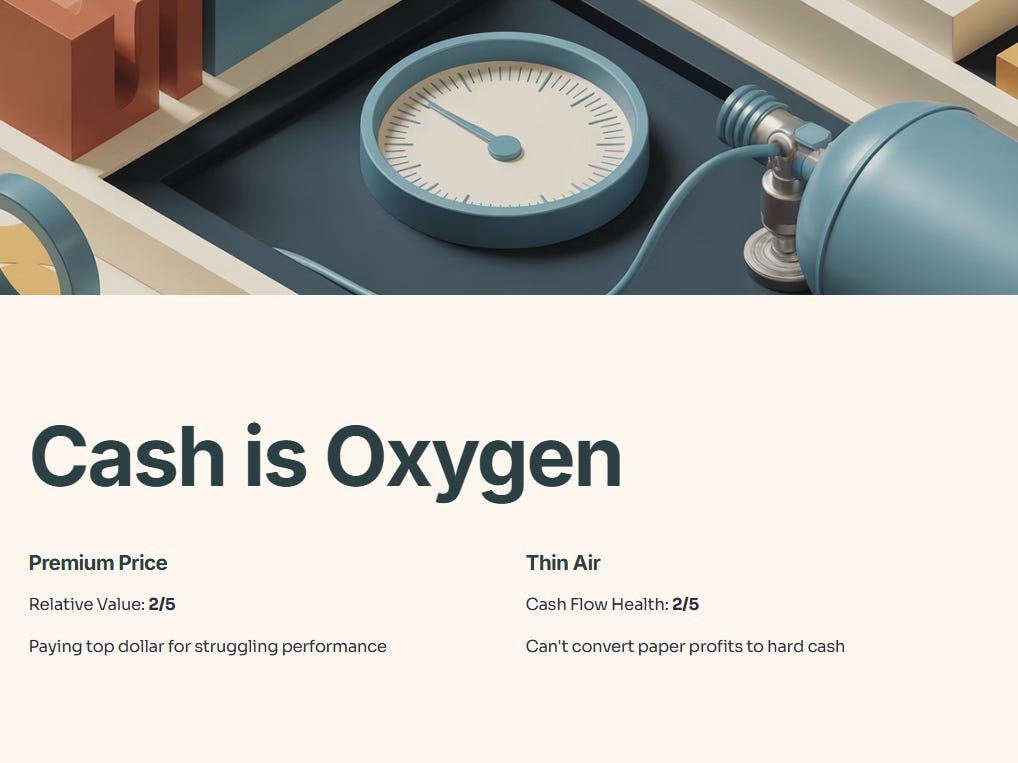

You are being asked to pay a premium price (Relative Value: 2/5) for a company that is currently struggling to convert paper profits into hard cash flow (Cash Flow Health: 2/5). In this volatility, cash is oxygen. BBCA is running thin on oxygen.

