Indonesia's $908 Billion Gamble — What Prabowo's Resource Nationalism Means for Your SGX Portfolio

Singapore kopi, electricity, ports hostage to Jakarta: Your SGX dividends trapped in Indonesian state banks

I was reading through regional business news last Wednesday when a headline stopped me. Indonesia had just handed control of every palm oil, coal, and ferroalloy export to a single state company. My first reaction was not about commodity prices. It was about cash flow. Specifically, the cash flow of every Singapore investor holding stocks that depend on those trade routes clearing cleanly.

Every major port city has faced the same question at some point: what happens when the trade route moves? Malacca faced it in the 1500s. Rotterdam faced it when container ships changed global logistics. Singapore is facing it now — not because the ships have stopped moving, but because the legal architecture governing what those ships carry has just been rewritten overnight.

On 20 May 2026, Indonesian President Prabowo Subianto made a significant policy shift. He moved control of all palm oil, thermal coal, and ferroalloy exports to a single state company called PT Danantara Sumberdaya Indonesia. Private exporters can no longer sell directly to buyers outside Indonesia. The state now stands in the middle of every contract, every shipment, and every dollar of revenue.

If you are managing your CPF Special Account or SRS portfolio, this is not just regional news. It is an immediate event for your money. The commodities passing through this state bottleneck flow directly through Singapore’s port infrastructure, our refining capacity, and our bank financing pipelines.

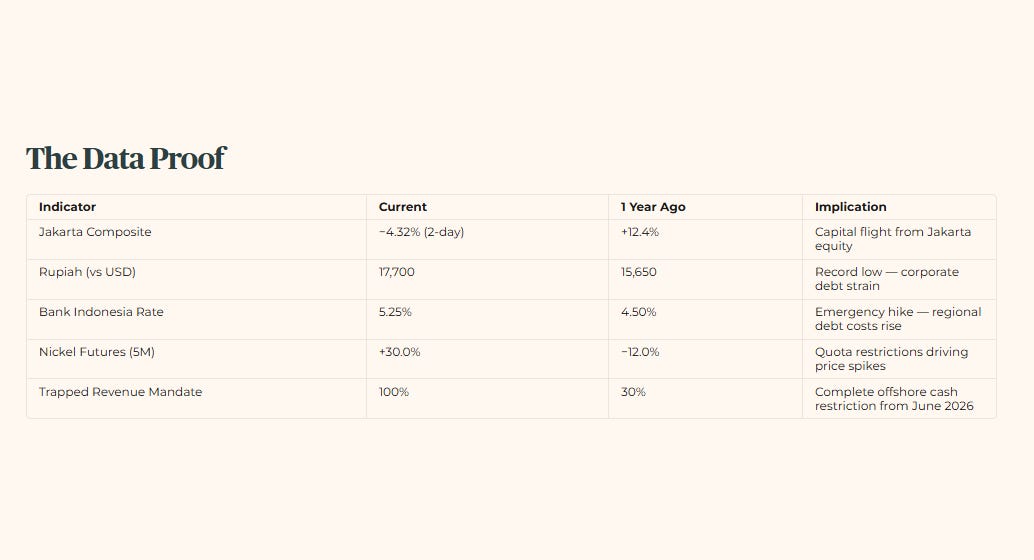

Jakarta says this fixes a long-standing problem. President Prabowo has claimed Indonesia lost as much as US$908 billion in revenues over the past 34 years from under-priced commodity exports — a figure he cited to parliament to justify centralising exports under the new Danantara-linked state agency. The market reacted fast. The Jakarta Composite Index dropped 3.5% on rumours the day before the announcement. It fell another 0.82% on the day itself. The Indonesian rupiah hit a record low of 17,700 per US dollar. Bank Indonesia then raised its benchmark rate by 50 basis points to 5.25% — a larger move than the market anticipated.

Most institutional analysts are calling this local resource nationalism. But the data tells a different story. They assume the friction stops at the Indonesian border. Indonesia remains one of Singapore’s most significant trade partners for refined fuel — historically accounting for more than half of its total oil product imports sourced from Singapore, though Jakarta now signals a pivot towards US and Middle Eastern suppliers. When you slow down trade at the source, you change the cash flow of every Singapore-listed company that takes a margin from those physical volumes.

Most financial content is built around excitement — what is surging, what is breaking out, what you might be missing. I am deliberately building something different. Retirement-grade investing is not exciting. It is disciplined, forensic, and it is designed to still be working when you need it most.

In This Article:

The Local Impact (The Wallet)

The Data Proof (The Evidence)

The Strategic Landscape (Scenario Matrix and SGX Sector Watch)

The Singapore Investor Playbook (Shock Absorption and Retirement Impact)

Conclusion

The Local Impact (The Wallet)

This friction will show up at your kitchen table before it appears in any annual report. For a household in Bedok or Toa Payoh, the first sign will not be the price of raw coal. It will show up in everyday expenses.

When global commodity routing gets a structural shock, the cost of processing, shipping, and refining moves. Think about what goes into your electricity tariff or the logistics costs baked into every consumer product arriving at our docks. If regional supply paths become congested because private exporters are locked in a three-month transitional reporting phase starting 1 June 2026, those operational costs will be passed down to you.

We sell US$39.83 billion in total exports to Indonesia, including a significant portion in mineral fuels as a refining and re-export hub. Any disruption in the upstream flow entering our refineries hurts our domestic processing efficiency. That creates an inflationary undercurrent that makes your daily cost of living stay higher for longer.

