Fed Cut? Here’s Why I’m Still Holding DBS, OCBC, UOB (Singapore Investor’s Guide)

Worried about falling rates? Here’s why holding Singapore’s top banks beats panic selling—and how you can profit with discipline.

Editor’s Note: This post has been updated on October 19, 2025, to ensure it is fresh and accurate, and now includes our refined analysis on the strategy for holding SG banks (DBS, OCBC, UOB) through the Fed rate-cut cycle.

Singapore’s big banks tumbled after the Fed’s latest rate cut, leaving investors anxious and headlines swirling. But beneath the noise, I’m staying cool—and here’s my step-by-step playbook for holding DBS, OCBC, and UOB. For Singapore investors, disciplined balancing and calm execution beat knee-jerk decisions every time.

Fed rates are down, but I’m still holding DBS, OCBC, and UOB. Here’s why I’m not panicking, what I focus on instead, and practical rules SG investors can use to keep cool and make smarter moves.

The Story Fast: Fed Cuts & SG Bank Shock

The Fed just dropped interest rates last week. As expected, Singapore’s big banks—DBS, OCBC, and UOB—saw their share prices fall in response. Screens flashed red, dividend estimates got cut, and social media was full of “sell now” hot takes. If you felt worried, you’re not alone.

Singapore banks make a chunk of their profits from net interest margins (NIMs)—that’s the gap between what they earn from loans and what they pay on deposits. So, when US rates fall, people expect bank profits here to shrink too. That’s why prices fell.

But headline drops and panic stories only show part of the picture. Short-term price swings aren’t the same as long-term risk to the business model. What really matters is how these banks handle these shifts, and whether their core strengths are still solid even when rates are lower.

