Can Mapletree Logistics Trust Survive 40.6% Gearing With 2.9x ICR | 4Q FY24/25 Results | 🦖EP1591

Gearing 40.6% breaches 35% ceiling while ICR 2.9x means banks get paid before you do

1. Cold Open

Exactly 37.8 percent of the current quarter distribution from Mapletree Logistics Trust is a return of your own capital, not organic cash flow. If you rely on this asset to fund your Supplementary Retirement Scheme withdrawals, your underlying principal is bleeding out to maintain an optical payout. This forensic audit strips away the management narrative of operational stability to expose the severe structural leaks threatening your dividend.

Mapletree Logistics Trust has been sitting in the portfolios of retiring Singaporeans for years — not because it was exciting, but because it felt reliable. A logistics landlord with Asian reach, a name you could explain to your spouse over dinner without a whiteboard. When the 4Q results landed, I went through the deck the same way I go through every set of numbers — slowly, and with the assumption that the headline is not the whole story.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips — the interest coverage, the gearing, the free cash flow sustainability — so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

In This Article:

The Slide by Slide Audit

Distribution Per Unit and Income Quality

Gearing Ratio and the Debt Wall

Interest Coverage Ratio

Rent Reversion and the China Portfolio Drag

Tax Provisions and Capital Drain

The Reality Check

The Scorecard and Yield Spread

The Forward Outlook

Outro and Disclaimer

2. The Slide by Slide Audit

We evaluate the earnings report exactly as management presented it, but we process the numbers through a strict forensic filter. For industrial landlords and real estate investment trusts, we lead with Distribution Per Unit and Gearing. These two metrics dictate whether your retirement income survives a macro shock.

Distribution Per Unit and Income Quality

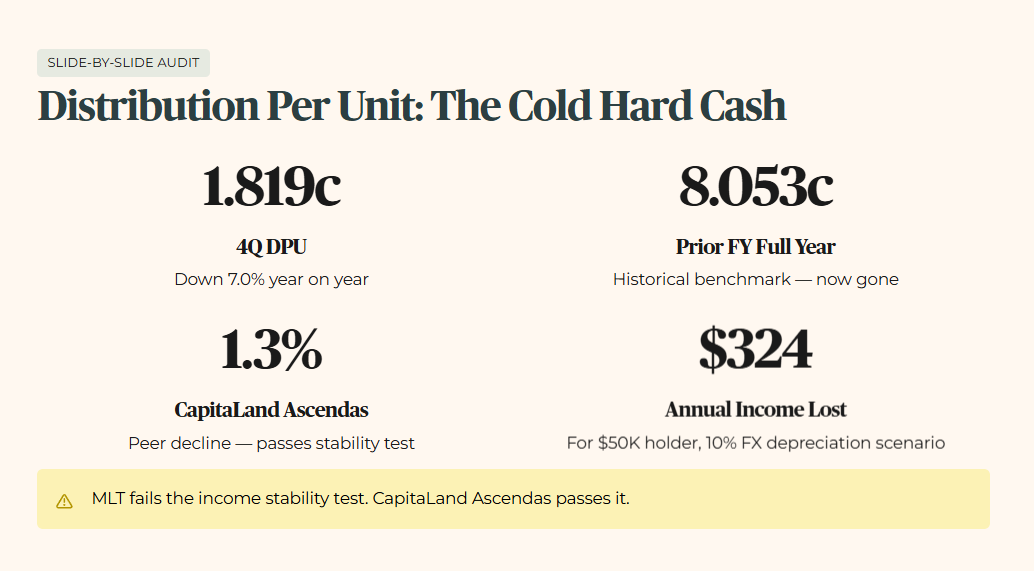

The raw fact is that the total Distribution Per Unit for the fourth quarter contracted by 7.0 percent year on year to 1.819 cents. Distribution Per Unit is the actual cold, hard cash deposited into your bank account every quarter. This falls sharply against the historical benchmark of the Trust. In the prior financial year, the full year payout stood at a much healthier 8.053 cents.

