iFAST Corp: Record Profit, S$987.75M Net Cash, So Why Does the Dividend Stay Small?

Inside the Balance Sheet Strength That's Quietly Capping Your Payout

S$9.11 iFAST Corp: The S$987.75M Net Cash Paradox Breaking Institutional Buy Ratings

One hundred and eight million dollars in net profit stands as a historic high for a local platform giant, yet it hides a structural cash reality that most retail investors completely overlook. When institutional analysts chase a S$12.20 price target, they are pricing a high growth tech engine rather than a reliable wealth sanctuary. For a fifty-five-year-old Singaporean counting on sustainable distributions, this mismatch reveals why a multi-billion-dollar ecosystem can simultaneously be a brilliant business and a hazardous income trap.

Reviewing the Financial Statements

Tracking the local capital markets means separating the operational noise of corporate expansions from the cold reality of what drops into your central depository account. We want businesses that dominate their fields, but we want them to respect the immediate cash flow requirements of a retirement portfolio. Let us dissect the numbers filed in the latest financial statements to see what a new dollar is actually buying at today’s market price.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips, the interest coverage, the gearing, the free cash flow sustainability, so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

Section 1 — The Analyst’s Case

Section 2 — Iggy’s Forensic Screen

Section 3 — The Dividend Trajectory

Section 4 — The Forensic Gap

Section 5 — What To Watch Next

Section 1 — The Analyst’s Case

Before we get into RHB’s thesis, here is the framing that matters most. This article applies my 4.7% minimum yield hurdle, the income threshold I require before any stock qualifies for a retirement portfolio, against an institutional case built on a completely different objective: capital appreciation, not cash income.

The institutional thesis from RHB remains clear and aggressive, reiterating a BUY rating on iFAST Corporation Ltd. (SGX: AIY) with an unchanged price target of S$12.20. This target implies a significant 36% capital upside from the current market price of S$9.110.

RHB’s forward valuation relies heavily on recent infrastructure enhancements within iFAST Global Bank, specifically the rollouts of the Alipay+ “Worldwide Scan & Pay” cross-border QR payment rail for retail clients and Single Euro Payments Area (SEPA) rail support for corporate multi-currency accounts. The analyst frames these payment rails not as standalone core profit centers, but as strategic ecosystem enhancers designed to drive user stickiness, accelerate corporate deposit accumulation, and lower execution costs compared to the legacy SWIFT transfer network.

The report openly acknowledges that the near-term earnings impact from these launches will be highly restricted. Instead, the investment case is anchored on the long-term compounding of the group’s asset-light wealth management platform, regional pension administration contracts in Hong Kong, and scaling digital banking assets in the United Kingdom. Key risks identified by the house include earnings volatility tied to fluctuations in Assets Under Administration (AUA), regional regulatory adjustments, and foreign exchange translation exposure.

THE LOAD-BEARING ASSUMPTION: RHB assumes that iFAST can successfully scale its digital banking assets and multi-currency payment infrastructure into high-margin recurring fee streams before rising corporate infrastructure costs compromise platform profitability.

