2026 Haw Par 3 Good 3 Red Flags Review - Forensic Deep Dive |🦖EP1523

Tiger Balm brand is world-famous, but the dividend is more like cat scratch. Don't let the cash pile bluff you.

This stock sits on nearly eight hundred million dollars in cash, yet it hands shareholders a regular yield of just 2.37%, mathematically destroying your purchasing power against a 4.0% CPF baseline.

For the Singaporean retiree drawing down their SRS or CPF, holding this asset acts as a hidden tax that starves your monthly income. This bull and bear forensic audit will define exactly whether that massive balance sheet is a genuine valuation opportunity or a permanent trap for your capital.

In This Article:

The Financial Snapshot The Baseline

The 3 Good The Bull Case

The Sovereign Grade Liquidity Moat

The UOB and UOL Dividend Engine

Significant Asset Backed Margin of Safety

The 3 Red Flags The Bear Case

The Structural Yield Trap Reality

Softening Heartland and Regional Demand

The Banking Concentration Paradox

The Singaporean Context The Stress Test

The Weighing Scale Forensic Synthesis

Iggy’s Forensic Compliance Standards Standard Disclaimer

About Iggy & the Elite Investors

The Crash Wasn’t a Surprise. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided before the opening bell — not after the damage is done. The red flags are always there. The question is whether you had the forensic framework to read them in time.

Iggy’s Elite Investors didn’t chase the headline yield. They had the full forensic breakdown — the gearing ratios, the occupancy gaps, the debt overhang — before the market opened and before the price moved. Zero-day reports, the complete “Red Zone” watchlist, and institutional-grade cheatsheets that flag the landmines disguised as opportunities.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

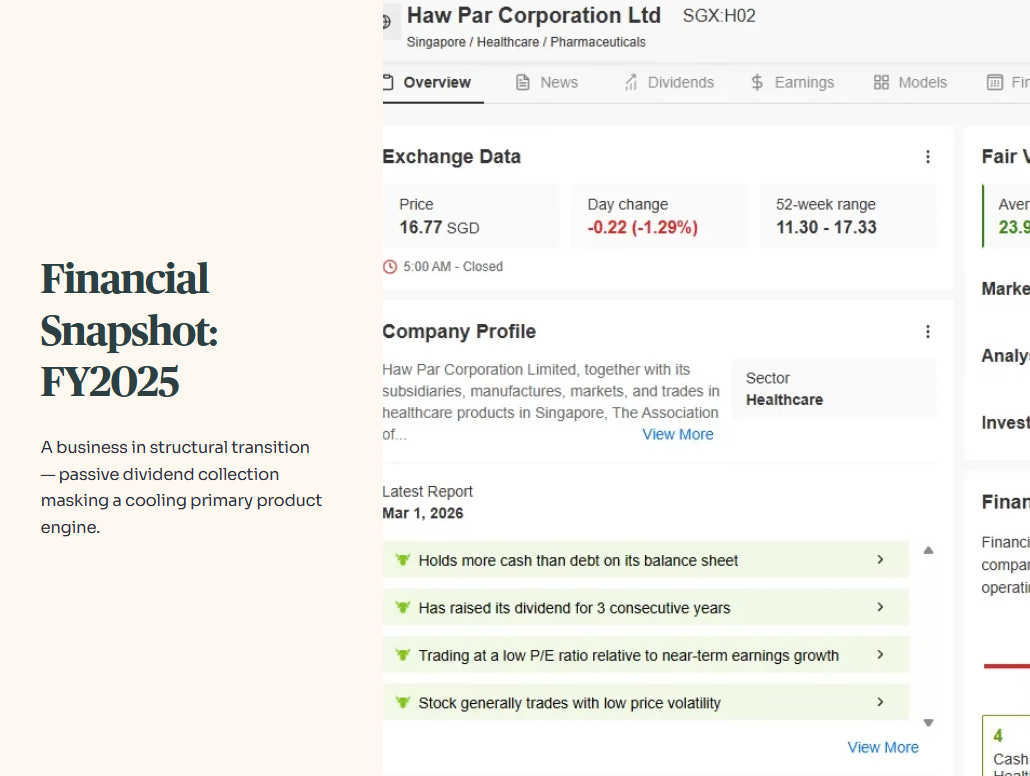

1. The Financial Snapshot (The Baseline)

Haw Par’s performance for the financial year ended 31 December 2025 reveals a business in structural transition, where passive dividend collection aggressively masks a cooling primary product engine.

