How to Optimise Your SRS Account (The Forensic Singapore Retirement Guide)

Most Singaporeans turning 55 this year will leave S$47,000 in compounding returns on the table by making one avoidable SRS decision.

How to Optimise Your SRS Account (The Forensic Singapore Retirement Guide)

Most Singaporeans turning 55 this year will leave S$47,000 in compounding returns on the table by making one avoidable SRS decision.

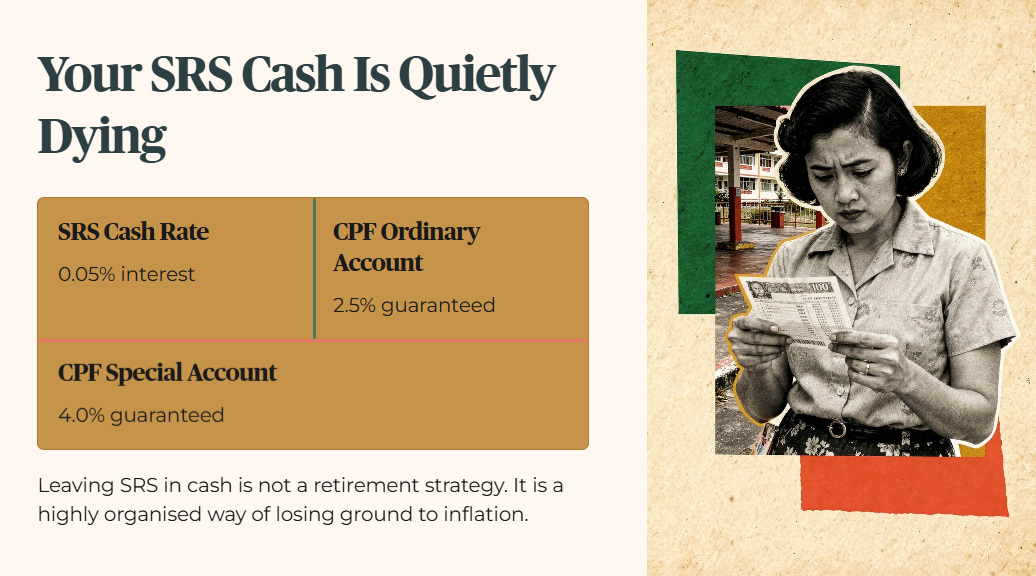

Every year, tens of thousands of Singaporeans deposit money into their Supplementary Retirement Scheme (SRS) account, take the immediate tax relief, and then do absolutely nothing. That cash sits in the account earning 0.05% interest at the bank. For context, your CPF Ordinary Account pays 2.5% and your Special Account pays 4.0% guaranteed. Leaving your SRS in cash is not a retirement strategy. It is a highly organised way of losing ground to inflation.

If you are between 45 and 65, treating your SRS account as a simple tax receipt rather than an active investment vehicle is costing you thousands of dollars. This forensic guide will show you exactly how the SRS framework works, identify the three fatal mistakes heartland investors make, and give you a clear, numbers-driven plan to turn your tax shelter into a compounding sanctuary.

Before we get into the numbers, I want to say who I am doing this for. Not the trader with a twenty-year runway. Not the growth chaser hunting the next ten-bagger. I am doing this for the retiring and retired Singaporean who needs their capital to work reliably — not spectacularly.

In This Article:

What SRS Actually Is (And What It Is Not)

The Three Fatal SRS Mistakes

The Pivot: What You Should Be Doing With SRS Funds

The SRS Investment Framework

The Worked Example (The Live Case Study)

Strategic Considerations

Disclaimers

1. What SRS Actually Is (And What It Is Not)

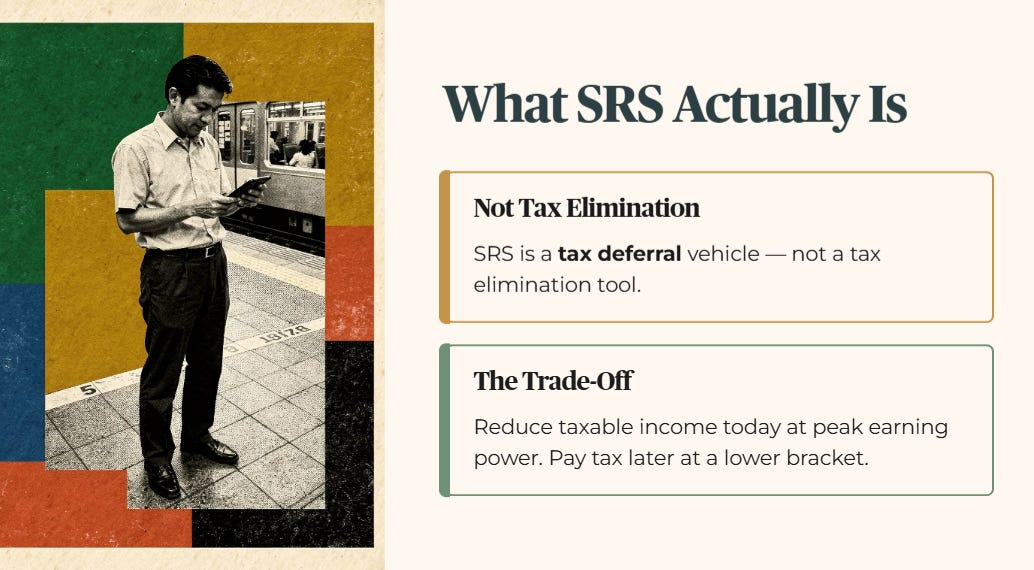

The Supplementary Retirement Scheme (SRS) is a voluntary programme designed to complement your CPF savings. But many retail investors misunderstand its core nature. SRS is not a tax elimination tool. It is a tax deferral vehicle. You reduce your taxable income today when your earning power is at its peak. In return, you agree to pay tax on those withdrawals later in life when you are in a lower or zero tax bracket.

For Singapore citizens and Permanent Residents (PRs), the annual contribution limit is S$15,300. For foreign workers, the limit is S$35,700. Every dollar you contribute reduces your taxable income by one dollar for that year, up to an overall personal income tax relief cap of S$80,000 across all relief categories.

The real magic does not happen when you put the money in. It happens when you take the money out.