When we look at peer context, CapitaLand Ascendas REIT experienced a mere 1.3 percent decline for their full year. CapitaLand Ascendas passes the income stability test, while Mapletree Logistics Trust fails it.

For a forward scenario, consider a 10 percent further depreciation in regional currencies against the Singapore dollar. This specific macro trigger would shave an estimated 5 percent off the current yield. The wallet impact is visceral. For a 55 year old Singaporean holding 50,000 dollars in this asset, this translates directly to a loss of 324.18 dollars in annual income. That is a tangible cut to your household budget.

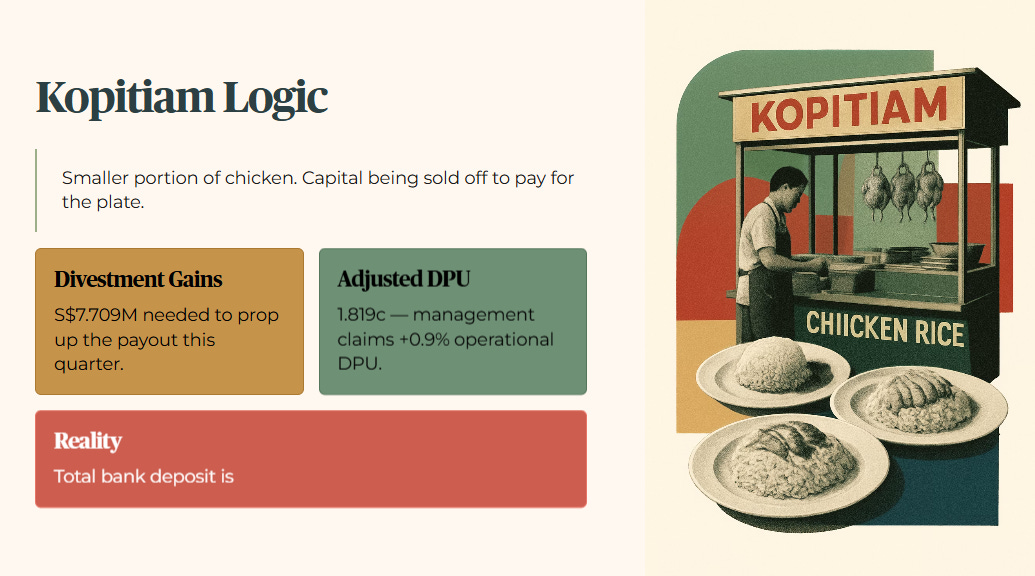

Think of this using Kopitiam Logic. If your favourite stall raises prices but gives you a smaller portion of chicken, you are paying more for less. Here, management is giving you a smaller portion of cash while the underlying chicken, your capital, is being sold off to pay for the plate. We see this in the 4Q FY24/25 figures where divestment gains of 7.709 million dollars were needed just to prop up the payout. Without those gains this quarter, the Adjusted DPU is 1.819 cents. While they claim this is a 0.9 percent increase in operational DPU, it does not change the fact that your total bank deposit is shrinking.

Gearing Ratio and the Debt Wall

The raw fact is that aggregate leverage sits at 40.6 percent. Gearing is simply how much of the property portfolio is bought with borrowed money. This elevated figure sits uncomfortably above the historical average of the Trust, representing a structural upward creep from the 39.0 percent seen in the prior period.

Against our peer context, CapitaLand Ascendas REIT maintains a much safer gearing of 39.0 percent. CapitaLand passes our safety test, but Mapletree Logistics Trust fails the strict 35.0 percent forensic ceiling.

Looking at a forward scenario, if a severe recession triggers a 10 percent downward revision in portfolio property valuations, gearing would immediately spike above 45 percent. This macro trigger breaches the regulatory ceiling. The wallet impact for a heartland investor is brutal. You would face a deeply discounted equity fund raising. You would have to inject fresh capital just to maintain your current stake, or suffer permanent dilution to your retirement portfolio.