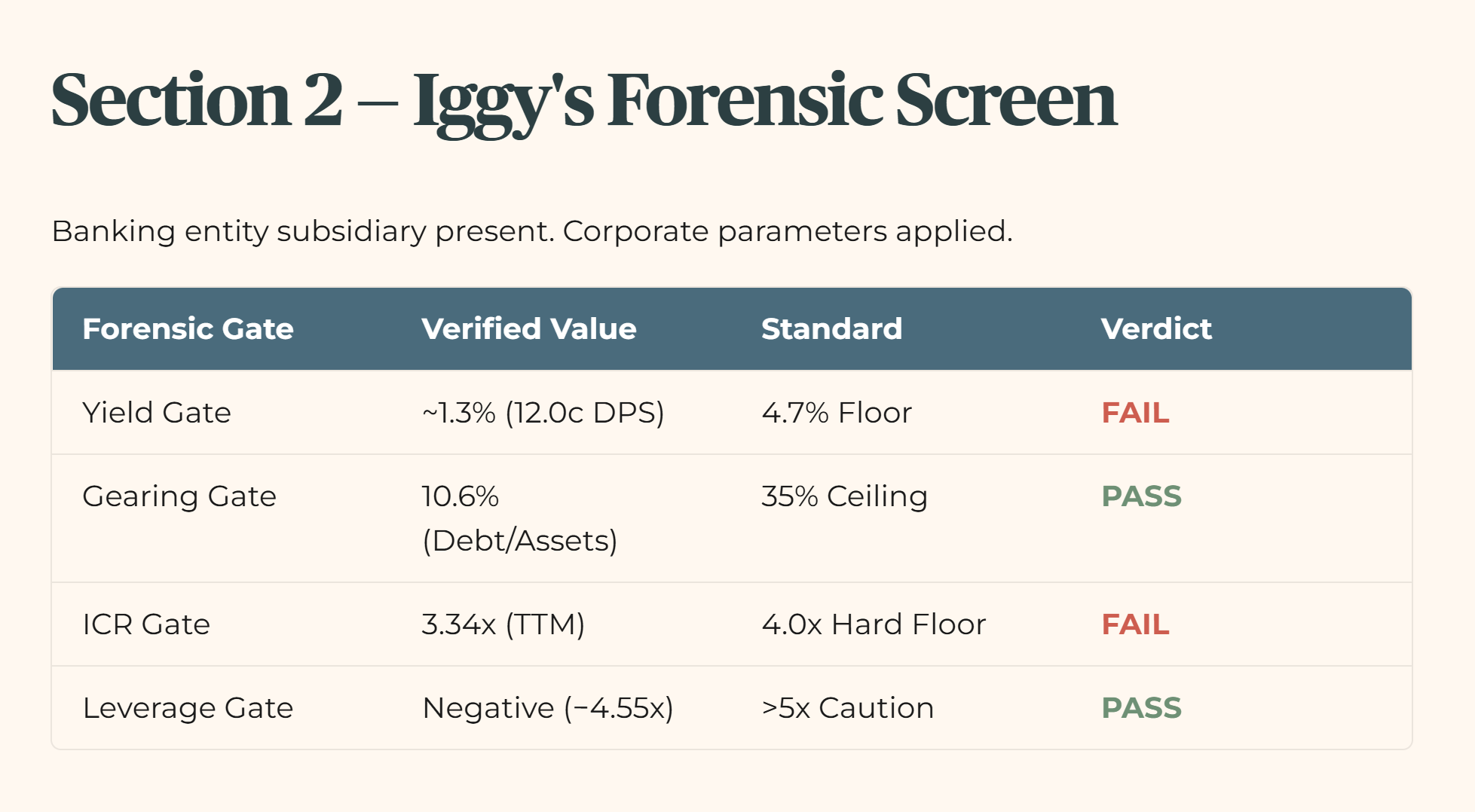

Section 2 — Iggy’s Forensic Screen

When we step away from institutional growth models and apply Iggy’s Forensic Compliance Standards, the operational picture changes completely. We evaluate assets based on immediate cash reliability and absolute debt safety.

Financial Health Checklist

Banking entity subsidiary present. Corporate parameters applied with contextual reference to client-related liabilities.