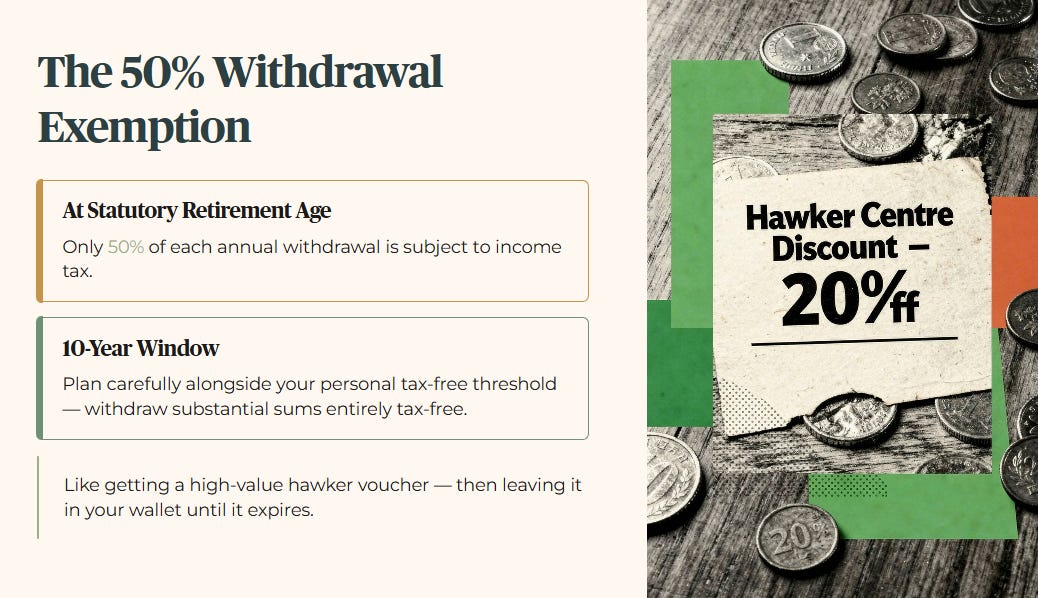

When you reach the statutory retirement age (the age at which your SRS withdrawals become eligible for the 50% tax exemption) that applied when you made your first SRS contribution, you unlock a 50% tax exemption. That means when you withdraw your savings during the permitted 10-year window, only half of the annual distribution amount is subject to income tax. If you plan your withdrawals carefully alongside your personal tax-free threshold, you can pull substantial sums out of your SRS account entirely tax-free.

Leaving your SRS contributions in cash is like getting a high-value discount voucher for your favourite hawker centre, walking home, and leaving it in your wallet until it expires. You did the hard work of getting the voucher. You failed to extract any real value from it.

Table 1 — SRS Contribution and Tax Relief Reference

2. The Three Fatal SRS Mistakes

Forensic analysis of heartland retirement portfolios reveals three systemic errors that ruin the structural benefits of the SRS framework.

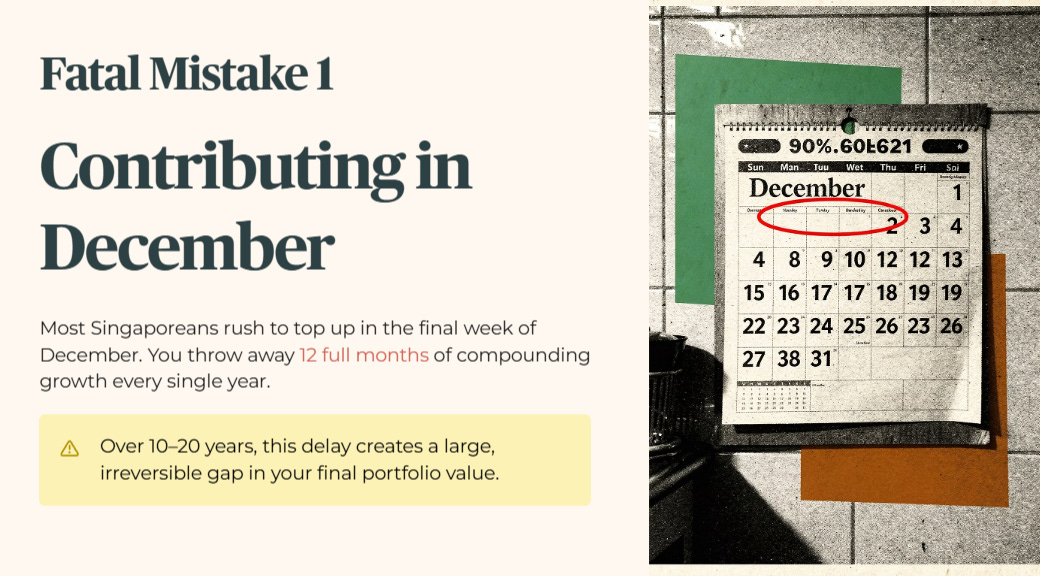

Mistake 1: Contributing in December Instead of January

Most Singaporeans rush to top up their SRS accounts in the final week of December to meet the deadline for that year’s tax assessment. By treating SRS as an end-of-year afterthought, you throw away 12 full months of potential compounding growth every single year. Over 10 or 20 years, this delay creates a large, irreversible gap in your final portfolio value.

