Forget Hospitals. Buy These 3 SGX “Efficiency” Stocks Instead

The consensus trade is to buy Healthcare REITs. The contrarian trade is to short labor intensity and go long on “Medical Logistics.” (Note that this is my contrarian view for another perspective)

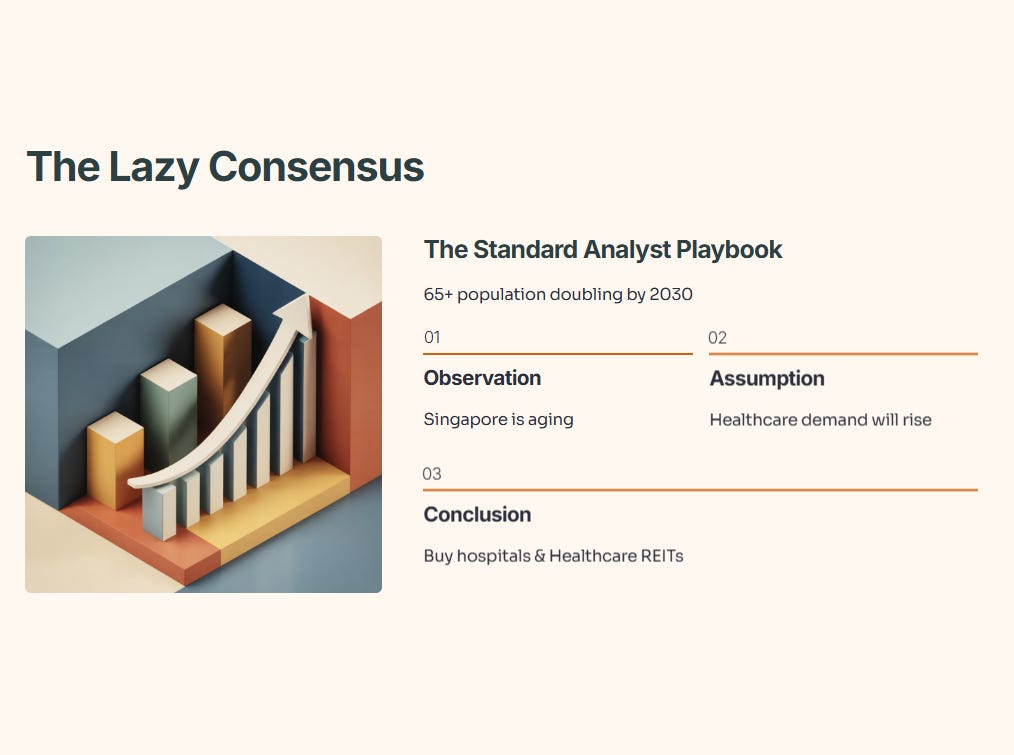

If you open any standard analyst report on Singapore’s demographic shift, you will see the same chart: a hockey stick graph showing the 65+ population doubling by 2030.

The accompanying advice is almost always a variation of the same “Lazy Consensus”:

“Singapore is aging. Demand for healthcare will rise. Therefore, buy hospitals (IHH, Raffles Medical) and Healthcare REITs (Parkway Life, First REIT).”

On the surface, this is logical. But in investing, the obvious trade is rarely the profitable one. The market has already priced in the demand. What the market has mispriced is the cost of supply.

Today, we are going to dissect why the “Aging = Buy Real Estate” thesis is flawed, and why the real money in Singapore’s silver economy will be made in the unsexy world of logistics, specialized manufacturing, and automation.

In This Article:

• The Macro Disconnect: The Dependency Ratio

• The Bear Case for Healthcare REITs

• The “Japanification” of the SGX

• The Alpha Watchlist: The “Picks and Shovels”

• 1. The MedTech Manufacturer: ???

• 2. The Mobility Play: ???

• 3. The Efficiency Play: ???

