Frasers Centrepoint Trust: UOB Kay Hian's BUY Call Ignores a Two-Gate Balance Sheet Problem

The malls are 99.8% occupied and the yield clears our hurdle. The balance sheet still fails on two separate counts.

The Broker Buy Call with a S$2.6 Billion Debt Reality

Institutional analysts look at the property market through the lens of transaction premiums and portfolio optimisation. When UOB Kay Hian reiterated its BUY rating on Frasers Centrepoint Trust with a S$2.70 price target, the headline celebrated the S$467 million divestment of White Sands at an 8.4% premium to valuation.

But for a retail investor building a reliable retirement income stream, the real story is never the exit premium on a single asset. The real story is the structural debt load left behind on the balance sheet.

When you scale back the corporate narrative, you find a capital structure that requires major deleveraging to meet basic safety standards. A premium divestment is a fine operational milestone, but it does not automatically turn a highly leveraged balance sheet into a retirement sanctuary.

Section 1 — The Analyst’s Case

Section 2 — Iggy’s Forensic Screen

Financial Health Checklist

How Iggy Rates Every Stock

Section 3 — The Dividend Trajectory

Section 4 — The Forensic Gap

Iggy’s Insight Box 1

Section 5 — What To Watch Next

Iggy’s Insight Box 2

Closing — The Forensic Stance

Section 1 — The Analyst’s Case

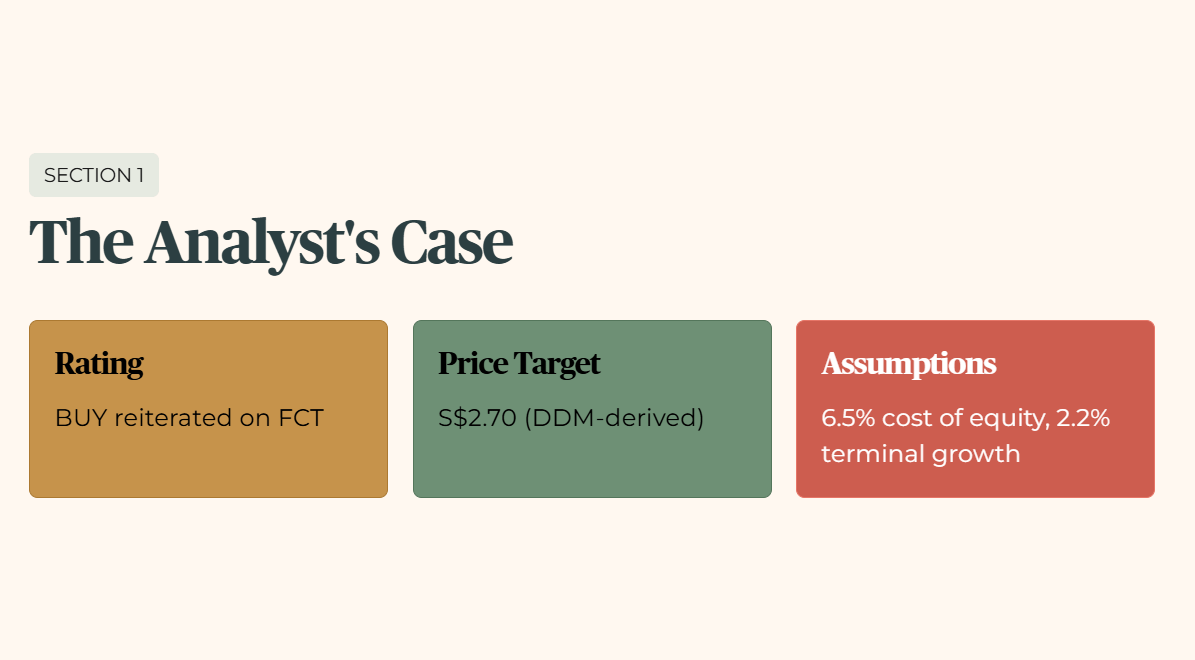

UOB Kay Hian has reiterated its BUY rating on Frasers Centrepoint Trust (SGX: J69U) with a Dividend Discount Model derived price target of S$2.70. This valuation is built on a 6.5% cost of equity assumption and a 2.2% terminal growth rate.

