If SIA & DBS Drop Another 20% — Is Your Dividend Sanctuary Dead? | 🦖EP1517

Institutional money is already pricing in the 2026 Corridor Collapse. Here is why your 4.7% yield is now high-risk.

If The Market Drops Another 20% — Does Your SGX Portfolio Survive?

The Straits of Malacca are the arteries of your portfolio, but right now, global geopolitical cholesterol is spiking. The dividends you rely on are the ones feeling the chest pain. The market is looking at the surface data and cheering loudly. The Port of Singapore is processing record twenty-foot equivalent units. The maritime channels look as busy as ever. But volume is not the same as profitability. Motion is not the same as margin.

The real story is happening beneath the waterline. Global trade corridors from the Red Sea to the South China Sea face unprecedented disruption. The cost of moving goods is surging across every node. The cost of insuring hulls is climbing rapidly. The price of fueling vessels is quietly eroding the foundations of Temasek-linked blue chips. For a local investor managing retirement allocations, this shift changes the entire calculus of risk. You might think you own defensive assets protected by geographic moats. In reality, you hold equities exposed to a silent tax.

In This Article:

The Forensic Gap in Singapore’s Maritime Advantage

From Trade Disruption to Your Retirement Cash Flow

Jet Fuel Prices and the Hidden Tax on SGX Dividends

Macro Evidence Dashboard and Operational Friction

SGX Sector Watch Aviation Transport and Logistics Under Pressure

Macro Scenario Matrix for SGX Investors

Shock Absorption Capacity of SIA and Keppel’s Debt Wall

Action Steps for Accumulators and Retirees Under Corridor Stress

Iggy’s Forensic Compliance Standards Standard Disclaimer

About Iggy & the Elite Investors

One Community. One Forensic Lens. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. While free subscribers are reading yesterday’s story, Iggy’s Elite Investors are already cross-checking the next setup — together, in real time.

Iggy’s Elite Investors don’t just get the report earlier. They get the full forensic picture the moment it’s finalised — zero-day breakdowns, the complete “Red Zone” watchlist, and institutional-grade cheatsheets built around the same Five-Layer Audit you see here. The difference is they get it before the market opens, not after it has already moved.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

