ComfortDelGro, SIA and Keppel: The $100 Oil Verdict for Your Passive Income

Don’t let your SRS account bleed quietly while high oil prices and 1.04% SORA rates crush your transport yields.

THE STRAIT OF HORMUZ SHOCK: AUDITING THE SGX TRANSPORT DEBT WALL

Picture this. You are standing at the neighbourhood Esso station in Toa Payoh on a Tuesday evening. The queue of cars spills out onto the main road, and the uncle at the pump next to you is staring at the RON 95 meter like it has personally insulted his ancestors. The numbers on the digital display are spinning faster than a ceiling fan in a hawker centre. Everyone is complaining about the sheer cost of filling up their Toyota Sienta, pointing fingers at the headlines about the Strait of Hormuz blockade.

While retail investors are busy calculating their monthly petrol budget, the real silent killer is working somewhere quieter. The oil shock guarantees that interest rates stay elevated. And elevated rates are quietly suffocating the operating cash flows of SGX transport counters while structurally collapsing the yield spreads of your favourite dividend-paying assets. This is a macroeconomic pressure test that changes the retirement math for anyone relying on passive income.

In This Article:

A NOTE ON THE STRESS-TEST FLOOR

STEP 1: THE HEALTH CHECK — COMFORTDELGRO (C52)

The Five-Layer Audit — ComfortDelGro (C52)

Financial Health Checklist — ComfortDelGro (C52)

STEP 2: THE WEALTH CHECK — SINGAPORE AIRLINES (C6L)

The Five-Layer Audit — Singapore Airlines (C6L)

Financial Health Checklist — Singapore Airlines (C6L)

STEP 3: THE PRICE CHECK — KEPPEL LTD (BN4)

The Five-Layer Audit — Keppel Ltd (BN4)

Financial Health Checklist — Keppel Ltd (BN4)

STEP 4: THE BOTTOM LINE

The Bull View

The Forensic Verdict

InvestingPro Reality Check

The Verdict

About Iggy & the Elite Investors

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

A NOTE ON THE STRESS-TEST FLOOR

Before we begin the audit, you need to understand the ruler I am measuring against. I apply a conservative forensic floor of 3.2% as the working risk-free benchmark throughout this article.

Yes, the current 6-month T-bill spot rate sits lower than that — but I test against 3.2% because it reflects the historical average CPF Special Account floor your retirement planning was likely built around. If the yield spread holds at 3.2%, the margin of safety is a fortress. If it does not, you are taking equity-level risk for bond-level returns. That is the deal I refuse to accept for my own portfolio, and I will not let you accept it quietly either.

