Indonesia’s Nickel Nationalism: When Jakarta Stole the Battery Chain

The 34% quota cut is a deliberate price floor. China now controls the tap, not Jakarta. Be careful.

Section 1: The Global Headline (The Storm)

Every major port city in history has faced the same existential question: what happens when the trade route moves? Malacca asked it in the sixteenth century when the winds of commerce shifted. Rotterdam asked it when containerisation rewrote European logistics overnight.

Singapore is asking it now, as the economic centre of gravity for critical materials moves south across the Java Sea. This is not just about a raw material. It is about the construction of a regional monopoly that rewrites the cost of living for every household in the heartlands.

In This Article:

The Global Headline (The Storm)

The Local Impact (The Wallet)

The Data Proof (The Evidence)

The Strategic Picture — Scenario Matrix and SGX Sector Watch

The Singapore Investor Playbook (Shock Absorption and Retirement Impact)

Outro and Disclaimer

The Corridor Economics of Base Metals has been Rewritten

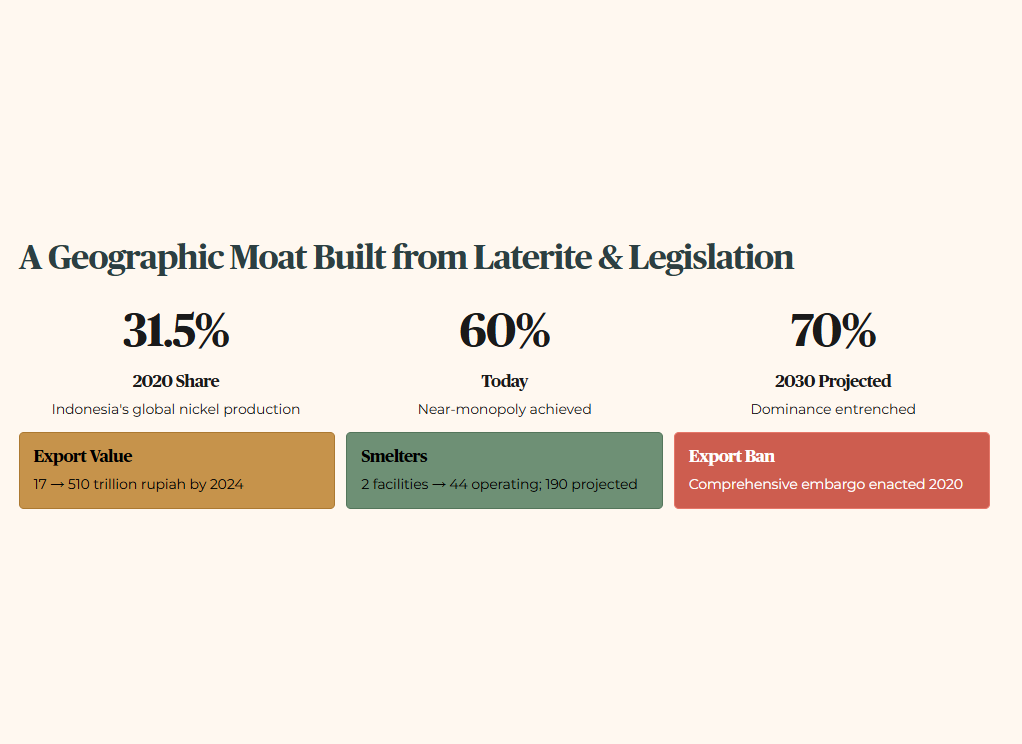

The global headline is not simply that Indonesia has captured the battery supply chain. They have fundamentally rewritten the corridor economics of base metals. Through a series of legislative export bans culminating in a comprehensive embargo in 2020, Jakarta has forced a staggering concentration of global supply. Indonesia’s share of global nickel production surged from 31.5 percent in 2020 to approximately 60 percent today.

By 2030, that figure is projected to reach 70 percent. This is no longer a free trade corridor. It is a geographic moat constructed from laterite and legislation. The export value of Indonesian nickel exploded from 17 trillion rupiah pre-ban to 510 trillion rupiah by 2024. Smelter capacity expanded with equal aggression, from just two operating facilities to over 44. Projections aim for 190 total processors — 54 in operation and 120 under construction — by the end of this year.

