Is Coliwoo’s S$288 Million IPO Your Ticket to Singapore’s Co-Living Boom—Or a High-Leverage Trap?

Singapore’s co-living market leader is going public at premium valuations with massive debt. Here’s what the numbers really tell you.

The co-living sector in Singapore has transformed from a niche housing alternative into a S$1.4 billion investment magnet. Coliwoo Holdings, the market leader with 32% share, is now launching its initial public offering on the Singapore Exchange Mainboard. The company offers 80.3 million shares at S$0.60 each, targeting a market capitalization of S$288.5 million when trading begins on November 6, 2025.

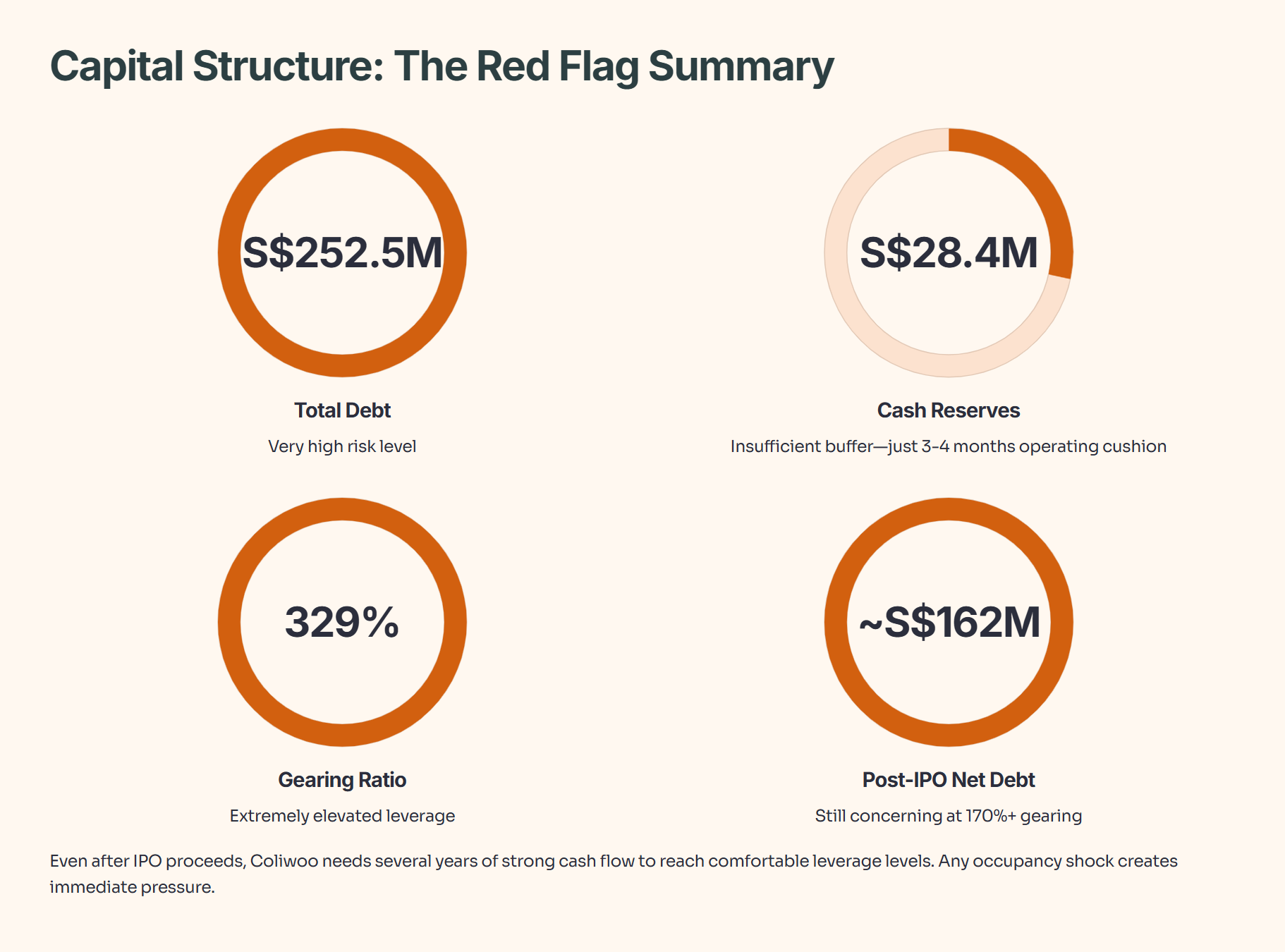

But beneath the impressive growth story lies a financial reality that demands your attention. Coliwoo carries S$252.5 million in debt against just S$28.4 million in cash. The company’s gearing ratio stands at a staggering 329%. This IPO isn’t just about growth—it’s about survival and deleveraging.

Let me walk you through the real numbers, the hidden risks, and whether this IPO deserves your hard-earned money.

In This Article:

• The Growth Story That Caught Everyone’s Attention

• The Debt Mountain That Changes Everything

• The Valuation Puzzle Investors Must Solve

• The Numbers Behind My Investment Decision

• Financial Performance Table

• Valuation Comparison Table

• Capital Structure Red Flags

• Master Lease Model: High Returns or High Risk?

• Competition Intensifies as Market Matures

• Foreign Demand: The Critical Growth Driver

• IPO Structure and Cornerstone Commitment

• The Expansion Plan That Determines Success or Failure

• Realistic Scenarios for Investors

• Bull Case: The Growth Premium Pays Off

• Base Case: Muddling Through With Modest Returns

• Bear Case: The Debt Trap Closes

• Red Flags That Keep Me Up at Night

• The Competitive Moat Question

• My Investment Verdict: Pass or Proceed with Extreme Caution

• The Questions I’m Still Asking

• The Alternative Investment Opportunity

• Final Thought: Great Business, Wrong TimeThe Growth Story That Caught Everyone’s Attention

