MLT Dividends Cannot Beat Your CPF Accrued Interest Ghost

Why Using CPF for REITs Can Quietly Destroy Your HDB Retirement Math

The air at the Bedok Interchange Hawker Centre is thick today — not just with the smell of roasting duck and the humidity of a pre-monsoon afternoon, but with a palpable sense of confusion. A group of retirees huddled over their phones, eyes squinting at the latest financial news. One point four six percent. That is the number currently causing the stir. It is the latest six-month T-Bill yield, and while the mainstream headlines are trumpeting a “bounce” from previous levels, the forensic reality is far less celebratory.

If you are standing here, looking at that 1.46% while the price of your favourite plate of chicken rice has quietly crept up by another fifty cents, you are witnessing a market paradox. The market is celebrating a minor uptick in government debt yields, but for the retail investor over fifty, this is a loud, clear signal: the easy sanctuary of short-term debt is no longer providing the inflation protection you need to sustain a retirement in one of the world’s most expensive cities.

For the person managing a hard-earned CPF Ordinary Account (OA) or a Supplementary Retirement Scheme (SRS) pot, the priority has shifted from “getting rich” to “staying solvent.” When you see a T-Bill yield of 1.46%, you must realise that after accounting for the 2.5% you earn by doing absolutely nothing in your OA, you are starting the race in a deficit. You are paying a premium for safety that might be quietly eroding your future purchasing power.

Today, we are going to audit the receipts. We are looking at Mapletree Logistics Trust to see if its dividends offer a genuine risk premium or if they are just another version of a yield trap disguised as a blue chip. But more importantly, we are addressing the Accrued Interest Ghost — the ticking time bomb of lost interest that most Singaporeans in the 45-to-60 bracket are sitting on because they used CPF to pay for their homes without calculating the true opportunity cost. Today, we are not just auditing a REIT.

We are launching the forensic solution: Elite Tool #1 — The CPF Penalty-Yield Arbitrage Calculator, available exclusively for Iggy’s Elite Investors..

In This Article:

Step 1 — The Health Check: Solvency and Financial Health Checklist

Step 2 — The Wealth Check: Yield, Cash Flow and Dividend Trajectory

Elite Tool #1 — The CPF Penalty-Yield Arbitrage Calculator

Step 3 — The Price Check: Valuation and Peer Comparison

Iggy’s Insights

Step 4 — The Bottom Line: Strategic Stance

Iggy’s Forensic Compliance Standards — Standard Disclaimer

About Iggy & the Elite Investors

One Community. One Forensic Lens. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. While free subscribers are reading yesterday’s story, Iggy’s Elite Investors are already cross-checking the next setup — together, in real time.

Iggy’s Elite Investors don’t just get the report earlier. They get the full forensic picture the moment it’s finalised — zero-day breakdowns, the complete “Red Zone” watchlist, and institutional-grade cheatsheets built around the same Five-Layer Audit you see here. The difference is they get it before the market opens, not after it has already moved.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

Step 1: The Health Check (Solvency Audit)

Before we even look at the yield, we have to look at the foundation. In the forensic world, we do not care how fast a car goes if the brakes are made of cardboard. We are looking for a Fortress Balance Sheet — a gearing ratio below 35% and an Interest Coverage Ratio (ICR) above 4.0x.

Mapletree Logistics Trust is often touted as the gold standard of logistics REITs because of its Temasek-linked sponsor. A forensic audit does not care about the name on the building. It cares about the numbers in the ledger.

Financial Health Checklist: Mapletree Logistics Trust (MLT)

Educational Note: Gearing and Your Nephew’s Kopitiam

Imagine your nephew wants to start a small business selling artisanal coffee. If he spends S$100 of his own money, he owns it fully. But if he borrows S$40 for every S$60 he puts in, he has a gearing of 40%. In a kopitiam context, gearing is the amount of cai fan your nephew buys on credit. If the stall increases prices — that is, interest rates rise — he might not be able to afford the fish anymore. At 40.8%, MLT is eating expensive fish right now. When a REIT has to refinance debt at 4.5% that was previously pegged at 1.5%, that money has to come from somewhere — and it usually comes out of your dividend cheque.