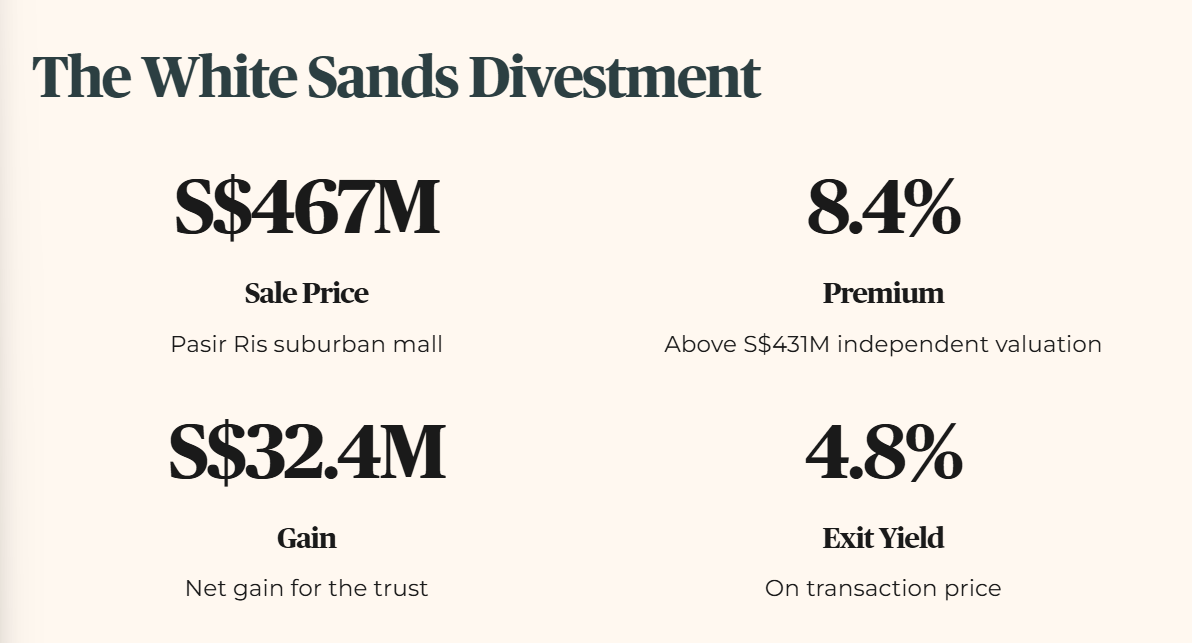

The core of the analyst’s thesis rests on the structural optimisation of the portfolio. FCT agreed to divest White Sands, its smallest suburban mall located in Pasir Ris, for S$467 million. The analyst house highlights that this transaction was executed at an 8.4% premium to an independent valuation of S$431 million, reflecting an exit yield of 4.8% and netting a gain of S$32.4 million for the trust.

To account for the loss of income from this asset, which contributed S$11.1 million in net property income (NPI, the actual rental income a property generates after operating costs) during the first half of financial year 2026, or roughly 6.9% of the group’s total NPI, the analyst house trimmed its financial year 2027 Distribution Per Unit forecast, according to the broker’s own report. However, they frame this divestment as a positive balance sheet strengthening move that allows management to sharpen its focus on its largest dominant suburban retail assets.

The primary catalysts cited in the report to drive the stock toward the S$2.70 target include rising shopper traffic, healthy tenant sales, local household income growth, and active asset enhancement initiatives underway at Hougang Mall, Nex, and Causeway Point.

