Hormuz Gate Locked: Why Your REIT Dividends Will Drop

Institutional desks say 'temporary spike,' but the Qatar LNG data shows a 5-year hole. Retail is being lulled.

HORMUZ GATE LOCKED: WHY YOUR REIT DIVIDENDS WILL DROP

Section 1: The Global Headline — The Storm

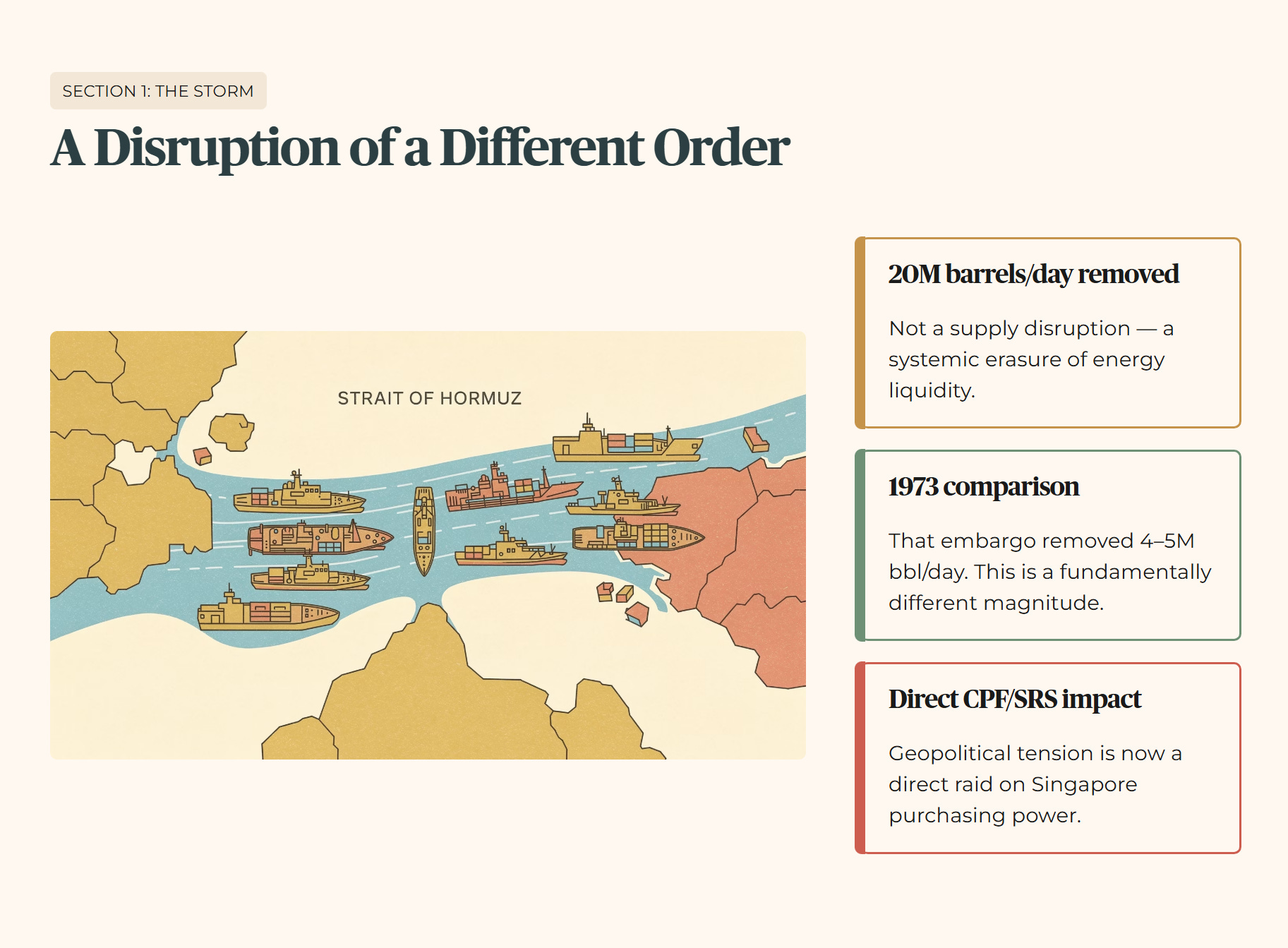

The Strait of Hormuz has effectively become a locked gate, and the keys are at the bottom of the ocean. Following the military actions of February 28, 2026, the removal of twenty million barrels of oil per day from the global market is not just a supply disruption. It is a systemic erasure of energy liquidity.