The gearing level here is the primary friction point. While the MAS regulatory limit is higher for S-REITs, our personal 35% ceiling is designed to protect you from the rate shock that occurs when the Debt Wall arrives in 2027. ICR at 3.7x is also below our 4.0x threshold — the trust is getting squeezed on both sides of the ledger.

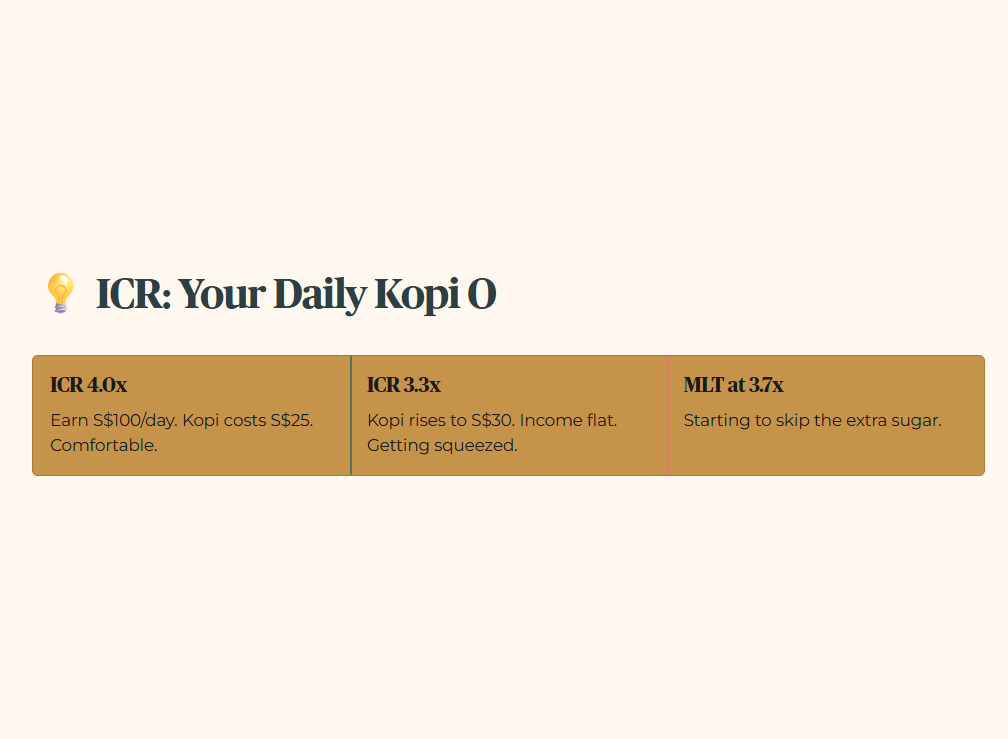

Educational Note: ICR (Interest Coverage Ratio)

Think of this as your ability to pay for your daily Kopi O. If you earn S$100 a day and your Kopi costs S$25, your ICR is 4.0x. You can afford the coffee and still have money for rice. If the price of coffee goes up to S$30 because interest rates have risen, and your income stays flat, your ICR drops to 3.3x. You are getting squeezed. MLT at 3.7x is starting to skip the extra sugar.

Step 2: The Wealth Check (Yield & Cash Flow Trajectory)

Now that we have identified the structural risks, we calculate what MLT is paying us to take them on. The consensus forward dividend yield for 2026 sits at approximately 6.0%, based on a forecast DPU of roughly 7 Singapore cents against a current price of S$1.16. This figure comes from third-party consensus forecasts across multiple aggregators, not from an officially filed distribution announcement — treat it as a directional working figure rather than a confirmed number.