“Don’t overpay for the hype. See the math behind the momentum.” .....

Use the Fair Value models I use in every video. Code INVESTINGIGUANA gets you 50% off the world’s most powerful stock screener.

🦎 [Spot Undervalued Gems Here]

Forensic Verdict Beat: The balance sheet looks mathematically flawless until you realise management is running a high-conviction banking fund disguised as a legacy pharmacy business.

Financial Health Baseline

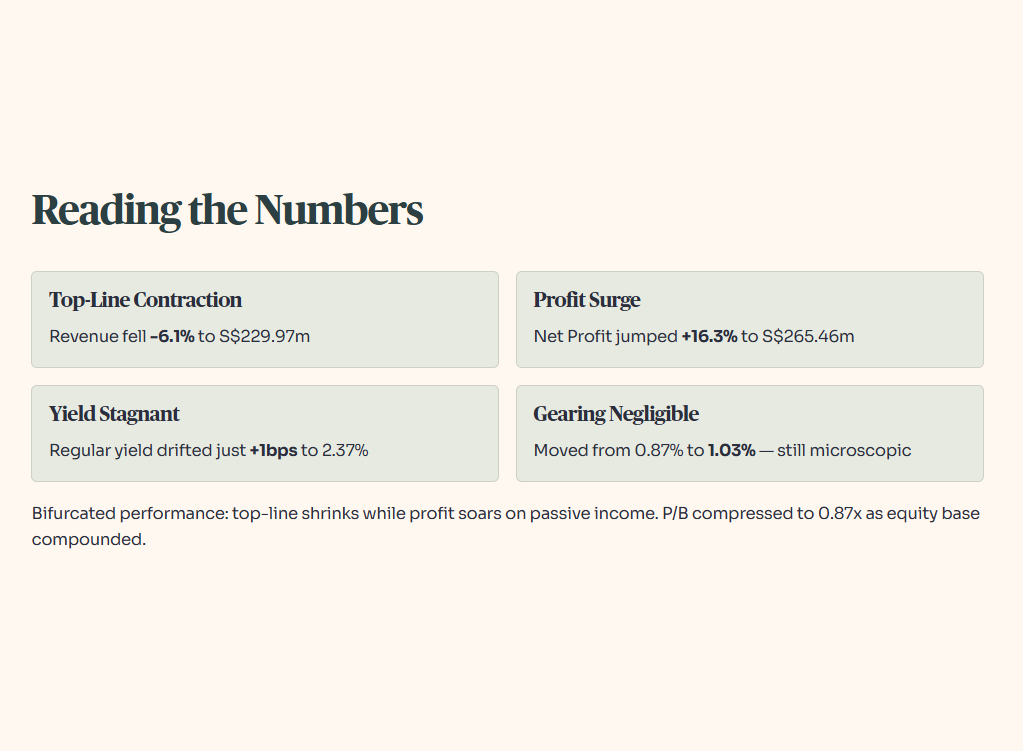

To satisfy the double-entry mandate, we must trace every metric from the baseline table directly into the operational reality. The stock price closed the period at S$16.99, marking a fractional +0.47% variance from the prior period’s S$16.91. Operating performance was highly bifurcated at the core level; total Group Revenue fell by -6.1% to land at S$229.97m, down from the previous S$244.82m. In stark contrast to the top-line contraction, Net Profit registered a massive +16.3% jump, reaching S$265.46m against the prior S$228.27m.

On the balance sheet, Gearing shifted up by a negligible +16bps, moving from 0.87% to a still-microscopic 1.03%. Despite the net profit surge, the Regular Yield remained functionally stagnant, posting a +1bps drift from 2.36% to 2.37%. Consequently, the P/B Ratio compressed by -3.3%, narrowing from 0.90x to 0.87x as the underlying equity base compounded.

