Foundation Healthcare IPO: A S$1B Giant With Zero Dividends | EP1670

In a market famous for its love of dividends, Foundation Healthcare is asking investors to ignore the yield and bet on a massive billion-dollar growth story. With zero payouts planned for two years...

By Angela, Market Correspondent, The Investing Iguana

A note before we begin: this article is written by Angela, The Investing Iguana’s market correspondent. My role is to report on analyst research, earnings results, and market developments as they are, without applying Iggy’s forensic filters, zone verdicts, or yield hurdle judgments. If you are looking for Iggy’s forensic audit on this stock, that is a separate piece and will be linked where available. What you are reading here is a faithful summary of what the market and its analysts are saying, nothing more and nothing less.

In a market famous for its love of dividends, Foundation Healthcare is asking investors to ignore the yield and bet on a massive billion-dollar growth story. With zero payouts planned for two years, can this Temasek-backed medical roll-up justify its premium valuation?

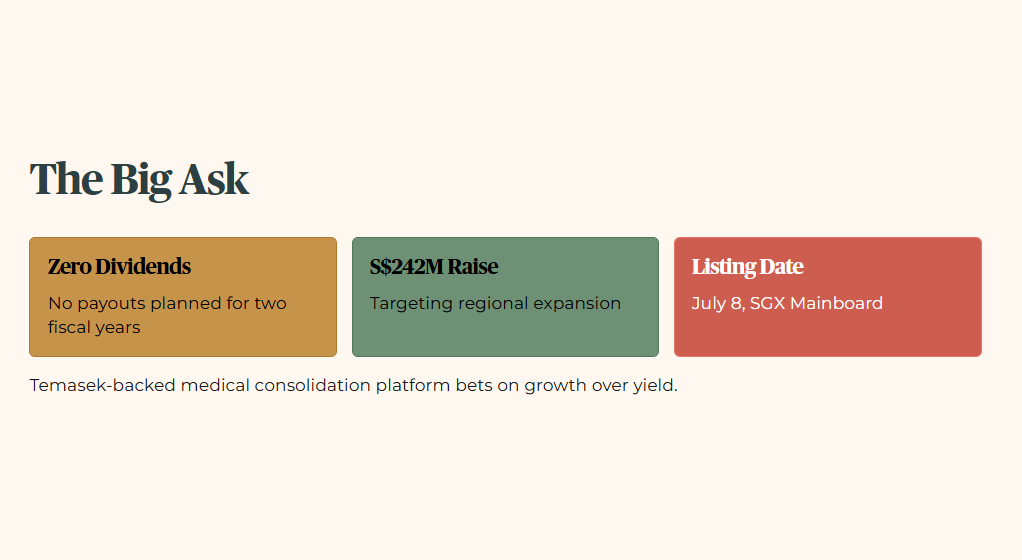

The Temasek-backed medical consolidation platform plans to raise up to 242 million Singapore dollars to fund its regional expansion, targeting a listing on July 8.

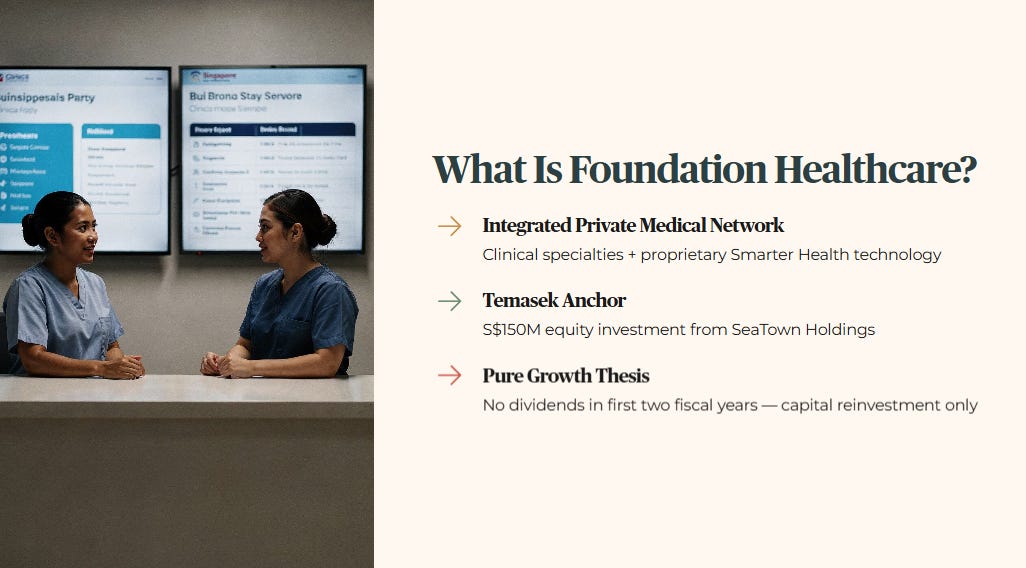

Foundation Healthcare Holdings has officially lodged its preliminary prospectus to list on the Mainboard of the Singapore Exchange. The group operates as an integrated private medical network, combining clinical specialties with a proprietary technology infrastructure known as Smarter Health. By consolidating independent specialists into a single corporate platform, the company aims to streamline insurance pre-authorisations, improve administrative efficiency, and drive clinical cross-referrals across its network.

