Don’t Buy The REIT. The "Hidden" IOI Trade Revealed

Two massive REIT listings, two different currencies, and one clear mission: to save the balance sheet. Here is why Singaporean investors need to look past the headline numbers.

IOI Properties is planning to spin off nearly USD 8 billion (S$10.7 billion) in real estate assets across two separate REITs in Malaysia and Singapore.

If you only read the headlines, this looks like a standard “growth story.” A developer monetizing assets to build more.

But if you look at the balance sheet, the story changes. This isn’t just about growth; it is about survival and sustainability. With net gearing potentially spiking to 0.93x following the massive South Beach acquisition, IOI Properties is sitting on a mountain of floating-rate debt that is increasingly expensive to service.

For Singaporean investors—especially those of you chasing yield for your SRS or cash portfolios—this dual-listing presents a unique, albeit complex, opportunity. But is it a “Buy”?

Let’s dig into the numbers.

In This Article:

• The Blueprint: One Giant, Two REITs

• The Context:

• Iggy’s Insight:

• The “Why”: The Debt Trap

• The Singapore Office Dilemma

• Iggy’s Insight:

• The Verdict: How to Play This

• Iggy’s Insight:The Blueprint: One Giant, Two REITs

IOI Properties isn’t just launching one REIT; they are attempting a rare “dual-market” strategy. They plan to package their Malaysian retail assets into a Bursa-listed REIT (2026) and their prime Singapore office assets into an SGX-listed REIT (2027).

Here is the breakdown of the proposed split:

The Context:

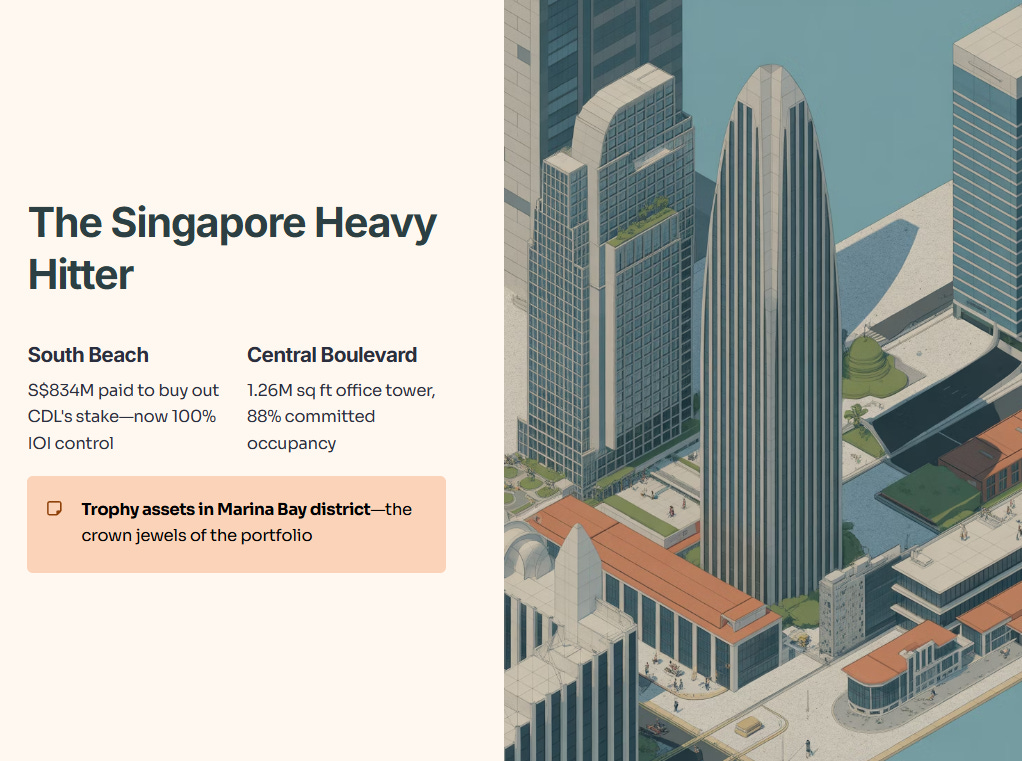

The Singapore leg of this deal is the heavy hitter. The South Beach complex and IOI Central Boulevard Towers are absolute “trophy assets” in the Marina Bay district.