🦎 Iggy’s Insight Block 1

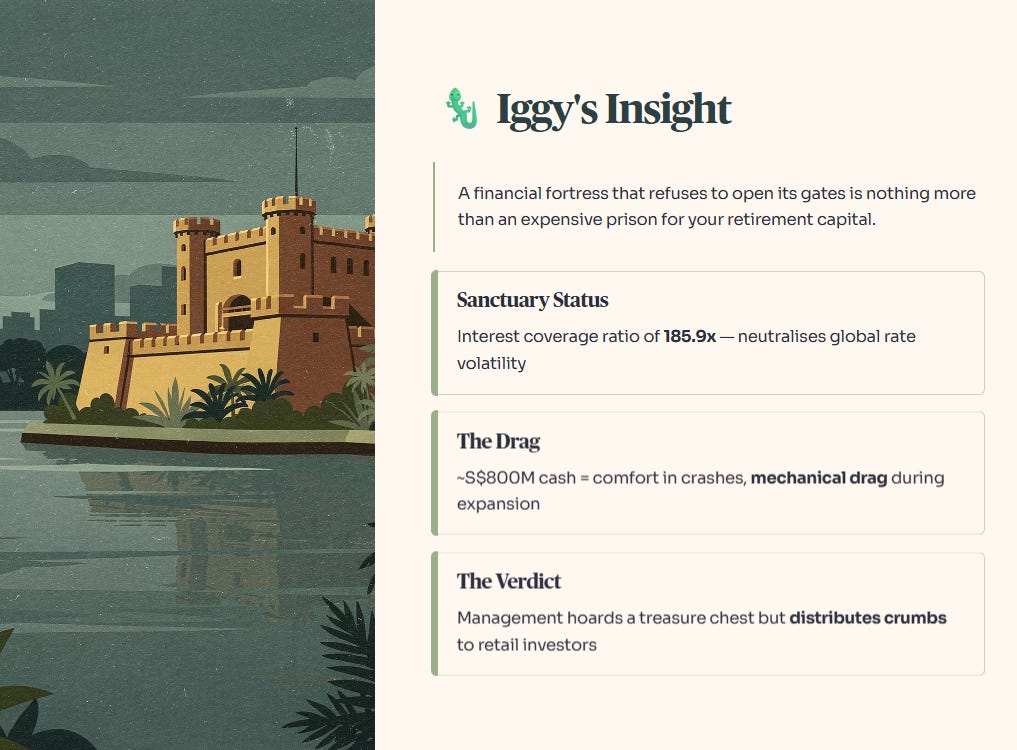

Haw Par is the purest definition of a Sanctuary on the local exchange, boasting a sovereign-grade interest coverage ratio of 185.9x that effectively neutralizes global rate volatility. However, the market applies a permanent conglomerate discount because the enterprise lacks an aggressive capital recycling strategy.

While sitting on nearly eight hundred million in cash provides exceptional psychological comfort during a severe market correction, it acts as a mechanical drag on equity returns during periods of normal economic expansion. Management is hoarding a treasure chest but distributing crumbs to the retail base.

Forensic Punchline: A financial fortress that refuses to open its gates is nothing more than an expensive prison for your retirement capital.