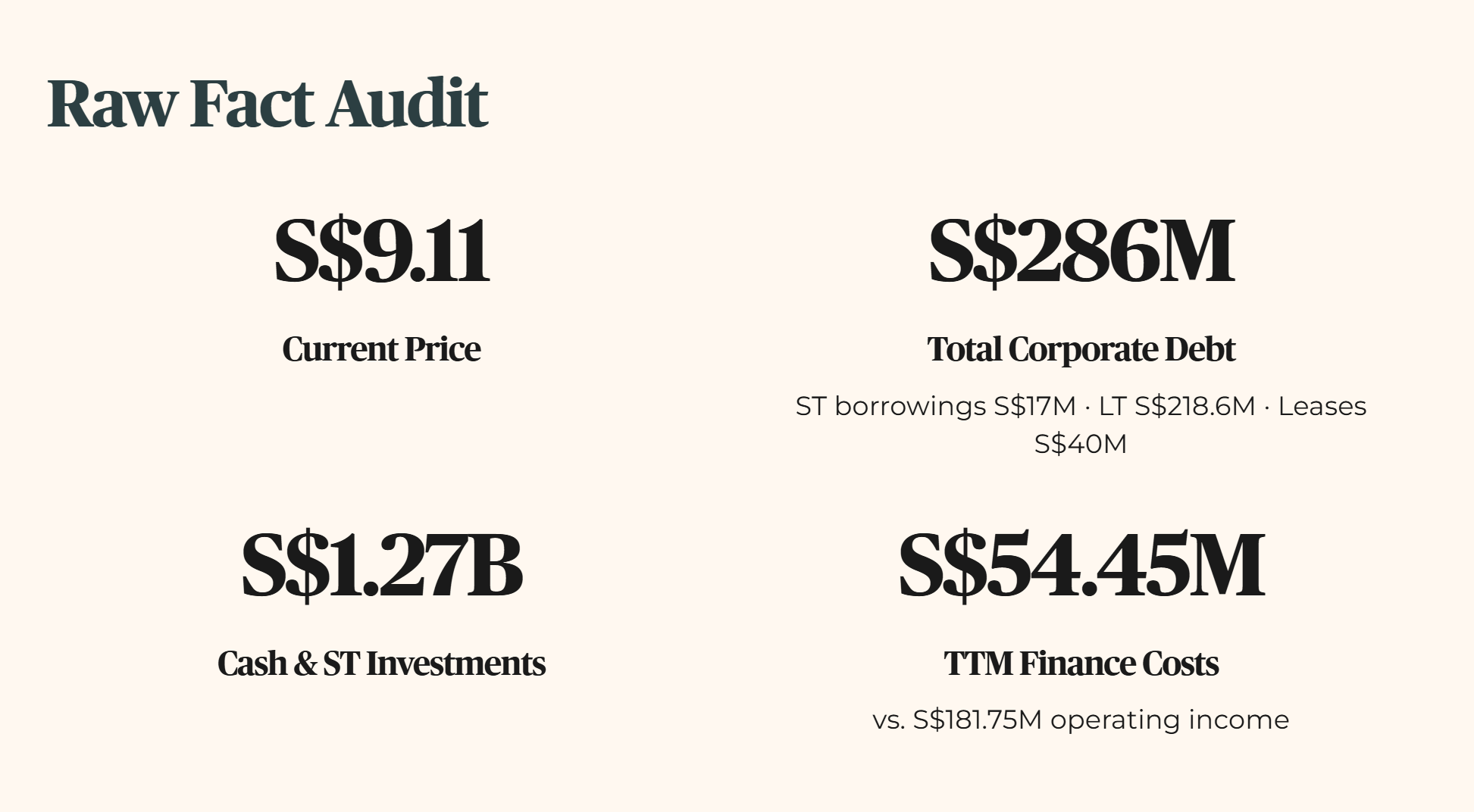

Raw Fact Audit: The current price sits at S$9.110. Total corporate debt is verified at S$286.0M, comprising short-term borrowings of S$17.0M, a current long-term portion of S$10.4M, long-term debt of S$218.6M, and capital leases of S$40.0M. Total cash and short-term investments stand at S$1,273.77M. Operating income for the trailing twelve months (TTM) is S$181.75M, confirmed across four quarters from Q2 2025 to Q1 2026, against finance costs of S$54.45M over the same period.

