First Resources Ltd (SGX:EB5): 3 Gems vs 3 Red Flags — Full Forensic Audit

A record 14.70-cent dividend meets a debt-fueled 40% gearing surge following a massive Indonesian land grab.

If you have been sitting on the sidelines watching palm oil stocks and wondering whether the commodity cycle has finally turned in your favour, the First Resources full-year 2025 results demand your attention. This is not a story about a sleepy plantation stock grinding out modest dividends. This is a story about a management team that made a billion-dollar acquisition bet, doubled its land bank overnight, and is now asking you to decide whether the reward justifies the new weight on the balance sheet.

For a Singaporean investor managing CPF or SRS funds, the forensic question is simple: does a 5.61 percent yield from a 40 percent geared upstream palm oil producer deserve a place in a retirement portfolio, or is this a yield trap dressed in a green and yellow plantation jersey? We are going to run the full audit today — three things working in your favour, three things that could unravel the thesis — and by the end, you will have a forensic verdict grounded in the numbers, not the narrative.

The CPF Special Account pays 4.0 percent with zero risk. That is your sanctuary benchmark. Everything we audit today gets measured against that floor first.

In This Article:

The Global Headline — The Storm

The Forensic Gap is widening by the hour

Iggy’s Insight

The Local Impact — The Wallet

You cannot optimize your way out of a physical supply collapse

The Data Proof — The Evidence

The forensic linchpin here is the 1.37 percent yield

Note on the Stress-Test Buffer

The Strategic Landscape

Forensic Portfolio Stress-Test Questions

The Singapore Investor Playbook

Part A — Shock Absorption

Part B — The Accumulator (aged 50–57)

Part C — The Drawdown Investor (aged 58–65)

Iggy’s Bottom Line

Iggy's Verdict

About Iggy & the Elite Investors

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

THE FINANCIAL HEALTH CHECKLIST

Before we get into the gems and the red flags, here is the forensic baseline.

Five passes, one fail. The fail is not a minor data point. A gearing jump from 8 percent to 40 percent in twelve months is a fundamental change in the risk profile of this business. The revenue and EBITDA growth are real and impressive, but they were purchased with leverage. The forensic audit exists precisely to separate growth that was earned from growth that was borrowed.

🦎 Iggy’s Insight: The Leveraged Sanctuary

First Resources has spent a decade building one of the most efficient upstream palm oil operations in Southeast Asia. The 2025 numbers confirm that operational excellence is intact — an 18.3 percent ROE and a 16.7 times interest coverage ratio are not accidents. But the ANJ acquisition has transformed the balance sheet from a fortress into what we call a Leveraged Sanctuary.

The yield of 5.61 percent is genuinely attractive for a Singaporean retirement investor, and the B50 mandate provides a structural demand floor that most commodity stocks cannot claim. The forensic question is not whether this is a good business. It clearly is. The question is whether the new debt load gives management enough room to manoeuvre if CPO prices soften by fifteen percent in the next eighteen months.

Forensic Punchline: A sanctuary with a mortgage is still a sanctuary — until the rate resets.

