Hormuz Strait Closed Means Your Power Bill Jumps 20% Soon

A standard HDB flat faces $30 to $50 extra every month from July while SIA and ComfortDelGro dividends face margin cuts from the same fuel spike

The Strait Has Closed: What the Hormuz Blockade Means for Your SGX Portfolio

The Global Headline

Every major port city in history has faced the same existential question: what happens when the trade route is abruptly severed? Malacca asked it in the sixteenth century when colonial powers redrew the maps. Rotterdam asked it when containerisation rewrote European logistics. Singapore is answering that question right now, not as a theoretical exercise, but as an active crisis cascading through the maritime corridors of Southeast Asia.

In This Article:

The Local Impact

The Data Proof

The Forensic Sector Read

The Singapore Investor Playbook

The Red Flags Were Always There

The Forensic Conclusion

Iggy’s Forensic Compliance Standards — Standard Disclaimer

Strait Re-Closed

On 18 April 2026, the Strait of Hormuz was officially re-closed by Iran. Iran cited a continuous naval blockade that entirely negated a brief, twenty-four-hour window of promised maritime passage. This geographic chokepoint is no longer a distant geopolitical abstraction. For a fifty-eight-year-old retail investor in Singapore relying on Supplementary Retirement Scheme funds heavily allocated toward transport and utility equities, this closure is a direct and present threat to the income floor of your portfolio.

The press release narrative pushed just a day prior by diplomats projected a waterway completely open and ready for business following a regional ceasefire in Lebanon. The raw data reality tells a different story. Ship-tracking forensics and stark warnings from shipping associations about uncleared mine threats within the traffic separation scheme prove that the opening was a tactical mirage. The gap between those two narratives is exactly where retail capital is currently being trapped.

🦎 Iggy’s Insight

Institutional capital rarely waits for the news to confirm what the freight insurance rates already show. The psychological gap we are witnessing right now is the space between the official diplomatic optimism broadcast on television and the physical reality of crude tankers turning around in the Gulf. Retail investors are buying the headline of a stabilised Middle East, while the smart money is quietly modelling a protracted maritime blockade.

The consensus narrative assumes a temporary supply chain glitch, but the physical market is pricing in a structural fracture. The headline tells you the trade route is safe; the premiums tell you the route is uninsurable. This is the mispricing of distance.

The Local Impact

The macro reality of a severed maritime corridor eventually lands on the domestic balance sheet. This is where the regional shift translates directly into the Singaporean wallet. The cost of living impact is moving faster than the official data suggests, bypassing the geographic moats we usually rely on.

In Bedok and Toa Payoh, households have already absorbed a 2.1 percent increase in SP Group electricity tariffs in April. But that is merely the preamble to a much larger structural shift. Ninety-five percent of Singapore’s power generation is indexed to natural gas, which trails crude oil pricing through a two-and-a-half-month rolling average. The true cost of this blockade will manifest as a much sharper tariff increase in the July to September billing window. We project a domestic utility overhead surge of 15 to 20 percent. That translates to an actual, unavoidable expense expansion of $30 to $50 per month for a standard household. It fundamentally alters the baseline cost of maintaining a home in Singapore.

On the surface that makes sense. But here is the uncomfortable truth: the very assets you rely on to pay those rising utility bills are facing their own margin compression from the exact same energy shock. This forces a strict re-evaluation of the Supplementary Retirement Scheme calculus. When domestic inflation accelerates, the risk-free environment must be measured rigorously against the real yield of equity exposure. The CPF Special Account currently offers a 4.0 percent sanctuary benchmark, providing absolute capital protection. Against that risk-free floor, deploying retirement capital into equities requires a substantial and secure premium. Right now, a fuel-exposed transport stock represents a high opportunity cost for a mature investor trying to defend their purchasing power.