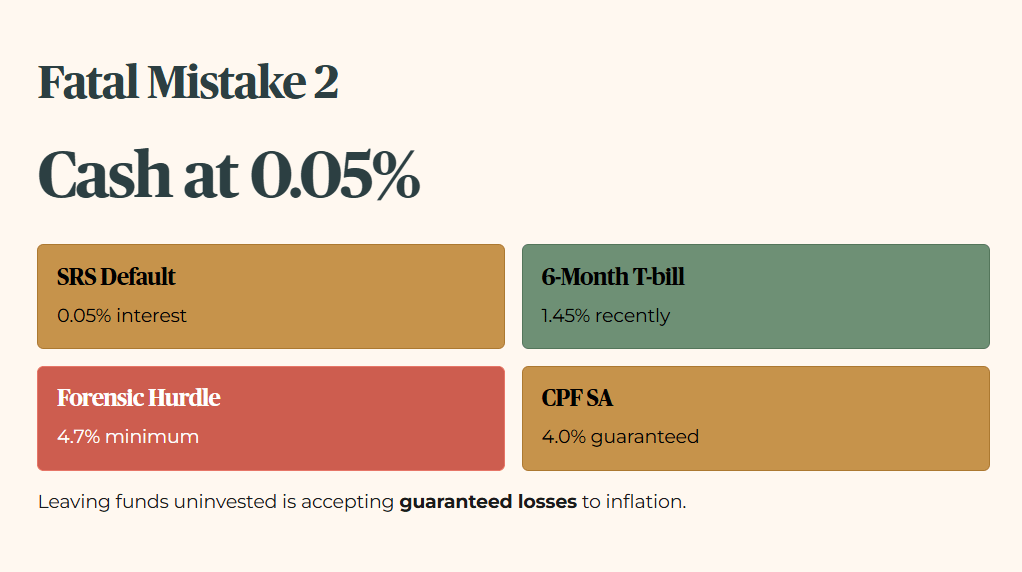

Mistake 2: Leaving the Balance in Cash at 0.05%

This is the single biggest act of wealth destruction in the Singapore retirement landscape. The bank accounts holding your SRS capital pay just 0.05% interest. Your CPF Special Account pays 4.0% guaranteed. Even a 6-month Singapore Treasury bill (T-bill) recently paid 1.45%. But that still fails my personal 4.7% yield hurdle — the minimum return I require before any investment justifies stepping away from guaranteed CPF rates. By leaving your funds uninvested, you are accepting guaranteed losses to inflation.

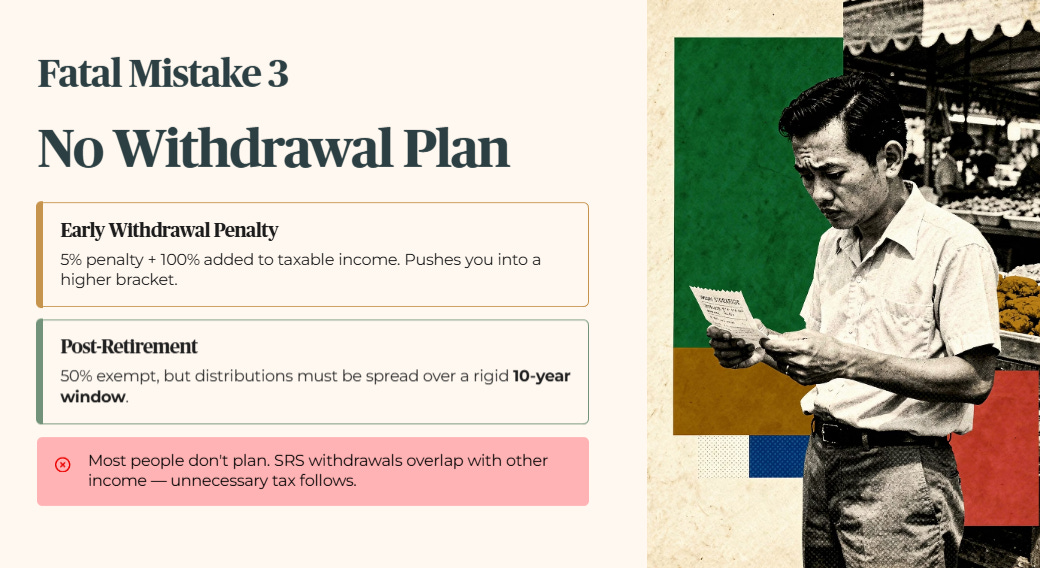

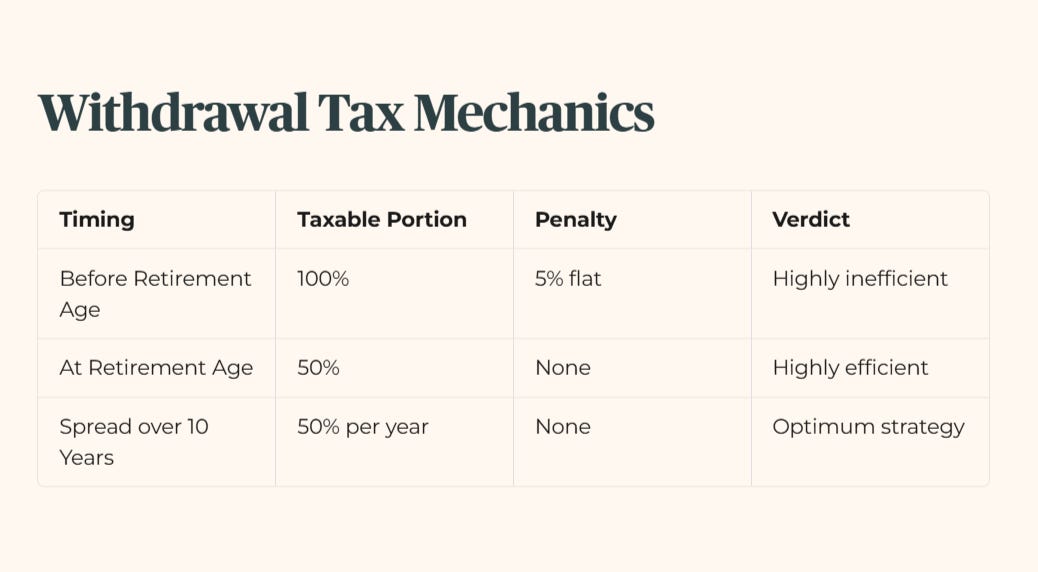

Mistake 3: Failing to Plan the Withdrawal Architecture

The rules for SRS withdrawals are intentionally rigid. If you withdraw any funds before reaching your statutory retirement age, you pay a 5% penalty on the entire withdrawal amount. On top of that, 100% of that early withdrawal is added to your taxable income for that year, pushing you into a higher tax bracket. After you reach retirement age, your distributions are 50% tax-exempt and must be spread carefully over a rigid 10-year window. Most people do not plan this timeline. They end up paying unnecessary tax when their SRS withdrawals overlap with other income.