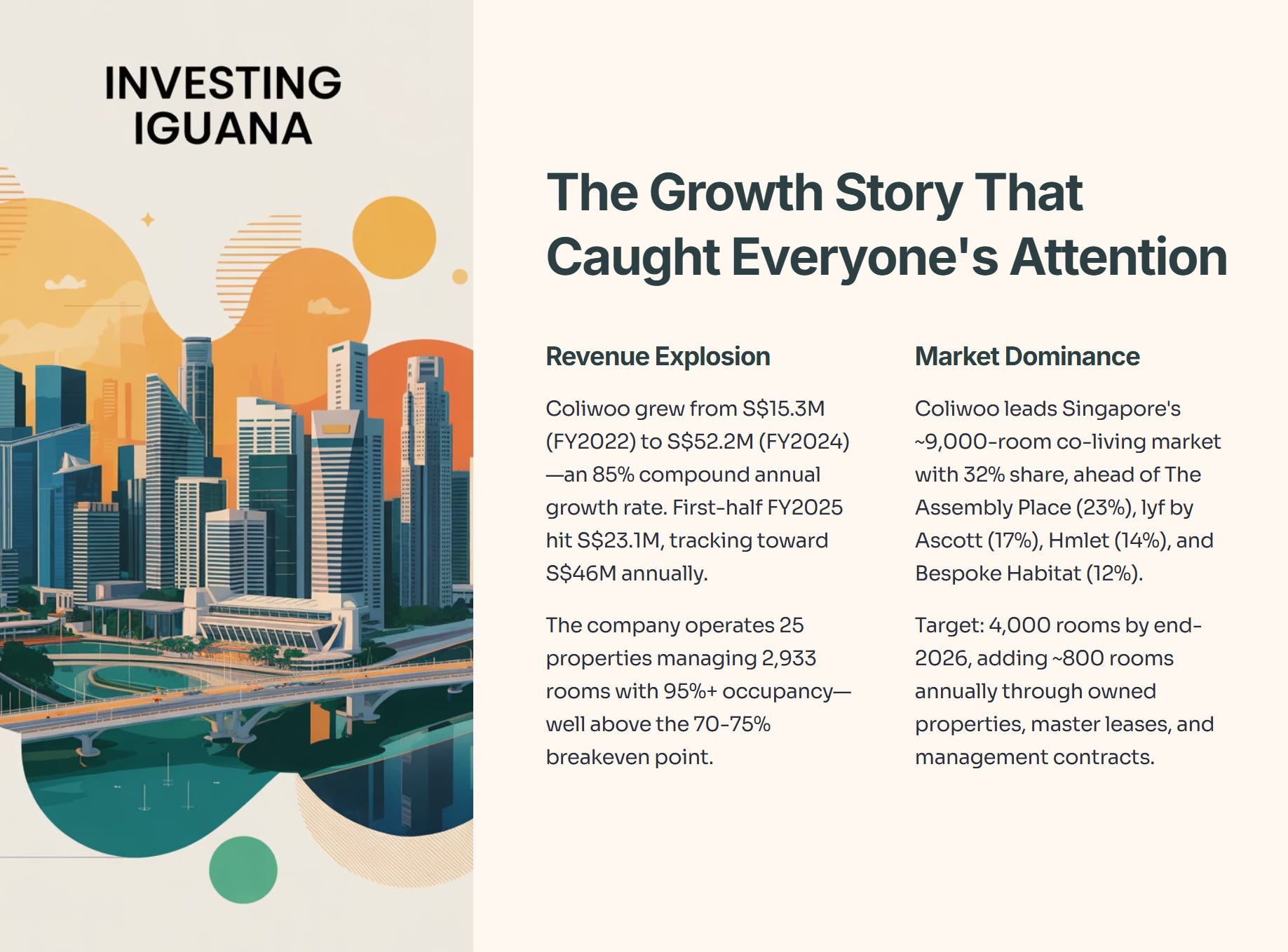

Coliwoo’s revenue trajectory looks stellar on paper. The company grew from S$15.3 million in FY2022 to S$52.2 million in FY2024—a compound annual growth rate of 85%. First-half FY2025 revenue reached S$23.1 million, putting the company on track for approximately S$46 million annually.

The business operates 25 properties across Singapore, managing 2,933 rooms with an average occupancy rate exceeding 95%. This occupancy level sits well above the industry breakeven point of 70-75%. The company dominates Singapore’s co-living market, which contains roughly 9,000 total rooms across 20 active operators.

Coliwoo’s market leadership comes from aggressive expansion. Between 2021 and 2022, parent company LHN Group added six co-living assets during a period of surging rental rates. The strategy paid off—Coliwoo captured the top market position ahead of The Assembly Place (23% share), Bespoke Habitat (12%), and established players like Hmlet (14%) and lyf by Ascott (17%).

The company plans to expand to 4,000 rooms by end-2026, adding approximately 800 rooms annually. This expansion will use a mix of owned properties, master lease agreements, and management contracts. The master lease model has delivered strong margins historically, with co-living operators achieving operating margins between 65% and 85% due to minimal staffing requirements and high occupancy.

The Debt Mountain That Changes Everything

Here’s where the story gets complicated. Coliwoo’s balance sheet reveals S$252.5 million in total debt as of August 2025, against just S$28.4 million in cash reserves. This creates net debt of S$224.1 million—nearly 4.3 times the company’s FY2024 revenue.

The gearing ratio tells an even more concerning story. With shareholders’ equity of just S$76.8 million (total assets of S$408.3 million minus liabilities of S$331.5 million), Coliwoo’s debt-to-equity ratio reaches 329%. Compare this to parent company LHN Group, which operated at 56% leverage as of September 2023.

The IPO aims to raise S$96.2 million in net proceeds, including cornerstone investments. But here’s the problem—only about S$22 million will go toward debt repayment based on the stated use of proceeds. The company plans to allocate approximately S$40 million for property expansion through master leases and another S$34 million for potential joint ventures and acquisitions.

This capital allocation raises a critical question. Why prioritize expansion over deleveraging when your gearing ratio exceeds 300%? The answer likely lies in the economics of the co-living business model. Coliwoo needs to maintain growth momentum to justify its premium IPO valuation. Standing still means losing market share to aggressive competitors like The Assembly Place and Dash Living.