South Beach: IOI recently paid S$834 million to buy out CDL’s stake, taking 100% control.

Central Boulevard: A massive 1.26 million sq ft office tower that is slowly filling up (88% committed occupancy).

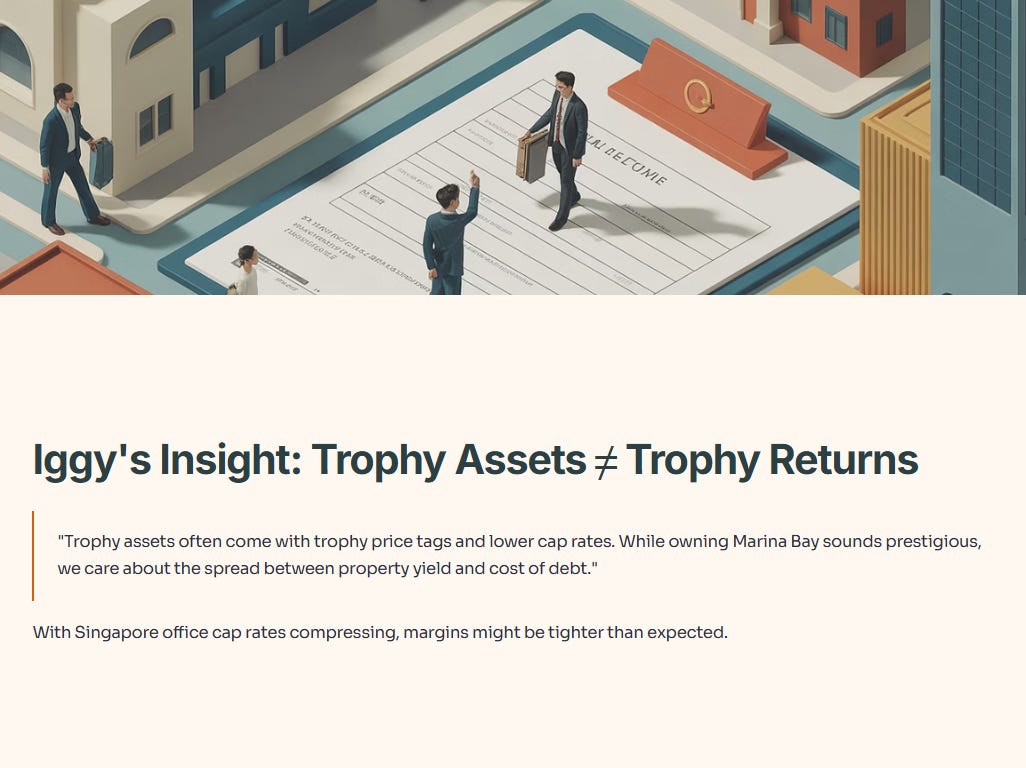

Iggy’s Insight:

Be careful not to confuse “Trophy Assets” with “Trophy Returns.” Trophy assets often come with trophy price tags and lower capitalization rates (yields). While owning a piece of Marina Bay sounds prestigious, as dividend investors, we care about the spread between the property yield and the cost of debt. With Singapore’s office cap rates compressing, the margins here might be tighter than you think.