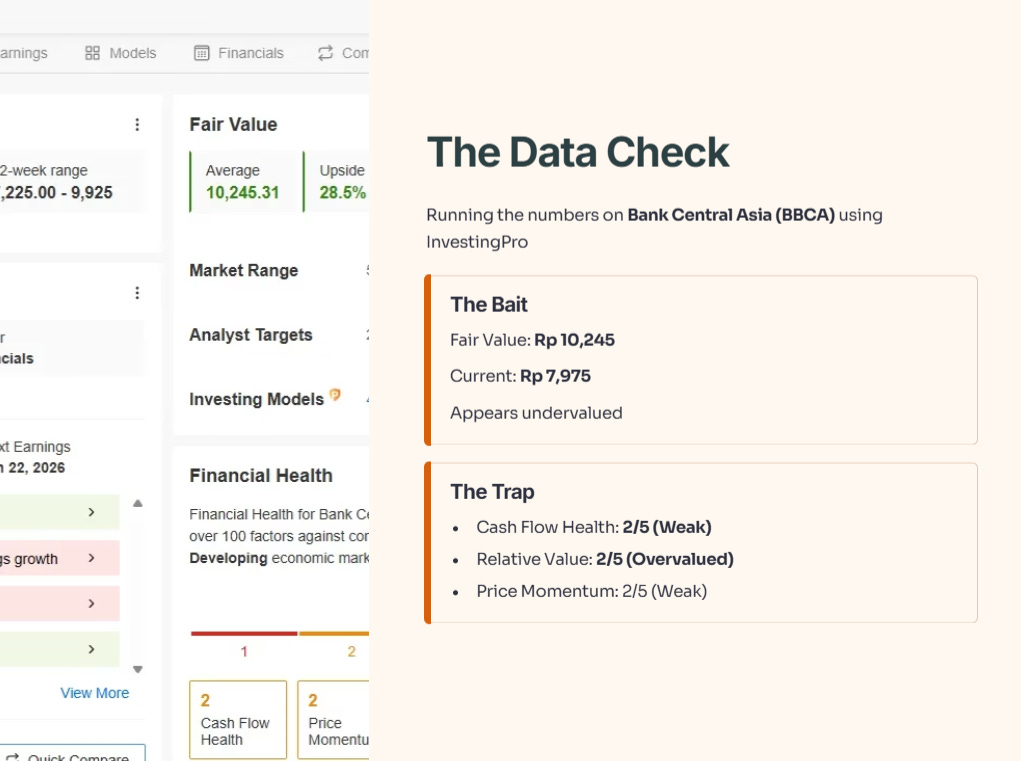

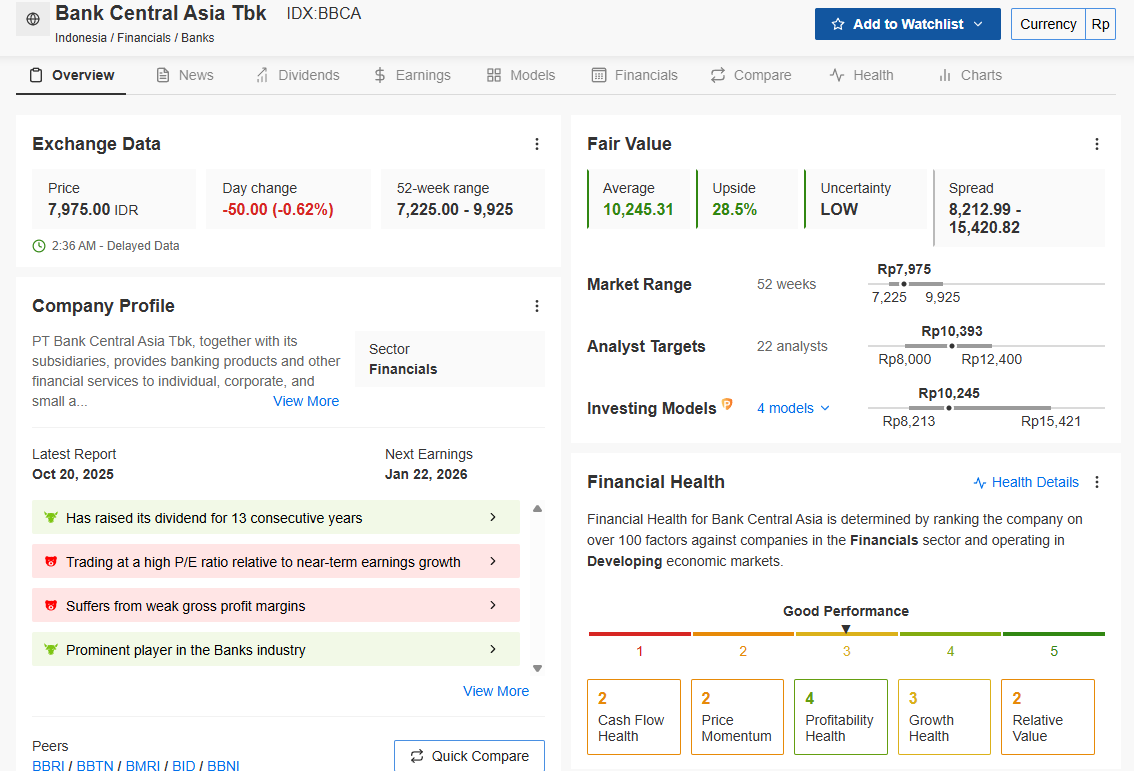

The Data Check

I ran the numbers on Bank Central Asia (BBCA) using InvestingPro to see if the hype holds water.