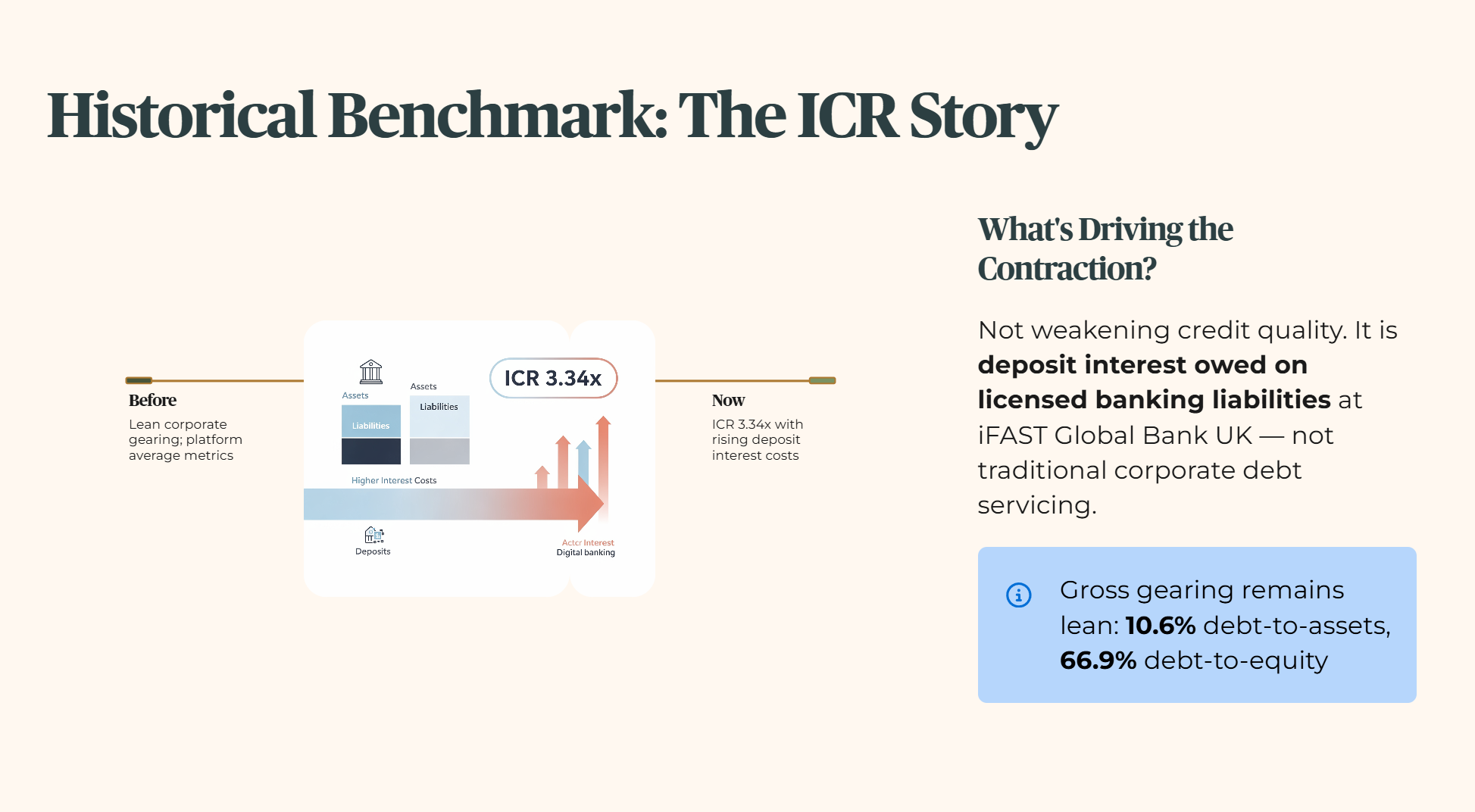

Historical Benchmark: Gross gearing is exceptionally lean at 10.6% on a debt-to-assets basis, or 66.9% on debt-to-equity. However, the trailing twelve-month ICR of 3.34x marks a noticeable contraction from historical platform averages. This is not a sign of weakening credit quality. It is driven by rising structural interest expenses as the banking wing scales, specifically deposit interest owed on licensed banking liabilities at iFAST Global Bank in the United Kingdom, not corporate debt servicing in the traditional sense.

