Geography Built DBS and SIA. Now Thailand Wants to Redraw the Map

The Forensic Audit of Singapore’s Geographic Moat — and What It Means for Your Retirement Portfolio

Right now, the Straits Times Index is flirting with the psychological resistance level of the 5,000-point milestone. You tap open your brokerage app while riding the MRT, and the screen is a comforting sea of green. Your dividend payouts are flowing reliably into your bank account. The chatter at the neighbourhood kopitiam is optimistic, filled with uncles confidently discussing their banking stocks. Everyone feels like a financial genius when the tide is rising. And on the surface, that makes perfect sense. The technical charts look beautiful. The local banking sector is practically printing cash.

But here is the uncomfortable truth that nobody wants to discuss over their morning kopi-o. While we are celebrating these record highs, the actual tectonic plates of ASEAN geography are shifting. The fundamental map underneath our wealth is being aggressively redrawn.

In This Article:

The Malacca Strait Moat

The Thailand Land Bridge

The SGX Forensic Implications

The Geographic-Regulatory Moat Audit

The Wallet Impact

InvestingPro Reality Check

Iggy's Verdict

About Iggy & the Elite Investors

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

Singapore’s entire economic miracle is not built on thin air, nor is it purely the result of exceptional governance. It is built entirely on saltwater. We sit at the absolute perfect geographical chokepoint of global trade. The Malacca Strait is the primary artery that pumps lifeblood into the heart of the SGX. But what happens to your portfolio when your northern neighbour decides to build a bypass surgery?

For Iggy’s Elite Investors who receive zero-day intel, you already know that we do not trade on political headlines. We trade on forensic reality. And the reality is that Thailand is pushing a massive, multi-billion-dollar infrastructure project designed specifically to bypass the Port of Singapore.

Iggy’s Insight Let us be very clear about how economic empires are actually built. We like to pat ourselves on the back, looking at our pristine HDB estates and assuming our wealth comes purely from superior governance. But Singapore is essentially a toll booth sitting on the most lucrative maritime highway in human history. Geography is our oldest and most ruthless competitive advantage. The Smart Money knows that regulatory excellence only matters if the ships actually show up. When another nation threatens to build a bypass around your toll booth, you do not ignore it. You forensically audit it.

The Malacca Strait Moat

Let us step back and respect the hard data. The Malacca Strait is not just another shipping lane. It is the jugular vein of the global economy. Approximately 40% of all global maritime trade passes through this narrow, congested stretch of water. That staggering volume includes roughly 25% of the world’s seaborne oil supplies and approximately 80% of the energy resources destined for China. This is not just a trade route — it is the physical spine of the Asian economic machine.

Think about what that geographical reality means for our local economy. When a massive container ship docks at our terminals, it does not just drop off a few metal boxes. It buys thousands of tonnes of bunker fuel. It requires complex maritime legal services. It mandates extensive ship repairs. It demands deep corporate financing. Our port throughput hit an extraordinary record of 44.66 million TEU in 2025 — an 8.6% year-on-year improvement that confirmed Singapore’s position as the world’s number one container port by throughput.