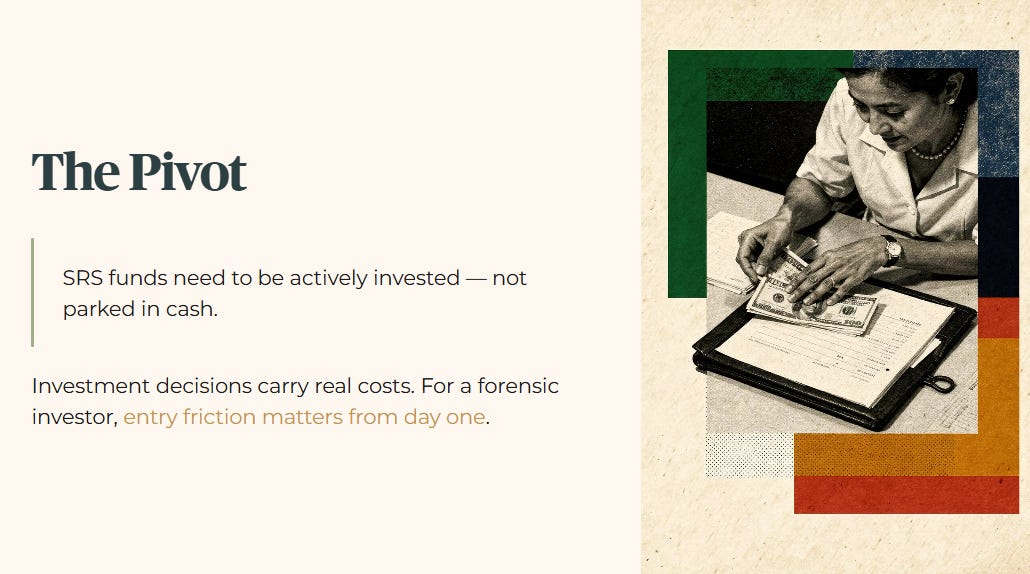

3. The Pivot: What You Should Be Doing With SRS Funds

The fix is simple. SRS funds need to be actively invested, not parked in cash. But investment decisions carry real costs. For a forensic investor, entry friction matters from day one.

Sponsored: Longbridge Singapore

In the world of dividend investing, we spend a lot of time talking about the yield spread — the difference between what a stock pays you and the risk-free rate. But there is a hidden leak that most retail investors completely ignore: transaction friction. If you are deploying S$10,000 into a Singapore REIT, and your broker eats a chunk of that in minimum commissions or platform fees, you are starting your investment in the red before you have even bought a single share.

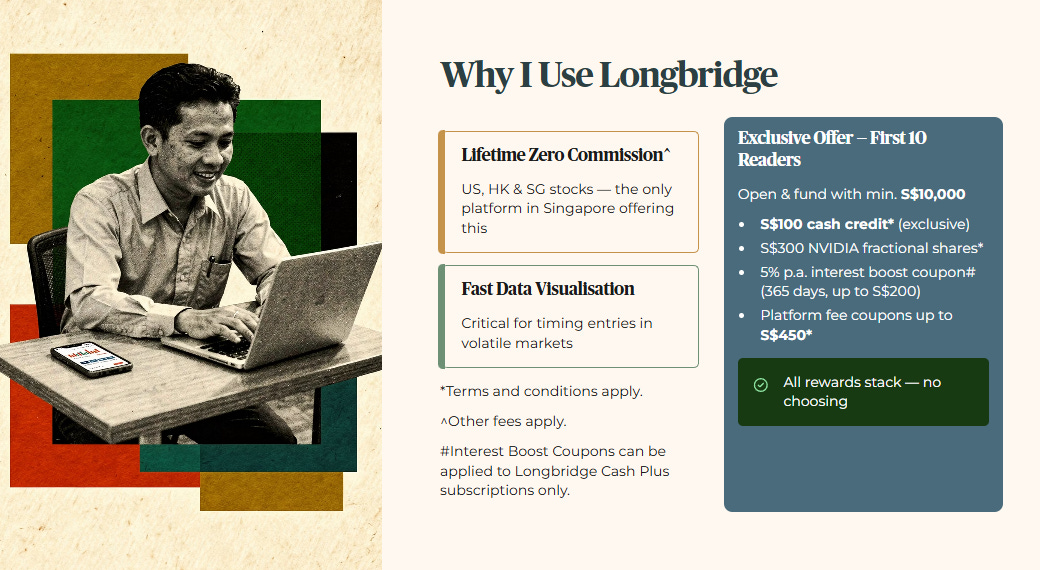

Data is only useful if you have the tools to act on it without getting eaten alive by those fees. That is why I use Longbridge. They are currently the only platform in Singapore offering lifetime zero commission^ for US, Hong Kong, and Singapore stocks. Their data visualisation is also some of the fastest I have used, which is critical when you are timing an entry in a volatile market.

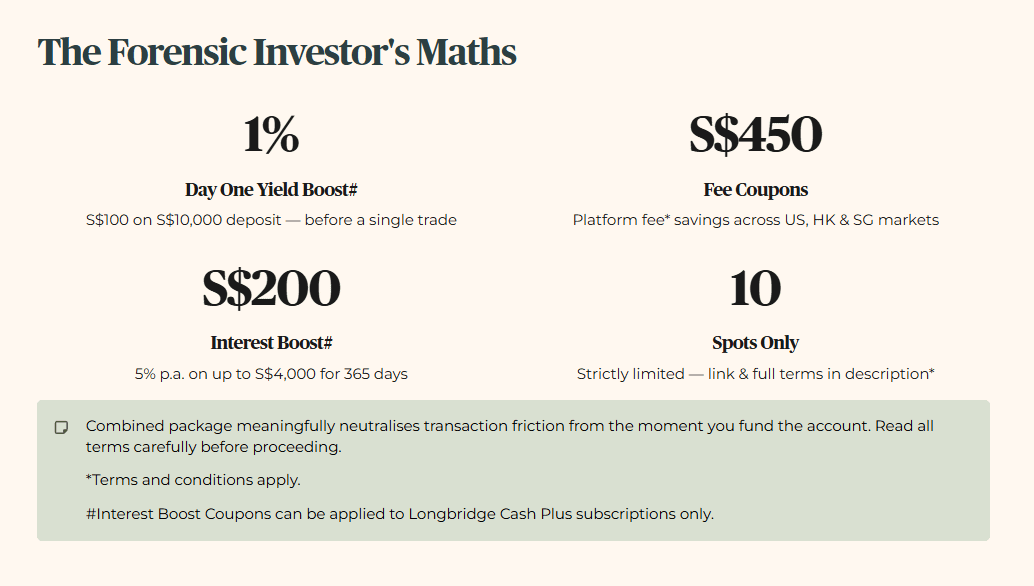

To help you plug that leak, I have partnered with Longbridge on an exclusive arrangement for my readers. For the first 10 readers who open and fund an account with a minimum of S$10,000, Longbridge is offering a direct S$100* cash credit on top of their already generous June welcome rewards.

Here is what the full package looks like if you deposit S$10,000, hold it for 90 days, and complete 5 buy trades. You receive the exclusive S$100 cash credit. You receive S$300 worth of NVIDIA fractional shares. You receive a 5% per annum interest boost coupon valid for 365 days on deposits up to S$4,000 — worth up to S$200 over the year. And you receive platform fee coupons worth up to S$450 across US, Hong Kong, and Singapore markets. All of these stack together. You do not have to choose between them.