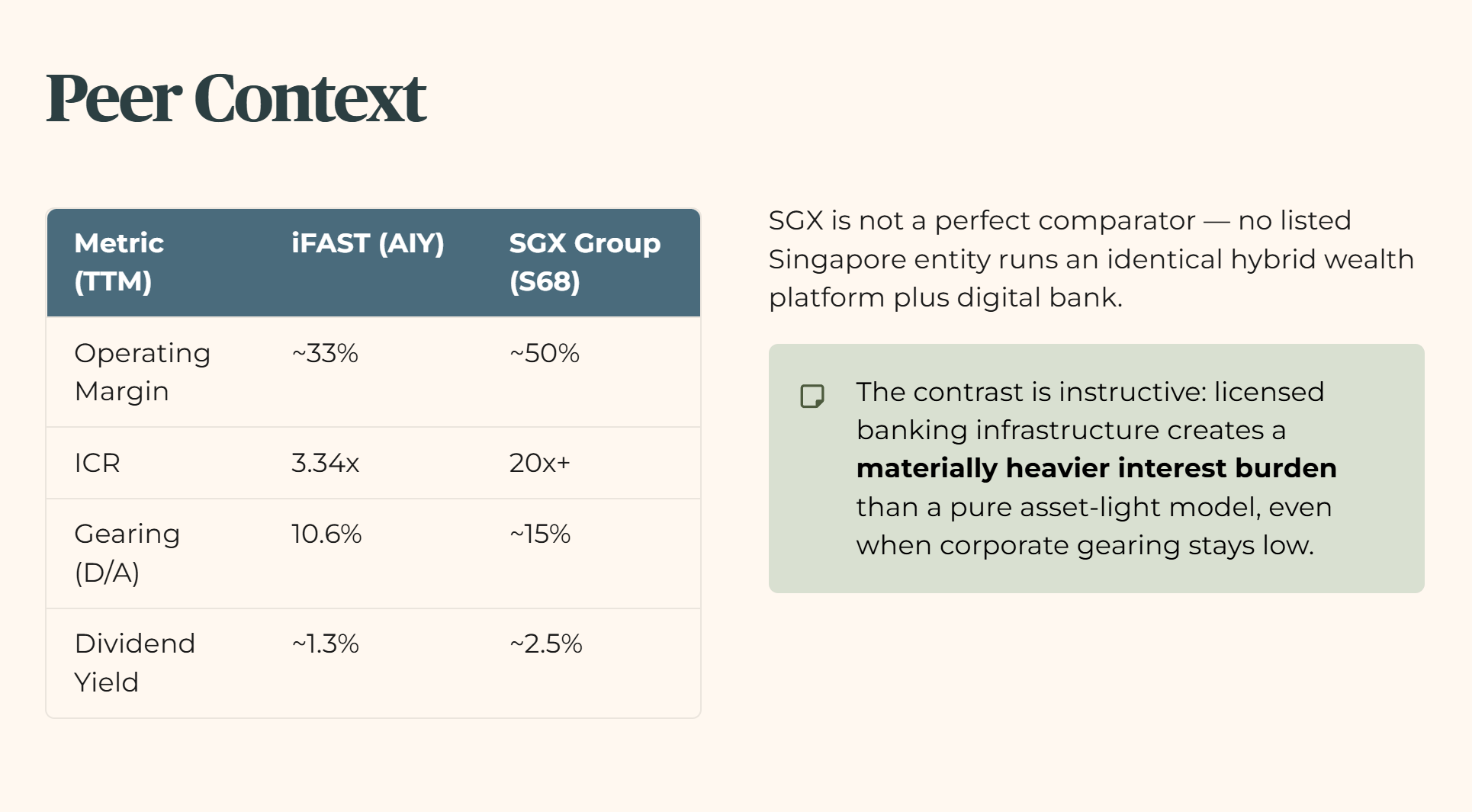

Peer Context

SGX Group is not a perfect comparator. No other listed Singapore entity runs an identical hybrid of asset-light wealth platform plus digital bank. But the contrast is instructive: it shows how taking on licensed banking infrastructure creates a materially heavier interest burden than a pure exchange or asset-light model carries, even when corporate gearing itself stays low.

