Is DBS Still Safe for Retirement at 2.4x Book Value?

What happens when your 'safe' dividend stock becomes 30% of your net worth

The Singapore market has a favorite pastime: collecting bank dividends and pretending it’s a “diversified strategy.” If you open your portfolio today, there is a statistically high probability that DBS, OCBC, and UOB make up the lion’s share of your net worth. On the surface, it looks like a masterstroke. Since 2020, DBS has delivered a total return of roughly 154%, turning a modest 15% position into a 30% monster through sheer organic growth. You didn’t necessarily choose to become a concentrated “Banker,” but the market forced the role upon you.

The contrarian truth, however, is that you are currently running a portfolio that would be illegal for a professional US mutual fund manager to operate. While retail investors poured nearly S$4 billion into these three banks in 2025 alone, they are ignoring a fundamental law of physics in finance: concentration works both ways. You think you are diversified because you own “The Big Three,” but since they all move on the same interest rate and credit cycle drivers, you aren’t holding three stocks—you’re holding one giant, leveraged bet on the MAS and the Fed.

In This Article:

The Masterclass: Portfolio Drift and the 25% Rule

Step 1: The Health Check

Educational Note: Concentration Risk

Educational Note: CET1 Ratio

Iggy’s Insight

Step 2: The Wealth Check

Educational Note: Payout Ratio

Iggy’s Insight

Step 3: The Price Check

Iggy’s Insight

Step 4: The Future Check

The Bottom Line (Strategic Conclusion)