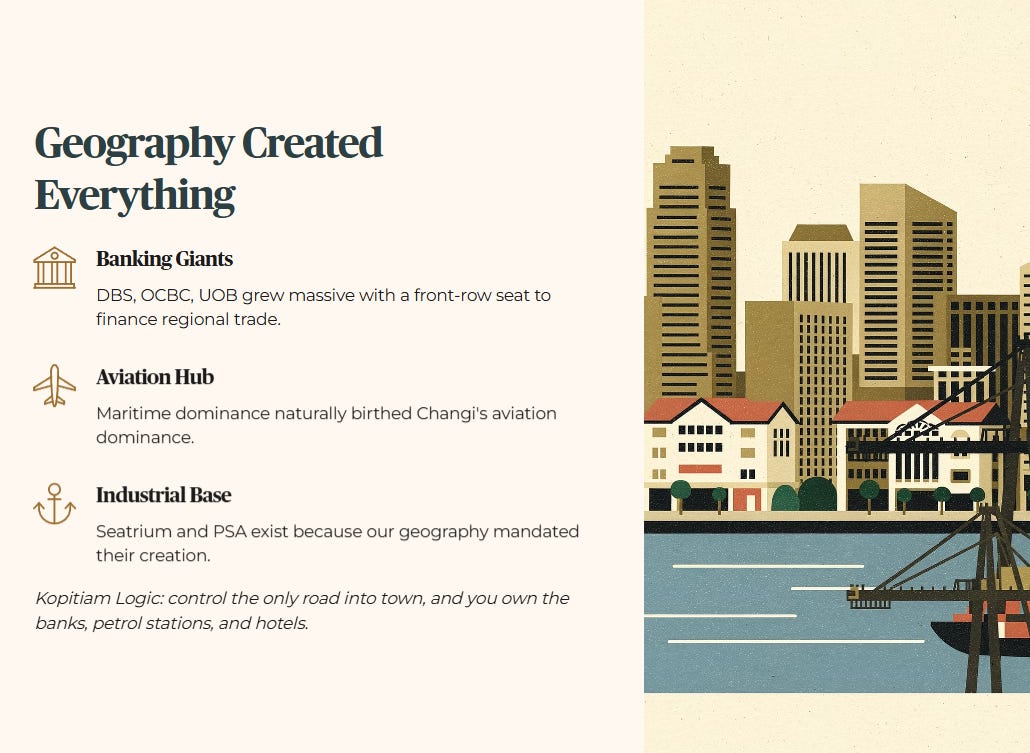

This geographic monopoly directly created the conditions for our financial hub status. DBS, OCBC, and UOB did not become regional titans by accident or pure luck. They grew massive because they had a front-row seat to finance the trade flowing through our waters. Singapore Airlines built Changi Airport into a premier global transit hub because maritime dominance naturally birthed aviation dominance. Companies like Seatrium and PSA Corporation exist because our geography mandated their creation. This is Kopitiam Logic at its finest: if you control the only road into town, you inevitably end up owning the banks, the petrol stations, and the hotels.

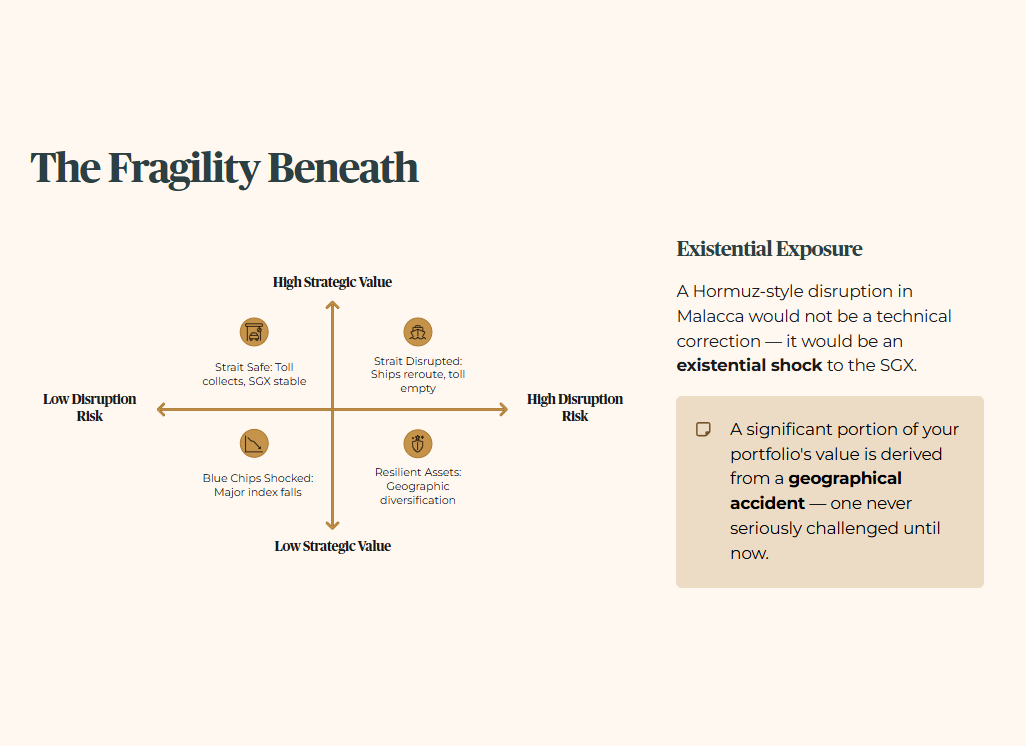

To truly understand the fragility of this setup, look at the Middle East right now. If the Strait of Malacca faced a sudden geopolitical disruption similar to the current Hormuz crisis, the SGX would not experience a minor technical correction. It would face an immediate, existential shock. If vessels cannot safely navigate the strait, they are forced to re-route. If they re-route, the toll booth collects nothing. Our beloved blue-chip stocks are deeply, uncomfortably leveraged to the physical safety and absolute necessity of this specific waterway.

So what does this mean for you? It means a significant portion of your portfolio’s value is derived from a geographical accident — one that has never been seriously challenged until now.

The Thailand Land Bridge

Enter the Thailand Land Bridge. Politicians and engineers have dreamt of cutting a canal through the Kra Isthmus for centuries. But this current iteration is heavily funded, highly politicised, and directly aimed at capturing Singapore’s market share.