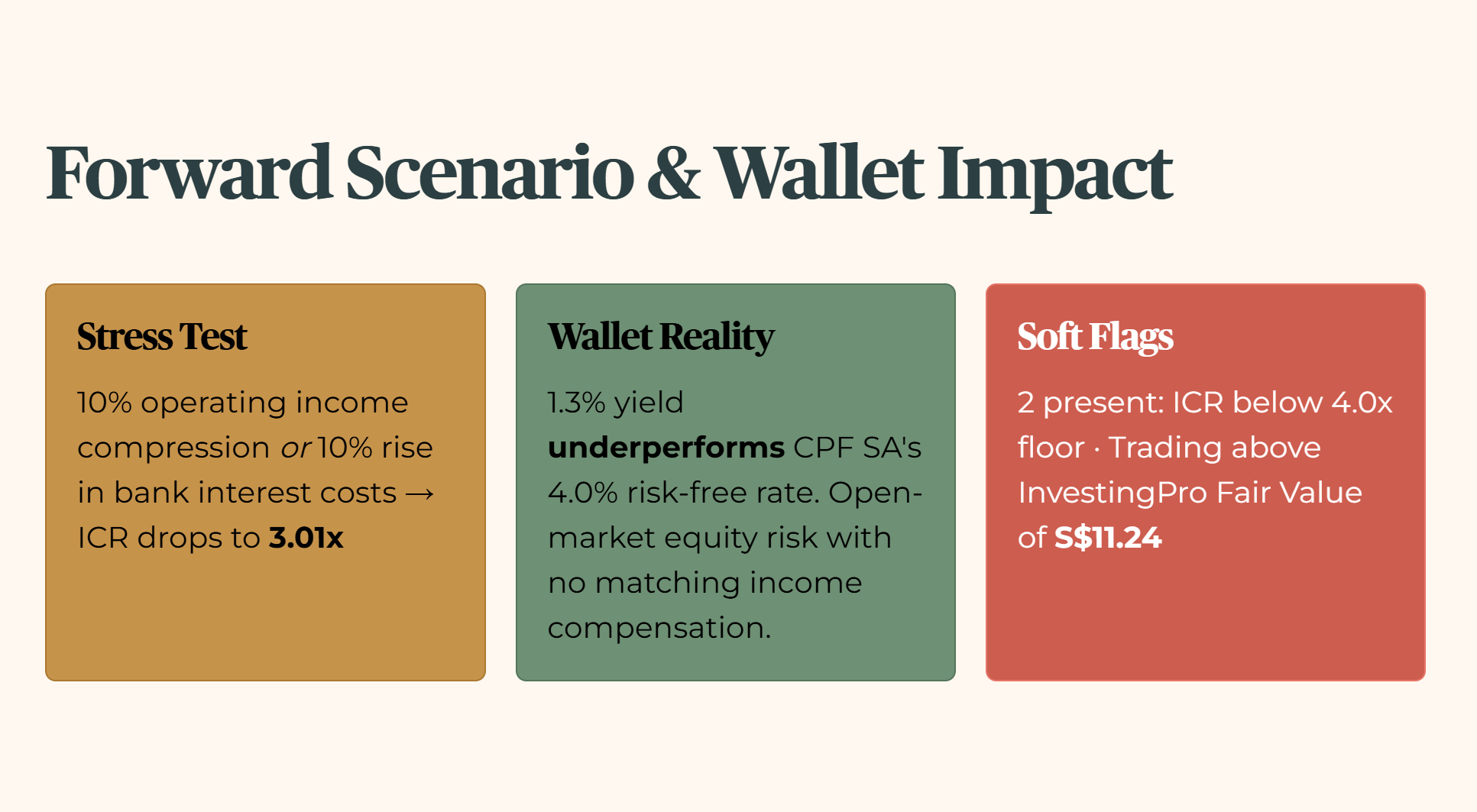

Forward Scenario: A 10% macro compression in platform operating income, or a 10% escalation in bank infrastructure interest costs, would compress the current ICR down to 3.01x, driving the metric deeper below our safety parameters.

Wallet Impact: For a retiree, the low 1.3% yield means your capital is heavily underperforming the 4.0% risk-free sanctuary of the CPF Special Account. You are taking open-market equity volatility for a return that does not clear inflation.

Soft Flag Count: 2 Present (ICR below the 4.0x hard floor; trading above the asset-backed InvestingPro Fair Value of S$11.24 relative to core equity capital reserves).