THE 3 GEMS — THE BULL CASE

Gem 1: The Inorganic Efficiency Multiplier — ANJ Integration

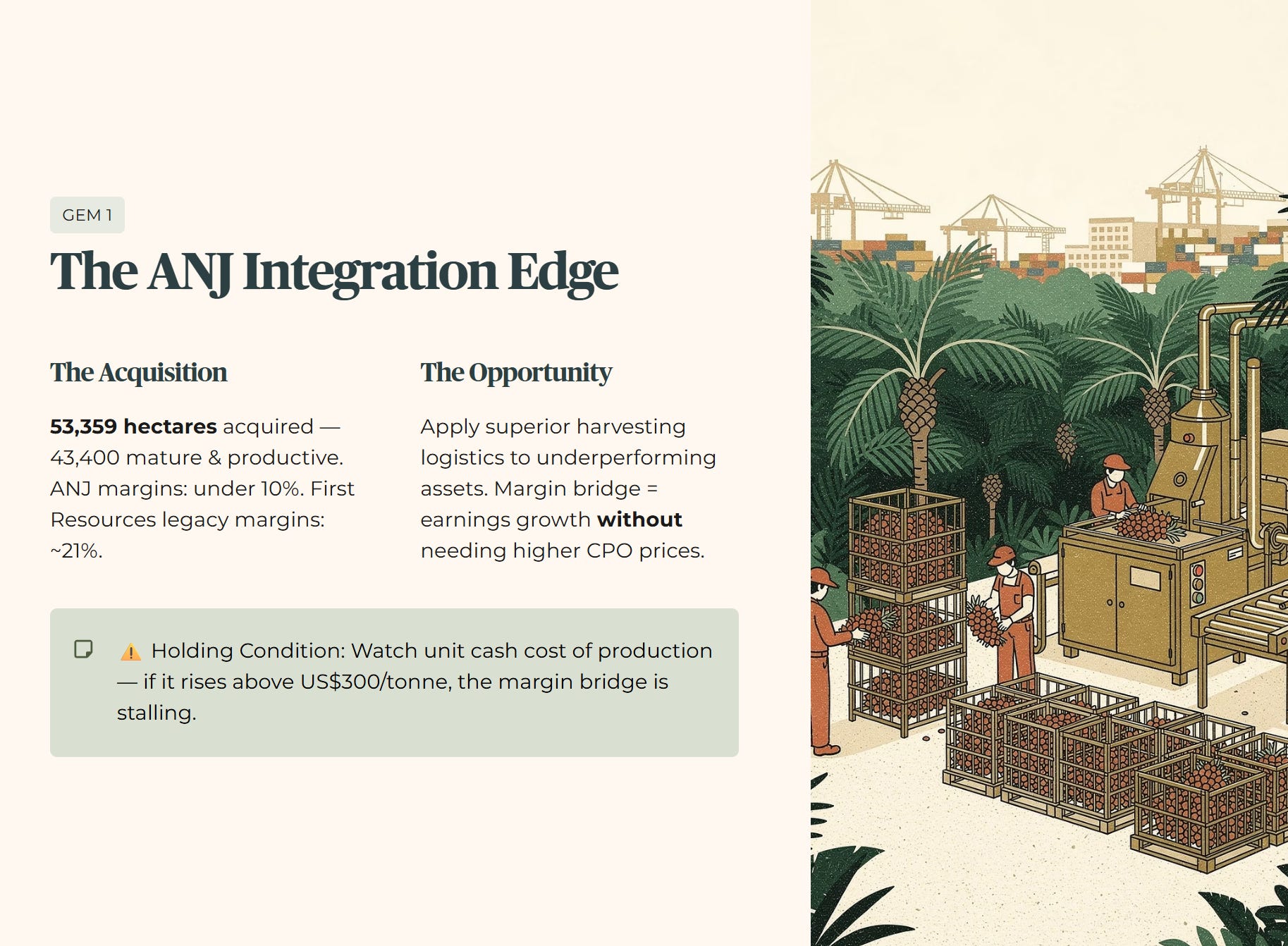

The acquisition of PT Austindo Nusantara Jaya in May 2025 is the primary engine behind the 59.9 percent revenue surge. But for a forensic auditor, the gem is not the headline acreage number. It is the management premium embedded in the deal.

First Resources has historically operated with a net profit margin of approximately 21 percent. ANJ was running at under 10 percent. By acquiring 53,359 hectares of plantation land — of which 43,400 hectares are mature and productive — and applying its superior harvesting logistics and fertiliser optimisation protocols, First Resources is effectively upgrading the yield of underperforming assets without needing higher crude palm oil prices to justify the return.

In kopitiam logic: they did not just buy a new stall. They bought a poorly run one, brought in their own recipe, and are now serving the best kopi on the block. If management can bridge even half the margin gap between legacy estates and the ANJ assets over the next two years, the earnings growth compounds without relying on a single favourable commodity move.

For an SRS investor in their fifties building toward drawdown, this is the kind of operational leverage that creates durable income rather than cyclical windfall. The revenue base is structurally larger, and the efficiency gains are in management’s hands rather than hostage to global commodity markets.

Holding Condition: This bull case only holds if integration OPEX does not exceed the productivity gains in the second half of 2026. Watch the unit cash cost of production — if it rises above US$300 per tonne, the margin bridge is stalling.

Gem 2: The B50 Biodiesel Safety Net

Indonesia’s transition to the B50 mandate — requiring a 50 percent palm oil blend in diesel fuel — in 2026 creates a structural demand floor for domestic CPO consumption that insulates First Resources from the volatility of European export markets and the growing regulatory pressure around deforestation certifications.

For an upstream-heavy producer operating entirely within the Indonesian supply chain, this is a material risk reduction. In a negative ten percent global export demand scenario — which is a realistic stress case given European regulatory headwinds — the increased domestic blending requirement absorbs the surplus and protects the US$614.9 million EBITDA baseline.