To put that in historical context: the 1973 oil embargo removed approximately four to five million barrels per day and sent shockwaves through the global economy for a decade. We are now looking at a disruption of a fundamentally different order of magnitude. For a Singaporean retail investor, this is the moment where geopolitical tension stops being a headline and starts being a direct raid on your CPF and SRS purchasing power.

In This Article:

The Global Headline — The Storm

The Forensic Gap is widening by the hour

Iggy’s Insight

The Local Impact — The Wallet

You cannot optimize your way out of a physical supply collapse

The Data Proof — The Evidence

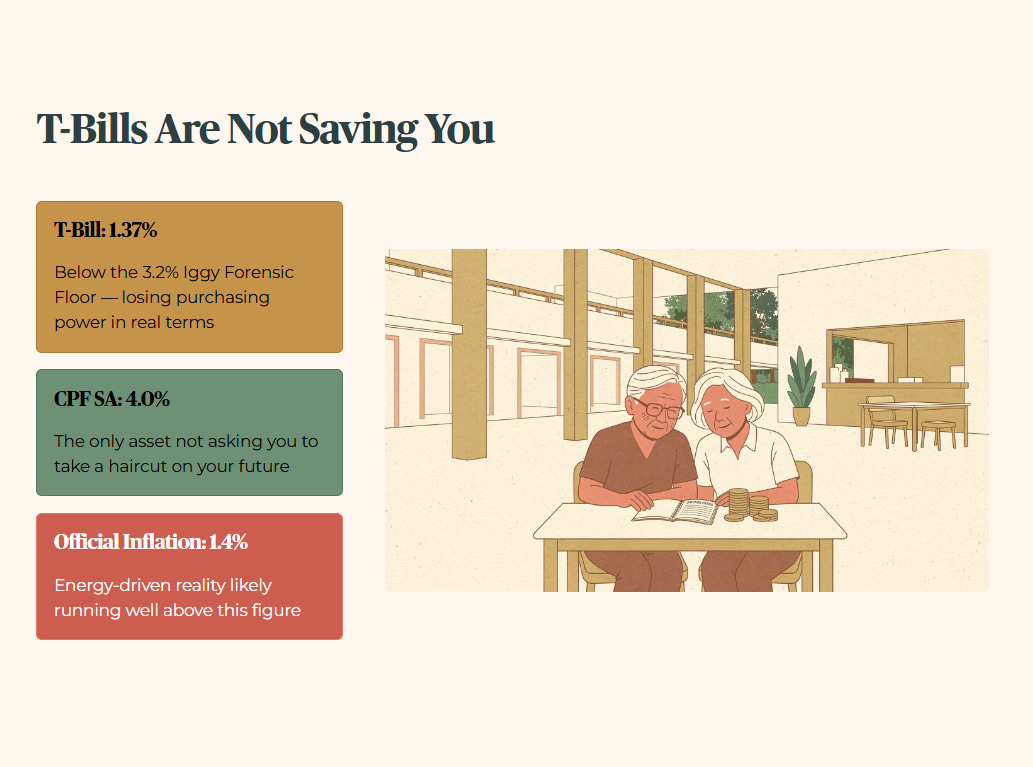

The forensic linchpin here is the 1.37 percent yield

Note on the Stress-Test Buffer

The Strategic Landscape

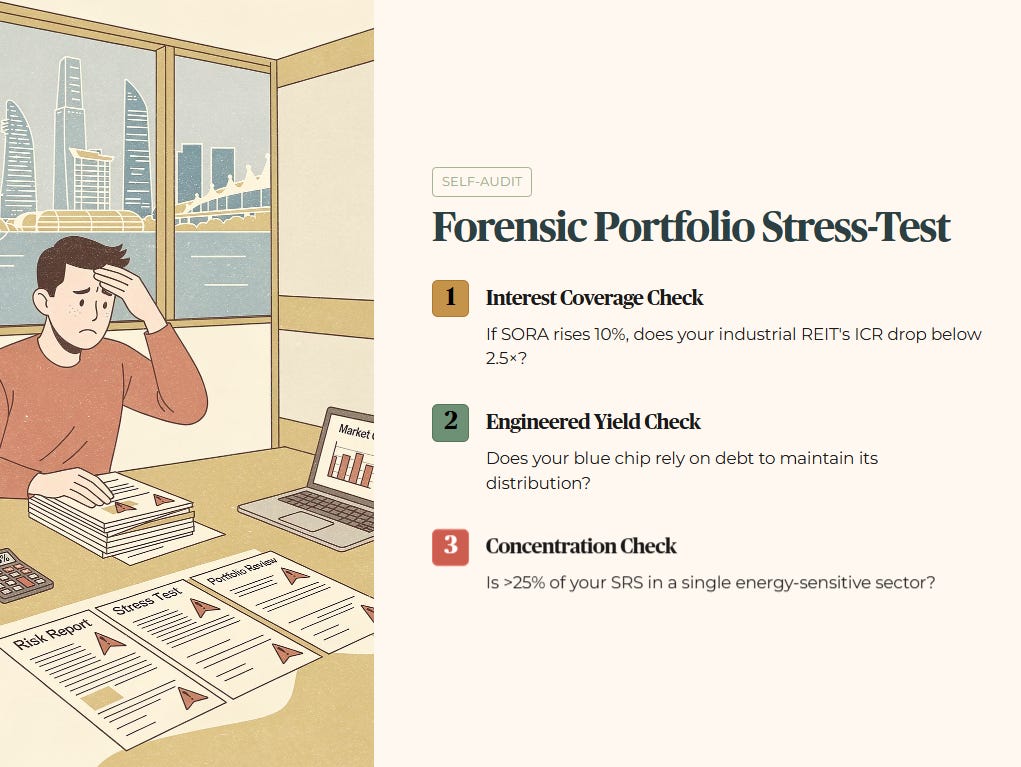

Forensic Portfolio Stress-Test Questions

The Singapore Investor Playbook

Part A — Shock Absorption

Part B — The Accumulator (aged 50–57)

Part C — The Drawdown Investor (aged 58–65)