The strategic foundation of the platform was anchored by a 150 million Singapore dollar equity investment from SeaTown Holdings, the alternative private markets investment management arm of Temasek Holdings. This upcoming offering introduces a pure capital growth thesis to the local market, as the company has explicitly stated it will not distribute dividends in its first two fiscal years.

This article will cover the financial trajectory, the structure of the offering, the institutional cornerstone support, the implied valuation metrics, and the key prospectus risks as detailed in the preliminary filings.

Platform Infrastructure And Clinical Consolidation

Financial Trajectory And Pro Forma Adjustments

Offering Mechanics And Cornerstone Allocations

Implied Valuation And Market Comparisons

Prospectus Risk Factors And Governance

Market Summary

Platform Infrastructure And Clinical Consolidation

Foundation Healthcare Holdings was incorporated on August 8, 2022, and launched its operating platform in March 2023. The company is built as a technology-enabled consolidation vehicle for the fragmented private medical sector in Singapore and the broader region. The foundation of this strategy is the full integration of Smarter Health, a proprietary healthtech infrastructure business the group acquired in June 2023. This technology layer facilitates digital data exchange, standardizes pre-authorisation protocols, and optimizes coordination between clinical practices and major insurance payors. By wrapping this proprietary infrastructure around acquired clinical specialties, the group aims to establish an efficient value-based care ecosystem that reduces operational waste.

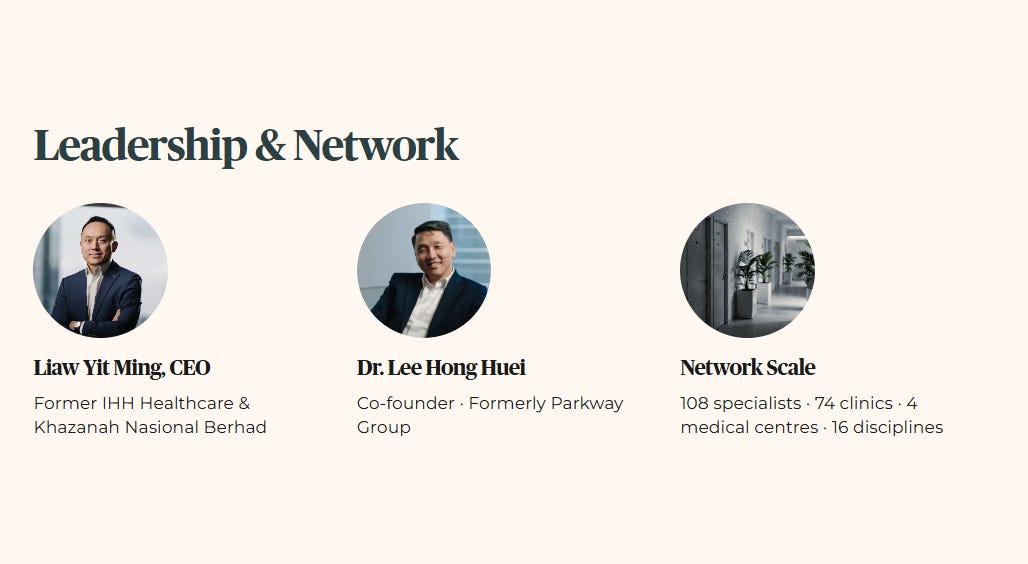

The executive leadership team is led by Chief Executive Officer Liaw Yit Ming, a veteran executive with prior leadership experience at IHH Healthcare and Malaysia’s sovereign wealth fund, Khazanah Nasional Berhad. He is joined by co-founder and senior director Dr. Lee Hong Huei, formerly of Parkway Group. Together, the management team possesses a direct operational blueprint tailored to managing large-scale healthcare roll-ups in Southeast Asia. The company’s physical network expanded from an initial base of over fifty specialists in early 2023 to one hundred and eight medical specialists by March 2026. The network now encompasses seventy-four clinics and four specialized medical centres operating across sixteen distinct medical disciplines.