The Divergence: Look at the contradiction in the image above.

The Bait: The “Fair Value” is Rp 10,245, suggesting the stock is undervalued at its current Rp 7,975.

The Trap: Look at the Financial Health breakdown at the bottom right.

Cash Flow Health: 2/5 (Weak).

Relative Value: 2/5 (Overvalued).

Price Momentum: 2/5 (Weak).

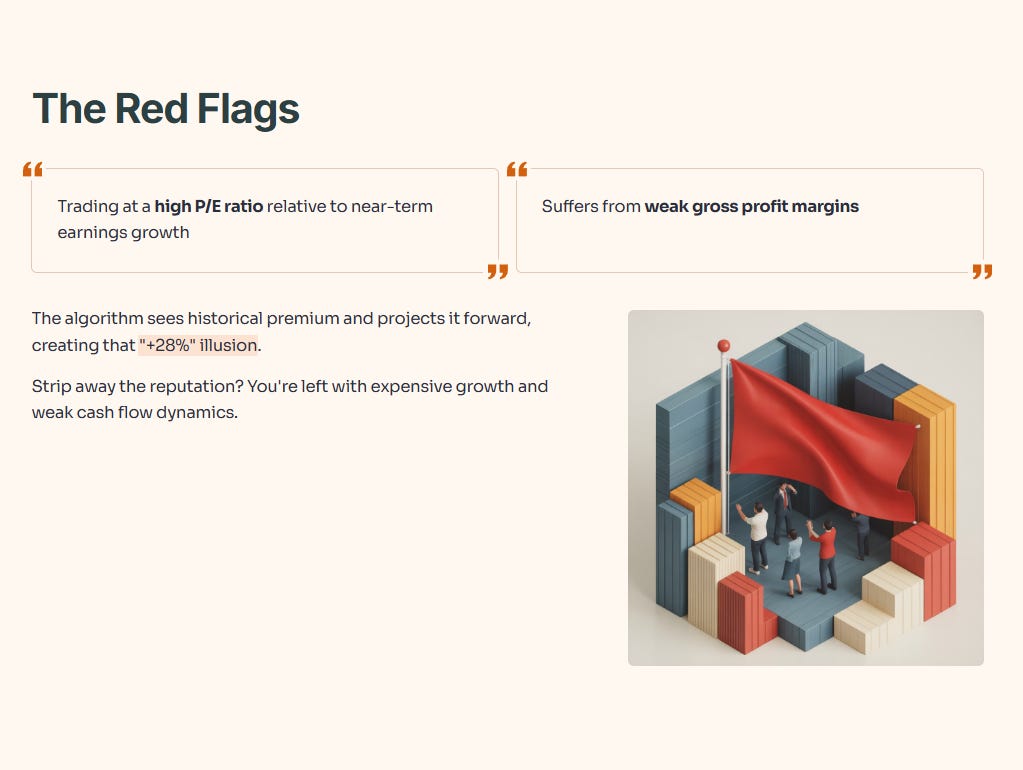

InvestingPro explicitly flags that BBCA is “Trading at a high P/E ratio relative to near-term earnings growth” and “Suffers from weak gross profit margins.”

The algorithm sees the historical premium and projects it forward, creating that “+28%” illusion. But if you strip away the reputation, you are left with a stock that is expensive relative to its growth and has weak cash flow dynamics.

Iggy’s Verdict