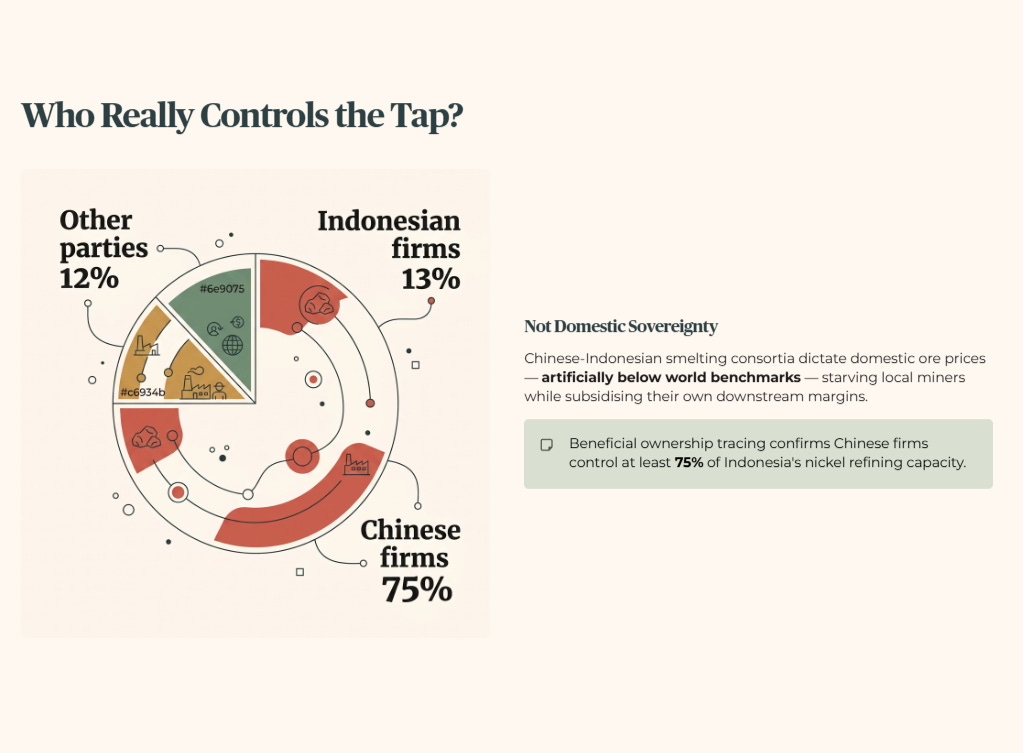

For a Singaporean investor managing CPF funds or a Supplementary Retirement Scheme portfolio, this regional monopolisation translates directly into margin risk. When one neighbour controls the raw material and another neighbour controls the capital, the local equities caught in the middle face an unprecedented squeeze. The consensus narrative broadcast by financial networks praises this “Hilirisasi” policy as a triumph of an emerging market ascending the value chain. The raw data reveals a completely different capital flow: the “Wet Market Lobang Paradox.” Jakarta acts as the market owner who bans all outside suppliers to force everyone to buy from the market’s own processing stalls.

But the “lobang” (opportunity) was captured entirely by one big wholesaler. Beneficial ownership tracing shows that Chinese firms now control at least 75 percent of Indonesia’s nickel refining capacity. Local Indonesian enterprises remain trapped in low-value activities, holding a mere 13 percent of domestic capacity. This is not domestic sovereignty. It is a monopsony where Chinese-Indonesian smelting consortia dictate domestic ore prices, keeping them artificially below world market benchmarks to starve local miners while subsidising their own downstream margins.