2. The 3 Good (The Bull Case)

Good 1: The Sovereign-Grade Liquidity Moat

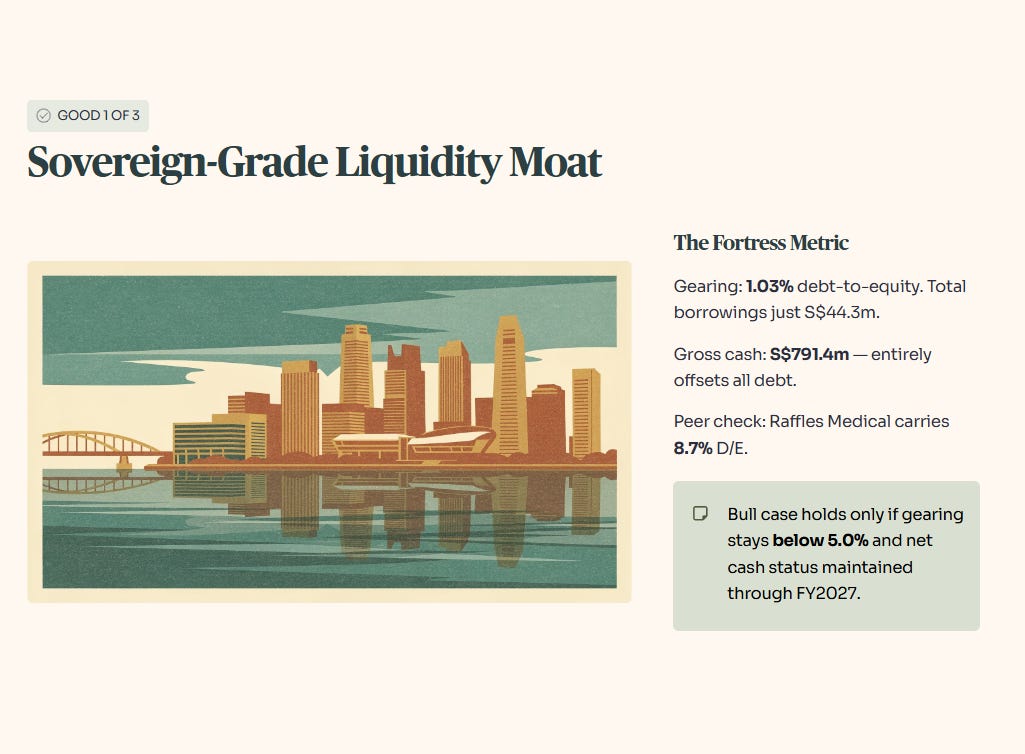

Haw Par’s most compelling feature is its almost total immunity to The Debt Wall that is currently fracturing the REIT and property developer sectors. The raw fact is that the Group operates with a gearing ratio of 1.03% (calculated strictly as debt-to-equity), meaning total borrowings sit at just S$44.3 million against an immense total equity base. This is a fortress metric.

To put this into sharp perspective, SGX healthcare peer Raffles Medical carries a debt-to-equity ratio of 8.7% when including lease liabilities. Haw Par’s minimal borrowings are merely short-term tactical drawdowns utilized to hedge foreign exchange exposure in Hong Kong Dollars. They are entirely offset by a staggering gross cash and bank balances position of S$791.4 million.

In a stress scenario where the 6-month T-Bill yield spikes 10% from its current 1.46% base, Haw Par experiences a net positive operational outcome. The interest income generated on its massive deposit base will materially outpace any fractional increase in its borrowing costs.

For a conservative capital allocator, this creates an unshakeable asset. It is the financial equivalent of a fully paid-off HDB flat where the owner just sits back and collects the rising fixed deposit interest with zero threat of foreclosure. There is absolutely no structural risk of insolvency or forced equity fundraising here.

This bull case only holds if the Gearing Ratio remains strictly below 5.0% and the Group maintains its net cash status through the conclusion of FY2027.