• Strategic Conclusion: How to Position

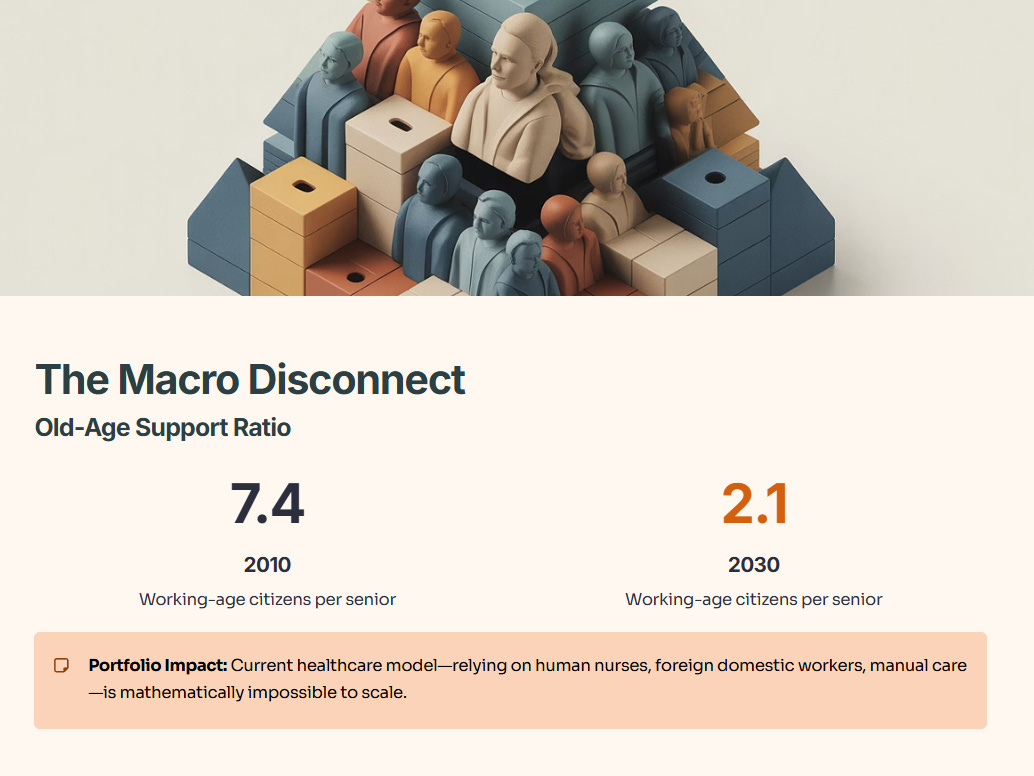

The Macro Disconnect: The Dependency Ratio

We need to look past the headline number (900,000 seniors) and look at the Old-Age Support Ratio.

In 2010, we had roughly 7.4 working-age citizens for every senior. By 2030, that number drops to 2.1.

Why does this matter for your portfolio? Because the current Singaporean healthcare model—which relies heavily on human nurses, foreign domestic workers, and manual care—is mathematically impossible to scale.