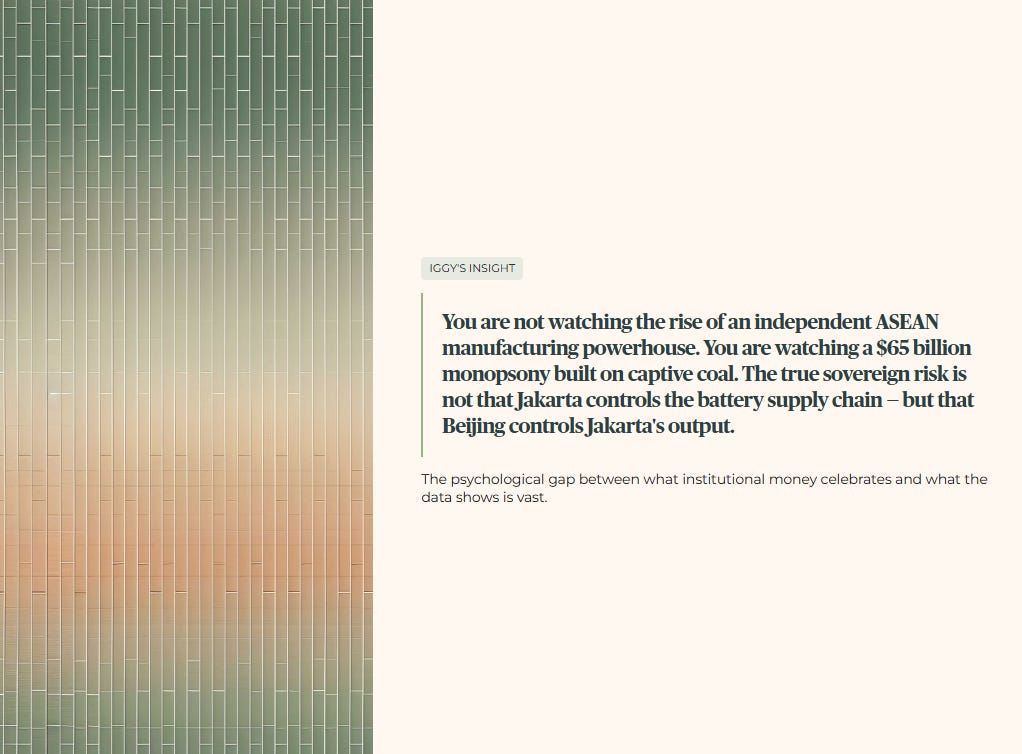

Iggy’s Insight The psychological gap between what institutional money is celebrating and what the data actually shows is vast. Global headlines praise a developing nation ascending the value chain, securing its economic sovereignty through raw material embargoes. The balance sheet archaeology tells a completely different story of proxy control. You are not watching the rise of an independent ASEAN manufacturing powerhouse. You are watching a 65 billion dollar monopsony built on captive coal. The true sovereign risk is not that Jakarta controls the battery supply chain, but that Beijing controls Jakarta’s output. End of story.

Section 2: The Local Impact (The Wallet)

The corridor shift across the archipelago does not stay confined to industrial parks in Morowali. It walks straight into your daily expenses and reshapes the calculus of your retirement planning. The most immediate transmission mechanism is the cost of living, specifically through the materials required to feed the nation. Hawker food inflation in Singapore reached 6.1 percent recently, with staple noodle and rice items rising up to 8 percent. Labour and rent take the blame, but the hidden tax is the metal itself. Nickel is the primary cost driver for Type 304 stainless steel, the exact alloy used in 90 percent of Singaporean commercial kitchens.

A standard hawker stall in Toa Payoh undertaking a full stainless steel kitchen fit-out today faces a material cost increase of 12 to 15 percent compared to 2020. The export bans drive this entirely through regional melt cost volatility. When the capital cost of outfitting a stall rises that sharply, the hawker does not absorb it. They pass it forward into the price of your chicken rice. This is the first-order wallet impact of Indonesian nickel nationalism. Furthermore, rising nickel processing costs contribute to global green inflation, indirectly affecting the cost of electric vehicle charging infrastructure being rolled out across HDB car parks.