Why does this math matter to a forensic investor? Because S$100 on a S$10,000 deposit is an immediate 1% Day One Yield Boost before you have executed a single trade. Combined with the interest boost coupon# and platform fee savings, the total welcome package meaningfully neutralises transaction friction and protects your margin of safety from the moment you fund the account.

This is strictly limited to the first 10 spots. The link and full terms are in the description. Other fees and terms and conditions apply, so read those carefully before you proceed. But for a forensic investor who cares about entry cost and yield from day one, this is worth five minutes of your time.

4. The SRS Investment Framework

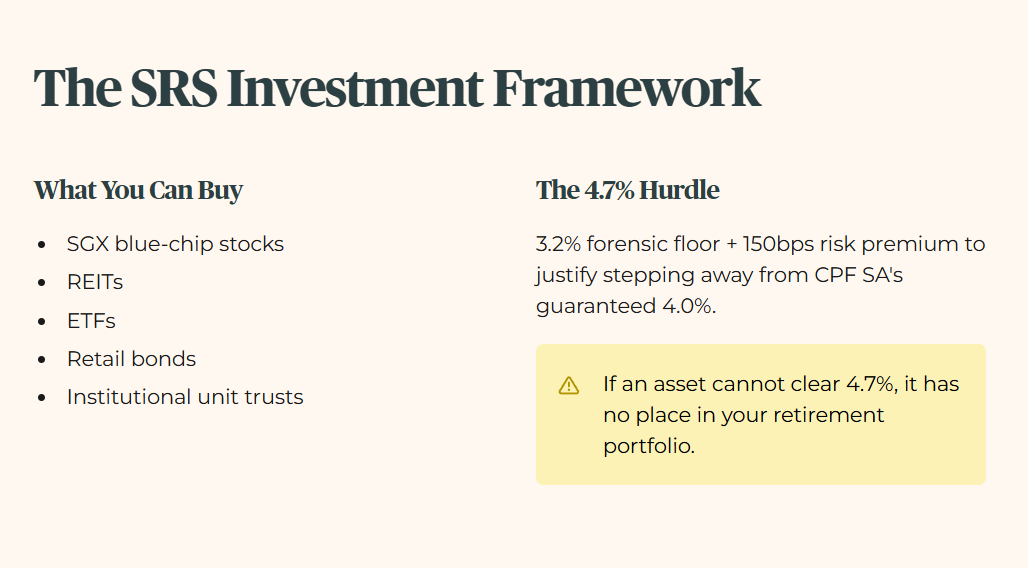

Once your capital is inside the SRS ecosystem, you have a range of investment choices. You can buy SGX-listed blue-chip stocks, Real Estate Investment Trusts (REITs), Exchange Traded Funds (ETFs), retail bonds, and institutional unit trusts. You cannot use SRS funds for CPF-approved instruments that require Ordinary Account or Special Account capital.

From a forensic standpoint, my mandatory 4.7% minimum yield hurdle applies to your SRS capital just as it applies to your cash portfolio. This 4.7% is not an arbitrary number. It is the 3.2% forensic floor plus a 150 basis point risk premium to justify stepping away from the guaranteed 4.0% risk-free return of the CPF Special Account. If an asset cannot reliably clear 4.7%, it has no place in your retirement portfolio.

🦎 Iggy’s Insight Block 1

The single biggest optimisation error heartland investors make is treating SRS as a standalone tax hack instead of integrating it with their CPF balances. They happily take a S$2,000 tax saving today but ignore the fact that their idle SRS cash loses 3.5% in real purchasing power every year compared to the risk-free CPF alternative. Over 15 years, that uninvested capital completely wipes out the initial tax relief. Your retirement architecture is a unified machine. Every dollar sitting at 0.05% is a structural failure. Build for long-term yield, not just immediate tax gratification.

To execute this, you need to know where you sit in the investor lifecycle.

The Accumulator Profile (Ages 45–54)

In this phase, your main goal is maximising yield-to-risk efficiency. Your capital needs to work hard because you still have time for compounding growth. Shift your contribution timing from December to January. Focus your asset selection on balance sheets that generate sustainable distributions above the 4.7% yield hurdle.

The Drawdown Investor Profile (Ages 55–65)

Once you cross age 55, the retirement planning conversation shifts from accumulation to precise sequencing. The CPF Board creates your Retirement Account (RA) using funds from your OA and SA up to the Full Retirement Sum (FRS) of S$220,400 for members turning 55 in 2026. At this stage, you must map out your SRS withdrawal timeline before you hit your statutory retirement age. Calculate how to distribute your SRS balances over the 10-year window so your combined income covers your expenses without pushing you into a higher tax bracket.

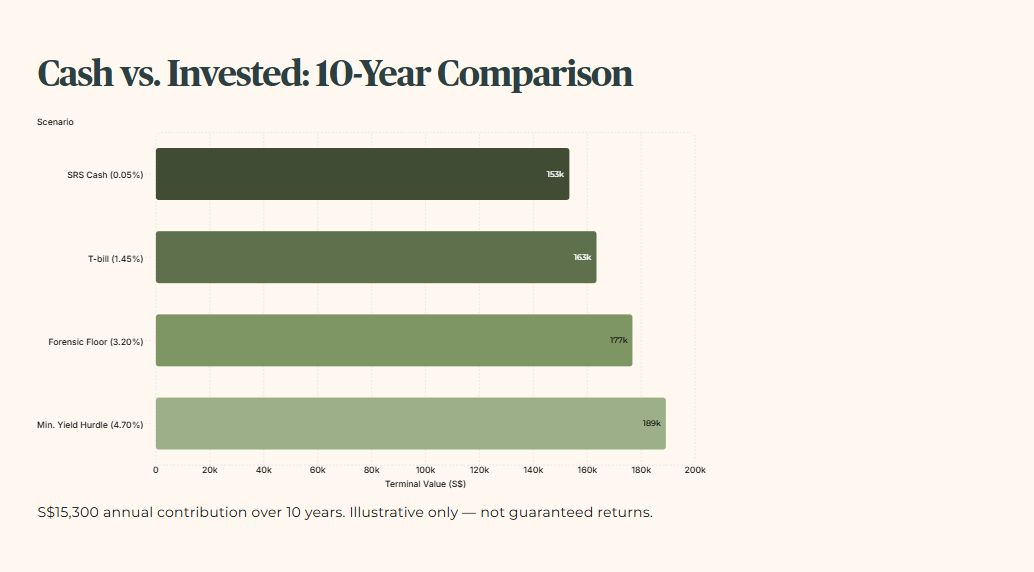

Table 2 — SRS Cash vs. Invested: 10-Year Illustrative Comparison

Note: All figures in Table 2 are strictly illustrative and do not represent guaranteed market returns. Capital values are rounded to the nearest whole dollar.