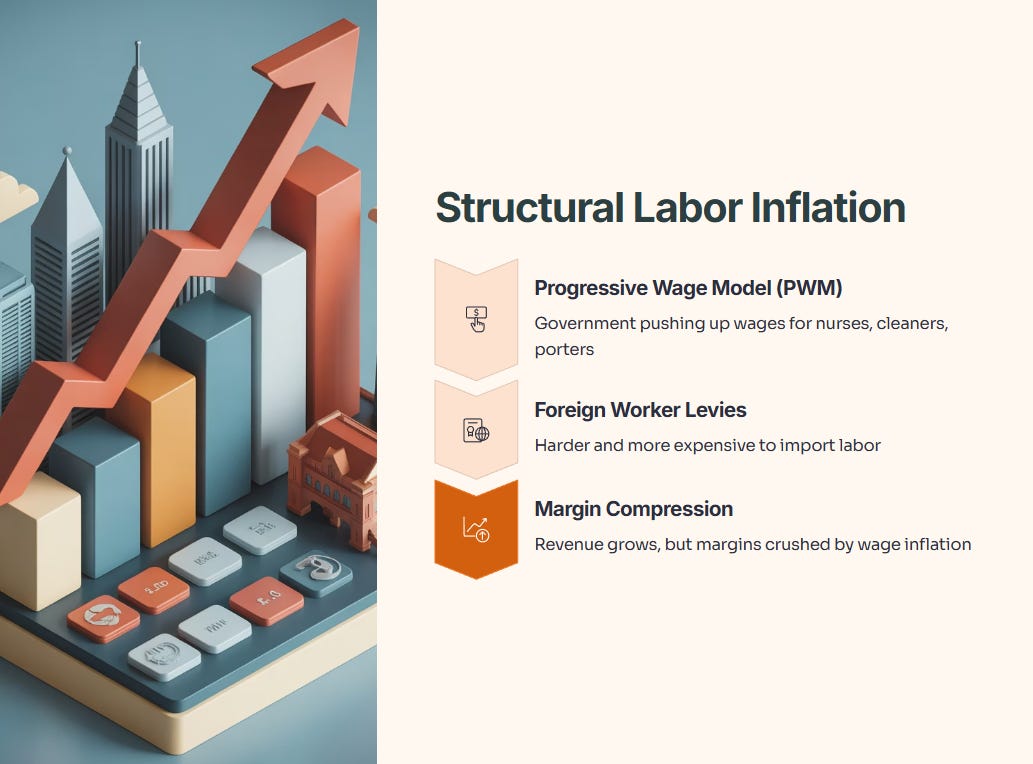

We are entering an era of structural labor inflation.

The Progressive Wage Model (PWM): Singapore’s government is actively pushing up wages for lower-income workers (nurses, cleaners, porters).

Foreign Worker Levies: It is getting harder and more expensive to import labor.

If you invest in a business that sells “human care” (like a nursing home operator), your revenue might grow, but your margins are going to get crushed by wage inflation.

The Bear Case for Healthcare REITs

Let’s look at the darling of the SGX: Parkway Life REIT (PLife).

I like PLife. I also own PLife. It’s a well-managed defensive asset. But is it a growth play for the next decade? I’m skeptical.

The “REIT” thesis assumes that because demand for beds is high, rental income will rise. But there is a ceiling. Healthcare operators (the tenants) operate on thin margins. If labor costs spike by 20% (due to the labor shortage I mentioned above), the operator cannot simply pay 20% more rent.

The Risk:

Tenant Solvency: In a labor-constrained environment, the operator takes the hit. If the operator struggles, the REIT’s upside is capped.

Cap Rate Compression: With interest rates higher for longer, the yield spread on stable REITs has narrowed. You are paying a premium valuation for a bond-like proxy.

Iggy’s Take: REITs act more like a safety net than a vehicle for growing wealth, especially in Singapore’s aging economy. While they can offer stable, defensive returns, the demographic shift—more seniors and fewer working-age people—means rising labor costs and tighter margins for healthcare operators, who are often the tenants of Healthcare REITs. These operators may see higher demand, but also face significant cost pressures from wage inflation and worker shortages, so they’re unlikely to afford much higher rents. As a result, REITs tied to healthcare real estate become more of a capital preservation play in this context—good for not losing money, but unlikely to deliver outsized gains from this demographic trend. If you want real growth, you need to look beyond just owning the buildings.

The “Japanification” of the SGX

To see where the alpha is, look at Japan. Japan is 20 years ahead of us.

When their labor force collapsed, the companies that skyrocketed weren’t just the nursing homes. They were the companies that substituted capital for labor.

Robotics: Automating patient transport.

Remote Monitoring: keeping patients out of expensive hospitals.

Centralized Logistics: Industrializing food and medicine delivery.

The winning formula for Singapore 2025-2035 is: Long Technology, Short Labor.

The Alpha Watchlist: The “Picks and Shovels”

If we reject the “Buy Buildings” thesis, we must embrace the “Buy Efficiency” thesis. Here are three specific SGX-listed examples of how to express this view.