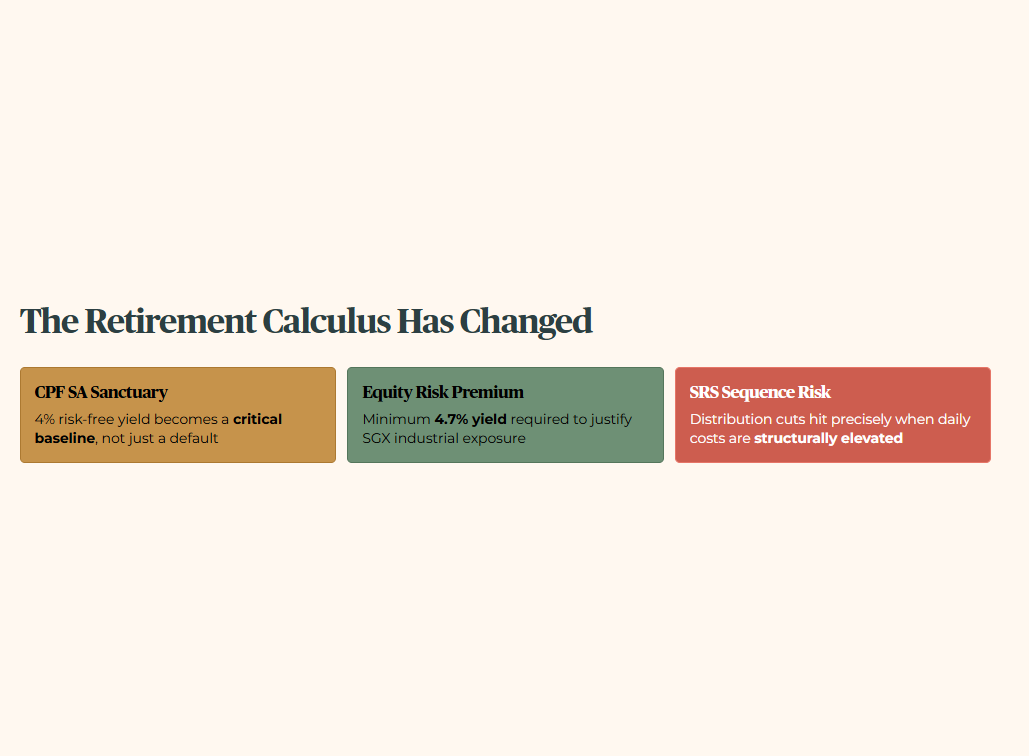

This dual pressure alters the fundamental risk-free calculus for your retirement funds. The 4 percent yield from the CPF Special Account transitions from a simple baseline into a critical sanctuary. To justify pulling money out of that sanctuary and deploying it into the market, investors must demand a higher equity risk premium. Based on the fundamental forensic architecture, you currently require a minimum 4.7 percent yield to offset the volatility of SGX-listed industrials exposed to the Jakarta-Beijing axis. If you are drawing down your SRS account for dividend income, you face a heightened sequence-of-returns risk. Should the distress in Indonesian smelters trigger distribution cuts across local counters, your income shrinks precisely when the cost of daily necessities is structurally elevated.

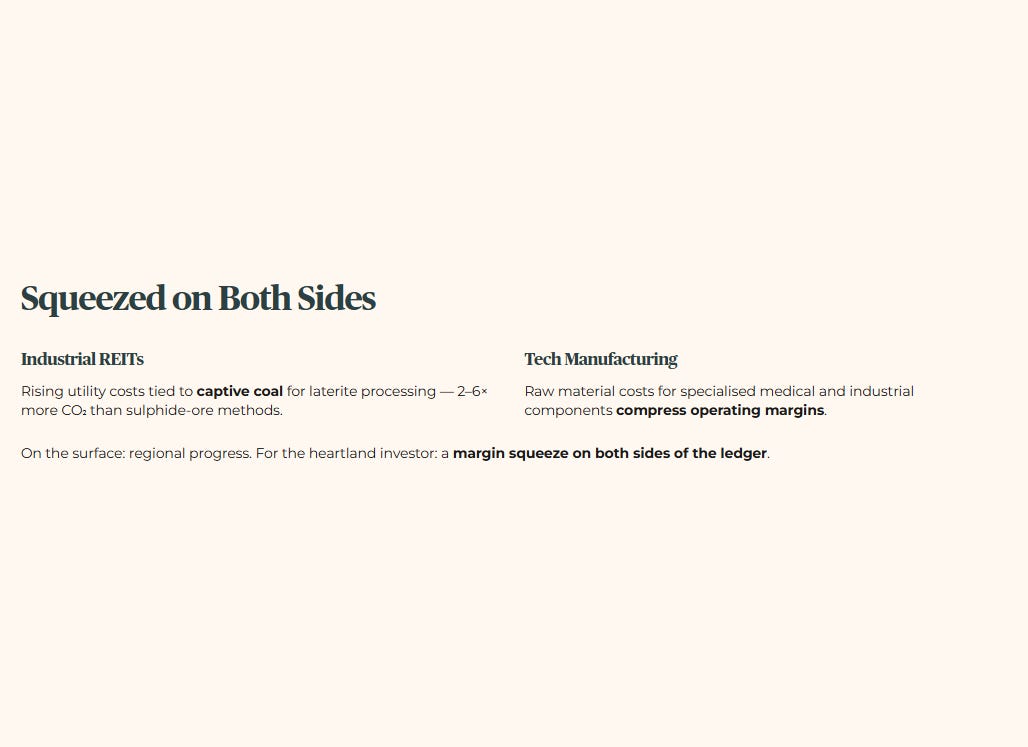

We see this pressure forming clearly in two specific sectors. Industrial real estate investment trusts face rising utility costs tied to captive coal required for laterite processing. This energy-intensive method requires two to six times more CO2 than traditional sulphide-ore methods. Simultaneously, the technology manufacturing sector watches raw material costs for specialised medical and industrial components compress their operating margins. On the surface, the regional macro story sounds like progress. But for the heartland investor, it is a margin squeeze on both sides of the ledger.