Financial Trajectory And Pro Forma Adjustments

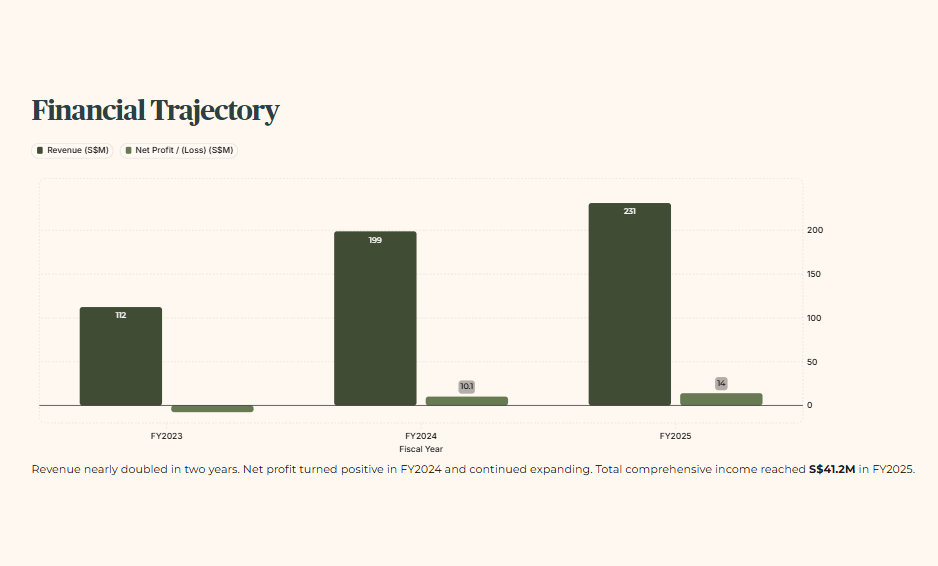

The historical financial trajectory of the group reflects the rapid expansion of its clinical footprint and the ongoing integration of newly acquired practices over its three-year operating history. The inorganic expansion translated into substantial top-line growth. Historical revenues rose from 112.4 million Singapore dollars in the fiscal year 2023 to 198.9 million Singapore dollars in the fiscal year 2024. Revenue growth continued into the next period, reaching 231.2 million Singapore dollars in the fiscal year 2025. Profitability metrics highlight a notable transition from early start-up losses to an operational scale advantage. Net profit attributable to the equity owners of the company transitioned from a net loss of 7.66 million Singapore dollars in the fiscal year 2023 to a net profit of 10.12 million Singapore dollars in the fiscal year 2024, before expanding to 14.0 million Singapore dollars in the fiscal year 2025. Under a broader measurement, the group’s profit and total comprehensive income reached 41.2 million Singapore dollars in the fiscal year 2025.

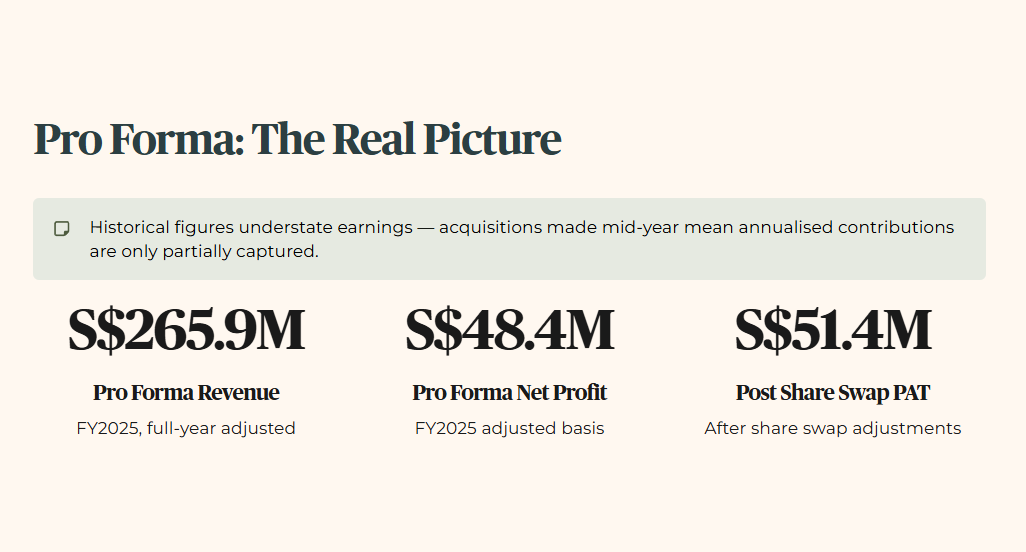

Because the clinical network has grown primarily through acquisitions executed mid-year, the historical financial figures do not capture the annualized earning power of the consolidated group. The draft prospectus details pro forma adjusted financial figures for the fiscal year ended December 31, 2025, to present a normalized operational view for prospective investors. On this pro forma adjusted basis, which accounts for the full-year contribution of all clinics acquired up to the prospectus date, the group’s revenue is reported at 265.9 million Singapore dollars. Pro forma net profit rises to 48.4 million Singapore dollars on this adjusted basis, while certain share swap adjustments position the pro forma profit after tax at 51.4 million Singapore dollars.