Good 2: The UOB and UOL Dividend Engine

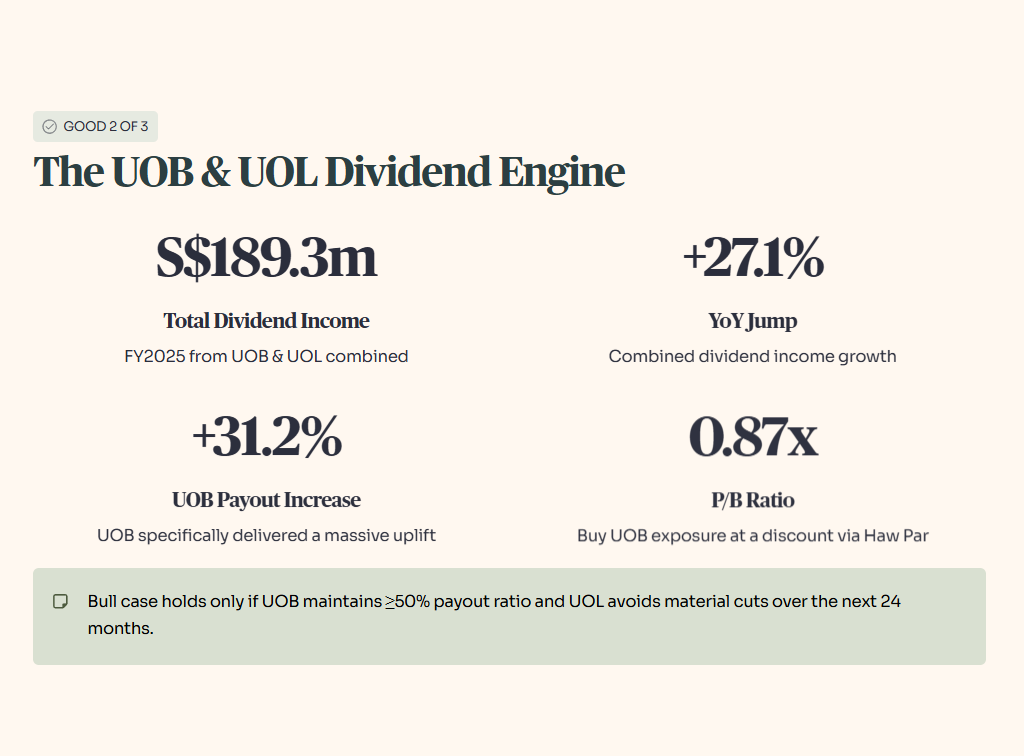

While the retail public automatically associates this ticker with topical ointments and pain relief, the forensic reality is that the enterprise operates primarily as an elite dividend collection vehicle. The core driver of net profit growth is the strategic investment portfolio, heavily concentrated in United Overseas Bank (UOB) and UOL Group.

For the financial year ended 31 December 2025, combined dividend income from these two specific entities jumped 27.1% year-over-year. UOB specifically delivered a massive 31.2% increase in payouts, elevating Haw Par’s total dividend income to an impressive S$189.3 million. This flow functions as pure Organic NPI—it is a high-margin cash stream that requires zero operational overhead, zero marketing spend, and zero supply chain logistics.

Acquiring Haw Par shares is effectively a discounted proxy trade on Singapore’s banking dominance. Because the enterprise is currently trading at a P/B Ratio of 0.87x, you are acquiring indirect exposure to UOB shares at a lower cost basis than buying the bank directly on the open market.

If UOB continues to benefit from favorable interest rate environments and executes its capital return policy, Haw Par’s non-operating segment will continue to comfortably subsidize any weakness in the legacy manufacturing divisions.

This bull case only holds if UOB maintains a dividend payout ratio of at least 50% and UOL Group avoids material distribution cuts over the next 24 months.