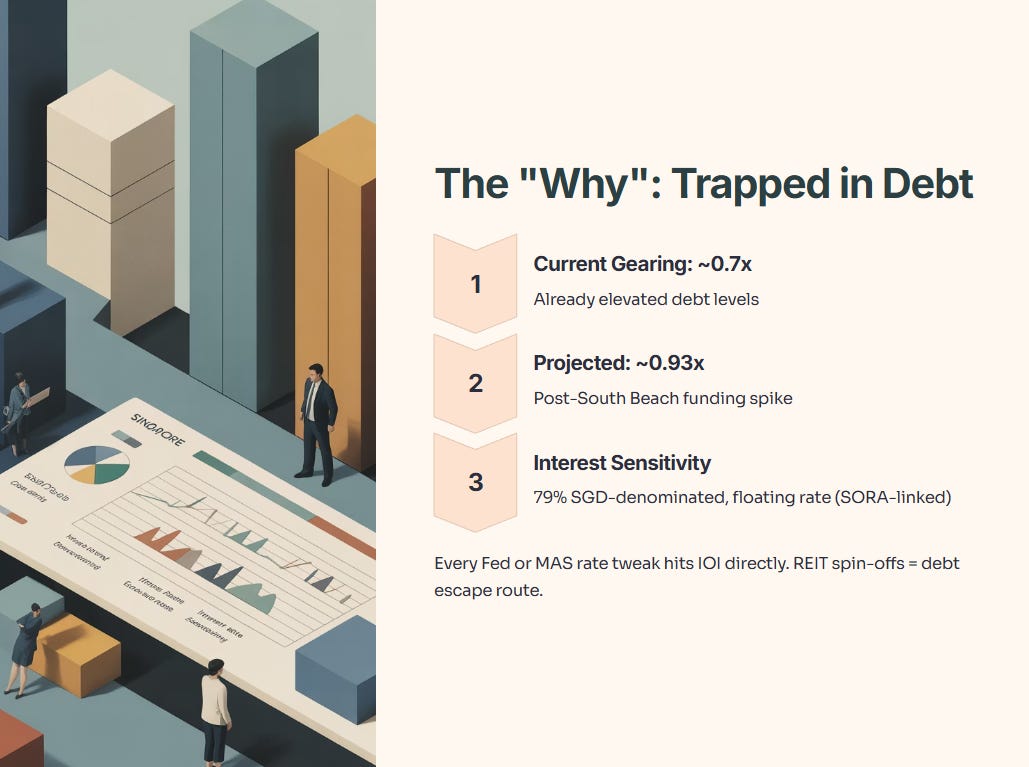

The “Why”: The Debt Trap

Why go through the headache of two separate listings? Debt.

IOI Properties is currently holding a significant amount of debt, much of it denominated in SGD to fund their Singapore expansion. With interest rates staying “higher for longer,” this debt is eating into their core net profits.

The Financial Squeeze:

Current Gearing: ~0.7x

Projected Gearing: ~0.93x (Post-South Beach funding)

Interest Sensitivity: ~79% of borrowings are SGD-denominated and floating rate (linked to SORA).