Iggy’s Bottom Line

Iggy's Verdict

About Iggy & the Elite Investors

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

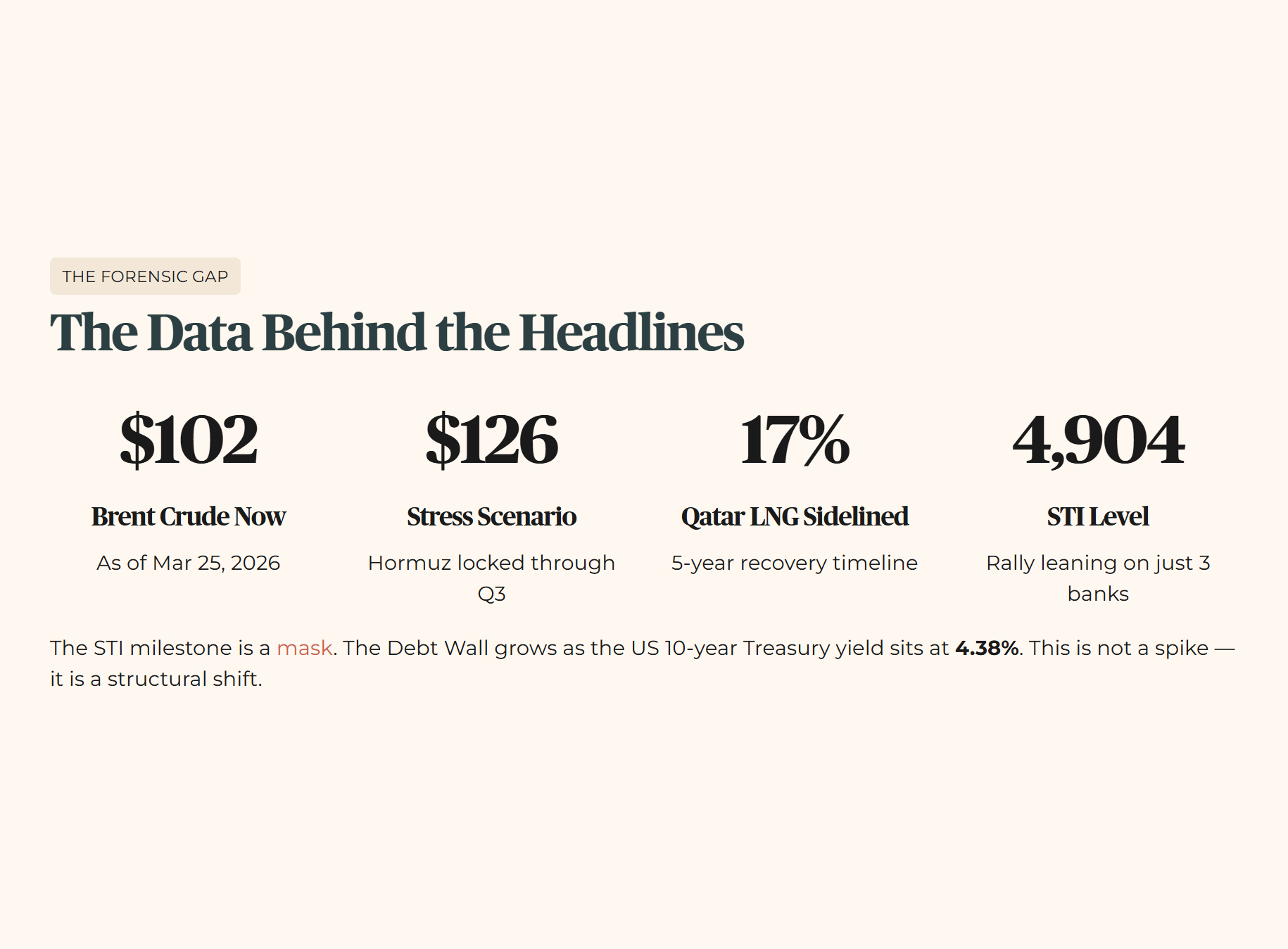

The Data Behind the Headlines

The Forensic Gap is widening by the hour. Brent crude is currently trading around US$102 per barrel as of March 25, 2026. That is the baseline. The forensic stress scenario — which assumes Hormuz remains effectively locked through the third quarter — projects Brent pushing toward US$126 per barrel as physical supply tightens further.

While institutional analysts talk about temporary price discovery, the data shows Qatar LNG export capacity sidelined by seventeen percent with a five-year recovery timeline. This is not a spike. It is a structural shift. If you are managing a retirement portfolio in Bedok or Toa Payoh, the consensus narrative says the STI at 4,904 points is a sign of strength. But look at the data: that rally is leaning almost entirely on three banks while the rest of the landscape faces a brutal Debt Wall as refinancing costs climb alongside the US ten-year Treasury yield of 4.38%.

Iggy’s Insight

There is a dangerous psychological gap between the “everything is fine” rhetoric coming from institutional desks and the physical reality of energy gating. The market is trying to price this as a cyclical event, but the destruction of infrastructure at the Ras Laffan complex suggests a multi-year supply hole. Retail investors are being lulled by a 5,000-point STI milestone, but that number is a mask. The forensic truth is that the cost of capital is being permanently reset higher. If your yield does not clear the hurdle now, it never will. Forensic Punchline: A rising tide lifts all boats, but a storm surge only reveals who has not patched their hull.

Section 2: The Local Impact — The Wallet

The energy crisis is no longer distant thunder. It is a tax being collected at every hawker centre and utility meter in Singapore. Because we rely on imported natural gas for ninety-five percent of our electricity, the closure of the Strait hits our wallet with a seven-day delay. We are seeing electricity retailers like Senoko and Geneco hiking fixed-price plans by over eleven percent in a matter of weeks. For a family in a four-room HDB in Marine Parade, that is an extra ten dollars a month just to keep the lights on — money that used to go toward the retirement sanctuary.