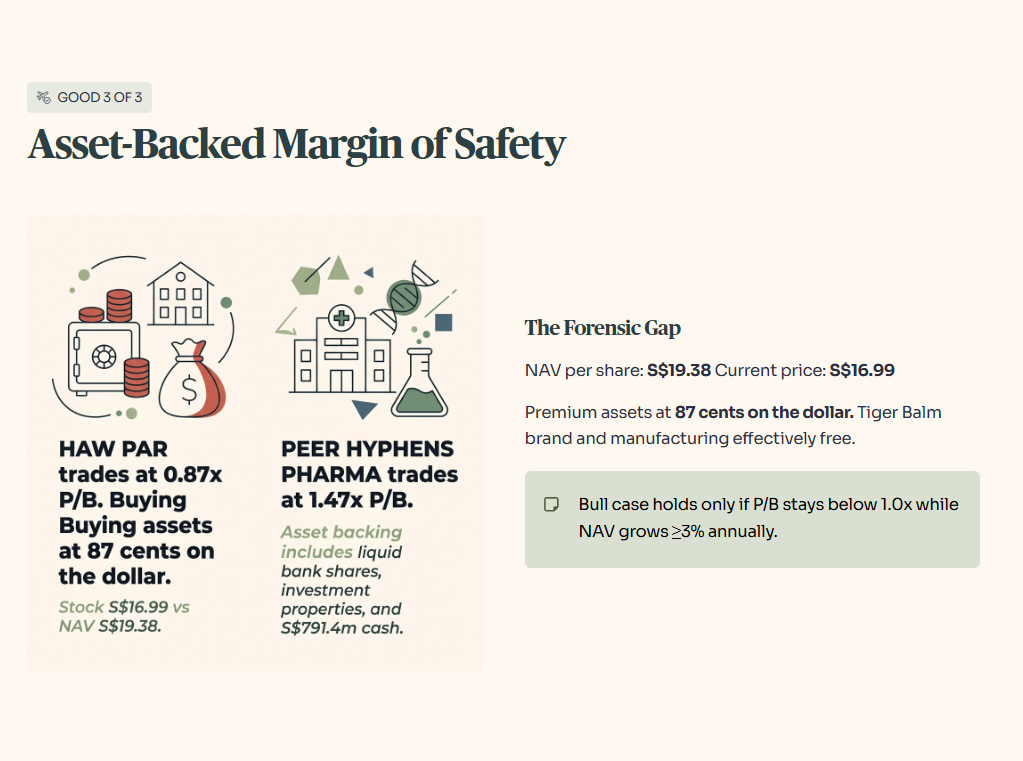

Good 3: Significant Asset-Backed Margin of Safety

The third pillar of the bull thesis rests entirely on extreme, quantifiable undervaluation relative to the firm’s tangible asset base. With a Net Asset Value (NAV) per share reported at exactly S$19.38 for the FY25 period, the stock’s current trading price of S$16.99 represents a significant Forensic Gap. You are acquiring premium assets for roughly 87 cents on the dollar.

When we run a peer context check, we see that Hyphens Pharma trades at a P/B ratio of 1.47x, highlighting exactly how deeply discounted Haw Par remains relative to other listed pharmaceutical names. This valuation floor is not composed of intangible goodwill or speculative intellectual property. It is heavily backed by highly liquid bank shares, prime investment properties, and nearly eight hundred million in hard cash. Even if the healthcare business hypothetically flatlined tomorrow morning, the liquidation value of the balance sheet vastly exceeds the current market capitalization.

For the defensive investor, this creates a thick shock absorber against systemic crashes. While growth analysts might lament the lack of aggressive geographic expansion, the current pricing essentially gives you the entire Tiger Balm brand portfolio and the physical manufacturing infrastructure for free, forcing you to pay only for the underlying financial assets.

This bull case only holds if the Price-to-Book ratio remains below 1.0x while the Net Asset Value per share continues to grow at a minimum of 3% annually.