The project proposes a 90-kilometre infrastructure corridor physically connecting the Andaman Sea to the Gulf of Thailand. Instead of sailing hundreds of miles south around the Malaysian peninsula and Singapore, ships would dock at the proposed deep-sea port of Ranong on the Andaman side. Cargo would be transferred onto a high-speed rail and motorway network, transported across the Thai terrain, and reloaded onto new vessels at the port of Chumphon on the Gulf side.

The financial numbers are staggering. The estimated cost is THB 990 billion to THB 997 billion — approximately US$27 to US$36 billion depending on the exchange rate applied. The projected capacity models envision Ranong handling 19.4 million TEU and Chumphon handling 13.8 million TEU by the late 2030s. Thailand is actively courting foreign capital from China, Saudi Arabia, and the United States, running high-profile roadshows across the region.

The sales pitch is aggressively simple. The Land Bridge claims to cut shipping times by up to four days compared to the traditional Malacca routing. In a highly optimised global supply chain where every hour is monetised, four days sounds like an eternity.

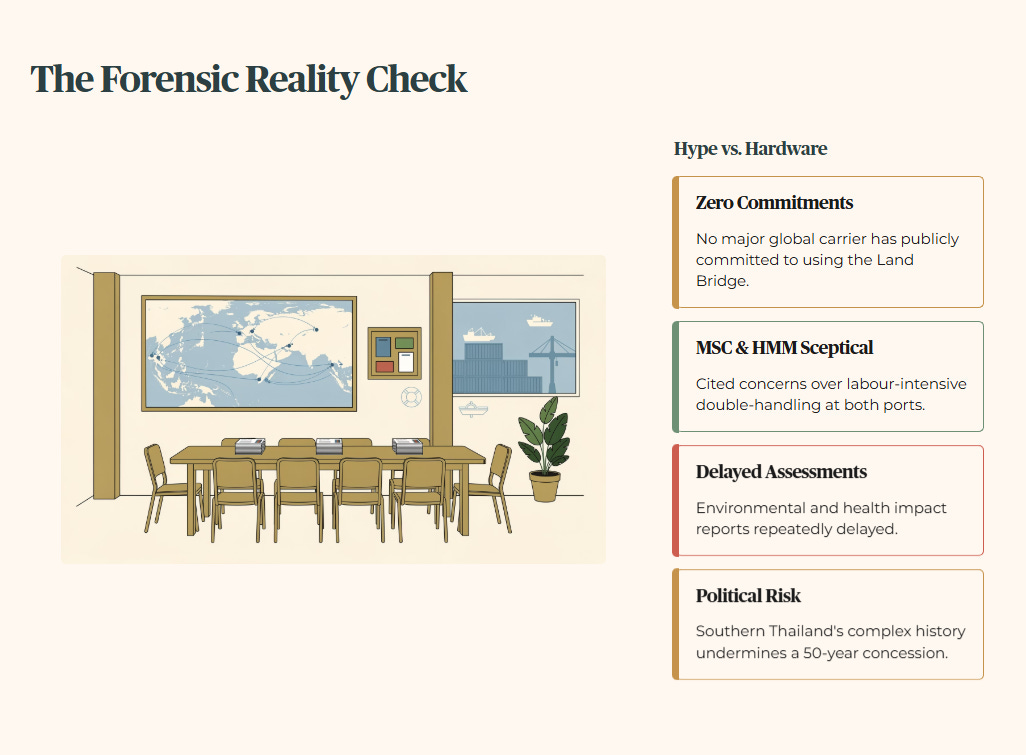

But here is where the forensic audit separates political hype from logistical hardware. Despite glossy brochures and enthusiastic press conferences, zero major global shipping companies have publicly committed to utilising the Land Bridge. Major carriers including MSC and HMM have specifically cited concerns over the labour-intensive double-handling required at both ports. Independent maritime economists remain highly sceptical of the underlying economics. The environmental and health impact assessments have been repeatedly delayed. The political stability required to underwrite a 50-year infrastructure concession in southern Thailand — a region with a complex history — remains a genuine open question.

Iggy’s Insight Do not let the slick political presentations push you into a reactive stance. The Thailand Land Bridge is battling the fundamental physics of global logistics. You cannot lift 20,000 shipping containers off a vessel in the Andaman Sea, load them onto a train, drag them across a jungle, and reload them onto another vessel in the Gulf of Thailand without destroying your profit margin.

Shipping companies are ruthless optimisers. Double-handling cargo is financial suicide. Until a major carrier signs a binding volume commitment, this project remains a geopolitical PowerPoint presentation, not a logistical reality. But the Smart Money does not wait for the concrete to be poured before repositioning.