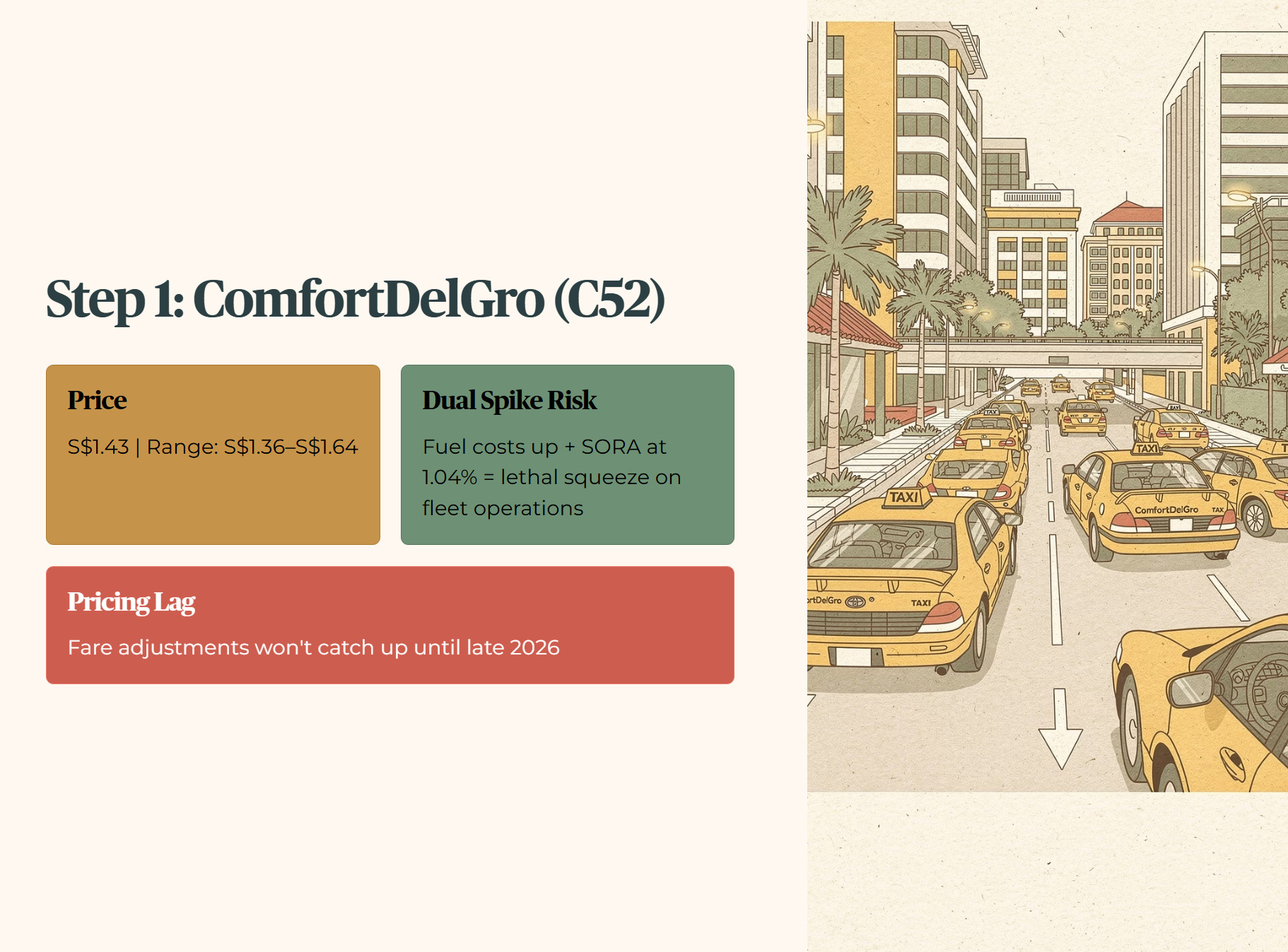

STEP 1: THE HEALTH CHECK — COMFORTDELGRO (C52)