InvestingPro Reality Check

Iggy's VerdictAbout Iggy & the Elite 150

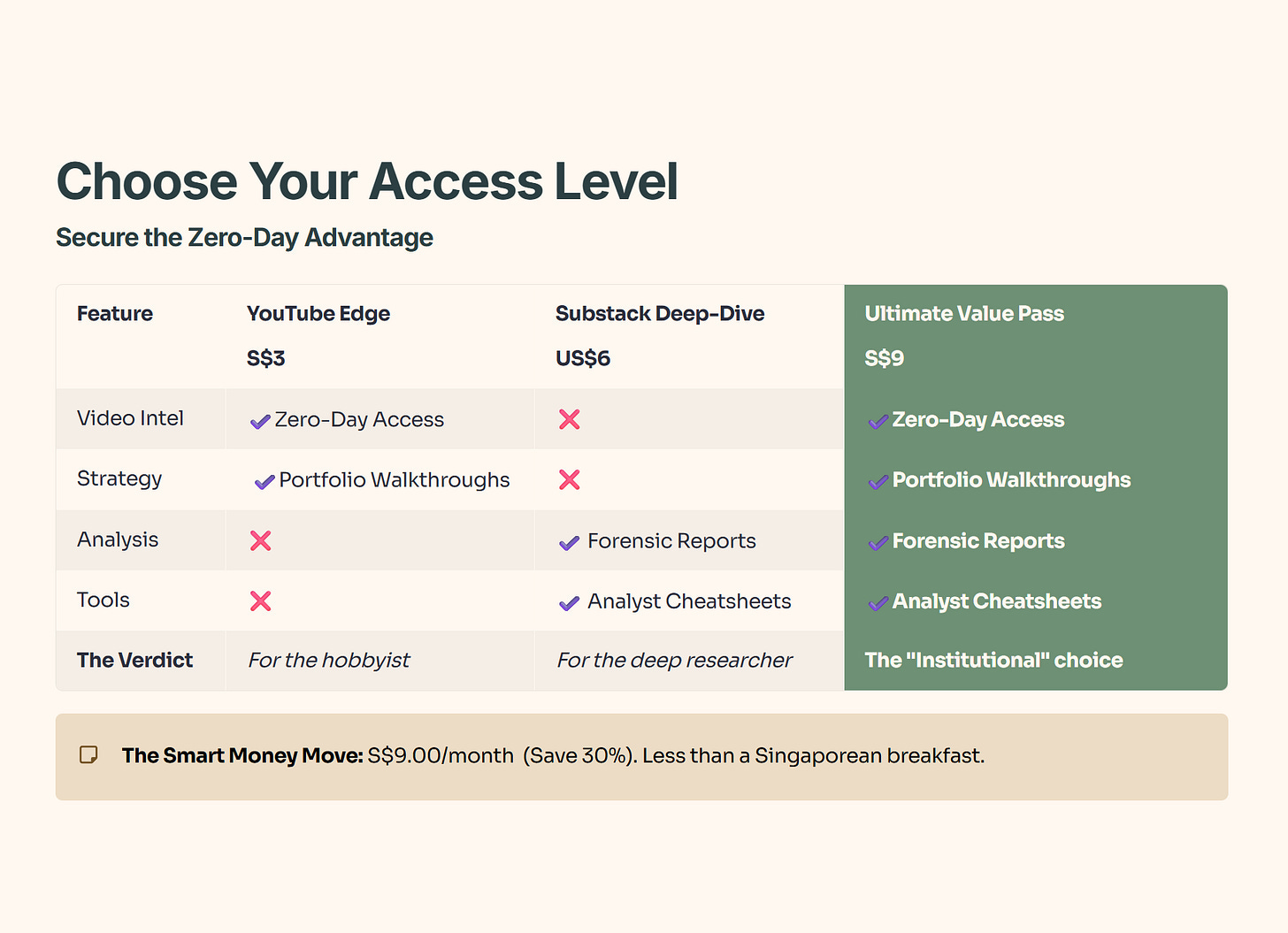

🦎 Join the Inner Circle: Secure Your Zero-Day Advantage

In the Singapore market, the gap between a winning entry and “holding the bag” is often just 48 hours. While 5,800+ readers wait two weeks for the “Old News” version, my Inner Circle gets the data while the opportunity is still live.

🚨 Stop Trading on a Delay

Free subscribers wait 14 days to see my analysis. In this jungle, if you aren’t first, you’re lunch. Get the data while it’s fresh.

Choose Your Edge:

⚡ Zero-Day Access: Watch every deep-dive video the second it’s rendered. No delays, no missed entries.

📂 The Forensic Vault: Get the full forensic reports and portfolio walkthroughs where I strip away the corporate hype to reveal the hard math behind every Singapore blue chip.

💎 The “Smart Money” Bundle: Get the full S$9/mo Pass (YouTube + Substack). It’s less than the cost of two coffees at Toast Box to trade with the same data as the pros.

[👉Join 150+ Investors in the Inner Circle Here]