Table 3 — SRS Withdrawal Tax Mechanics

5. The Worked Example (The Live Case Study)

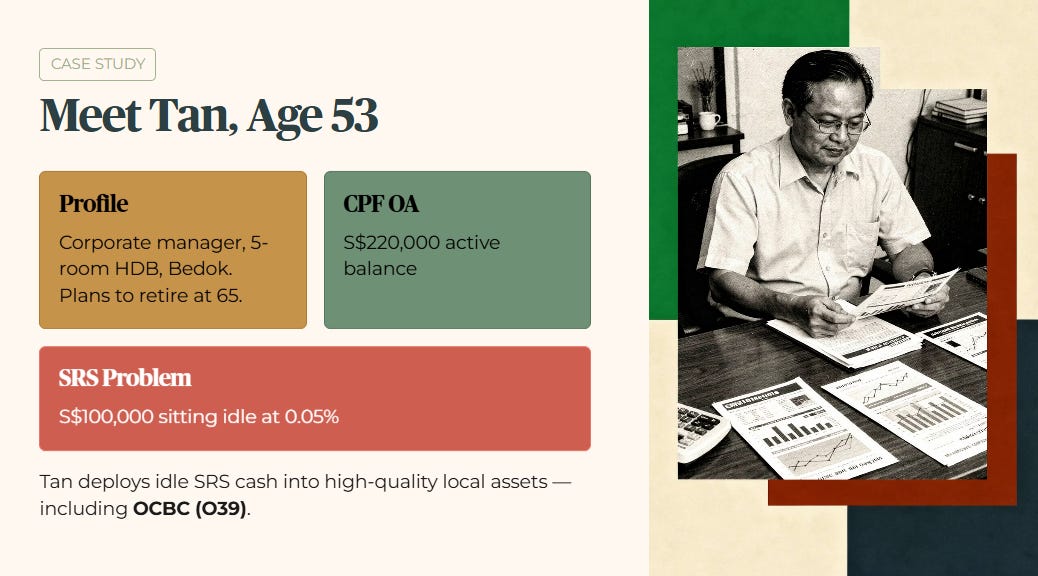

Let us examine Tan, a 53-year-old corporate manager living in a 5-room HDB flat in Bedok. Tan is a hypothetical investor constructed to illustrate how the SRS framework works in practice — the numbers are realistic but not drawn from any real individual’s portfolio. He plans to stop full-time work at age 65. He has an active CPF Ordinary Account balance of S$220,000 and maxes out his annual SRS contribution at S$15,300. He also holds a personal dividend income portfolio of local blue-chip equities and prime industrial REITs.

Currently, Tan has S$100,000 sitting idle inside his SRS account, earning 0.05%. To fix this, Tan decides to deploy his idle SRS cash into high-quality local assets. He allocates part of his capital to OCBC (Ticker: O39).

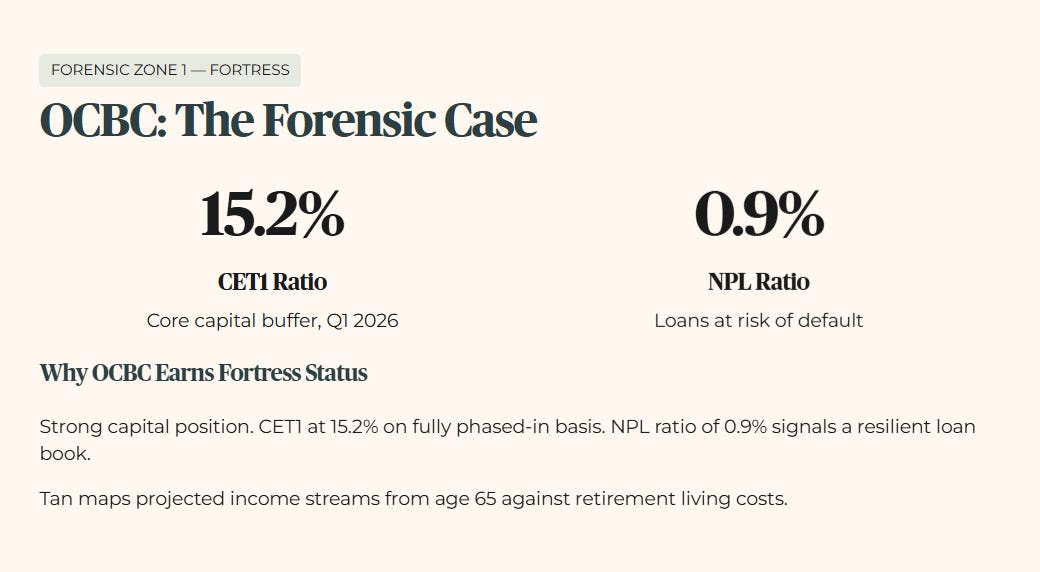

Iggy’s Forensic Zone: Zone 1 — Fortress

OCBC holds Iggy’s highest forensic rating because of its strong capital position. Its CET1 ratio (a bank’s core capital buffer, measured against its risk-weighted assets) stands at 15.2% on a fully phased-in basis as of Q1 2026, and its non-performing loan (NPL) ratio — the share of loans at risk of default — sits at 0.9%.