For a Singaporean managing a retirement portfolio, think of this as the FairPrice house brand equivalent of energy security. Palm oil at 50 percent blend is not a premium product for Indonesia. It is essential infrastructure for the world’s fourth most populous nation. Governments do not quietly discontinue essential infrastructure mandates. The B50 floor is not guaranteed forever, but it is structurally more durable than export demand, which is subject to the mood of Brussels and the quarterly targets of European FMCG companies.

Holding Condition: This bull case only holds if the Indonesian government maintains the B50 mandate without reducing the subsidy structure that makes blending economically viable for domestic distributors.

Gem 3: The Aggressive Payout Pivot — 60 Percent Policy

Management has officially revised its dividend policy to distribute up to 60 percent of underlying net profit, up from the previous 50 percent cap. In FY2025, the 14.70 Singapore cent payout represented a 50 percent payout ratio. At the new 60 percent ceiling, the same earnings base would have produced 17.6 cents per share.

This policy shift does something important for the forensic investor: it creates a yield shield. Even if earnings normalise modestly in 2026 due to integration costs or a softer CPO price, the higher payout percentage can sustain the distribution per unit at levels that keep the stock competitive against the 4.7 percent minimum yield hurdle.

For an SRS account holder in their late fifties, this is the equivalent of a landlord upgrading the terms of your tenancy — the same property, but with a formal commitment to return more of the cash flow to you rather than retaining it for speculative reinvestment. The 20 percent relative increase in payout efficiency means your income compounds faster without requiring the business to grow its top line.

Holding Condition: This bull case only holds if net gearing stays below 50 percent. If leverage creeps higher, lenders may impose dividend restrictions as a covenant condition, and the 60 percent policy becomes aspirational rather than executable.

🦎 Iggy’s Insight: The Dividend Trajectory

The dividend trajectory at First Resources tells a story that most investors miss when they look only at the headline yield. The jump from 9.80 cents to 14.70 cents in a single year is not a one-off commodity windfall distribution. It reflects a deliberate management decision to reset the payout framework at a higher structural level. When a management team formalises a higher payout ratio rather than simply declaring a special dividend, they are making a forward commitment to shareholders — not just celebrating a good year.

For a Singaporean investor who has watched too many REITs quietly trim their DPU while maintaining the same reassuring press release language, this kind of explicit policy commitment is worth paying attention to. The forensic question is whether the balance sheet can support the promise. That is exactly what the three red flags below are designed to test.

Forensic Punchline: A higher payout policy is only as good as the cash flow that backs it.