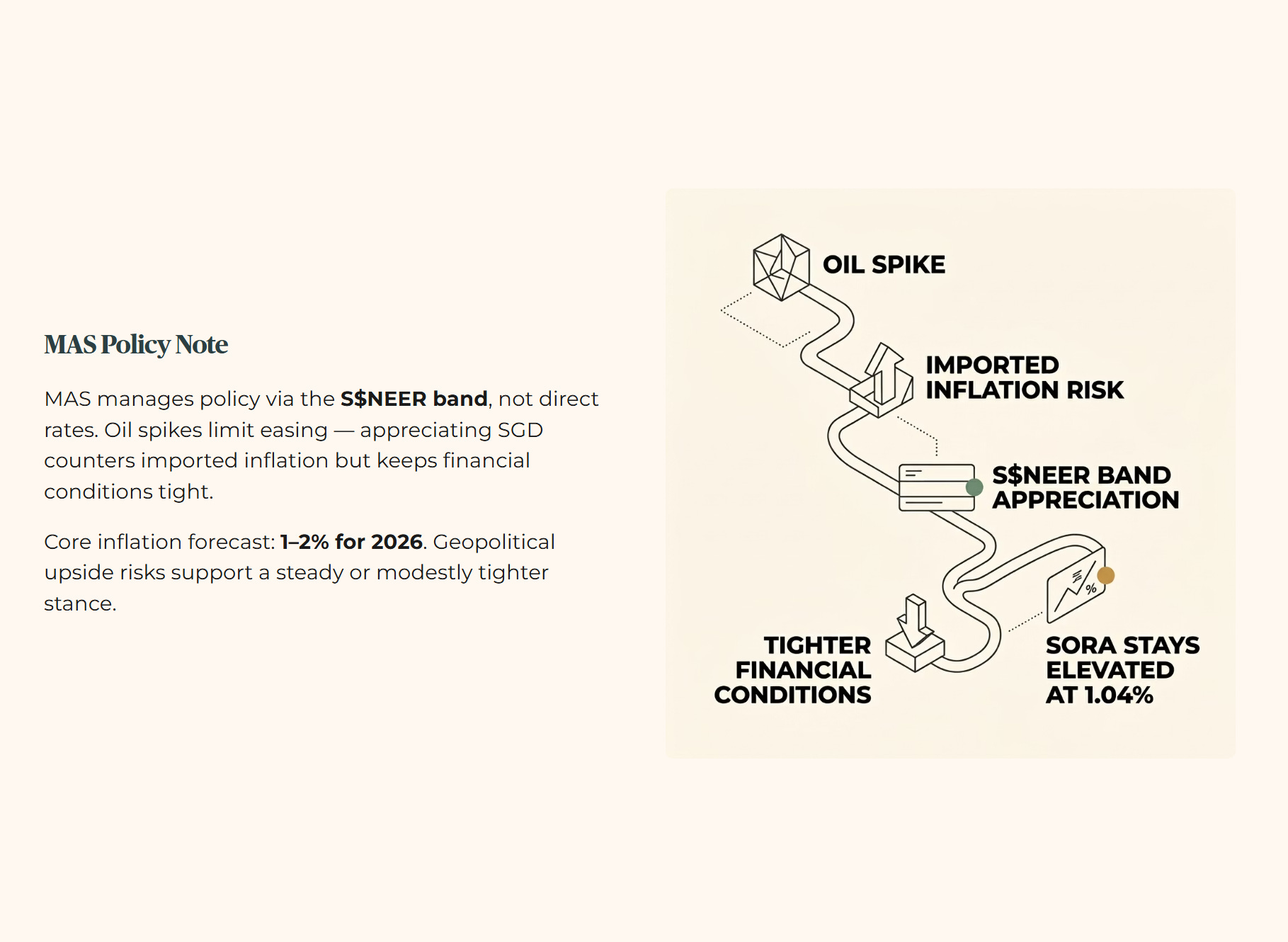

When the Strait of Hormuz effectively shuts down, Brent crude skyrockets. For the Monetary Authority of Singapore, this means zero room to loosen monetary policy. They are forced to keep the Singapore Dollar strong to fend off imported inflation, which keeps SORA elevated — with 1-month SORA currently at 1.04%.

“Don’t overpay for the hype. See the math behind the momentum.” .....Use the Fair Value models I use in every video. Code INVESTINGIGUANA gets you 50% off the world’s most powerful stock screener.

🦎 [Spot Undervalued Gems Here]