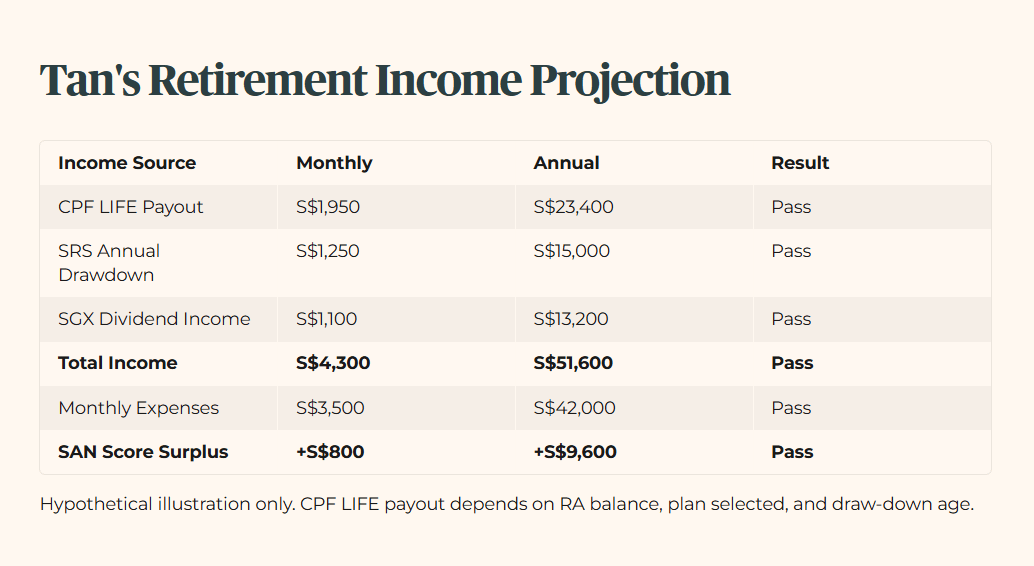

To build a resilient income floor, Tan maps his projected annual income streams from age 65 onwards against his expected retirement living costs.

Table 4 — Retirement Income Projection (Hypothetical Illustration)

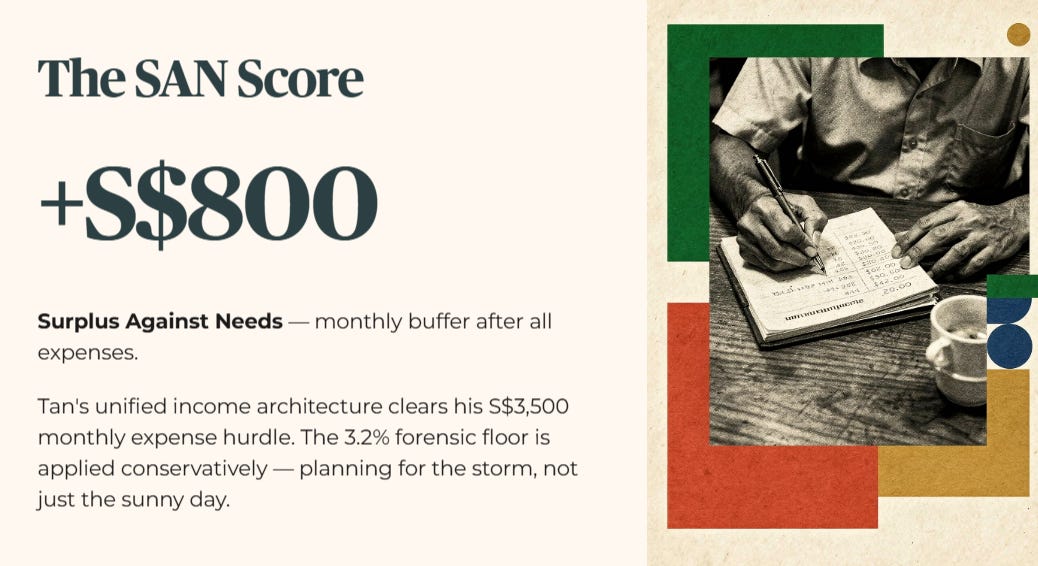

All figures in Table 4 are hypothetical illustrations. The CPF LIFE payout of S$1,950/month is an indicative example only — your actual payout depends on your Retirement Account balance, the CPF LIFE plan selected, and the age at which you start drawing. The calculations confirm that Tan’s unified income architecture clears his monthly expense hurdle of S$3,500, leaving a monthly SAN Score surplus of S$800.

Note on the Stress-Test Buffer: When projecting SGX dividend income against guaranteed CPF rates, I apply a conservative floor of 3.2%. We plan for the storm, not just the sunny day. The T-bill sits at 1.45%, but I do not lower my standards to match a temporary market dip. My floor remains at 3.2% to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle for any SGX holding in this portfolio is 4.7% — that is the 3.2% floor plus 150 basis points of mandatory risk premium.

🦎 Iggy’s Insight Block 2

The silent, second-order risk that Tan is ignoring is the re-investment risk in his 10-year SRS withdrawal window. If he hits a severe market downturn at age 65, he will be forced to sell his SRS equity assets to meet his annual distribution schedule. Selling dividend-paying shares into a depressed market locks in permanent capital losses. To protect your retirement portfolio against this trap, build an independent cash buffer outside the SRS system. That buffer will protect your core compounding engine when the market drops.

If you want zero-day access to Iggy’s full forensic watchlist, the Red Zone registry, and institutional-grade cheatsheets on every name I cover, Iggy’s Elite Investors gives you all of that for S$9/month on Substack. Free subscribers get the same analysis seven days later. The difference is timing — and in markets, timing is the whole game.

6. Strategic Considerations

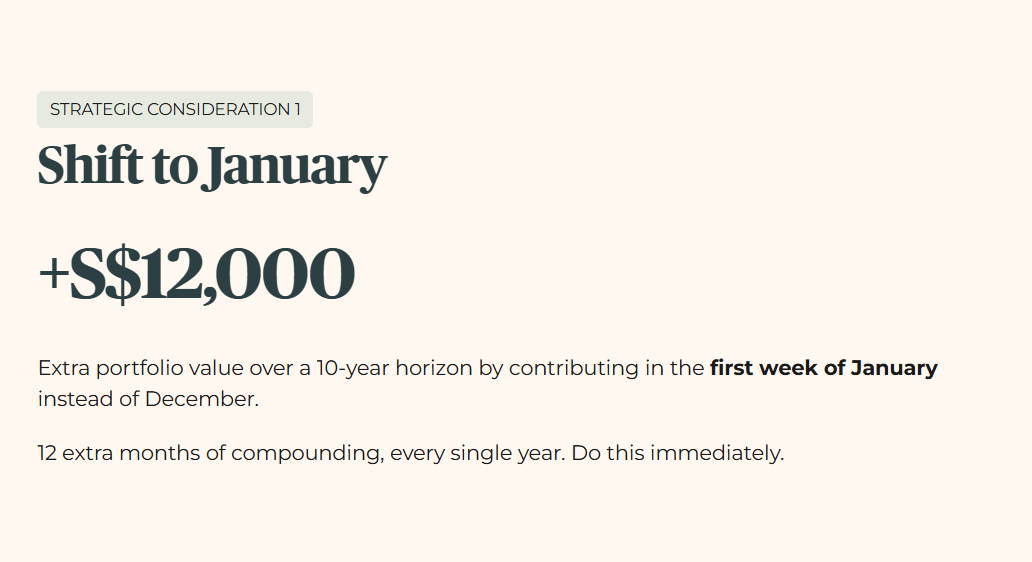

Strategic Consideration 1: Shift your annual SRS contribution timing from December to the first week of January immediately. Locking in an extra 12 months of compounding growth can add over S$12,000 to your final portfolio value over a 10-year horizon.