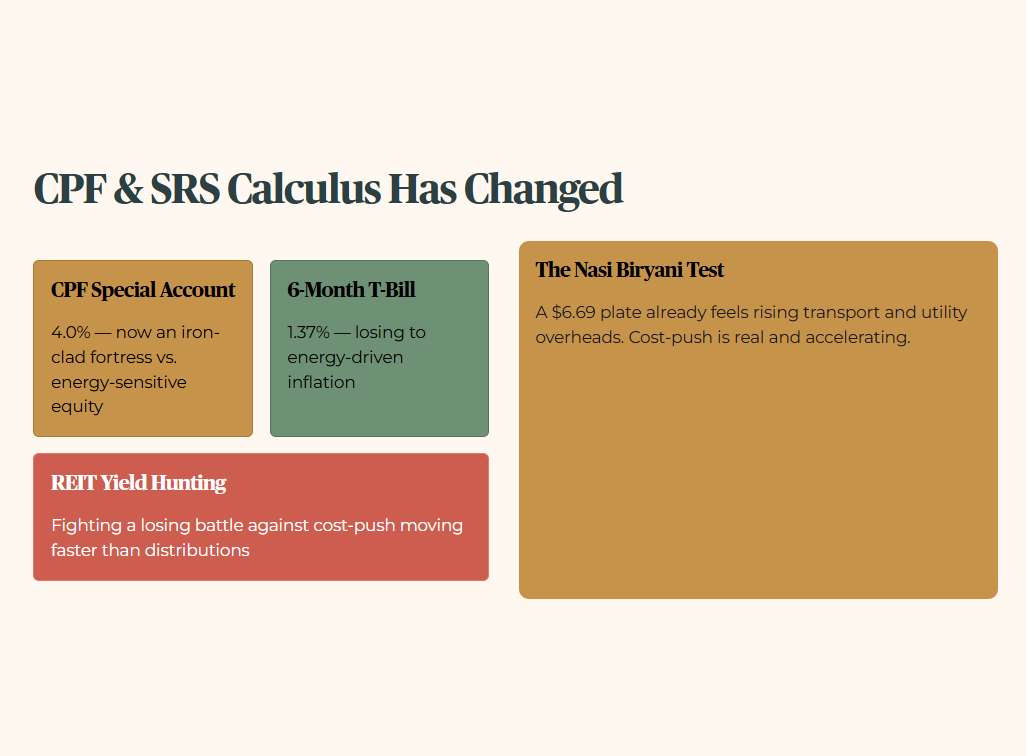

This shift fundamentally changes the CPF and SRS calculus. When six-month T-bills are yielding 1.37 percent, the sanctuary of the CPF Special Account at four percent becomes an iron-clad fortress. The risk-free environment is actually more attractive now because equity exposure in energy-sensitive sectors is becoming high-beta. If you are using SRS funds to hunt for yield in REITs, you are fighting a losing battle against a cost-push environment that is moving faster than your distributions. A plate of nasi biryani that cost six dollars and sixty-nine cents is already feeling the pressure of rising transport and utility overheads.

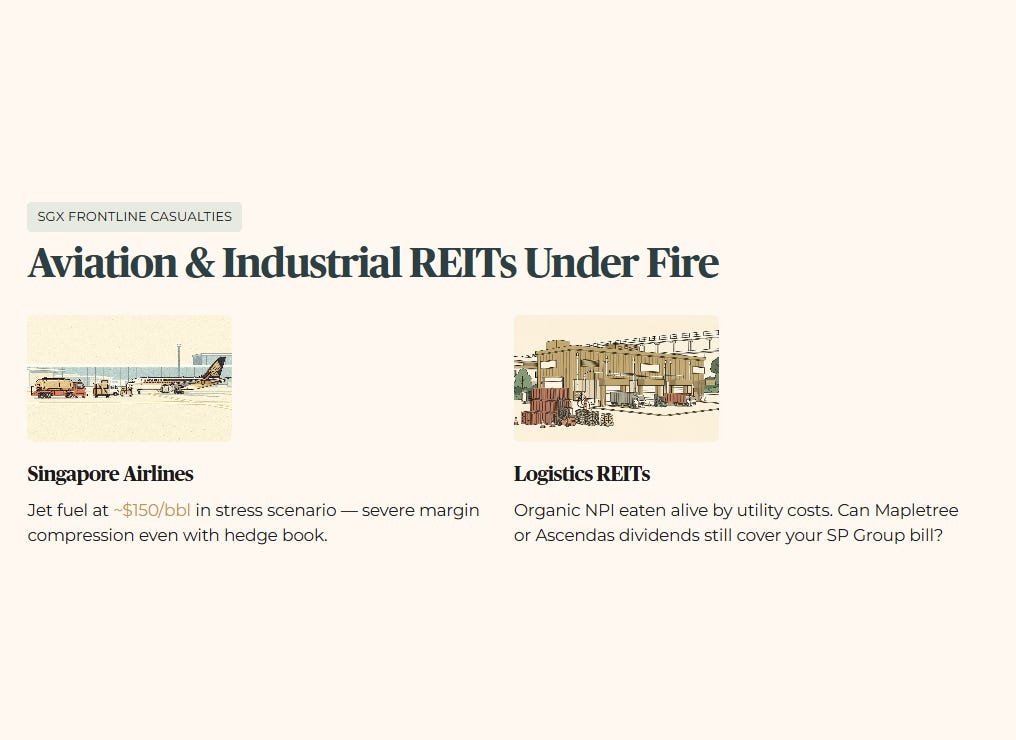

The SGX sector exposure is where the wallet consequence becomes visceral. Aviation and industrial REITs are the frontline casualties. Singapore Airlines is currently managing jet fuel costs against a Brent baseline of around US$102 per barrel. In the forensic stress scenario — Hormuz locked through Q3 — jet fuel prices project toward US$150 per barrel equivalent, a level that would compress SIA’s margin headroom severely even with its current hedge book. Logistics REITs are seeing their organic net property income eaten alive by utility costs. We are not talking about abstract percentages. We are talking about whether the dividend from your Mapletree or Ascendas holdings can still cover your monthly SP Group bill.