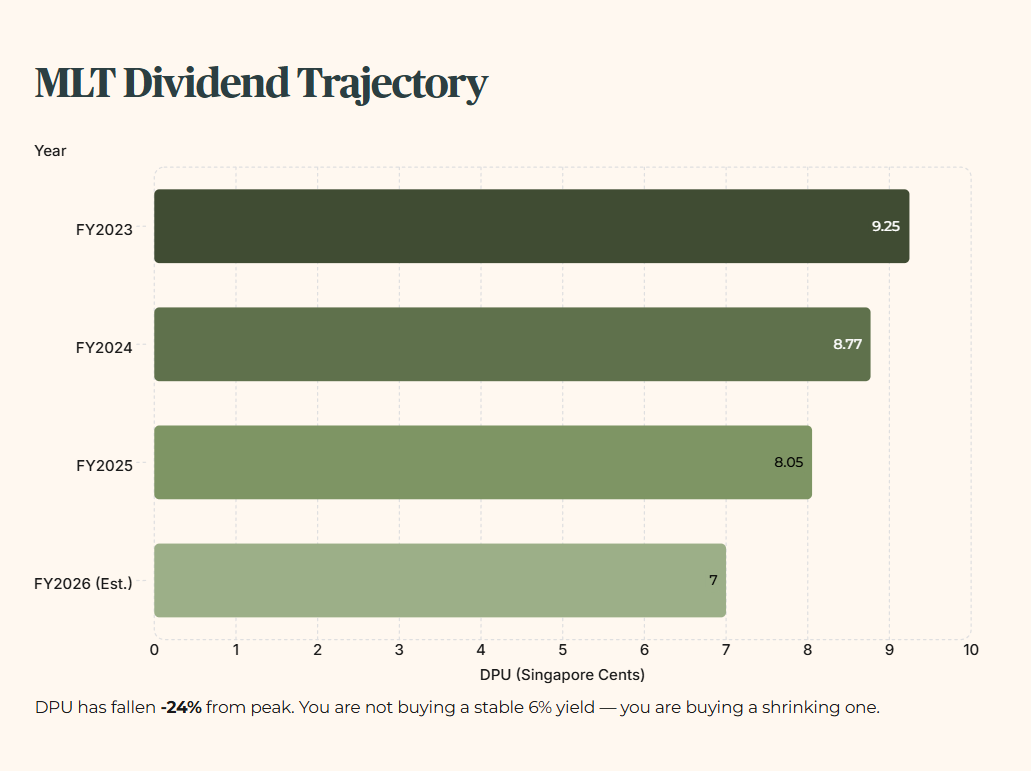

What matters more than the exact yield figure is the trajectory behind it.

Dividend Trajectory Audit: MLT

You are not buying a stable 6% yield. You are buying a yield that has been shrinking for two consecutive years, with the forward consensus pointing to a further decline. The forensic question the Five-Layer Audit demands you answer is whether that shrinkage has stopped or whether it has further to run.

Five-Layer Audit: MLT Yield

Layer 1 — Raw Fact: The consensus forward yield is approximately 6.0%. MLT clears our 4.7% absolute minimum yield hurdle at this figure.

Layer 2 — Benchmark: MLT’s DPU has declined from 9.245 cents to 8.053 cents over two years, with the 2026 consensus pointing to approximately 7.0 cents. You are buying into a declining trajectory, not a stable one.

Layer 3 — Peer Context: Compared to CapitaLand Ascendas REIT (CLAR), MLT’s exposure to the China logistics slowdown is significantly higher. CLAR has delivered positive organic NPI growth over the same period.

Layer 4 — Forward Scenario: If the China logistics market sees a further 10% rent reversion, the effective yield could compress from 6.0% toward 5.4%. At Morningstar’s more conservative 5.66% forecast, the margin of safety narrows further.

Layer 5 — Wallet Impact: For a 60-year-old in Marine Parade transitioning from accumulation to income drawdown, a declining distribution is not just a yield problem — it is a purchasing power problem. If the Elite Tool #1 says your CPF breakeven yield is 6.5%, a drifting 6.0% is a net loss against your Accrued Interest Ghost before the first dividend lands.

Note on the Stress-Test Buffer: For this audit, I apply a conservative floor of 3.2%. This is my static personal standard for capital protection — we audit for the storm, not just the sunny day. While the T-Bill sits at 1.46%, I do not lower my standards to match a temporary market dip. My floor remains at 3.2% to ensure your sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7% — that is the 3.2% floor plus 150 basis points of mandatory risk premium. MLT clears this hurdle at the consensus figure, but the declining trajectory is the real risk that the headline number conceals.

The painful truth is that most HDB owners are already losing this “shrinking prata” battle inside their CPF without realising it—because they have never calculated the exact breakeven penalty yield that quietly turns a 6% REIT into a net loss.