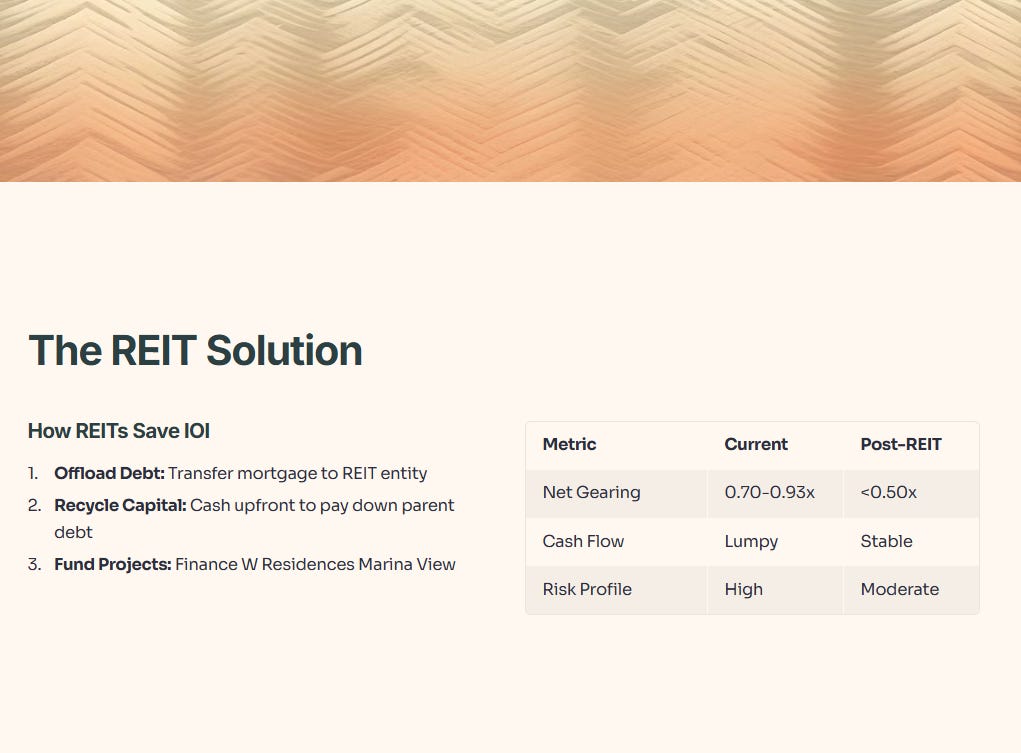

Every time the US Fed or MAS tweaks rates, IOI feels it. By spinning these assets off into REITs, they can:

Offload Debt: Transfer the mortgage to the REIT entity.

Recycle Capital: Get cash upfront to pay down parent-co debt or fund the new W Residences Marina View project.

The Singapore Office Dilemma

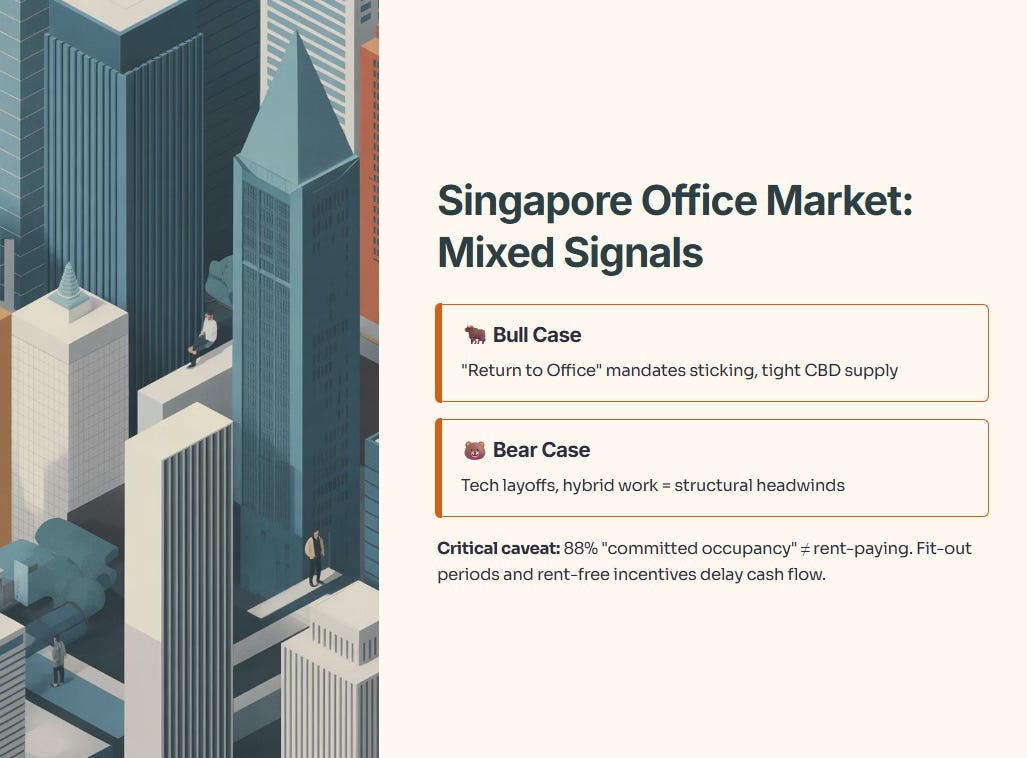

The success of the Singapore REIT (listing 2027) hinges entirely on the Singapore Office Market.