3. The 3 Red Flags (The Bear Case)

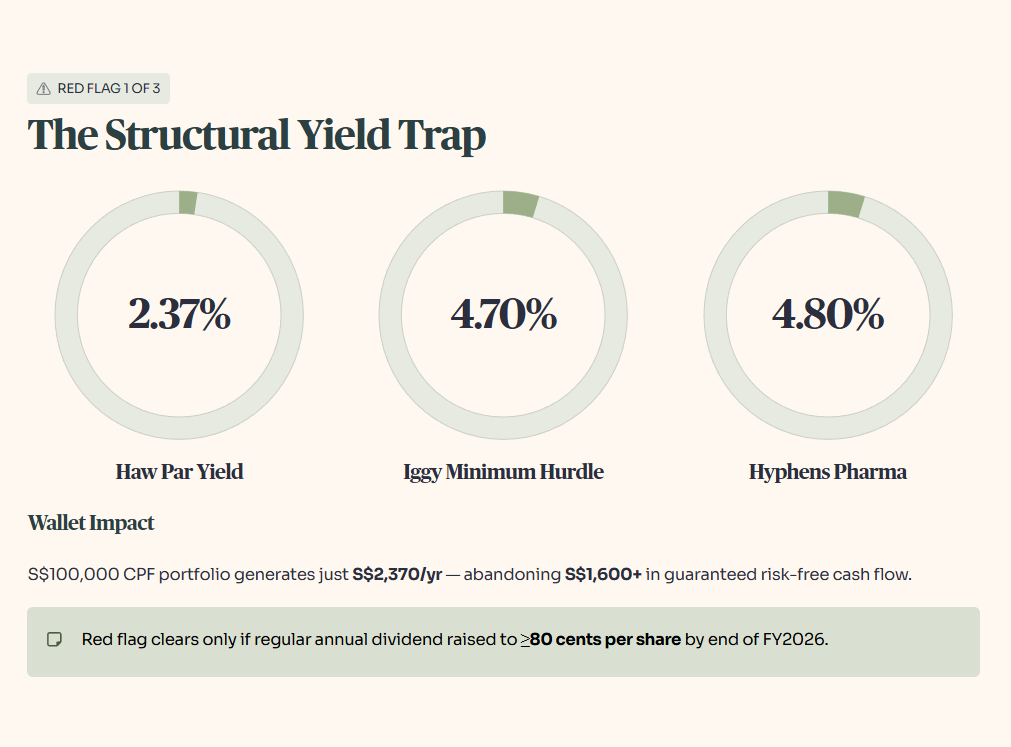

Red Flag 1: The Structural Yield Trap Reality

We must apply the strict Five-Layer Rule here due to a severe threshold breach on distributions.

Layer One establishes the raw fact: based on the audited FY25 financials, Haw Par distributes a regular yield of exactly 2.37%.

Layer Two applies the benchmark: this metric completely fails the Iggy minimum yield hurdle of 4.7% and sits drastically below the 3–5 year historical sector average of 4.5% expected from mature, cash-rich enterprises.

Layer Three provides peer context: when we audit direct SGX healthcare peers like Hyphens Pharma, they currently pass this exact same threshold by offering a yield near 4.8%, proving that regional distributors can indeed execute shareholder-friendly capital returns.

Layer Four dictates the forward scenario: if Singapore experiences a macro trigger where imported inflation forces a 10% structural increase on core household utility tariffs, this frozen 2.37% distribution offers zero defensive offset, resulting in a quantified real-return compression of approximately 1.5% against your baseline living costs.

Layer Five defines the wallet impact: for the 62-year-old heartland archetype managing a S$100,000 CPF drawdown portfolio, holding this asset limits your annual cash generation to just S$2,370. This creates a specific consequence where you are permanently abandoning over S$1,600 in guaranteed, risk-free annual cash flow compared to deploying those exact funds into state-mandated accounts.

My forensic stance is absolute: management’s refusal to adjust the payout ratio transforms a fundamentally invincible balance sheet into an active detriment for the income-seeking retiree.

This red flag clears only if management raises the regular annual dividend payout to a minimum of 80 cents per share by the conclusion of FY2026.