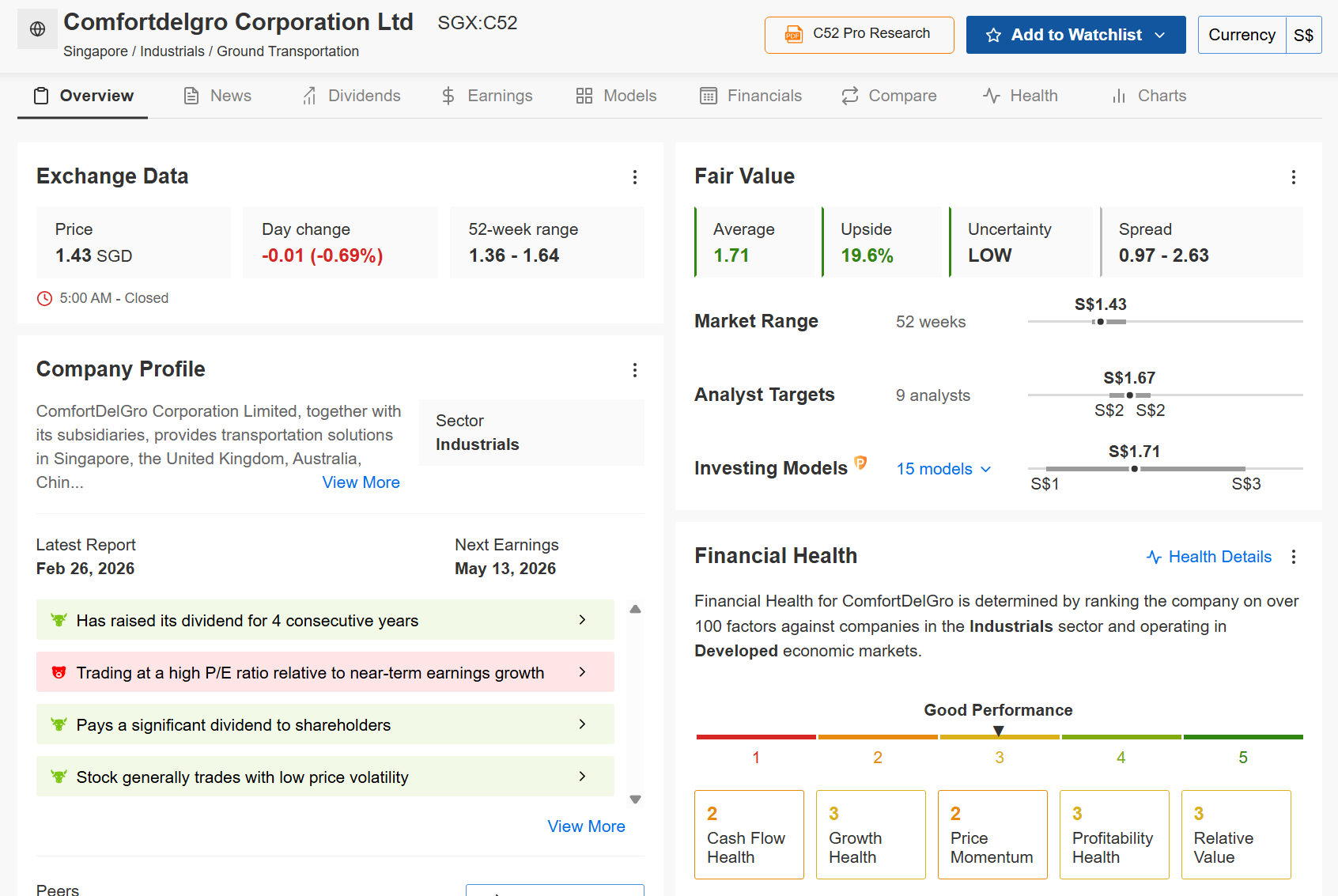

This is where the Debt Wall becomes dangerous. If a transport company needs cheap fuel to run its fleet and cheap debt to finance it, a dual spike in both is lethal. ComfortDelGro (C52) is trading at S$1.43. Their taxi fleet faces an immediate, unhedged spike in fuel costs long before any fare adjustment catches up with reality.

Iggy’s Note: MAS manages policy via the S$NEER band’s slope and level, not direct rates, to target inflation. Oil spikes limit easing options, as appreciating the SGD counters imported costs but keeps financial conditions tighter amid global rate alignments. Recent statements flag upside inflation risks from geopolitics, with core inflation forecasts at 1–2% for 2026, supporting a steady or modestly tighter stance.

The Five-Layer Audit — ComfortDelGro (C52)

Layer 1 (Raw Fact): C52 trades at S$1.43, within a 52-week range of S$1.36–S$1.64.

Layer 2 (Historical Benchmark): C52 has raised dividends for four consecutive years, 2022 through 2025.

Layer 3 (Peer Context): Unlike pure logistics peers, C52 generates predictable daily cash from its bus and rail concessions — but it has limited immediate pricing power when costs spike.

Layer 4 (Forward Scenario): If Brent crude sustains a 10% premium, margins will compress until regulatory fare reviews land in late 2026. That is a long wait with a high payout ratio.

Layer 5 (Wallet Impact): For those holding C52 in an SRS account as a retirement income anchor, a cash flow squeeze directly threatens payout sustainability at the worst possible time.

Financial Health Checklist — ComfortDelGro (C52)

Iggy’s Insight: Do not be fooled by a four-year dividend streak if Cash Flow Health is scoring 2 out of 5. C52 has maintained its payouts by stretching the payout ratio past 83%. In an oil shock environment, that is like driving a taxi with the check-engine light blinking. You can only ignore the fuel gauge for so long before the engine stalls.

STEP 2: THE WEALTH CHECK — SINGAPORE AIRLINES (C6L)