This sticky inflation changes the math for your CPF and SRS capital. Bank Indonesia just pushed its benchmark rate to 5.25% to defend a falling rupiah. That shifts the regional risk-free floor upward and keeps borrowing costs high across the region. In Singapore, your CPF Special Account gives you a safe 4.0% return. That means the hurdle rate for taking equity risk has never been higher. If you are risking retirement capital in Singapore-listed stocks that depend on Indonesian resource concessions, those stocks must deliver a yield that comfortably clears my minimum hurdle of 4.7% — the income threshold I require before any stock qualifies for a retirement portfolio.

Starting 1 June 2026, Indonesian exporters must bring 100% of their foreign revenue back into Indonesian state-owned banks. Cash that previously flowed into Singapore’s commercial banks to clear trade invoices will now be legally locked inside Jakarta’s capital controls. If you are relying on predictable quarterly distributions to fund your SRS drawdown strategy, this places an immediate question mark over whether those dividends will be paid.

The companies exposed on the Singapore Exchange fall into two main groups: agribusiness giants with large Indonesian plantations, and the corporate banks that fund regional mining infrastructure.

SGX-listed palm oil producers like Bumitama Agri and Golden Agri-Resources are no longer operating in a free-market export environment. Every tonne of crude palm oil they harvest in Sumatra or Kalimantan must be cleared by Danantara before it can leave port.

Singapore’s big banks are also caught in this tightening regulatory grip. The direct consequence for a local retail investor holding these stocks is a sudden loss of visibility over distributions. When a company loses control over its export payment process and its ability to move foreign currency out of the country, its historical balance sheet strength becomes a secondary concern. The primary question becomes whether it can survive under a state monopoly.

🦎 Iggy’s Insight: Institutional analysts are writing notes about regional risk and currency moves. They are telling clients to watch the Jakarta index. They are looking at the wrong map. The real story is not the price of coal or palm oil. It is the structural choking of how fast transactions can happen. When a state sovereign wealth fund unit takes full control over contract matching and export payment clearance, processing times become political decisions. For Singapore retail investors, the reassurance that commodity demand remains high is useless. If the delivery pipeline narrows, the cash generation cycle slows down. That is where earnings visibility disappears. The market values certainty. Jakarta just institutionalised friction.

The Data Proof (The Evidence)

This is where the storm becomes a kitchen-table problem.

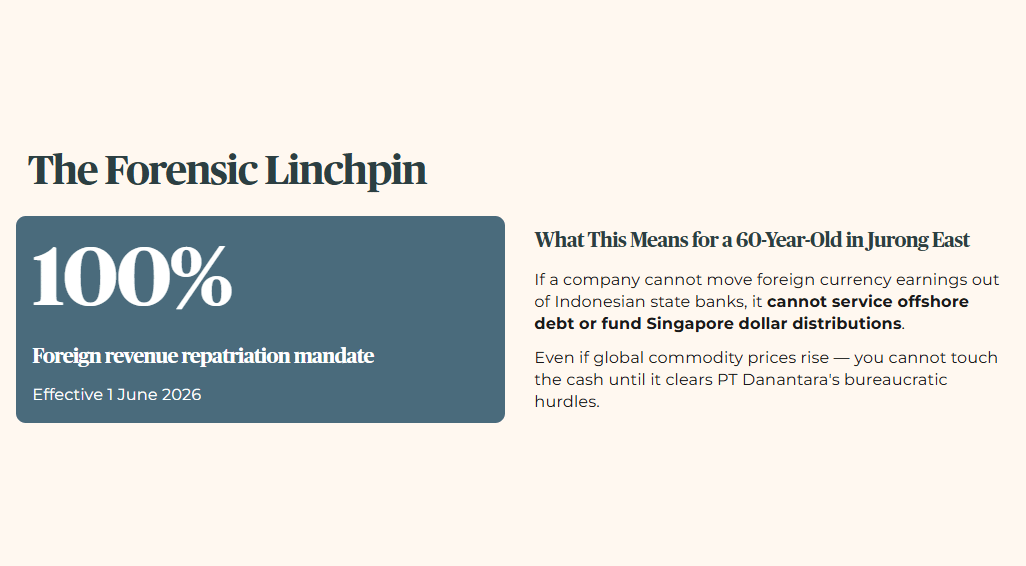

The single most important number in this entire table is the 100% foreign revenue repatriation mandate starting 1 June 2026. This is the forensic linchpin that makes all the broader macroeconomic commentary obsolete.

For a 60-year-old investor in Jurong East managing an SRS account and relying on regional agricultural or resource stocks for steady income, this single requirement creates a corporate cash block. If a company cannot move its foreign currency earnings out of Indonesian state banks, it cannot service its offshore debt or fund its Singapore dollar distributions.

Based on InvestingPro data, regional commodity companies have historically kept their main dividend-paying accounts inside the Singapore clearing system to optimise tax and liquidity. This policy severs that liquidity loop. Even if global commodity prices rise, you cannot touch the cash until it clears the bureaucratic hurdles of PT Danantara Sumberdaya Indonesia.

🦎 Iggy’s Insight: The secondary effect that retail investors are completely missing is the corporate treasury trap. Everyone is focused on whether Indonesia will physically stop palm oil or coal shipments. They will not. The state needs the volume. The real threat is the 100% foreign revenue repatriation mandate into Indonesian state-owned banks. When a Singapore-listed multinational cannot freely move its cash earnings from its Jakarta subsidiaries back to its main treasury node in Raffles Place, its operational liquidity drops. Dividends are paid from cleared treasury cash, not paper profits trapped in a state-controlled escrow account in Jakarta. The cash is locked. Your yield visibility just went out the window.

In the next section, I walk through how that 100% foreign revenue repatriation mandate, applied line by line to SGX-listed balance sheets, turns clean-looking dividend histories into cash-flow traps that fail my 4.7% retirement yield standard.