Iggy’s Insight

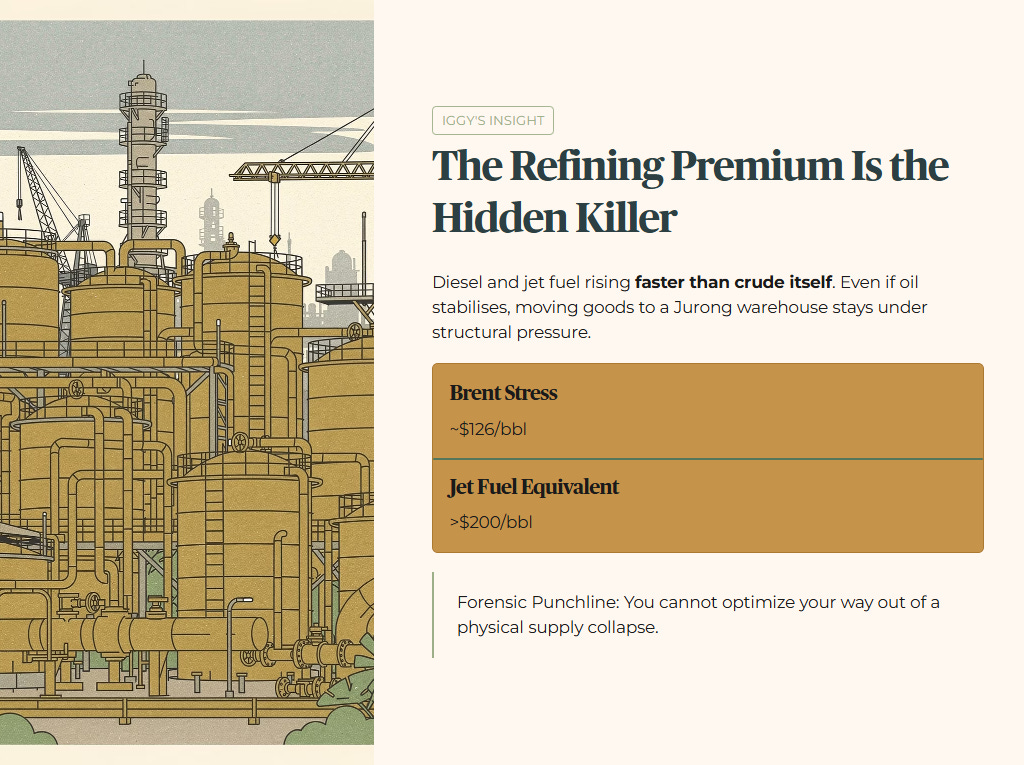

Most retail investors are watching the top-line inflation numbers, but the second-order effect they are missing is the refining premium. In Asia, diesel and jet fuel prices are rising faster than crude itself. This means even if oil stabilises at current levels, the cost of moving goods to a Jurong warehouse remains under structural pressure. In the stress scenario where Brent pushes toward US$126, the refining premium compounds the problem — exceeding US$200 per barrel equivalent for jet fuel and diesel. This is a squeeze on margins that no amount of cost-cutting can fix at the asset level. Forensic Punchline: You cannot optimize your way out of a physical supply collapse.

Section 3: The Data Proof — The Evidence

The forensic verdict is clear. The sanctuary of the CPF Special Account remains the only benchmark providing genuine capital protection while the rest of the yield landscape enters the red zone.