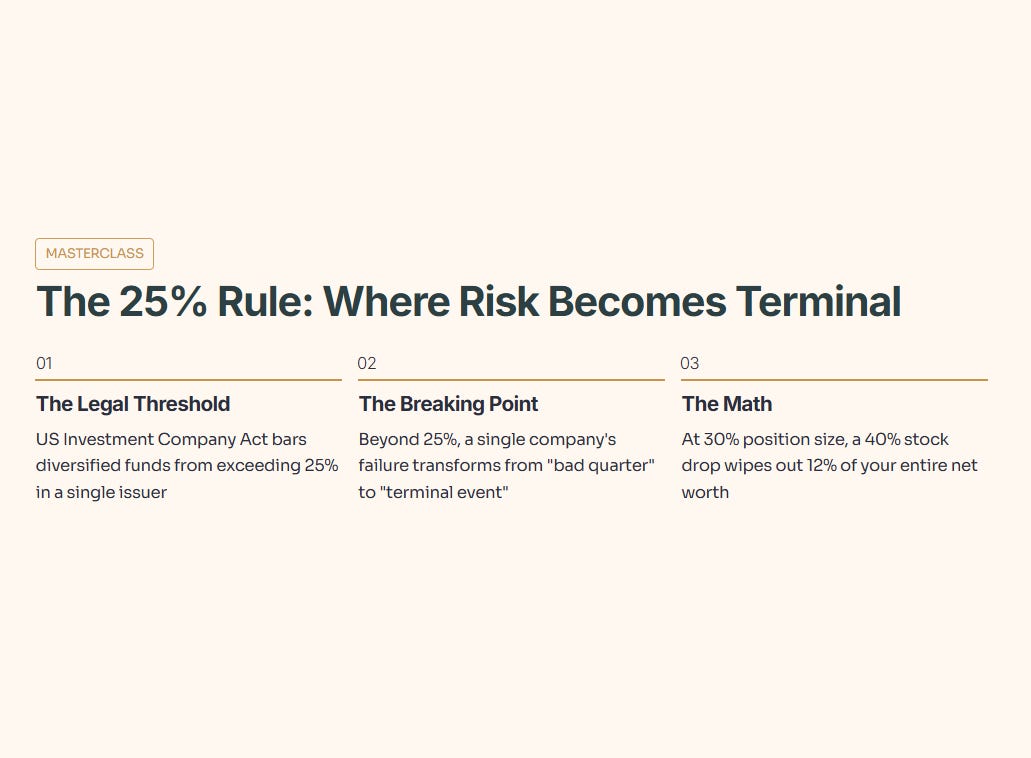

The Masterclass: Portfolio Drift and the “25% Rule”

Before we look at the numbers, we need to understand why the “25% Rule” exists. In the professional world, specifically under the US Investment Company Act, a “diversified” fund is legally barred from putting more than 25% of its assets into a single issuer. This isn’t an arbitrary number; it is the point where a single company’s failure ceases to be a “bad quarter” and becomes a “terminal event” for your wealth.

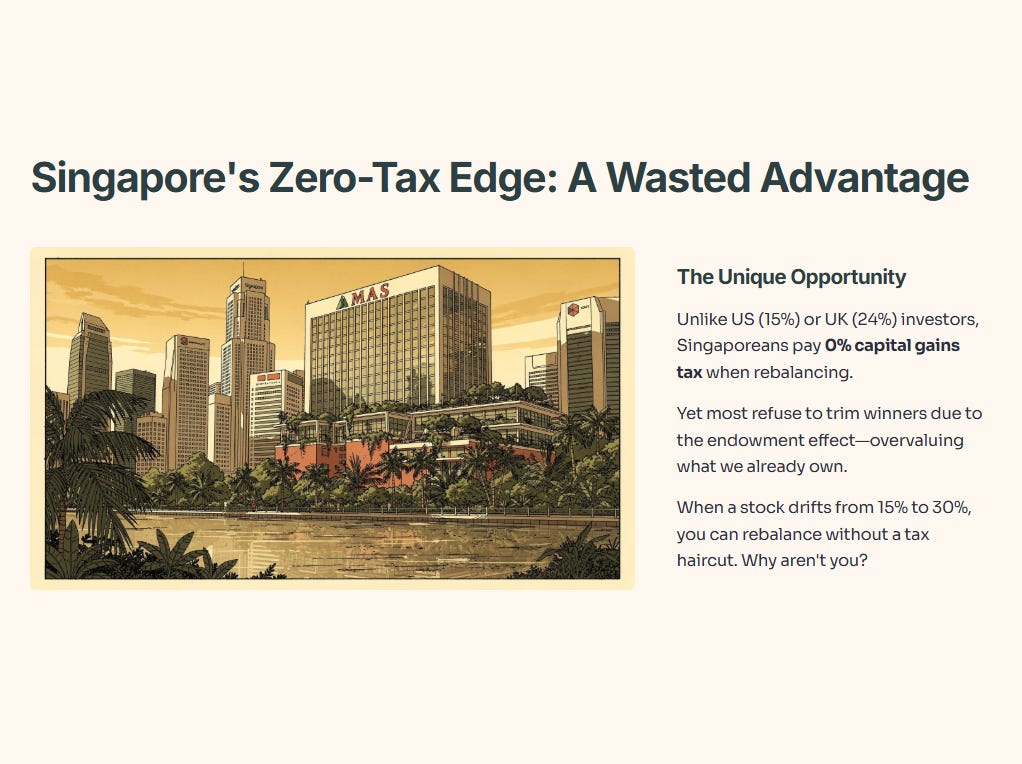

In Singapore, we have a unique “Zero-Tax Edge.” Unlike investors in the US or UK who lose 15% to 24% of their gains to the taxman when they rebalance, a Singaporean investor can trim a winner for a 0% tax hit. This makes the 25% rule even more powerful here. If a stock drifts from 15% to 30% of your portfolio, you can move that capital back to safety without a “tax haircut,” yet most investors refuse to do it because of the endowment effect—the psychological bias that makes us overvalue what we already own.