Management points to a well staggered debt maturity profile with an average duration of 3.6 years. But look closer at the debt profile post swap. JPY debt makes up 26 percent and RMB debt makes up 23 percent. These are volatile currencies. If the Yen continues its roller coaster ride, your gearing is at the mercy of exchange rates, not just interest rates. The debt wall for FY28/29 and FY29/30 is particularly steep, representing 22 percent and 21 percent of total debt respectively. We are looking at a cumulative 43 percent of the balance sheet that must be refinanced in a high rate environment within a two year window.

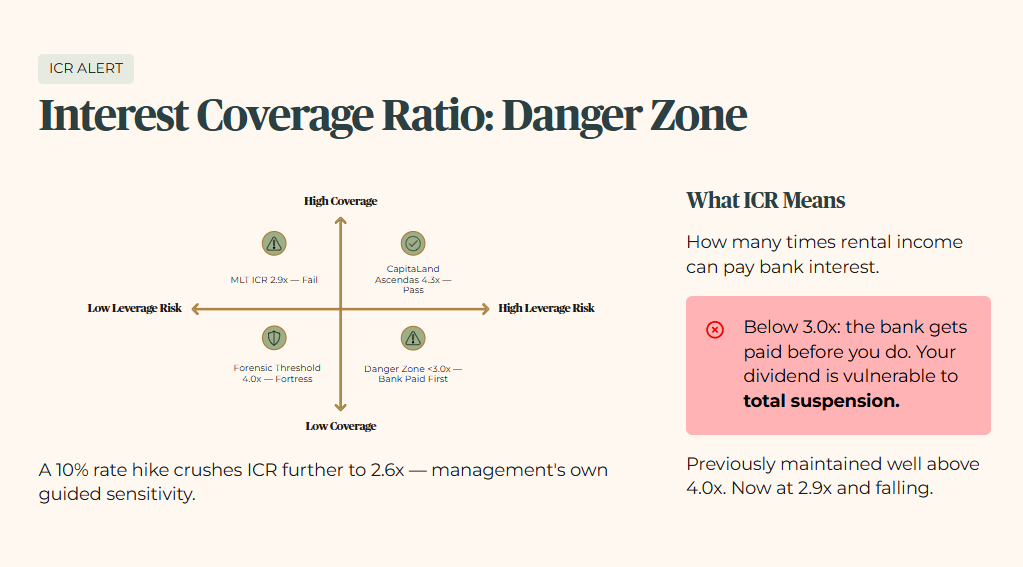

Interest Coverage Ratio

The raw fact is that the Interest Coverage Ratio has compressed to a dangerous 2.9 times. The Interest Coverage Ratio tells us how many times the rental income can pay the bank interest. Management previously maintained this ratio well above 4.0 times.

In peer context, CapitaLand Ascendas REIT boasts a coverage ratio of 4.3 times. They comfortably pass the fortress standard, while Mapletree Logistics Trust fails this critical debt safety check.

For a forward scenario, a 10 percent unexpected hike in base lending rates would crush the coverage ratio further down to 2.6 times. This is the exact sensitivity management guided for in their results deck. The trigger here is sticky inflation forcing central banks to hold rates higher for longer. The wallet impact is severe. For an investor relying on dividends, a coverage ratio below 3.0 times means the bank gets paid before you do. Your dividend becomes highly vulnerable to total suspension.

Rent Reversion and the China Portfolio Drag

Rent reversion measures whether new leases are signed at higher or lower rates than the expiring ones. The raw fact is that the China portfolio, representing 18.3 percent of total assets under management, delivered a negative 2.0 percent rent reversion. This is an improvement from negative 9.4 percent a year ago, but it is still a loss of income.

Historically, the China portfolio was a growth engine. Now, it is a lead weight. In peer context, Singapore industrial assets are seeing positive reversions of 5.8 percent. Mapletree Logistics Trust is being dragged down by its exposure to a sluggish Chinese recovery.

The wallet impact is a sustained drag on your dividend growth until that specific market clears its oversupply. For a Singaporean retiree, your global diversification is currently working against you, as the Singapore strength of 20.8 percent of AUM cannot offset the regional weakness.