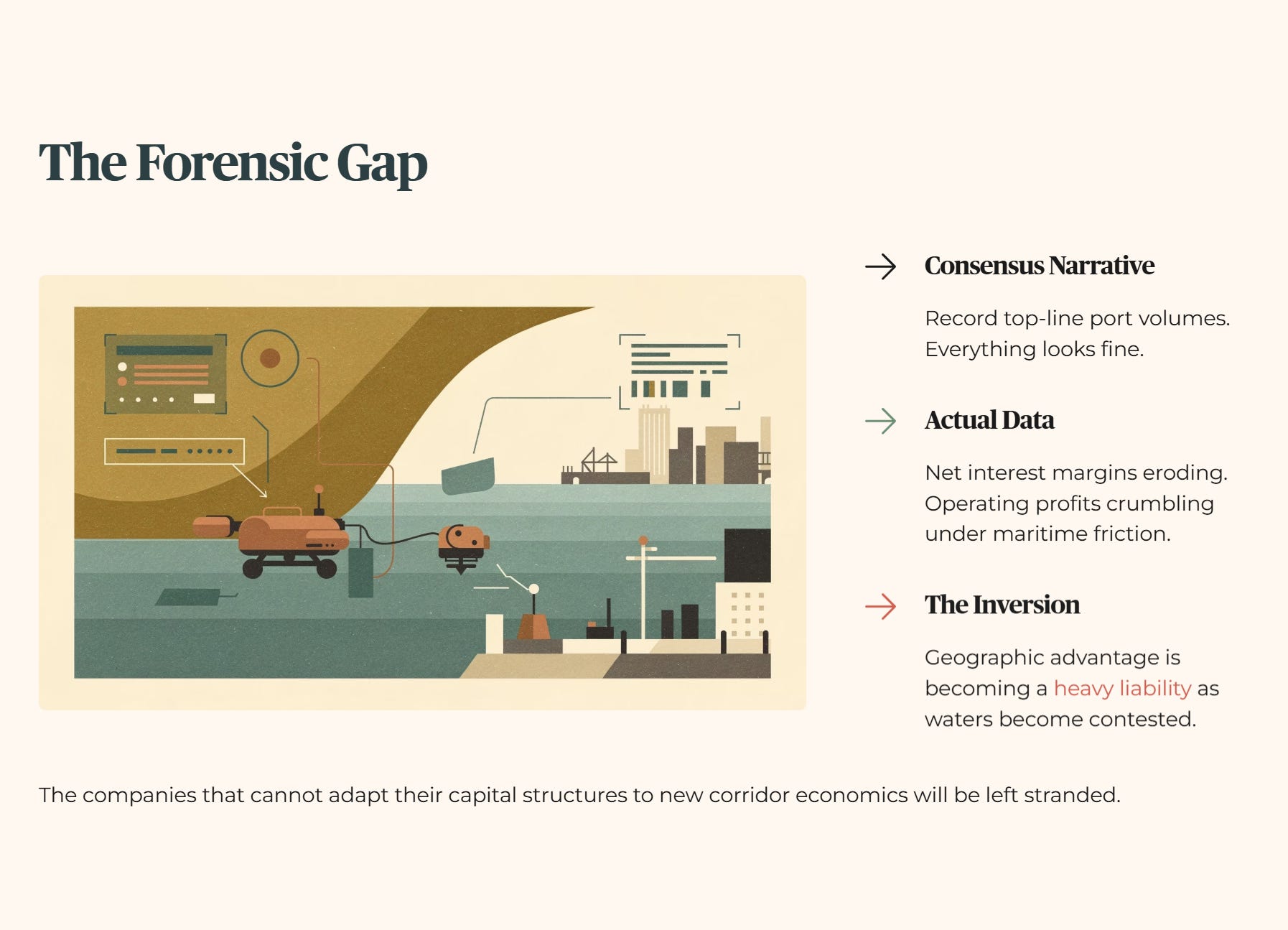

The Forensic Gap

This discrepancy is exactly what we call The Forensic Gap. The consensus narrative is entirely fixated on top-line record volumes at the port. The data actually shows a second-order erosion of net interest margins. It shows operating profits crumbling under the weight of maritime friction. The historical advantage of being a maritime hub is slowly inverting. When trade flows freely, geographic positioning is a massive premium. When the waters become contested, that same geography becomes a heavy liability.

We are witnessing the rewiring of global logistics in real time. The companies that cannot adapt their capital structures to this new corridor economics will be left stranded.