🎓 Educational Note: Concentration Risk

Concentration risk occurs when a portfolio is so heavily weighted toward a single stock, sector, or geographic region that a single negative event can cause disproportionate damage to the total value. While diversification reduces the “unsystematic risk” (risk specific to one company), concentration amplifies it.

Step 1: The Health Check (Balance Sheet & Net Debt)

Before we can even talk about the mouth-watering dividends, we have to ask: can these banks actually pay their bills if the music stops? For a bank, “health” isn’t measured by net debt in the traditional corporate sense (since debt is their raw material), but by their Capital Adequacy Ratio and Solvency. DBS, OCBC, and UOB are currently sitting on “fortress” balance sheets, but the risk isn’t internal—it’s systemic. With the three banks now making up over 52% of the Straits Times Index, the health of your portfolio is now inextricably linked to the health of the Singapore government’s regulatory environment.

🎓 Educational Note: CET1 Ratio

Common Equity Tier 1 (CET1) is a measure of a bank’s core equity capital compared to its total risk-weighted assets. It is the ultimate “emergency fund” that regulators require banks to hold to survive a financial crisis.

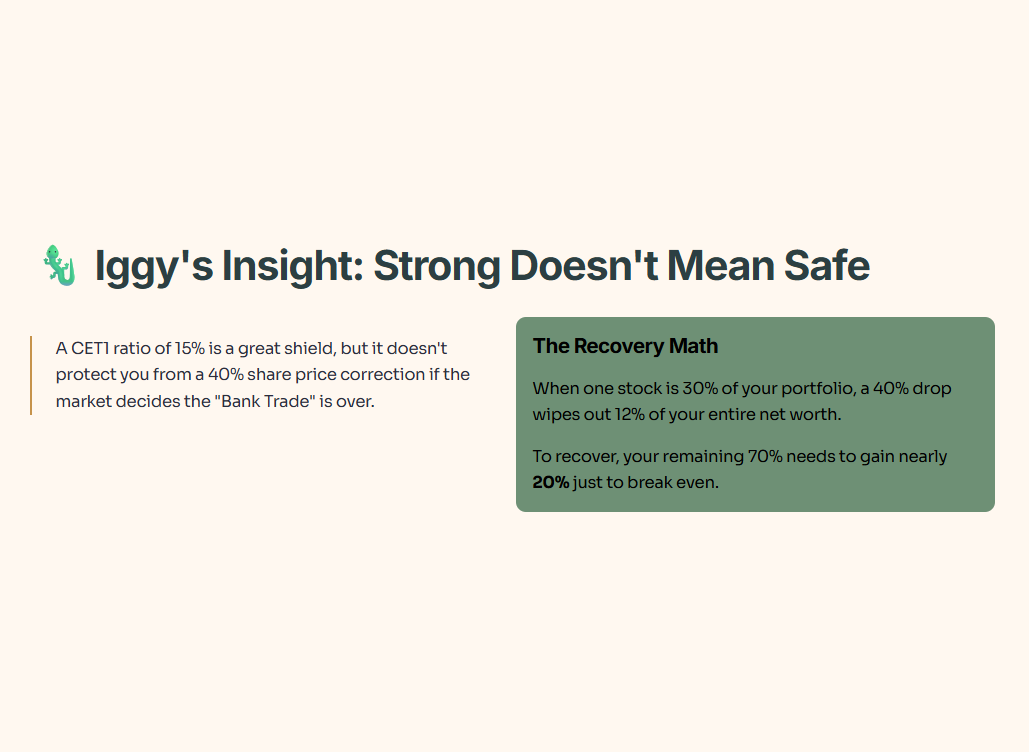

🦎 Iggy’s Insight:

The balance sheets are undeniably strong, but don’t let a “Pass” grade fool you into complacency. A CET1 ratio of 15% is a great shield, but it doesn’t protect you from a 40% share price correction if the market decides the “Bank Trade” is over. When one stock is 30% of your portfolio, a 40% drop wipes out 12% of your entire net worth. To recover that, you’d need your remaining 70% to gain nearly 20% just to get back to zero.