THE 3 RED FLAGS — THE BEAR CASE

Red Flag 1: The Leverage Leapfrog — Gearing Breach

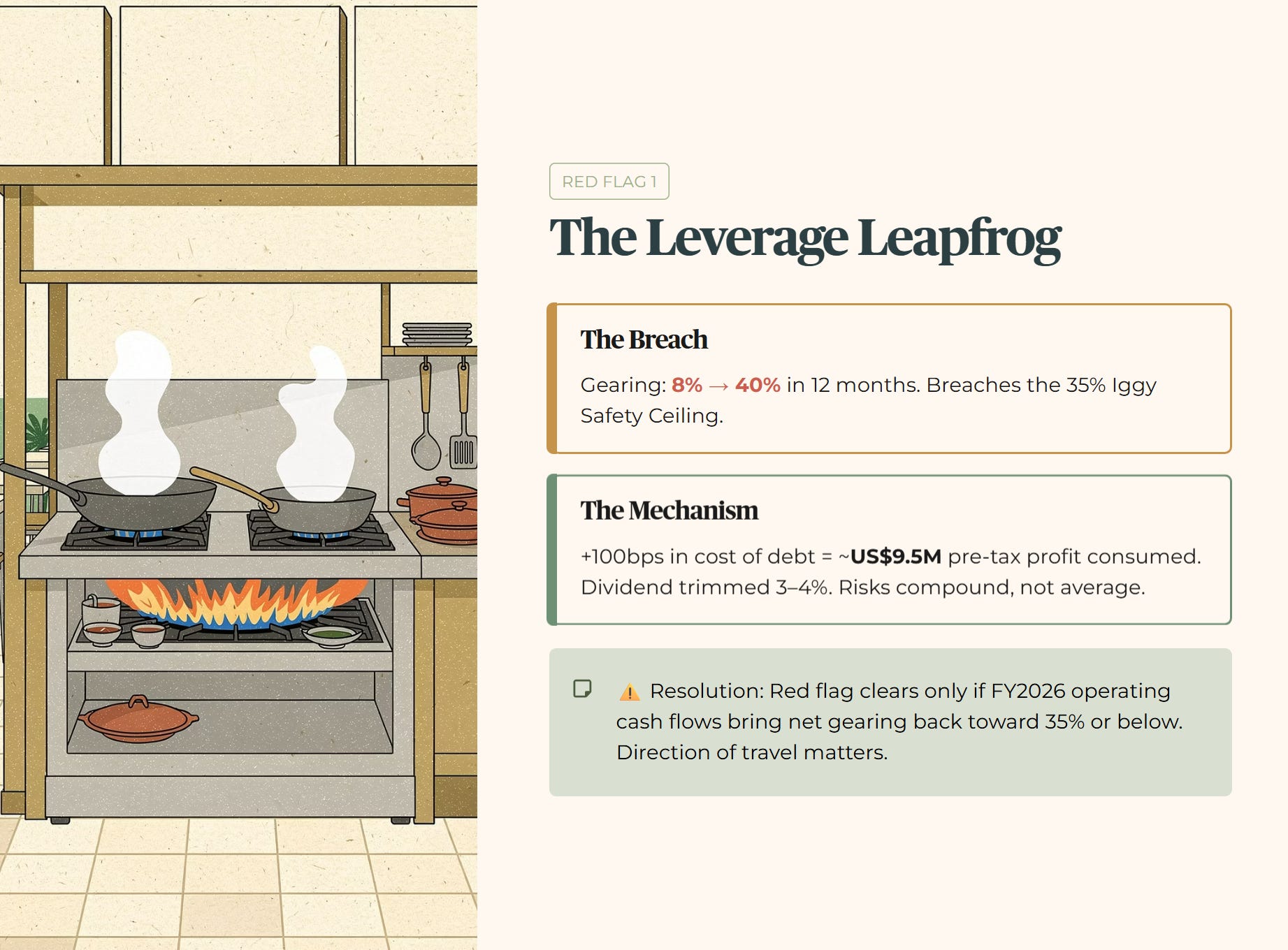

First Resources’ net gearing has jumped from 8 percent to 40 percent in twelve months. This is a forensic red flag because it breaches the 35 percent Iggy Safety Ceiling — the threshold below which we consider a balance sheet capable of absorbing a meaningful macro shock without forcing a dividend cut or an emergency equity raise.

The mechanism of risk is straightforward. If SORA remains at current levels [VERIFY] or climbs further, the interest expense on the enlarged debt load compounds against a net profit base that is already carrying higher integration costs. A 100 basis point rise in the average cost of debt would consume approximately US$9.5 million in pre-tax profit, trimming the dividend by three to four percent. That is a manageable haircut in isolation, but it arrives alongside potential CPO price softness and fertiliser cost pressure — and risks compound, not average.

Think of it like a hawker centre gas stove running at full flame. The output is impressive — the wok is hot, the orders are flying out, and the queue is long. But if the gas pressure spikes suddenly, the regulator blows, and the whole stall goes cold. The business did not become bad overnight. The infrastructure just could not handle the pressure at full load. First Resources is currently running its balance sheet at full flame.

Resolution Condition: This red flag clears only if the company uses FY2026 operating cash flows to bring net gearing back toward 35 percent or below. The direction of travel matters more than the absolute level — if gearing is declining, the thesis is intact.