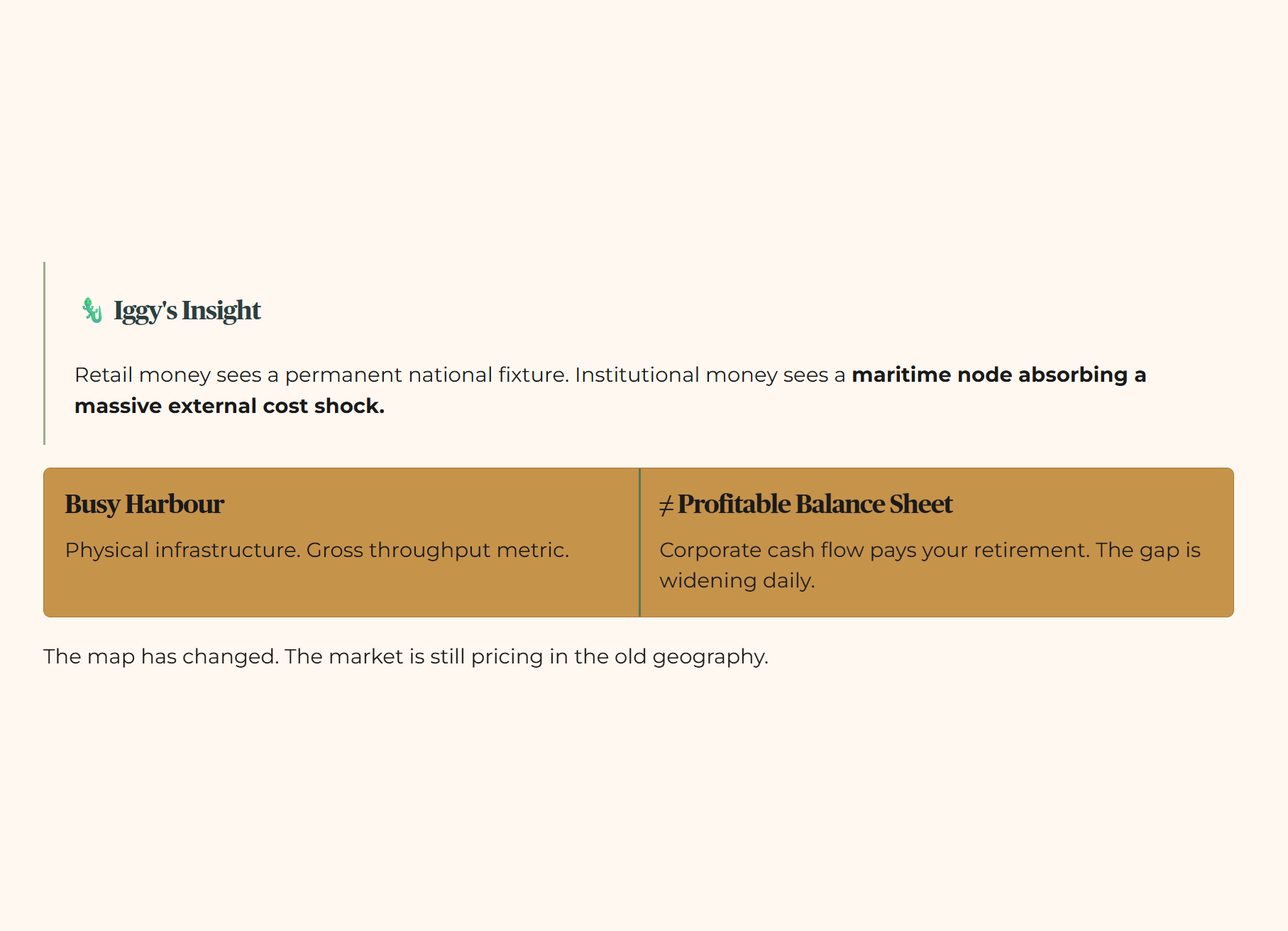

🦎 Iggy’s Insight

The psychological blind spot here is institutional inertia. Retail money looks at a major local transport or logistics blue chip and sees a permanent fixture of the national landscape. Institutional money looks at the exact same asset and sees a maritime node currently absorbing a massive external cost shock.

When shipping lanes require rerouting, the immediate reaction is to praise the resilience of our port infrastructure. But physical infrastructure does not pay your retirement distribution. Corporate cash flow pays it. The gap between a busy harbour and a profitable balance sheet is widening every single day. The map has changed, and the market is pricing in the old geography.

The disruption of global capital corridors eventually finds its way to the local consumer. Think of it as arterial plaque in the supply chain — invisible on the surface, but steadily narrowing the flow of cash that reaches your distribution statement. When freight insurance premiums multiply, cargo ships add thousands of nautical miles to avoid contested waters. The final imported price of basic goods adjusts upward immediately. A household in Bedok might notice their monthly grocery bill inching up. A standard logistics delivery fee for a basic household appliance quietly climbs. These are not isolated pricing errors. They are the downstream result of energy-driven operating cost inflation bleeding directly into the local retail supply chain.