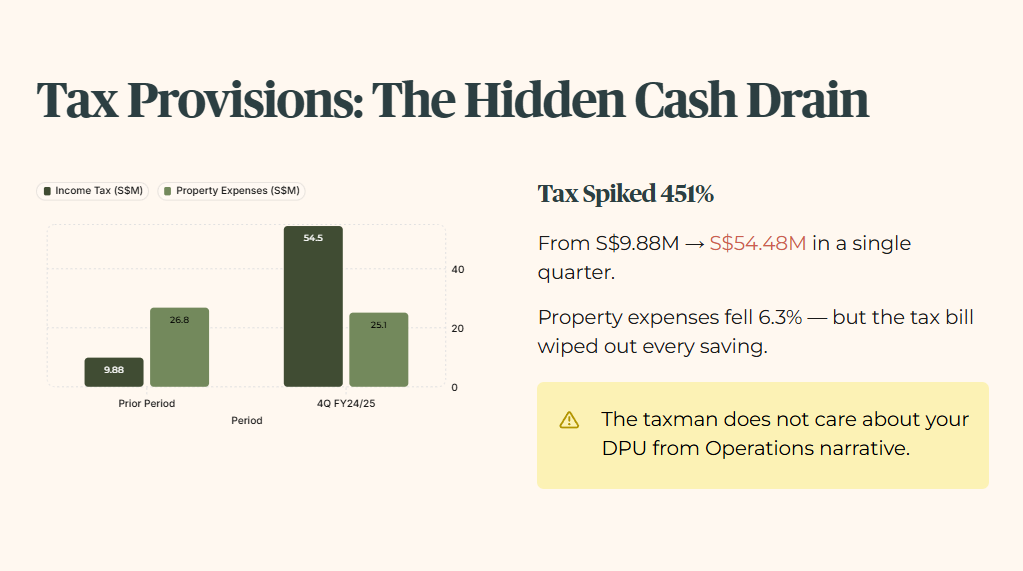

Tax Provisions and Capital Drain

The raw fact is that income tax for the quarter spiked violently to 54.48 million dollars, up from 9.88 million dollars in the prior period. The wallet impact is a massive, immediate drain on cash that should have been distributed to unitholders. While property expenses actually decreased by 6.3 percent to 25.132 million dollars, the tax bill wiped out those savings. When management talks about operational efficiency, they forget to mention that the taxman does not care about your DPU from Operations narrative.

🦎 Iggy’s Insight

Management spent almost no time addressing the severe internal auditing failure regarding the statutory exchange filing. Inverting the financial columns for the fourth quarter is not a minor administrative slip. It points to structural fatigue in the compliance layer. When a multi billion dollar entity cannot align its statutory profit and loss statements correctly, it forces us to question the rigour applied to property valuations and currency hedging calculations. Silence on compliance failures is the loudest warning sign for forensic auditors. The numbers do not lie, but the people typing them occasionally do. Forensic auditors watch the hands, not the mouth.

3. The Reality Check

We must contrast the optimistic guidance provided by management against the cold math of the InvestingPro Fair Value model. Management claims they are delivering stable portfolio and financial metrics. And let us be honest, they are not wrong about the occupancy rate holding at 96.9 percent. But here is the uncomfortable truth regarding valuation.

The InvestingPro Fair Value sits at 1.43 dollars. The current market price closed at 1.220 dollars. This means the stock is trading at a discount to forensic fair value by approximately 14.6 percent. However, we have a massive Forensic Gap Alert triggered by street consensus.