Step 2: The Wealth Check (Dividends & Cash Flow)

The narrative in the coffee shops is simple: “Buy DBS, get 5% yield, retire.” But we need to ask if they are paying us from sustainable earnings or if we are entering a “Refund” phase. Historically, these banks have been incredibly disciplined. However, as net interest margins (NIM) peak and the Fed begins to signal rate cuts in 2026, the “easy money” for bank earnings is drying up. If the payout ratio climbs too high while earnings stagnate, that dividend isn’t a “yield”—it’s a liability.

🎓 Educational Note: Payout Ratio

The Payout Ratio is the percentage of a company’s earnings paid out as dividends to shareholders. A ratio above 60-70% for a bank can be a warning sign that they are not retaining enough capital to grow or to buffer against future loan losses.

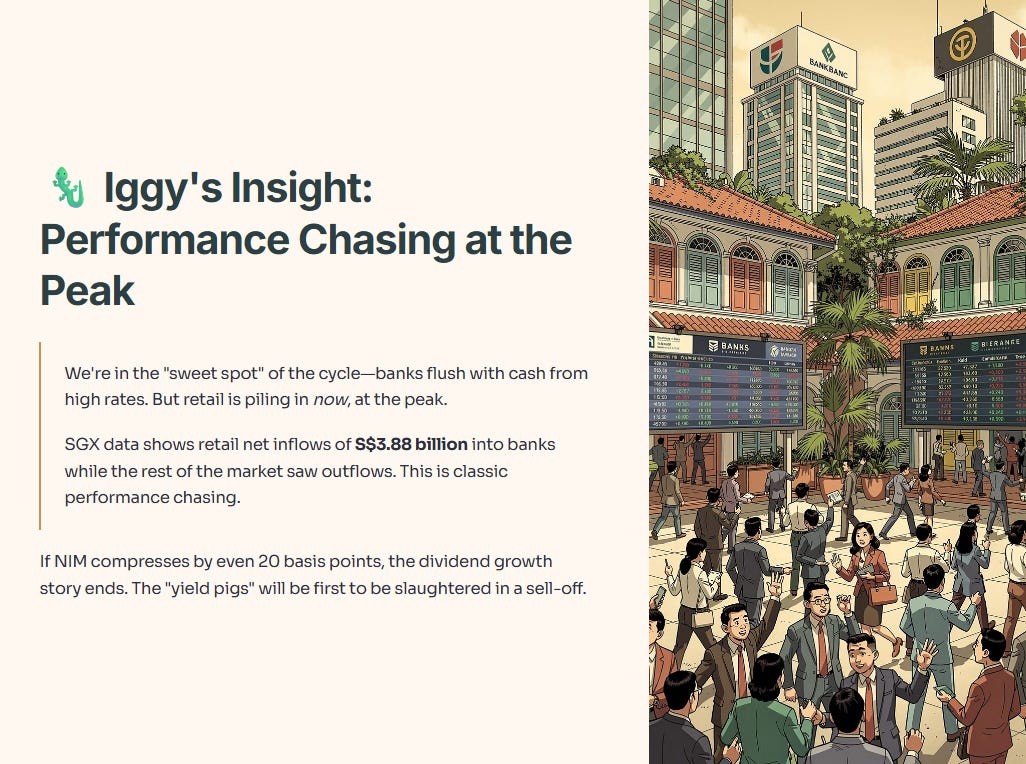

🦎 Iggy’s Insight:

We are currently in the “sweet spot” of the cycle, where banks are flush with cash from high-interest rates. But retail investors are piling in now—at the peak. SGX data shows retail net inflows of S$3.88 billion into banks while the rest of the market saw outflows. This is classic “performance chasing.” You aren’t buying a dividend; you are buying a crowded trade. If NIM compresses by even 20 basis points, the dividend growth story ends, and the “yield pigs” will be the first to be slaughtered in a sell-off.

Step 3: The Price Check (Valuation & Peers)

At a price of S$59.30, DBS isn't just priced for perfection; it's priced for a miracle. We are now staring at a 2.39x Price-to-Book ratio. Let that sink in. We aren't just at the ceiling; we are on the roof. When we compare our local giants to global peers, the “Singapore Premium” becomes obvious. We are paying for the safety of the SGD and the stability of the MAS, but at what point does that premium become a trap?

Next, I’ll show you the exact ‘line in the sand’ I use to decide whether a 30% bank position gets trimmed now—or held—using the same peer/value logic institutions use