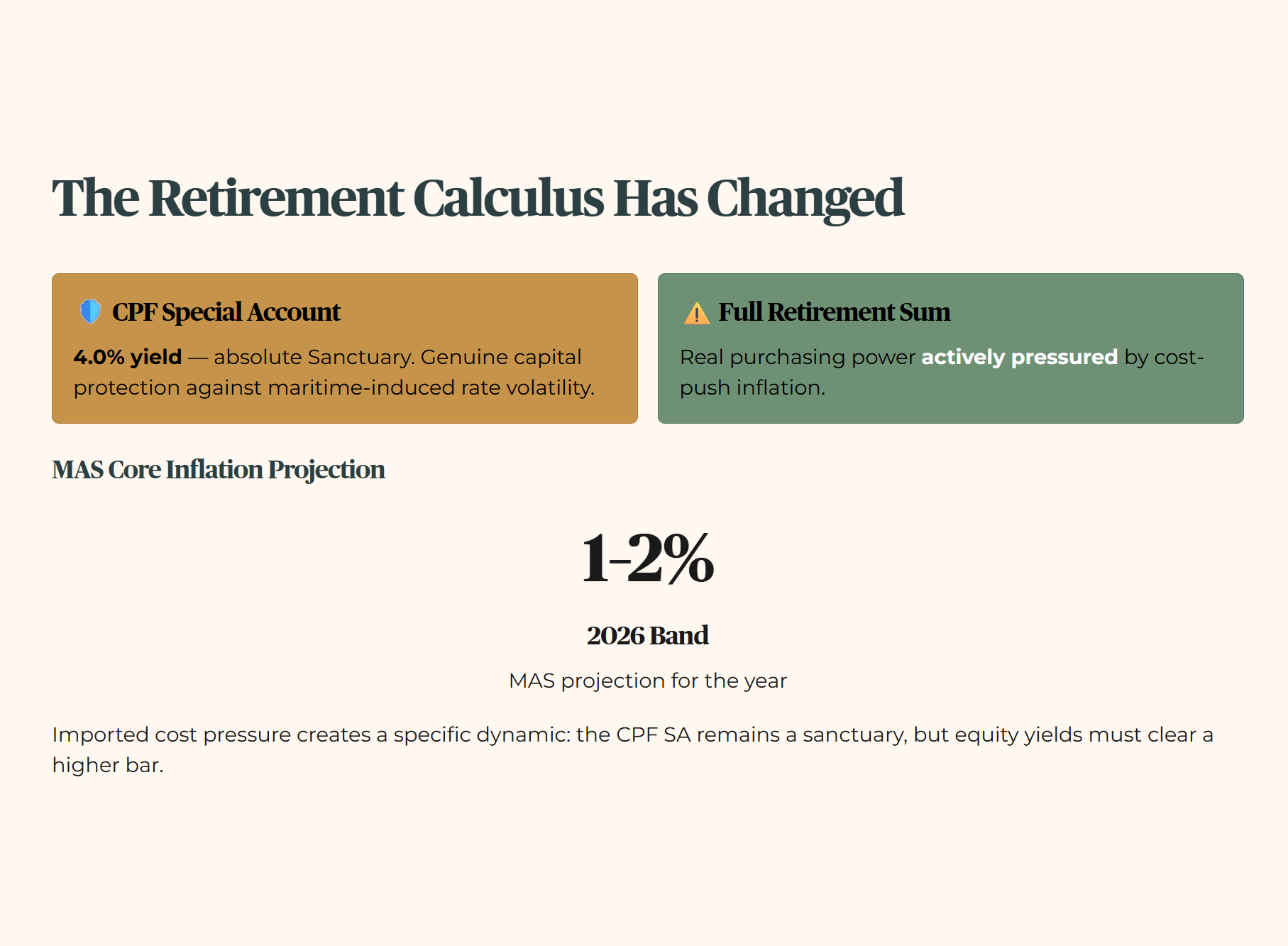

This imported cost pressure fundamentally alters the retirement calculus. The Monetary Authority of Singapore projects core inflation settling between one and two percent for the year. This creates a specific dynamic for your retirement funds. The Central Provident Fund Special Account, yielding four percent, remains an absolute Sanctuary. It provides genuine capital protection against this maritime-induced rate volatility. However, the real purchasing power of your Full Retirement Sum is actively being pressured by this cost-push inflation.