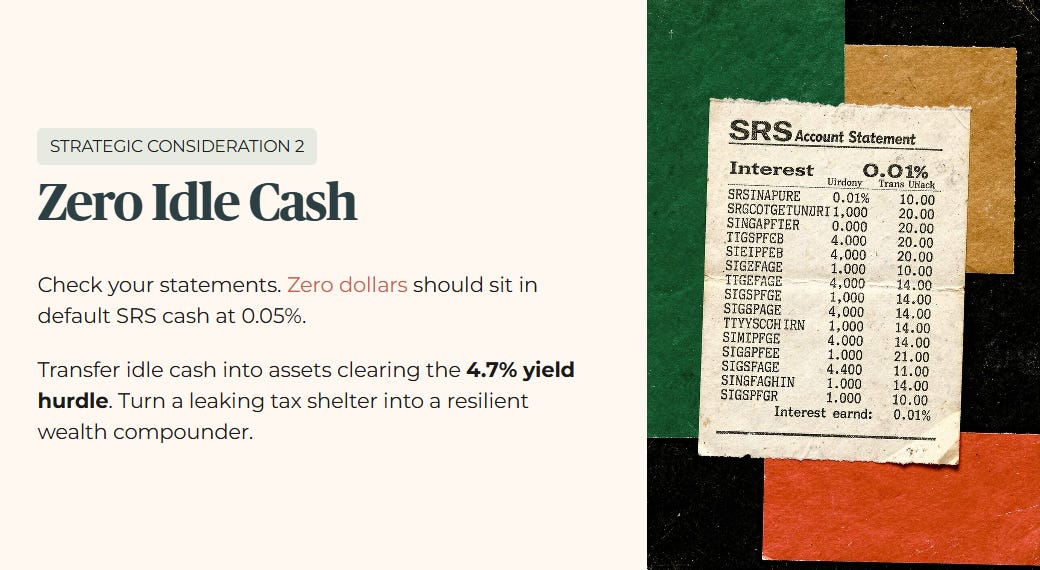

Strategic Consideration 2: Check your bank statements to make sure zero dollars are sitting in default SRS cash earning 0.05%. Transferring idle cash into assets that clear the 4.7% yield hurdle turns a leaking tax shelter into a resilient wealth compounder.

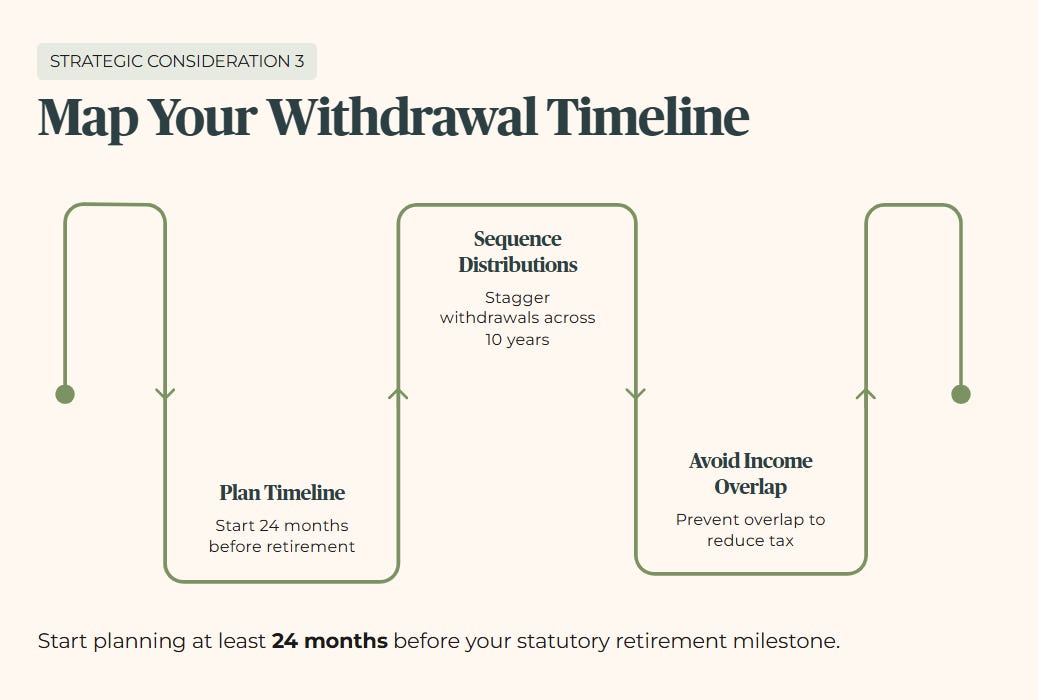

Strategic Consideration 3: Map out your exact 10-year SRS withdrawal timeline at least 24 months before hitting your statutory retirement milestone. Proper sequencing prevents your mandatory distributions from overlapping with other income streams and causing unnecessary tax exposure.

Are you genuinely managing your SRS account as a high-performance retirement pillar? Or are you letting your hard-earned tax savings quietly erode in a zero-interest banking vault?

Iggy’s Forensic Disclaimer

Longbridge Disclaimer

This article is a paid partnership with Longbridge Singapore. It is intended for general awareness and does not constitute investment advice or a recommendation to buy, sell, or otherwise engage with any investment products or financial services. The author is not a licensed financial adviser and is not offering financial advice. All views expressed are solely those of the author and do not necessarily reflect the views of Longbridge Singapore. All investments carry risks, may not be suitable for everyone, and you may lose your investment principal. Past performance is not indicative of future results. You should seek independent financial advice if you are unsure about any investment decisions. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Iggy’s Forensic Compliance Standards

This content is produced for educational and informational purposes only. I am not a financial advisor. I am a retail investor who applies forensic analysis to my own portfolio and shares that process publicly. Nothing here constitutes a recommendation to buy, sell, or hold any security. No specific target prices or personalised financial advice are offered. All data is sourced from public filings and verified sources. Where data is unverified it is explicitly flagged. All investments carry risk, including the potential loss of principal. Past performance is not indicative of future results. If you are making investment decisions involving CPF, SRS, or personal capital, please conduct your own due diligence or consult a MAS-licensed financial adviser before committing funds.