Right now, the market is sending mixed signals.

Bull Case: “Return to Office” mandates are sticking, and supply in the CBD is tight.

Bear Case: Tech layoffs and hybrid work are structural headwinds.

IOI Central Boulevard Towers is a massive injection of supply. While they report “88% committed occupancy,” remember that committed does not always mean rent-paying. There are fit-out periods and rent-free incentives that delay cash flow.

Iggy’s Insight:

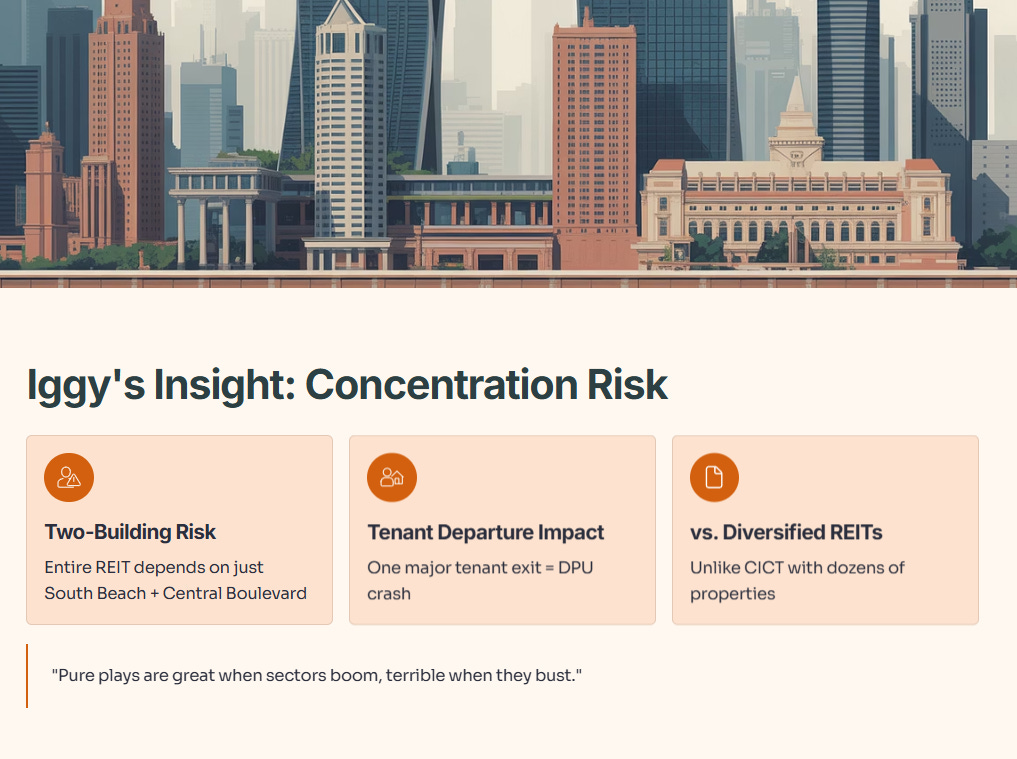

There is a specific risk here called “Concentration Risk.” This proposed Singapore REIT would essentially be a play on just two (massive) buildings. If one major tenant leaves Central Boulevard or South Beach, the DPU (Distribution Per Unit) gets hit hard. Unlike a diversified REIT like CapitaLand Integrated Commercial Trust (CICT) which owns dozens of malls and offices, this IOI REIT will be a “pure play” on Marina Bay offices. Pure plays are great when the sector booms, and terrible when it busts.

The Verdict: How to Play This

We have two years before the Singapore IPO. Here is how I am looking at this trade.