Iggy’s Insight The second-order effect that retail investors are completely failing to price into their portfolios is the shadow cost of captive coal. Indonesia’s captive coal capacity exceeded 15.5 gigawatts in 2024, with another 5 gigawatts in the pipeline for 2026. As Singapore tightens its mandatory ESG reporting requirements, that embedded carbon becomes a direct financial liability for every firm in your portfolio. The punchline is that your supposedly green investments will eventually bear the margin-crushing cost of offsetting the very supply chain they depend on.

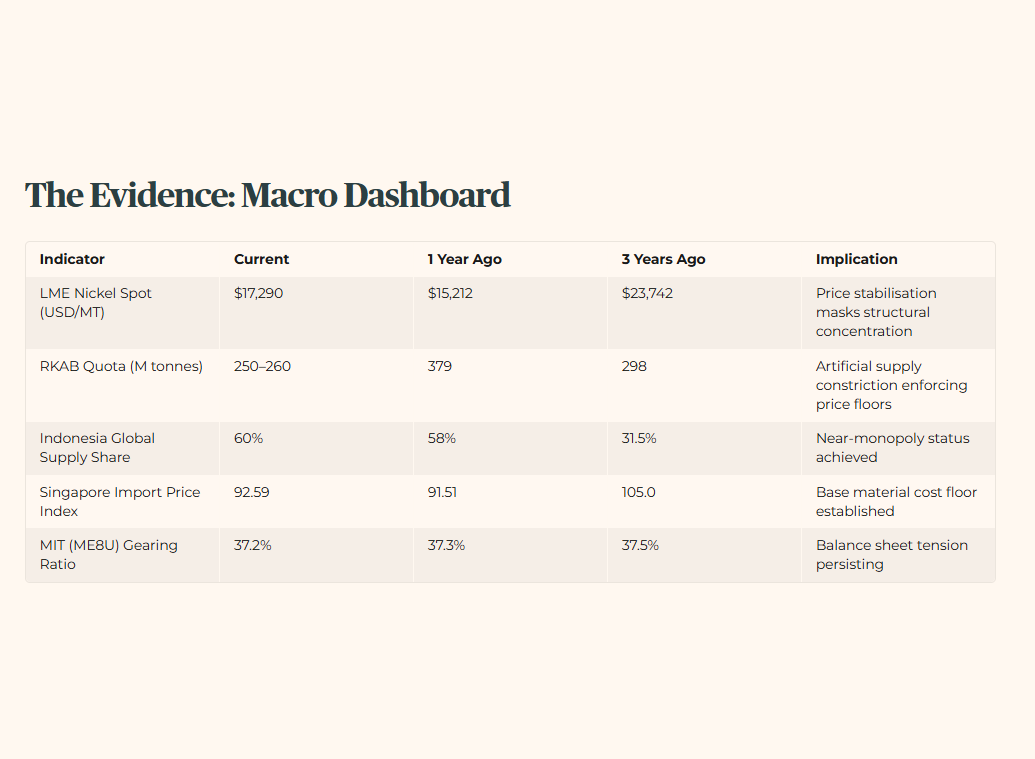

Section 3: The Data Proof (The Evidence)

The 2026 RKAB production quota reduction is the definitive signal that Indonesia has pivoted from market share growth to price-setting dominance.

Table 1: Macro Evidence Dashboard

The 34 percent reduction in the 2026 RKAB production quota — dropping from 379 million tonnes down to 250 million tonnes — is the singular signal that changes everything. This is the forensic linchpin: Indonesia has intentionally throttled its own output to ensure prices never return to a free-market equilibrium.

The 34 percent quota cut is the first fracture line — but the next section’s yield and stress-test calculations are where the real damage to your CPF and SRS retirement math actually shows up.