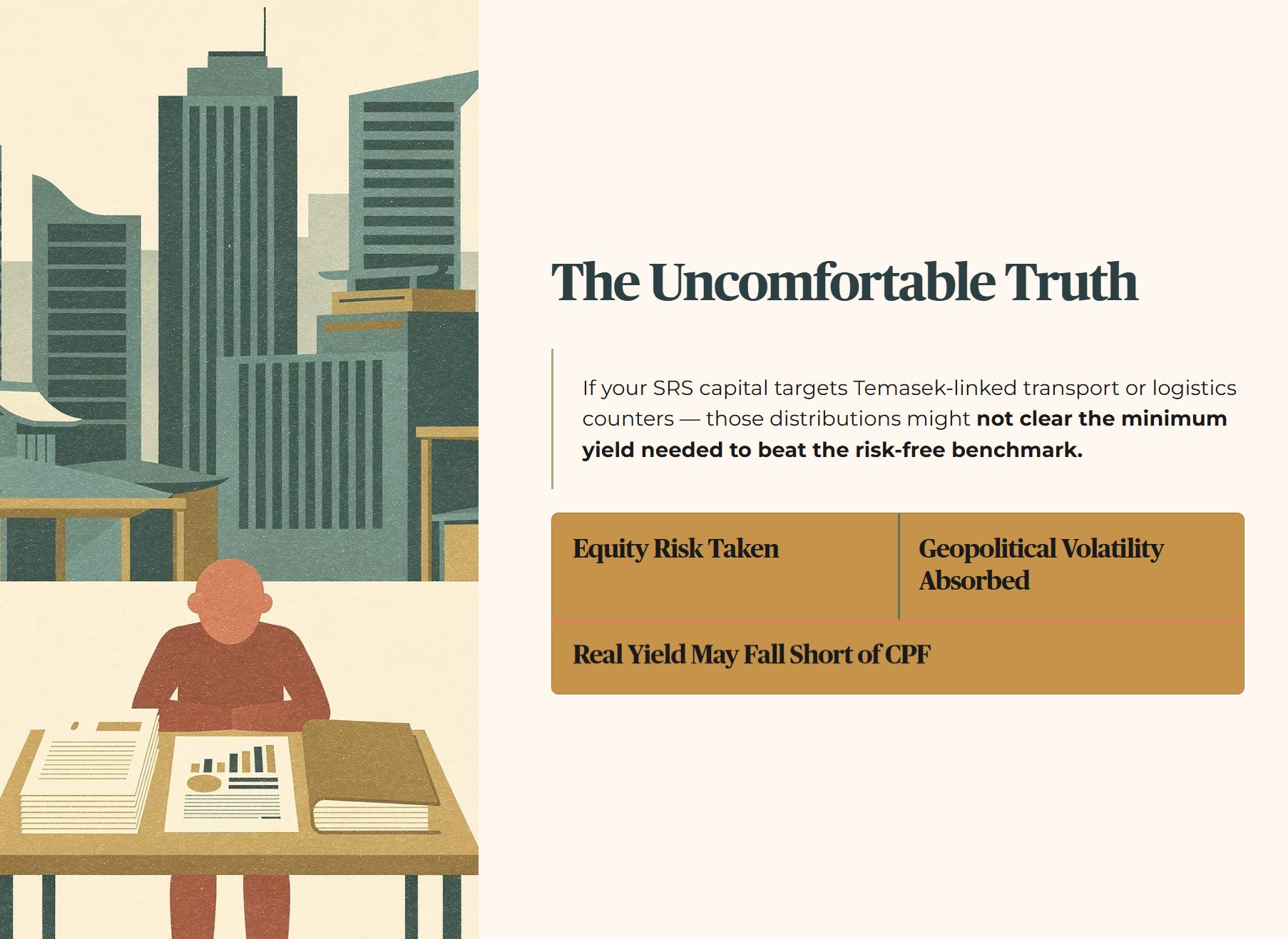

If you deploy your Supplementary Retirement Scheme capital into equity markets targeting passive income, the stakes are suddenly much higher. Here is the uncomfortable truth: if your portfolio is anchored in traditional Temasek-linked transport or logistics counters, those distributions might not clear the absolute minimum yield needed to beat the risk-free benchmark. You are taking on equity risk. You are absorbing geopolitical volatility. You are potentially receiving a real yield that falls short of simply leaving the money in the CPF system.