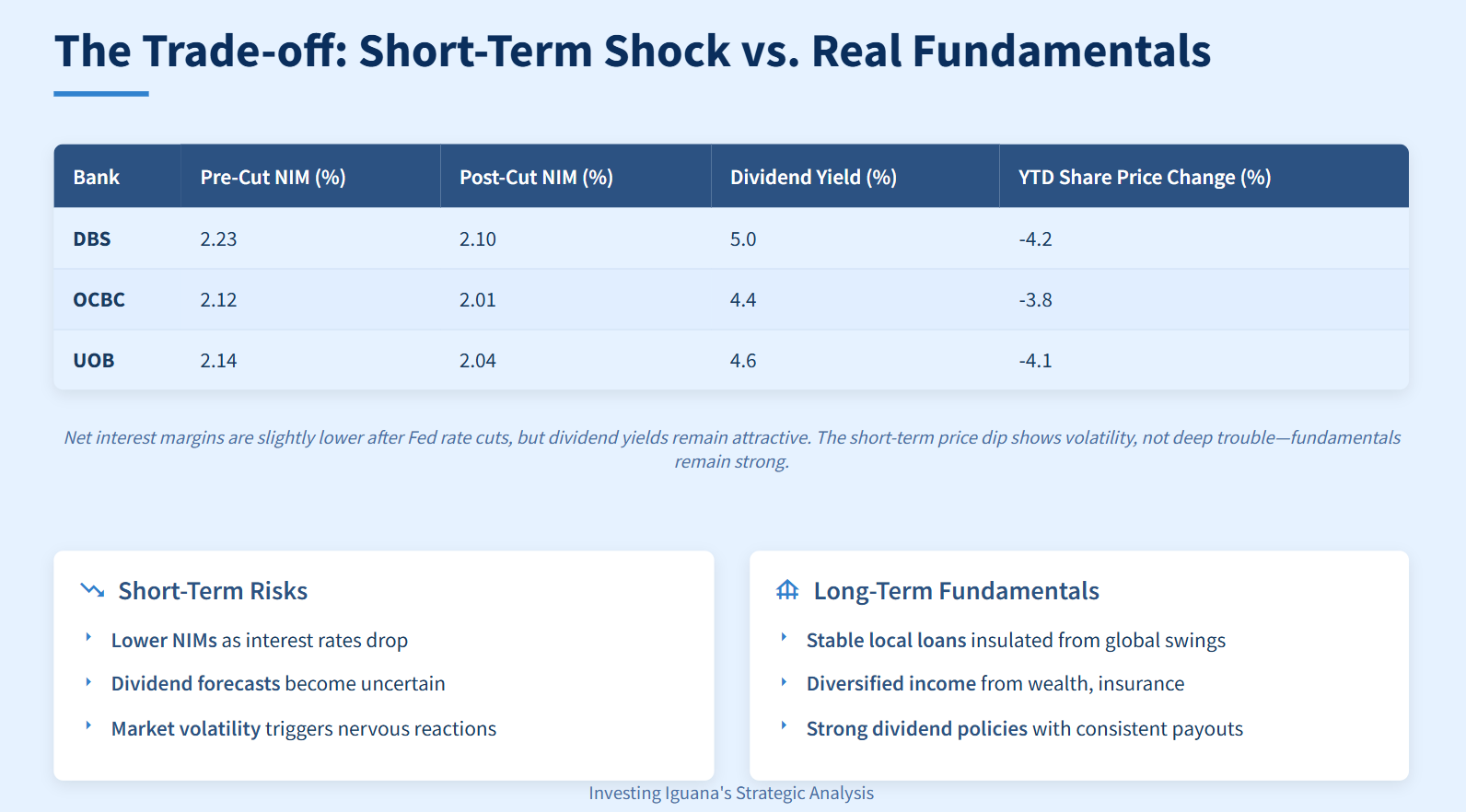

The Trade-off: Short-Term Shock vs. Real Fundamentals

Let’s look at what Fed rate cuts really mean for Singapore banks, both for the next few months and for the years ahead:

Short-Term Risks: As interest rates drop, the money banks earn from lending shrinks. Net interest margins (NIMs) get softer, which makes dividend forecasts wobble and causes more price swings on the market. This usually leads to nervous reactions and fast trades from investors chasing the news.

Long-Term Fundamentals: Even with lower rates, Singapore banks still have solid foundations. Their local loans stay steady, profits come from several streams (like wealth and insurance, not just lending), and their dividend policies remain strong. All three—DBS, OCBC, and UOB—hold up well compared to banks overseas, with safer assets and tighter regulations.

Why point all this out? Because headlines often make things sound worse than they are. Rate changes do hit the banks’ profits, but they don’t wreck the business model. The numbers show stability more than weakness.

Table 1: SG Banks—Interest Margin & Dividend Impact (2025 Estimate)

Caption:

Net interest margins are a bit lower after Fed rate cuts, but dividend yields are still attractive. The short-term price dip shows volatility, not a sign of deep trouble—fundamentals remain strong.