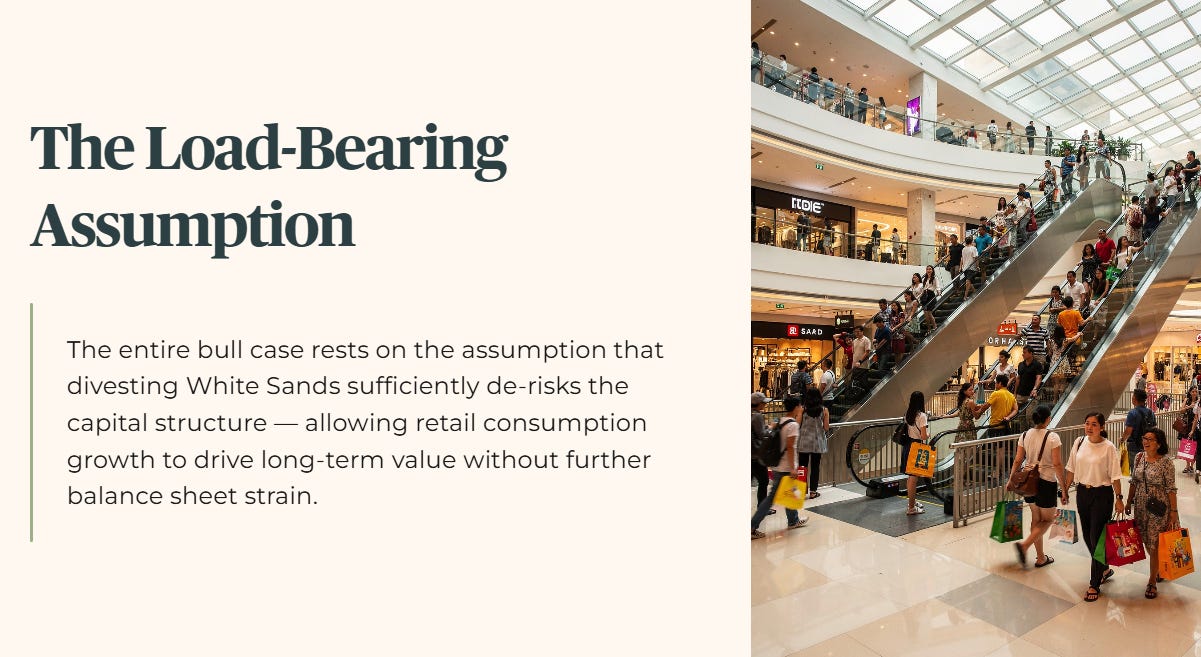

THE LOAD-BEARING ASSUMPTION: The analyst’s entire bull case rests on the assumption that divesting White Sands sufficiently de-risks the capital structure, allowing retail consumption growth and asset enhancements to drive long-term value without further balance sheet strain.

Section 2 — Iggy’s Forensic Screen

Our forensic framework does not evaluate retail momentum or asset aesthetics. We screen the hard numbers on the balance sheet to see if the capital structure protects a retiree’s principal. Applying our five-layer audit to the verified data reveals two independent structural fractures.

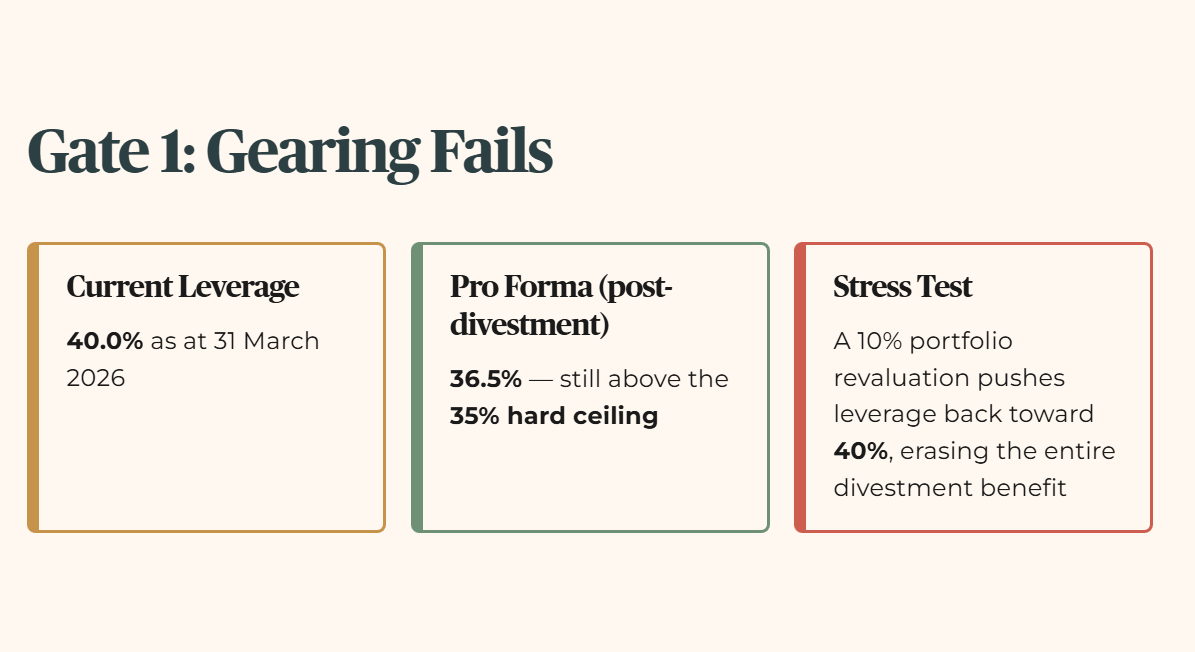

First, let us examine raw leverage. FCT’s reported aggregate leverage stands at 40.0% as of 31 March 2026. Management has guided that after the White Sands transaction completes around 30 September 2026 and the net proceeds are applied to debt repayment, pro forma leverage will compress to 36.5%.