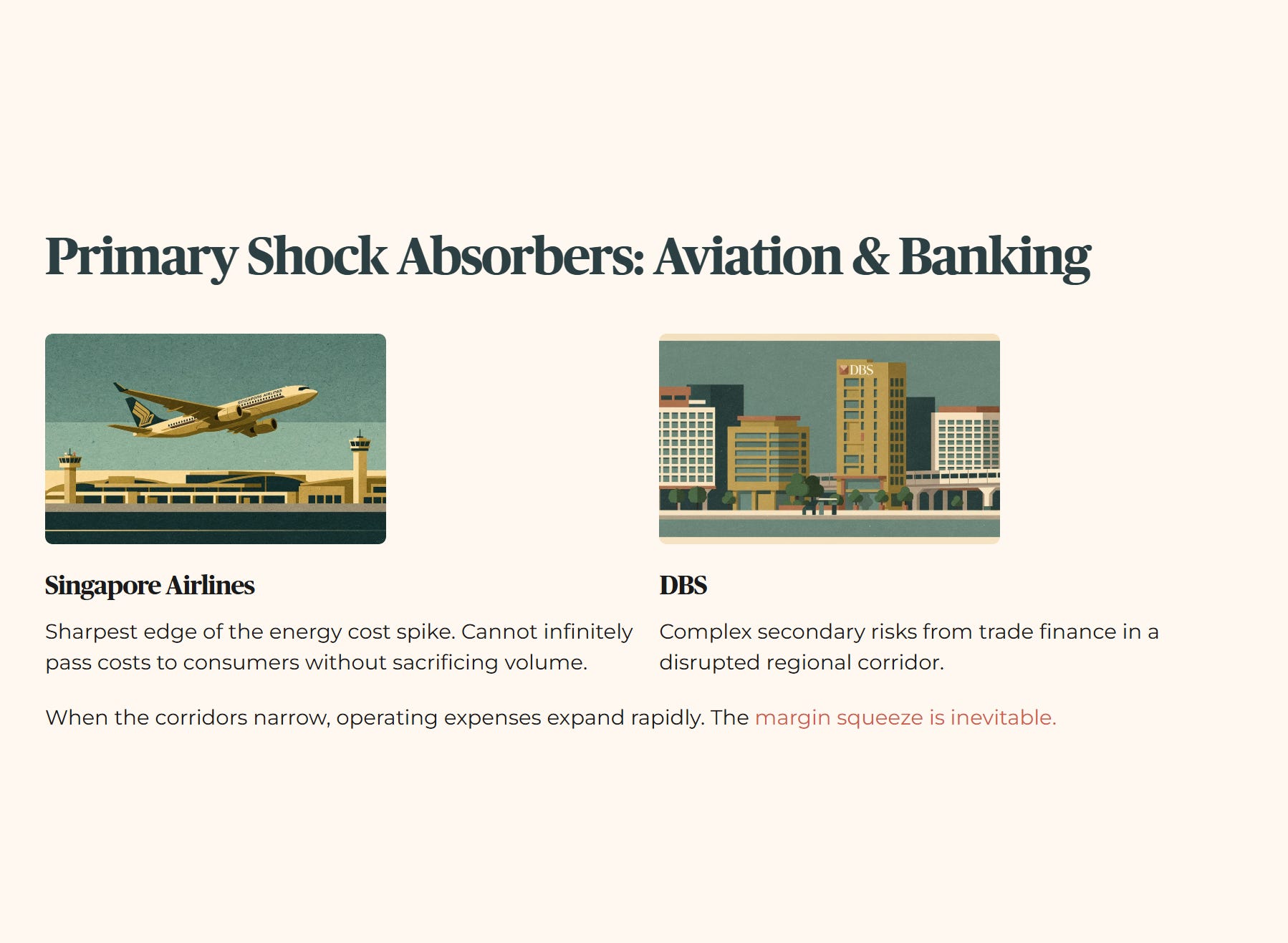

The specific sectors on the Singapore Exchange bearing the brunt of this transition are aviation transport and institutional banking. Singapore Airlines operates at the sharpest edge of the energy cost spike. DBS manages the complex, secondary risks associated with trade finance in a disrupted regional corridor. Both sectors sit at the intersection of global trade flow and local shareholder returns. They are the primary shock absorbers for the region. When the corridors narrow, their operating expenses expand rapidly. The heartland investor must understand that these companies cannot infinitely pass these costs down to the consumer without eventually sacrificing volume. The margin squeeze is inevitable.

This is where the maritime disruption transitions from a distant headline into a quantifiable margin squeeze on your distribution statements.

The Primary Shock Absorbers

The ninety-eight dollar per barrel jet fuel price is the undeniable linchpin of this entire geopolitical cycle, based on InvestingPro data. It is the single number that cuts through the noise of record port volumes and optimistic institutional forecasts. Every nautical mile added to avoid a maritime chokepoint burns fuel at this elevated premium. Every flight path altered to bypass a contested airspace destroys operating leverage. For a fifty-five-year-old investor in Marine Parade relying on aviation or logistics dividends, this fuel cost is a direct deduction from their future payouts.