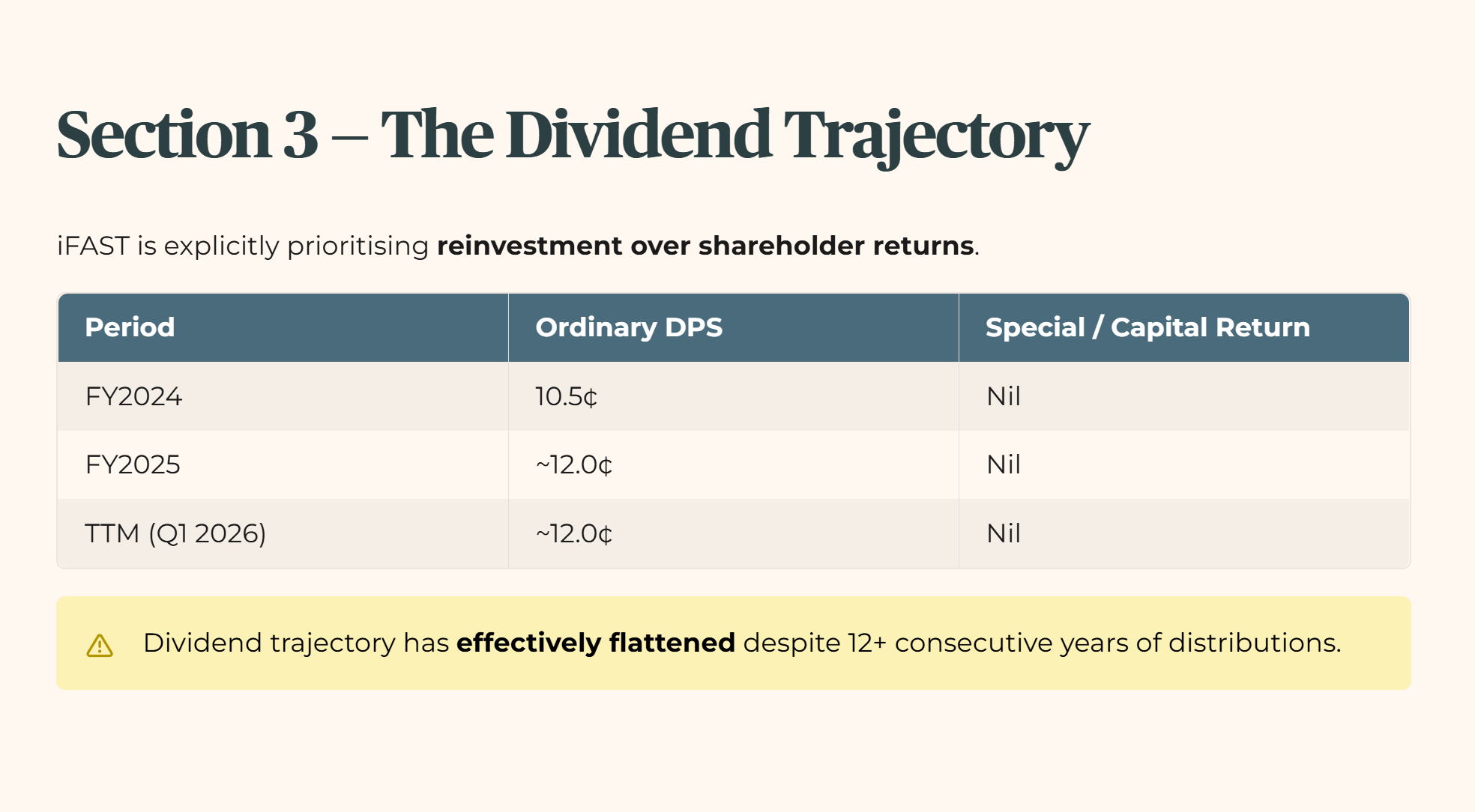

Section 3 — The Dividend Trajectory

A meticulous review of the distribution ledger reveals that iFAST is explicitly prioritizing corporate reinvestment over immediate retail shareholder returns.