While the trajectory is moving downward, a pro forma gearing (the proportion of the trust’s assets funded by debt) of 36.5% still fails our 35% hard gate ceiling. A stress test simulating a modest 10% downward revaluation of the remaining retail portfolio would instantly push pro forma leverage back toward the 40% mark, erasing the entire benefit of the divestment. For a fifty-five-year-old investor, this leaves little safety buffer against property market fluctuations.

Second, the debt service capacity is genuinely strained. The trust’s own reported adjusted interest coverage ratio (ICR, how many times over a company’s earnings can cover its interest payments) sits at 3.59 times as of 31 March 2026, per FCT’s own results presentation. This is a direct failure of our 4x safety floor.

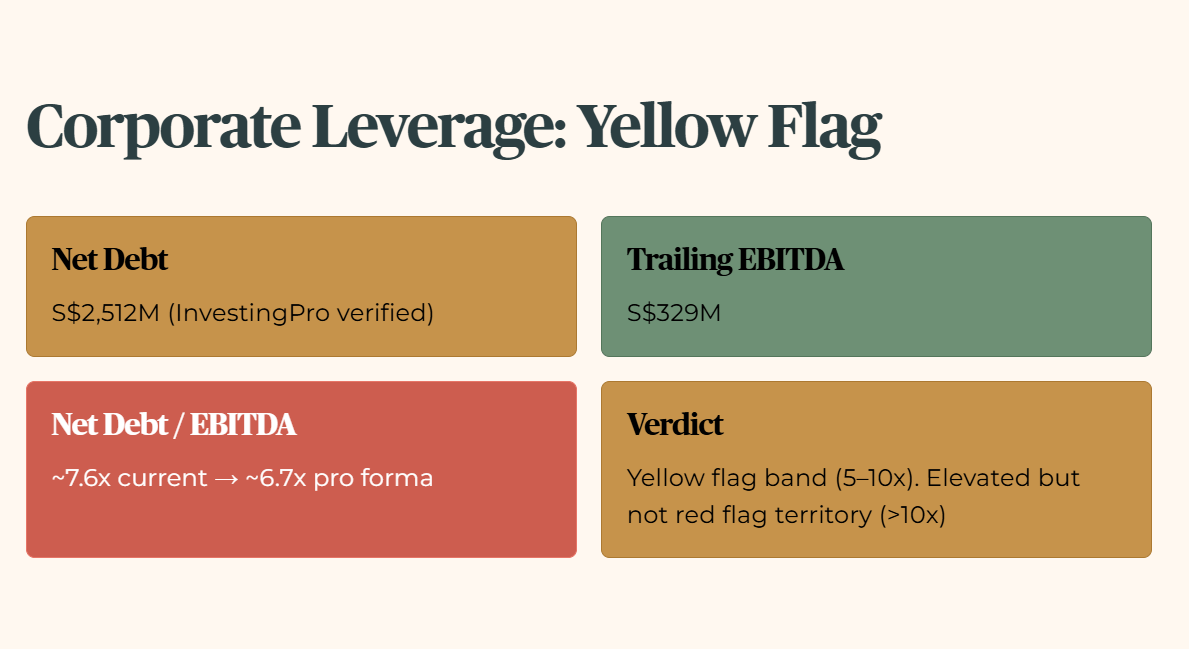

Third, our corporate leverage metric, Net Debt to EBITDA, sits at approximately 7.6 times on current InvestingPro-verified figures (net debt of S$2,512 million against trailing twelve-month EBITDA of S$329 million). Factoring in the post-divestment pro forma reduction in both net debt and EBITDA, the pro forma ratio moves to approximately 6.7 times. Both readings sit inside our 5 to 10 times yellow flag band, meaningfully elevated and worth monitoring, but not the structural red flag territory that would trigger above 10 times.

The property assets themselves are performing exceptionally well, with portfolio-wide committed occupancy at 99.8% as at 31 March 2026, confirmed directly against FCT’s own results presentation. But strong operational occupancy cannot compensate for an over-leveraged capital structure.

Before assigning the final zone verdict, we confirm the soft flag assessment. FCT shows zero weighted soft flags. Trailing revenue and net income are both growing year on year, with trailing twelve-month revenue at approximately S$499 million and net income at S$227 million, per InvestingPro. Leverage is trending downward rather than upward, and the current market price of S$2.24 trades at a clear forensic gap below the InvestingPro average fair value of S$2.54.

With a soft flag count of zero, the final verdict is dictated entirely by the two independent hard gate failures on gearing and interest coverage.

The entire verdict now turns on reconciling a yield that clears our 4.7% hurdle with a balance sheet that fails both its 35% gearing ceiling and 4.0x interest coverage floor at the same time.