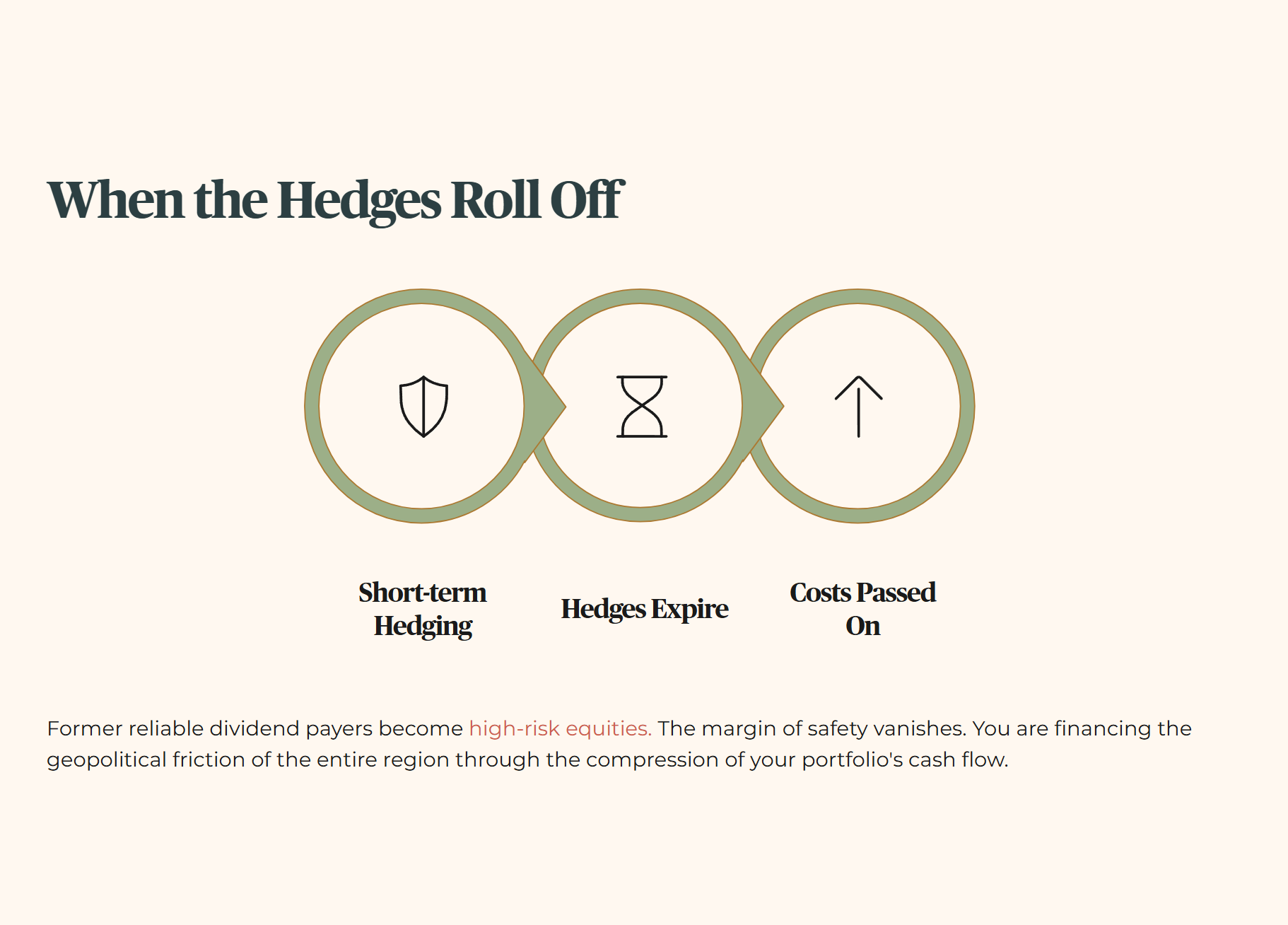

You cannot sustain historical distribution yields when the baseline cost of traversing the globe remains pinned near the hundred-dollar mark. The airlines and transport conglomerates can hedge their fuel exposure in the short term. However, those hedges eventually roll off. When they do, the new reality of corridor economics takes over. The companies are forced to absorb the higher baseline or pass it onto passengers who are already suffering from cost-push inflation. This dynamic turns former reliable dividend payers into high-risk equities. The margin of safety vanishes when the geographic moats dry up. The math is brutal and unforgiving. You are effectively financing the geopolitical friction of the entire region through the compression of your portfolio’s cash flow.

Table 1: Macro Evidence Dashboard

The forensic stance across the SGX universe reveals a clear divergence between asset-light resilience and heavy-infrastructure vulnerability.

🦎 Iggy’s Insight

When a trade route narrows, the first thing that clots is cash flow — not volume. The Port of Singapore can process record container throughput and still leave your distribution statement haemorrhaging.

The reason is simple: throughput is a gross metric. What funds your retirement is net margin after fuel, insurance, and rerouting costs are paid. These input costs behave like arterial plaque — accumulating silently, showing no symptoms until the blockage is severe. By the time the dividend cut is announced, the damage to your SRS income plan is already done. The forensic audit does not wait for the press release. It reads the balance sheet before the chest pain arrives.

Keppel’s interest coverage at 2.0x sets up the debt wall calculation that determines if this pivot survives the corridor shock.