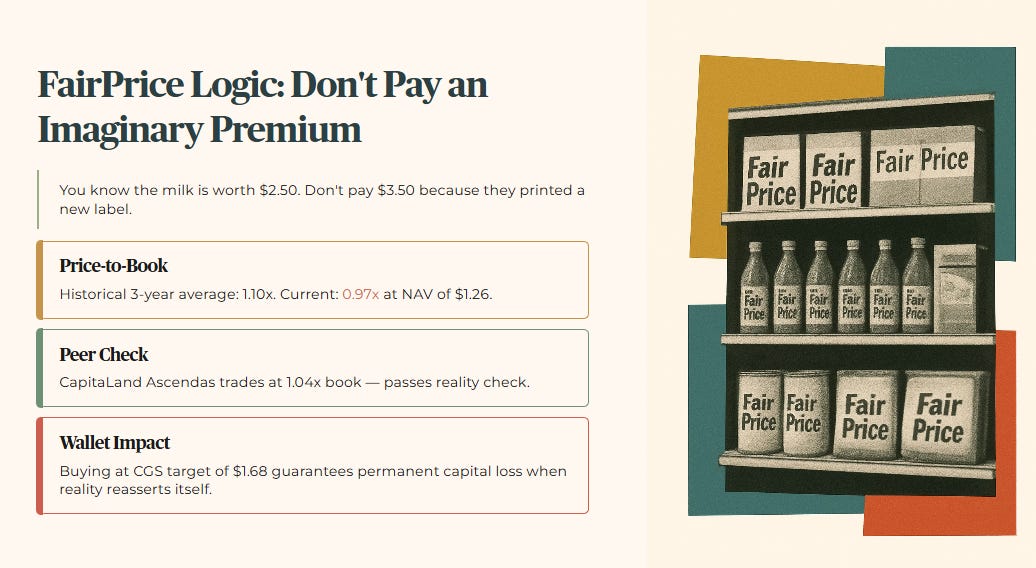

CGS International issued an add rating with a target price of 1.680 dollars. This target diverges from the forensic fair value by a staggering 17.3 percent. We must apply the five layer audit to this divergence.

Raw Fact: The CGS target of 1.680 dollars is verbatim from their latest analyst note. Historical Benchmark: Historically, the asset trades at a price to book ratio of 1.10 times over a three year average. At a Net Asset Value of 1.26 dollars, the price is currently at 0.97 times book value. Peer Context: CapitaLand Ascendas REIT trades at 1.04 times book value, passing the reality check. Forward Scenario: If the cost of debt rises by 10 percent, the aggressive terminal growth rates assumed in the CGS model will collapse. Wallet Impact: Buying at the street target of 1.680 dollars guarantees a permanent capital loss for a heartland investor when reality reasserts itself.

Think of this using FairPrice house brand logic. You know a carton of house brand milk is worth exactly 2.50 dollars. If a promoter tries to sell it to you for 3.50 dollars because they printed a new label on the box, you walk away. Price is what you pay, but value is what you get. Do not pay an imaginary premium for your retirement assets.