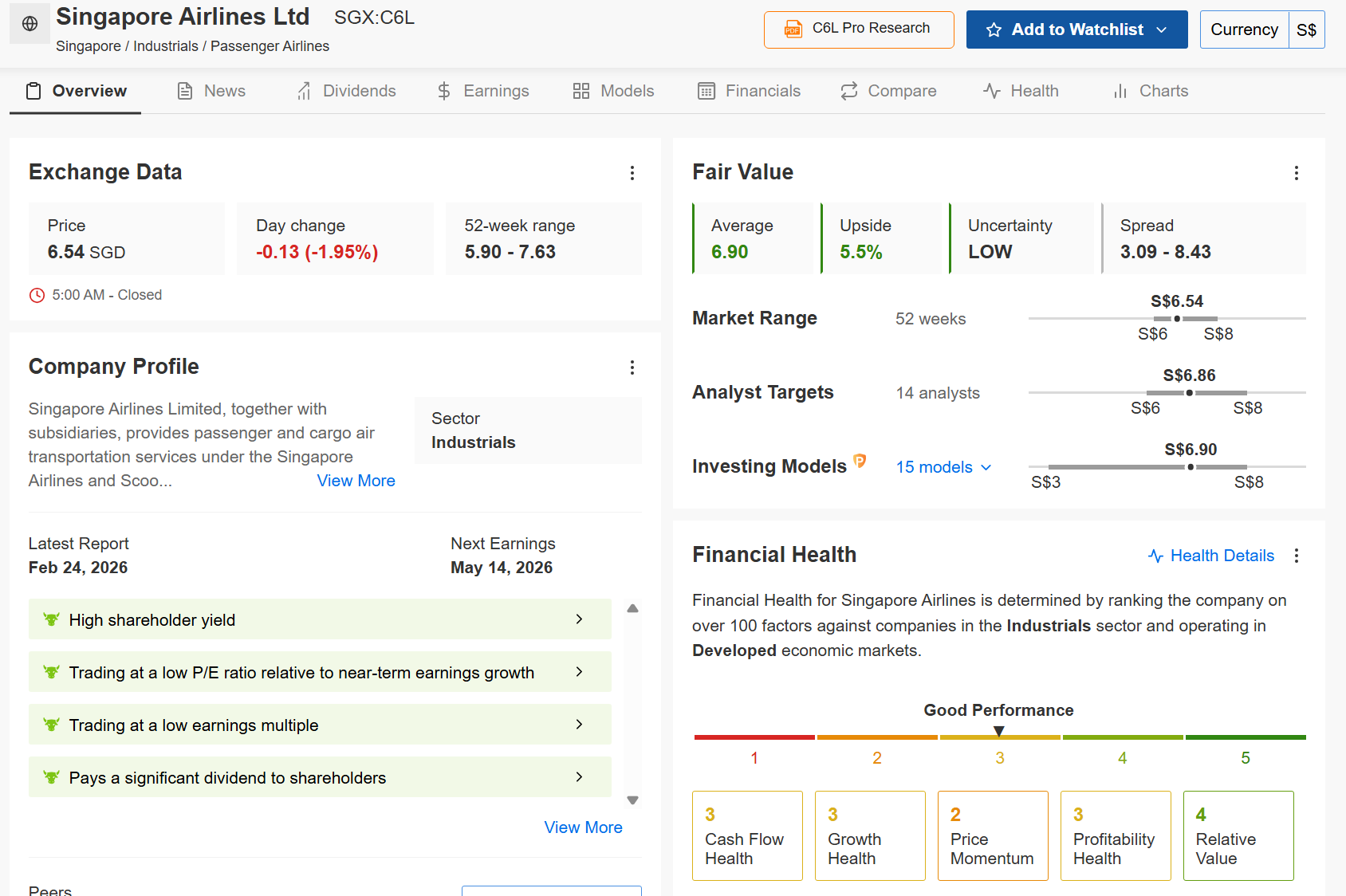

Singapore Airlines (C6L) is trading at S$6.54. Aviation is the ultimate high-stakes game of margin preservation, and this is where the forensic audit gets uncomfortable.

“Don’t overpay for the hype. See the math behind the momentum.” .....Use the Fair Value models I use in every video. Code INVESTINGIGUANA gets you 50% off the world’s most powerful stock screener.

🦎 [Spot Undervalued Gems Here]

The Five-Layer Audit — Singapore Airlines (C6L)

Layer 1 (Raw Fact): C6L trades at S$6.54 within a 52-week range of S$5.90–S$7.63. Fair value is estimated at S$6.90, implying a modest 5.5% upside at current prices.

Layer 2 (Historical Benchmark): C6L’s dividend is highly cyclical, tied directly to global travel volume and load factors — it is not a structural yield play in the way a REIT or telco would be.

Layer 3 (Peer Context): Unlike C52, SIA competes on premium pricing power globally. When fuel costs rise, SIA has more room to pass costs through via fuel surcharges than a regulated bus operator does.

Layer 4 (Forward Scenario): That pricing power has limits. Once current fuel hedges signed in 2025 expire, unhedged exposure bites into free cash flow. The question is not whether margins compress — it is by how much.

Layer 5 (Wallet Impact): At S$6.54 with a cyclical dividend structure, the yield spread against our 3.2% forensic floor is already thin. You are accepting equity-level volatility without equity-level yield compensation.

Financial Health Checklist — Singapore Airlines (C6L)

Iggy’s Insight: The health profile here is more nuanced than C52. Cash flow, growth, and profitability all pass the minimum threshold. Relative value is actually strong at 4 out of 5. The red flag is Price Momentum at 2 out of 5 — the market is telling you something about near-term direction. With next earnings on 14 May 2026, this is a name to watch rather than chase.

Keppel is the one counter here that looks like a “safe bet” in an oil shock—but once you run the same 5-layer audit on it, you’ll see exactly why chasing it now can turn a retirement “sanctuary” into a slow-motion yield trap.