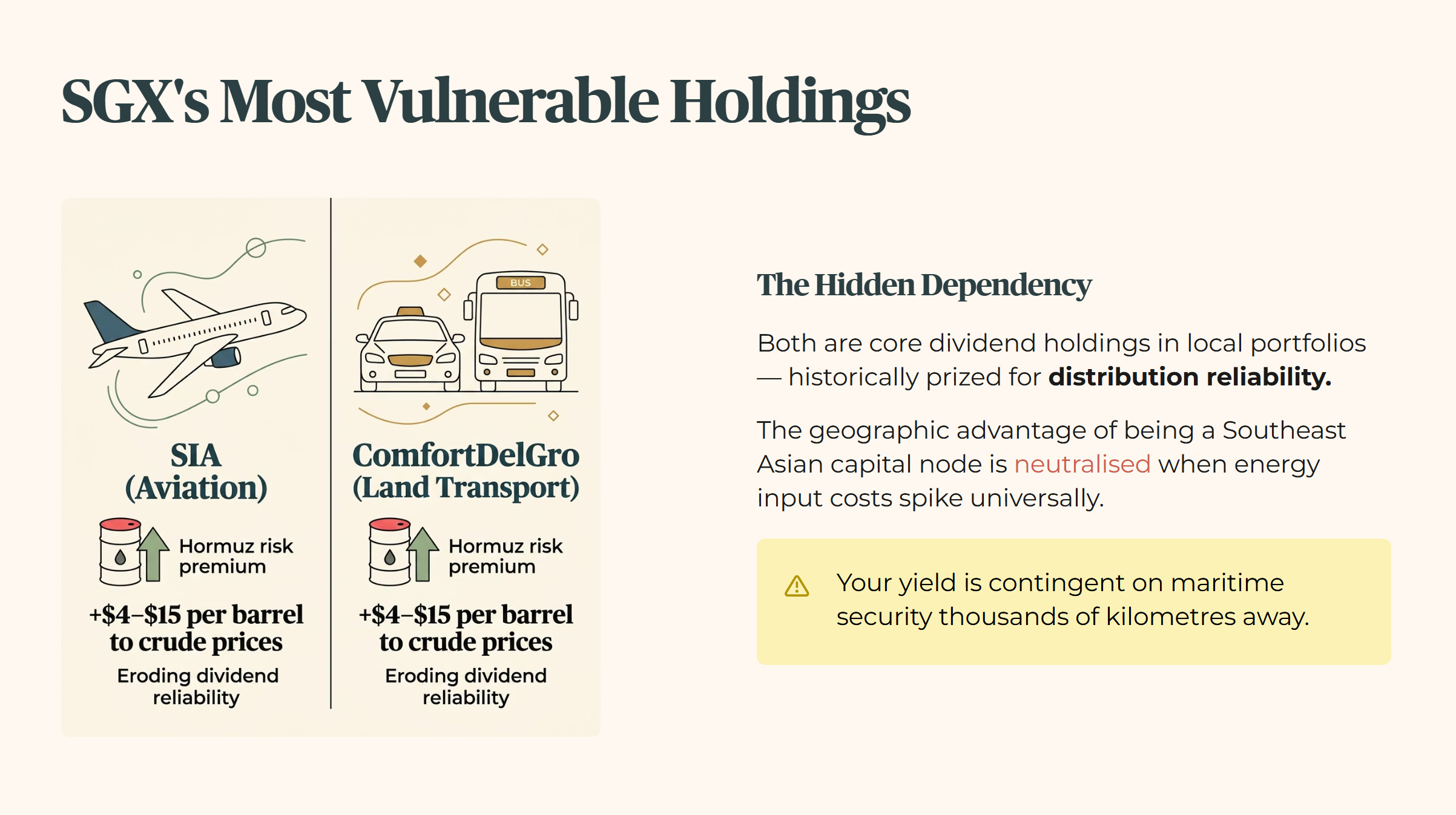

The SGX sector exposure most vulnerable to this corridor disruption sits squarely in transport and utilities. Singapore Airlines and ComfortDelGro represent core holdings in countless local dividend portfolios, historically prized for their distribution reliability. Yet both entities are now operating in an environment where the Hormuz risk premium adds a volatile variable of $4 to $15 per barrel to crude prices. The geographic advantage of being a Southeast Asian capital node is neutralised when the input cost of energy spikes universally. The yield you thought was secured by domestic consumer demand is actually contingent on maritime security thousands of kilometres away.

You’ve just seen how a $4 to $15 Hormuz premium bleeds straight into SIA and ComfortDelGro margins — but the next section walks through the exact 37 percent profit cut and yield coverage math that decides whether those dividends still clear your CPF-SA sanctuary floor.