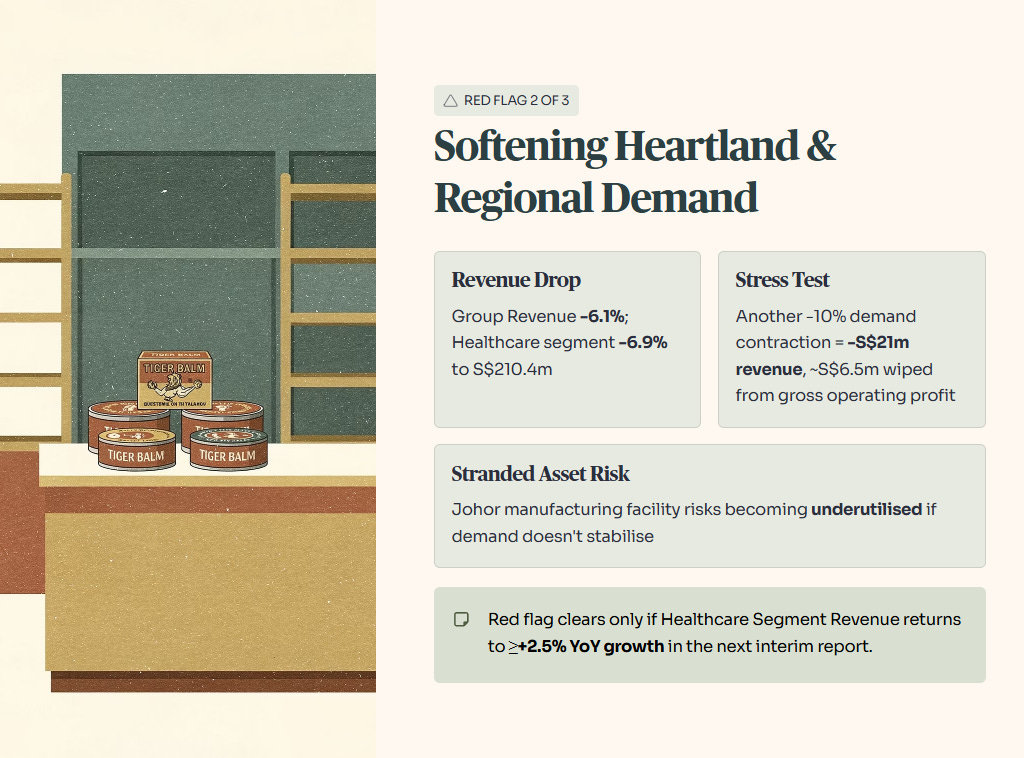

Red Flag 2: Softening Heartland and Regional Demand

The dividend distraction from the massive banking stakes is masking a concerning operational reality within the core business. In the audited FY25 financials, while Group Revenue fell 6.1%, the critical Healthcare segment revenue dropped an even steeper 6.9%, declining from S$226.0m to S$210.4m. This is a flashing indicator that the consumer moat is vulnerable to the regional cost-of-living squeeze.

Tiger Balm is an internationally iconic brand, but it is ultimately a discretionary pharmacy purchase. If Asian wholesale buyers and retail consumers face continued macroeconomic pressure, inventory destocking will accelerate. Think of it like a wet market stall: if the core product isn’t clearing the shelves, the stall owner cannot just point to their bank interest to call it a successful trading day.

We stress-test this trajectory: if regional demand contracts by another 10% in the current fiscal year, healthcare revenue sheds an additional S$21 million. Applying their historical operating margins, this would eliminate approximately S$6.5 million directly from the gross operating profit layer. The much-touted Johor manufacturing facility risks becoming a stranded, underutilized asset if end-demand does not stabilize rapidly.

This red flag clears only if the Healthcare Segment Revenue returns to positive year-over-year growth of at least 2.5% in the upcoming interim financial report.

Red Flag 3: The Banking Concentration Paradox

Haw Par’s greatest strength is simultaneously its most fatal vulnerability. Because dividend income from UOB and UOL drove the +16.3% rise in Net Profit to S$265.46m, the company has effectively morphed into a concentrated, un-diversified financial holding company. This severe lack of diversification violates core risk management principles.

If the global rate cycle decisively turns and central banks aggressively cut rates, bank Net Interest Margins (NIMs) will compress immediately. We do not need a catastrophic banking failure to see the impact; we only need a reversion to the mean.

If UOB is forced to cut its dividend by 25% due to tighter regulatory capital requirements, the math is brutal. Evaluating the FY25 UOB dividend haul of S$169.9 million, a 25% haircut would carve an immediate S$42.5 million hole in Haw Par’s annual earnings.

The stock is currently priced as a defensive healthcare play, but its earnings engine is heavily exposed to the cyclicality of the financial sector. You are carrying severe banking-sector risk without receiving the direct 5–6% yields that actual bank shareholders currently enjoy.

This red flag clears only if non-investment operating profit grows to represent at least 40% of the Total Group Profit mix by the end of FY2027.

The risk premium calculation in the following stress-test exposes whether this creates positive real returns against CPF alternatives or just erodes your retirement capital.