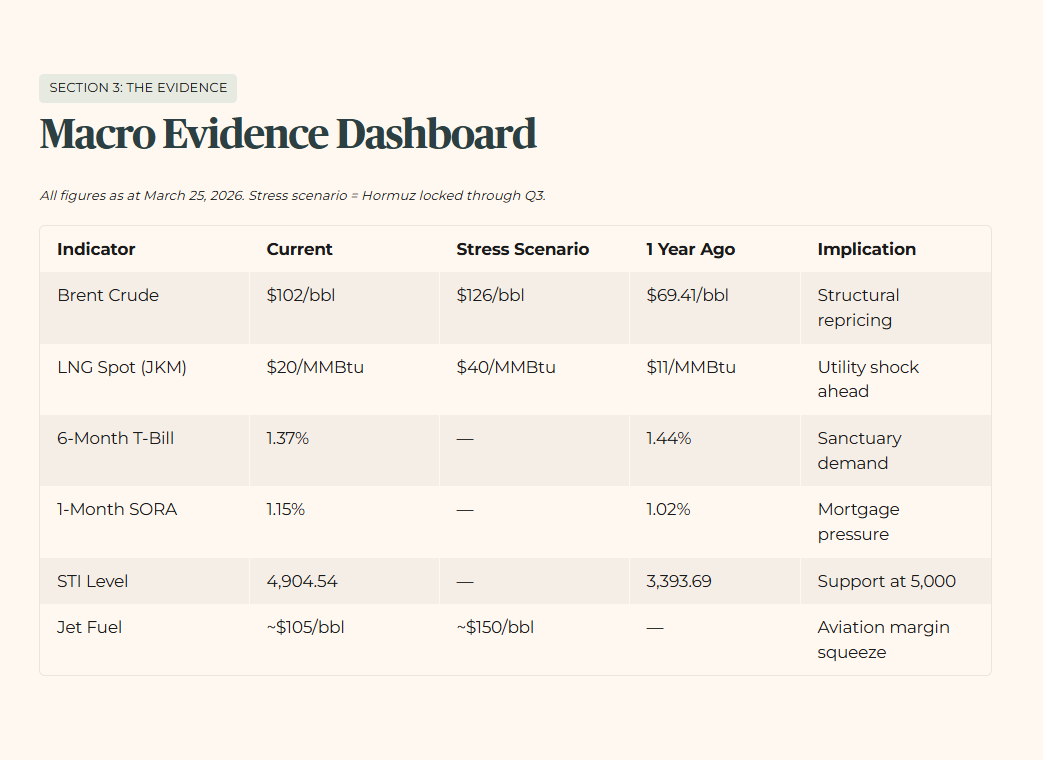

Table 1 — Macro Evidence Dashboard (All current figures as at March 25, 2026. Stress scenario figures reflect Hormuz-locked-through-Q3 projection.)

Note: Stress scenario figures are forensic projections assuming sustained Hormuz disruption through Q3 2026. They are not current spot prices.

The forensic linchpin here is the 1.37 percent yield on the latest six-month T-bill. While institutional money is dashing for cash, this rate is structurally low compared to the 3.2 percent Iggy Forensic Floor. For a fifty-five year old in Marine Parade, this means your safe money in T-bills is actually losing purchasing power against an energy-driven inflation rate that is likely running well above the official 1.4 percent core figure. The only reason to hold T-bills now is for immediate liquidity. For actual retirement growth, the 4.0 percent CPF Special Account is the only asset that is not asking you to take a haircut on your future.

When we look at LNG, the current JKM spot around US$20 per MMBtu is already approximately double year-ago levels. That is the baseline reality. The stress scenario at US$40 — which assumes the Ras Laffan disruption compounds through the second half of the year — would represent a shock four times year-ago levels and would make the utility cost pressure felt in Singapore households and industrial REITs structurally unmanageable without distribution cuts.