The SGX Forensic Implications

Let us translate this geopolitical theatre directly into your stock portfolio. If this megaproject materialises — even in a severely diluted form — it creates structural winners and losers on the SGX. We must audit our exposures coldly.

Singapore Airlines (SGX: C6L) derives enormous pricing power from Changi’s entrenched status as a premier passenger and cargo hub. If maritime trade shifts north structurally, aviation cargo networks will follow the new supply chains. A structural diversion of trade routes away from Singapore slowly erodes the premium SIA commands for its logistics division. This is not a sudden crash. It is a slow, structural bleed that plays out over decades, not quarters.

Mapletree Logistics Trust (SGX: M44U) is deeply exposed to ASEAN logistics. The critical forensic question for M44U unitholders is the specific location of their assets — which warehouses are dependent on Malacca Strait transshipment volumes, and which are servicing sticky domestic consumption that exists regardless of where ships route. If transshipment volumes soften near Tuas, warehousing demand in that corridor softens with it.

DBS Group (SGX: D05) is a fascinating forensic case. While DBS actively finances regional trade, their core revenue is increasingly anchored in wealth management — a business that runs on regulatory trust, not cargo volumes. You do not move billions of dollars of family office capital to a new port facility because a container ship saved three days going through a Thai jungle. DBS benefits from Singapore’s geography, but its true moat is the Monetary Authority of Singapore’s institutional credibility.

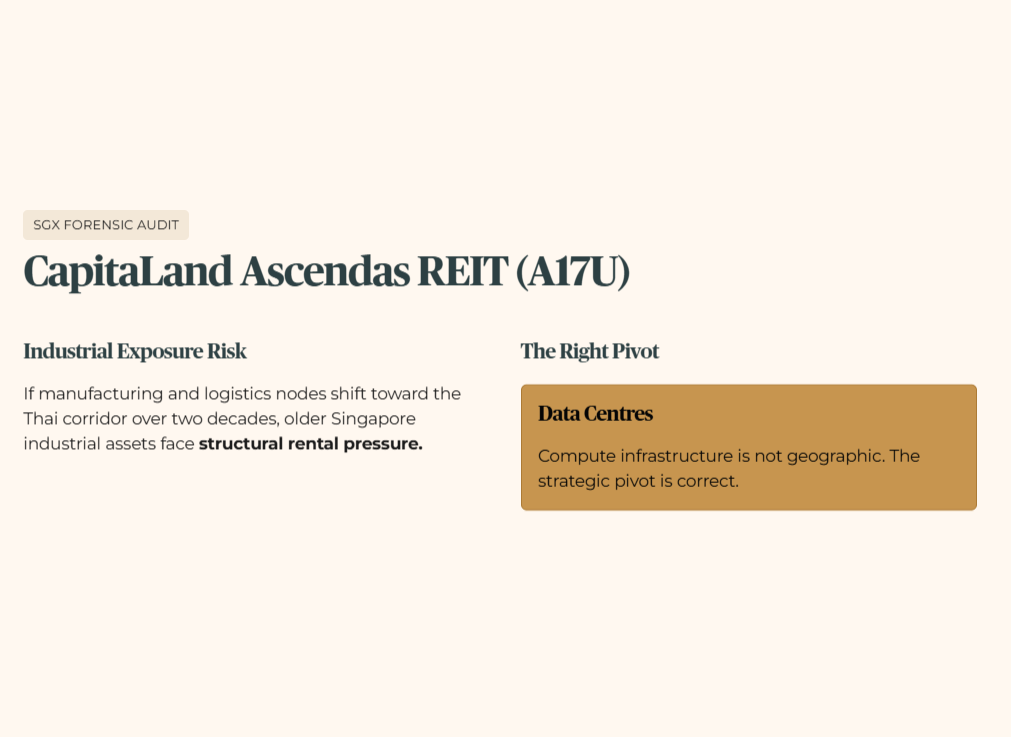

CapitaLand Ascendas REIT (SGX: A17U) faces a similar dynamic. Their regional industrial exposure is substantial. If advanced manufacturing and logistics nodes shift toward the new Thai corridor over the next two decades, older industrial assets in Singapore may face structural rental pressure. Their data centre pivot is the right strategic response — compute infrastructure is not geographic.

“Don’t overpay for the hype. See the math behind the momentum.” .....Use the Fair Value models I use in every video. Code INVESTINGIGUANA gets you 50% off the world’s most powerful stock screener.

🦎 [Spot Undervalued Gems Here]

The Land Bridge isn’t a headline risk—it’s a portfolio sorting machine, and the next section reveals the first SGX name that quietly flips from “blue-chip safety” into a long-term geography liability (plus the exact moat test to spot the next two).