4. The Scorecard and Yield Spread

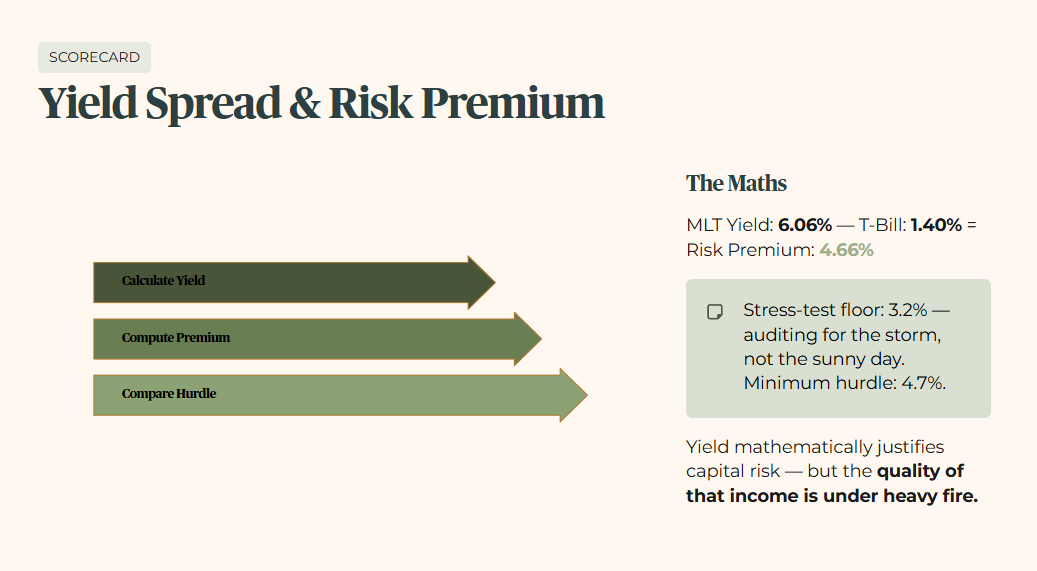

We calculate the true risk premium by taking the current asset yield and subtracting the risk free rate. The current Mapletree Logistics Trust yield sits at 6.06 percent. We subtract the Singapore 6 Month T-Bill Rate of 1.40 percent. This provides a risk premium of 4.66 percent.

Note on the Stress-Test Buffer: For this audit, I apply a conservative floor of 3.2 percent. We audit for the storm, not just the sunny day. While the T-Bill sits at 1.40 percent, I do not lower my standards to match a temporary market dip. My floor remains at 3.2 percent to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7 percent — that is the 3.2 percent floor plus 150 basis points of mandatory risk premium.

Our forensic verdict confirms the yield mathematically justifies the capital risk for income investors, but the quality of that income is under heavy fire.

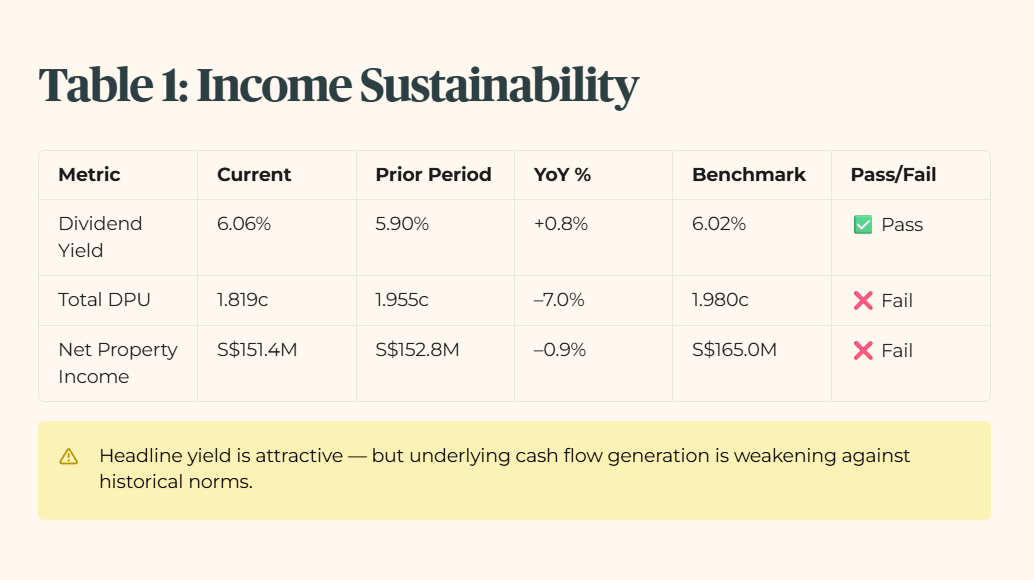

Table 1: Income Sustainability

Forensic Verdict: The headline yield is attractive, but the underlying cash flow generation is weakening against historical norms.

The current dividend yield is 6.06 percent. The prior period yield was 5.90 percent. This represents a year on year positive change of 0.8 percent. The sector benchmark provided by CapitaLand Ascendas REIT is 6.02 percent. The asset passes this specific income sustainability check. However, the total DPU of 1.819 cents is a 7.0 percent drop from the 1.955 cents seen in 4Q FY24/25. Net Property Income is 151.444 million dollars, down from 152.801 million dollars.

The forensic problem is that once you decompose that 6.06 percent yield into true cash generation versus capital recycling, the share of “real” income left on the table looks very different from what the headline suggests.