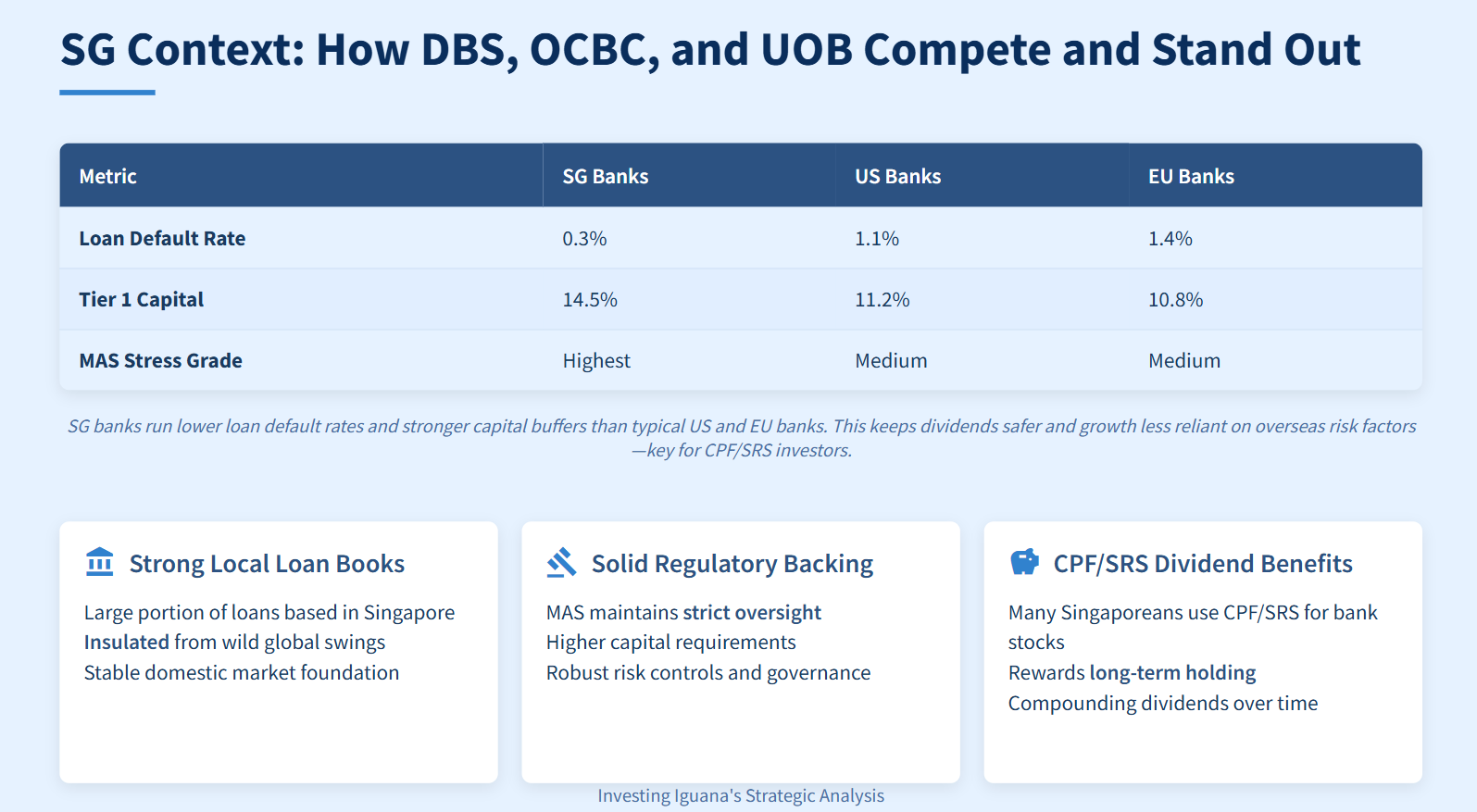

SG Context: How DBS, OCBC, and UOB Compete and Stand Out

Singapore’s three big banks—DBS, OCBC, and UOB—all share a stable local base and strong MAS oversight, but each takes a different route in growing and defending their business:

Strong Local Loan Books: A large chunk of their loans are based here in Singapore, insulated from wild global swings.

Solid Regulatory Backing: MAS keeps a tight leash—capital requirements are stricter and risk controls higher.

CPF/SRS Dividends: Many Singaporeans use CPF or SRS accounts to buy bank stocks. These platforms reward long-term holding, letting compounding dividends work over time.

DBS focuses on digital leadership and expands aggressively across Asia. DBS sets the pace in digital banking with innovative apps like digibank and fast-growing virtual wealth management services. Their regional reach—especially into Hong Kong, Greater China, and India—offers new opportunities, but also more exposure to shifts in international demand. DBS leads in consumer banking and is the top choice for tech-savvy, younger investors.

UOB drives expansion in Southeast Asia, tapping growth in Thailand, Vietnam, and Indonesia. UOB is the master of regional franchise building, often partnering with local businesses and launching new credit card programs. UOB’s core strategy has focused on enterprise and commercial markets, and their risk controls match MAS’s highest standards.

OCBC combines steady local lending with a focus on wealth and insurance. OCBC owns Great Eastern Life (insurance) and Bank of Singapore (private banking). Their edge is in serving high-net-worth clients and cross-selling insurance. OCBC shows strength in the SME sector and maintains robust growth in Malaysia and Indonesia. They offer balance—a strong dividend history and conservative lending strategy make them ideal for CPF/SRS investors seeking stability.

Table 2: SG vs. Overseas Banks—Risk Metrics

Caption:

SG banks run lower loan default rates and stronger capital buffers than typical US and EU banks. This keeps dividends safer and growth less reliant on overseas risk factors—key for CPF/SRS investors.

Competitive Positions

Mortgages: DBS often leads in home loans, offering lower rates and wider digital access.

Wealth Management: OCBC stands out with Bank of Singapore, serving the affluent and managing cross-border assets.

Insurance and Diversification: OCBC leverages Great Eastern for defensive growth.

SMEs & Regional Growth: UOB’s regional focus opens up new lending areas and fee streams.

Recent Initiatives That Help Offset NIM Pressure

DBS continues digital banking rollouts and expands its ecosystem through partnerships and acquisitions, integrating AI to cut costs and win younger clients.

OCBC strengthens private banking, enhances insurance cross-sell, and increases ESG-focused lending.

UOB builds its ASEAN footprint, investing in digital onboarding and new fintech tie-ups, making it easier for SMEs to access credit.

Bottom Line:

While MAS regulation and local loans provide stability, DBS, OCBC, and UOB each bolster their profits with unique growth moves—whether it’s tech and regional play (DBS), wealth and insurance (OCBC), or Southeast Asia expansion (UOB). These strategies help cushion lower net interest margins after Fed rate cuts, keeping SG banks resilient and competitive.

Iggy’s Playbook: My System for SG Banks

The real strategy isn’t reacting—it’s having a calm, repeatable system. Headlines change daily, but a proven system doesn’t. Here is my step-by-step playbook for managing SG bank positions with discipline.