Dividend Trajectory Ledger

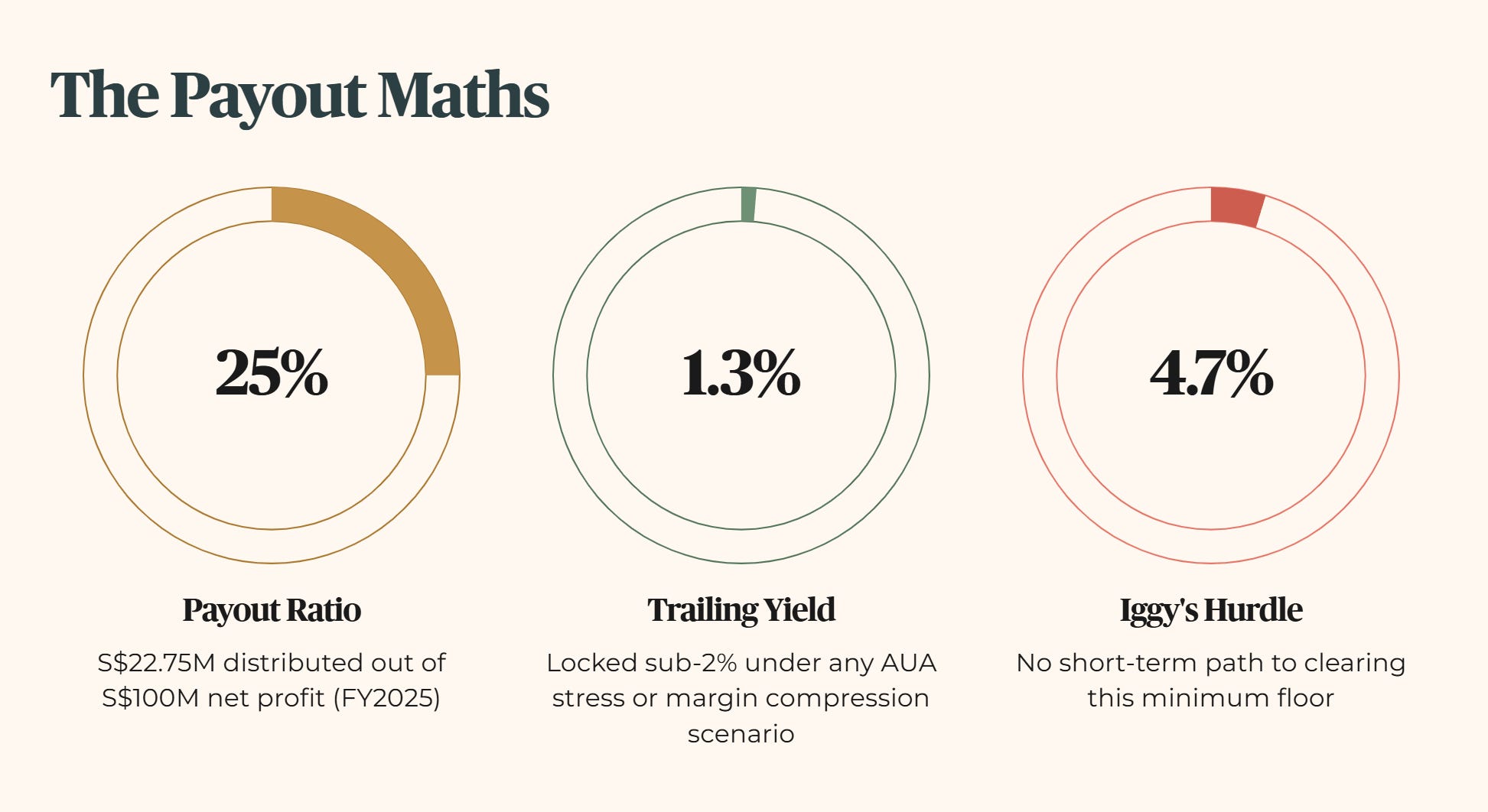

While iFAST deserves credit for maintaining consecutive dividend distributions for over 12 years, the dividend trajectory has effectively flattened. Total cash distributed in FY2025 was approximately S$22.75M out of a net profit of S$100.0M, translating to a conservative payout ratio of less than 25%. Under a forward stress scenario where global AUA contracts due to regional market volatility or margin compression inside iFAST Global Bank, the board’s strict prioritization of capital preservation will lock the ordinary yield into its current sub-2% range, completely eliminating any short-term path to clearing our 4.7% minimum hurdle.

The real forensic step happens next: tying this sub‑2% payout and sub‑4x interest coverage to the S$987.75M net cash pile that iFAST cannot freely release because it is structurally locked against licensed banking liabilities, which is the constraint that ultimately caps your dividend.