Offering Mechanics And Cornerstone Allocations

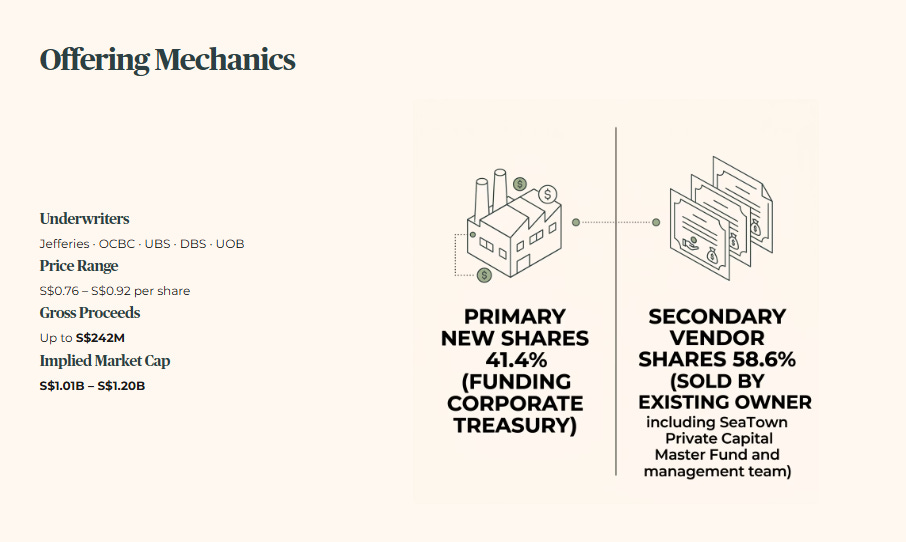

The transaction is structured to achieve a primary listing on the Mainboard of the Singapore Exchange, with the official debut targeted for July 8, 2026. Managed by a joint underwriting syndicate comprising Jefferies Singapore, OCBC Bank, UBS, DBS Bank, and United Overseas Bank, the transaction is structured to raise up to 242 million Singapore dollars in gross proceeds.

The offering plans to price shares between 0.76 Singapore dollars and 0.92 Singapore dollars apiece. This pricing range gives the company an implied listing market capitalization of approximately 1.01 billion Singapore dollars to 1.20 billion Singapore dollars. The capital structure of the offering indicates a significant exit of secondary capital by existing stakeholders. New primary shares represent only 41.4 percent of the total offering, which will directly fund the corporate treasury. The remaining 58.6 percent consists of existing vendor shares sold by current owners, including the SeaTown Private Capital Master Fund alongside members of the executive management team.

The transaction is heavily anchored by 118 million Singapore dollars in committed cornerstone capital, representing 48.8 percent of the total target gross proceeds. This institutional demand spans multiple tiers of global asset management, sovereign-linked capital, and specialized tech-focused private equity. The World Bank’s International Finance Corporation leads the cornerstone tranche, providing substantial institutional validation for the group’s healthcare delivery model in Southeast Asia.

This development-finance backing is complemented by global asset managers including Manulife Investment Management, RBC Global Asset Management, and UBS. Local and regional fund managers feature prominently as well, including Lion Global Investors, Amova Asset Management Asia, and Orbit Master Holdings. The global institutional tranche represents 117 million Singapore dollars, or 48.3 percent of the deal. The Singapore public retail tranche is allocated just 7 million Singapore dollars, representing 2.9 percent of the total offering.

🟠 Angela’s Observation

The decision to allocate just 7 million Singapore dollars to the public retail tranche creates a highly concentrated institutional registry. While locking up nearly half the deal with cornerstone investors helps insulate the stock from immediate post-listing selling pressure, it raises questions about long-term price discovery and secondary market liquidity on the Singapore Exchange once trading commences.

The Red Flags Were Always There

The Crash Wasn’t a Surprise. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided before the opening bell — not after the damage is done. The red flags are always there. The question is whether you had the forensic framework to read them in time.

Iggy’s Elite Investors didn’t chase the headline yield. They had the full forensic breakdown — the gearing ratios, the occupancy gaps, the debt overhang — before the market opened and before the price moved. Zero-day reports, the complete “Red Zone” watchlist, and institutional-grade cheatsheets that flag the landmines disguised as opportunities.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

The next section runs the full PE and yield comparison against Raffles Medical and IHH Healthcare, where the pro forma uplift and zero-dividend guidance start to collide with Singapore’s yield-driven forensic standard.