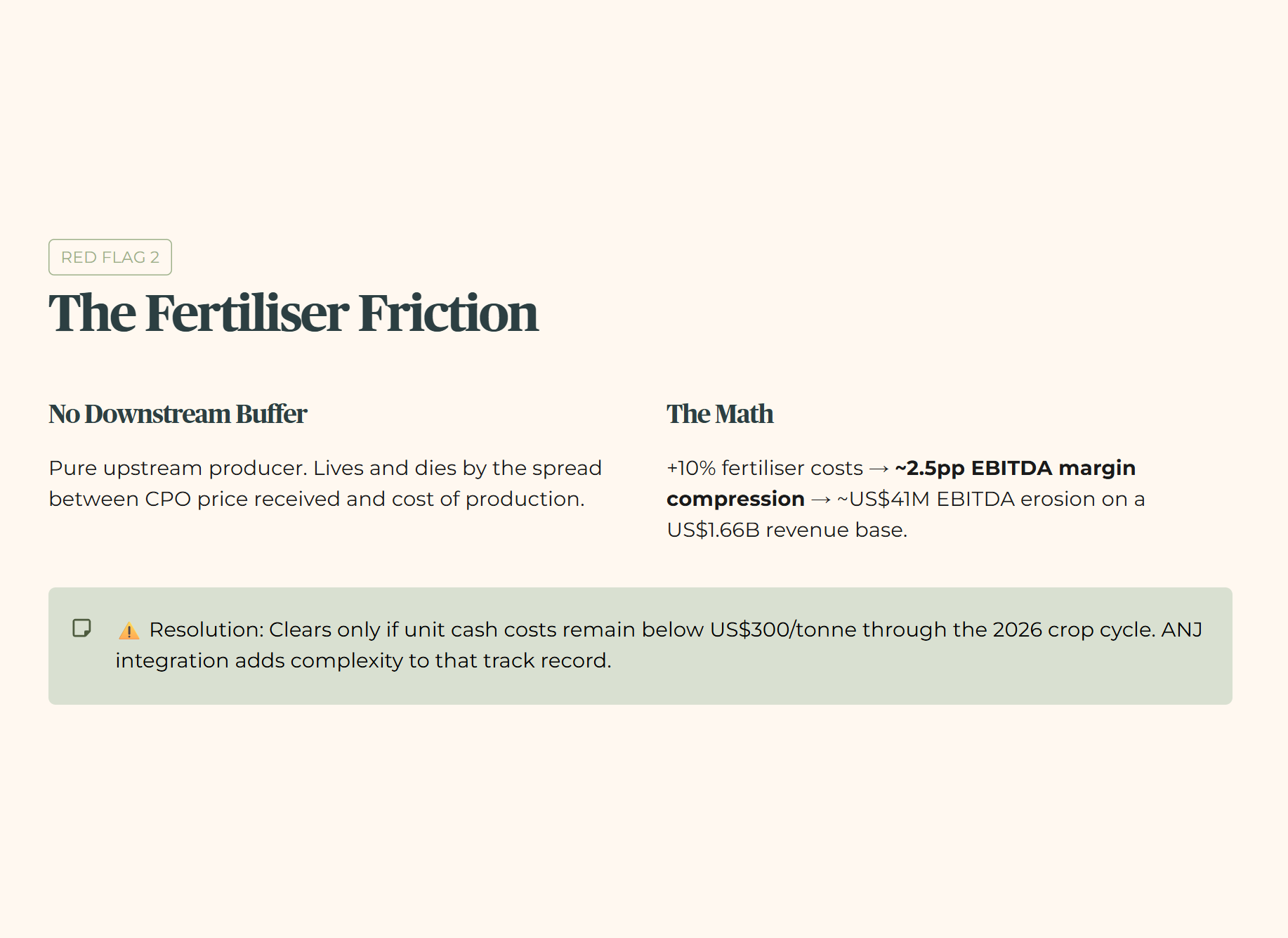

Red Flag 2: The Fertiliser Friction — Input Cost Squeeze

As a pure upstream producer, First Resources has no downstream buffer against input cost inflation. The business lives and dies by the spread between the price it receives for crude palm oil and the cost of producing it — and nitrogen-based fertilisers are the single largest controllable input cost in that equation.

Global supply chain disruptions in 2026 have kept fertiliser prices elevated. If costs increase by ten percent from current levels, the group’s EBITDA margin — currently a robust 37 percent — faces approximately a 2.5 percentage point compression. On a US$1.66 billion revenue base, that is roughly US$41 million in EBITDA erosion. The net profit impact flows through directly to the dividend calculation.

This is the wet market lobang gone wrong. You found a supplier selling fresh produce at a good price, built your whole stall around their supply, and then watched the wholesale cost double while your retail price stayed fixed by competition. For the investor, the US$353.9 million net profit figure is more fragile than it appears because OPEX is largely outside management’s control. The efficiency gains from the ANJ integration need to more than offset the input cost headwind — and that is not guaranteed.

Resolution Condition: This red flag clears only if unit cash costs of production remain below US$300 per tonne through the 2026 crop cycle. Management has historically delivered on cost discipline — but the ANJ integration adds complexity to that track record.

Leverage and fertiliser can hurt your dividend. The next risk can vaporise a decade of profits in one government notice — and most Singapore investors never see it coming.