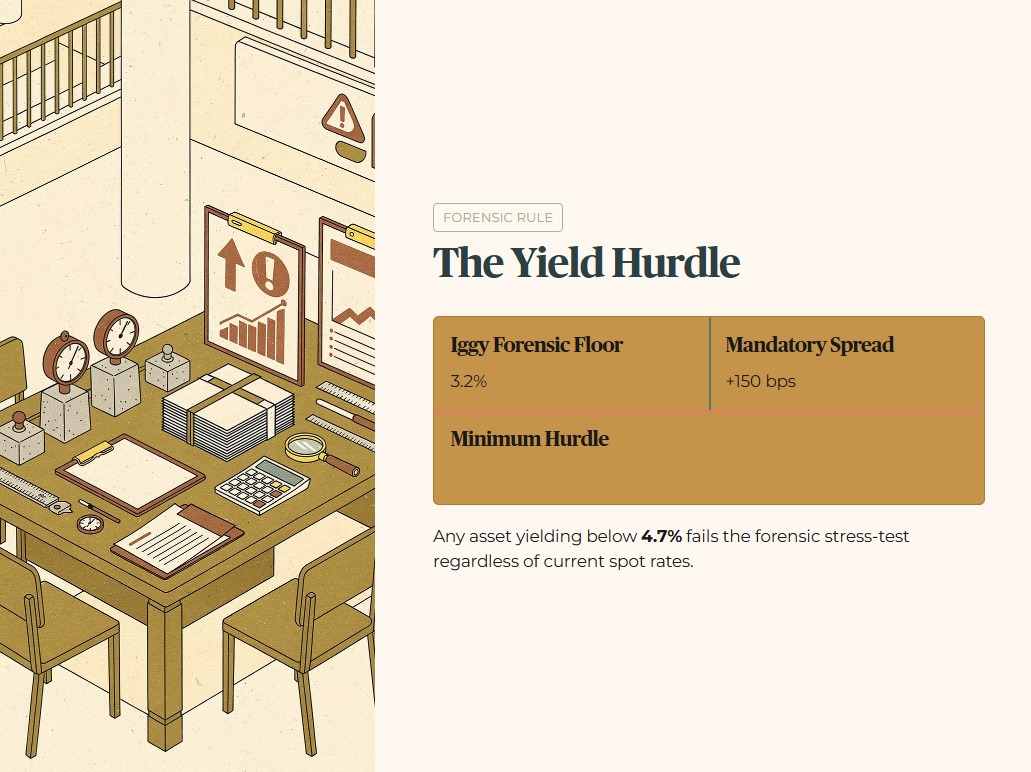

Note on the Stress-Test Buffer: When evaluating yields, the mandatory spread is 150 basis points above the Iggy Forensic Floor of 3.2 percent. This establishes a minimum yield hurdle of 4.7 percent. Any asset yielding below this threshold fails the forensic stress-test regardless of current spot rates.

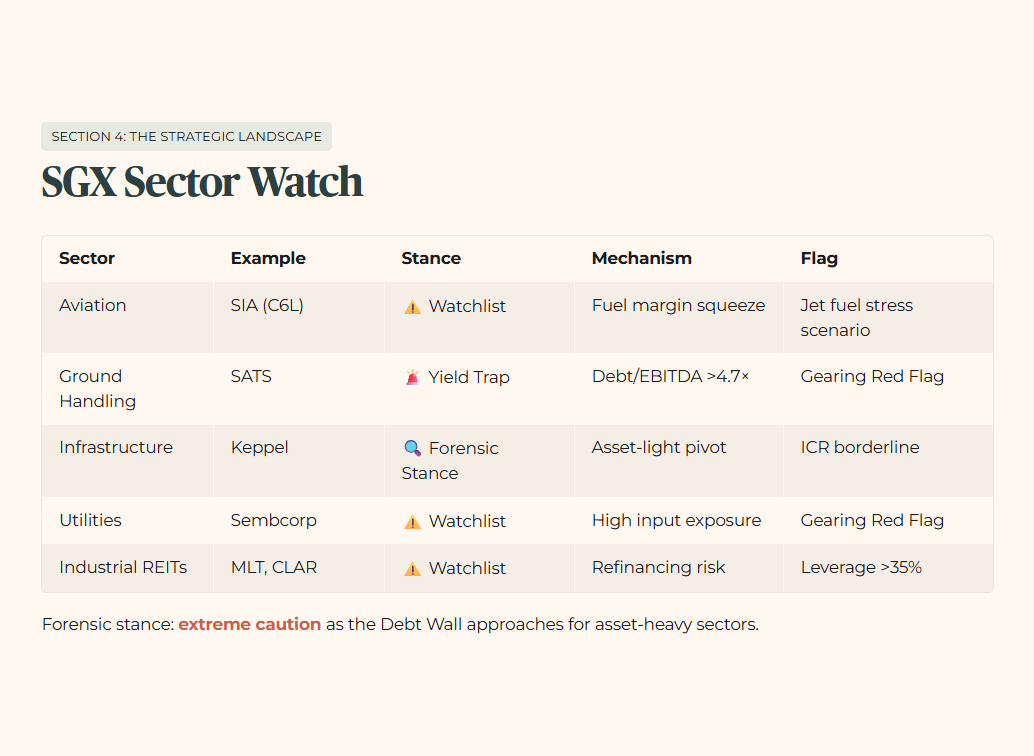

Section 4: The Strategic Landscape

The overarching forensic stance across the SGX is one of extreme caution as the Debt Wall approaches for asset-heavy sectors.

Table 2 — SGX Sector Watch

Table 3 — Macro Scenario Matrix

Forensic Portfolio Stress-Test Questions

This is where I stop talking about the storm and show you the exact 4.7% gearing filter that Elite Investors are using to decide which REITs survive the Debt Wall.