The debt burden creates immediate operational pressure. Assuming a 4% average interest rate, Coliwoo faces roughly S$10.1 million in annual interest expenses. With FY2024 earnings of S$33.9 million, this produces an interest coverage ratio of just 3.4 times—adequate but not comfortable given the expansion plans.

The Valuation Puzzle Investors Must Solve

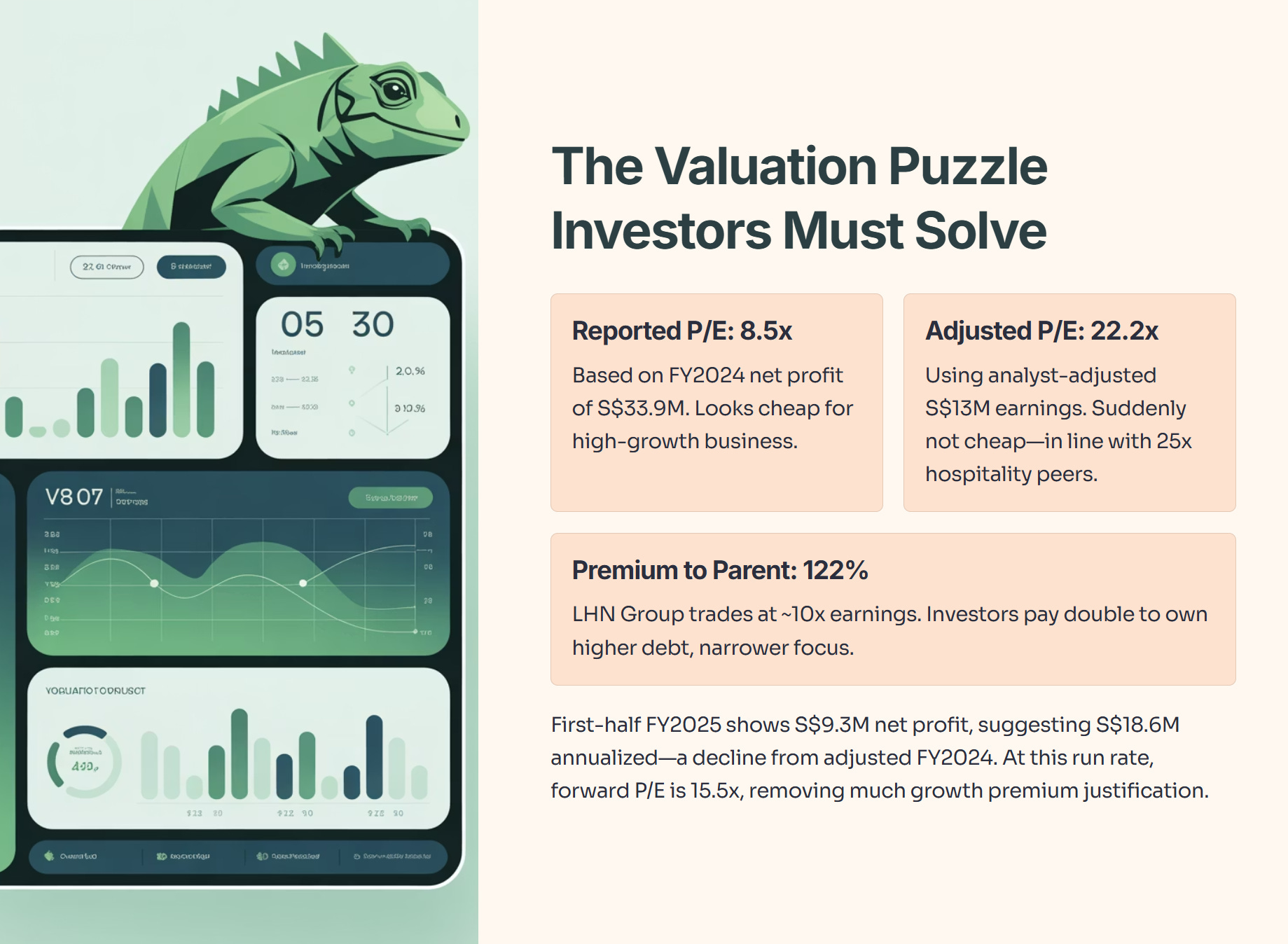

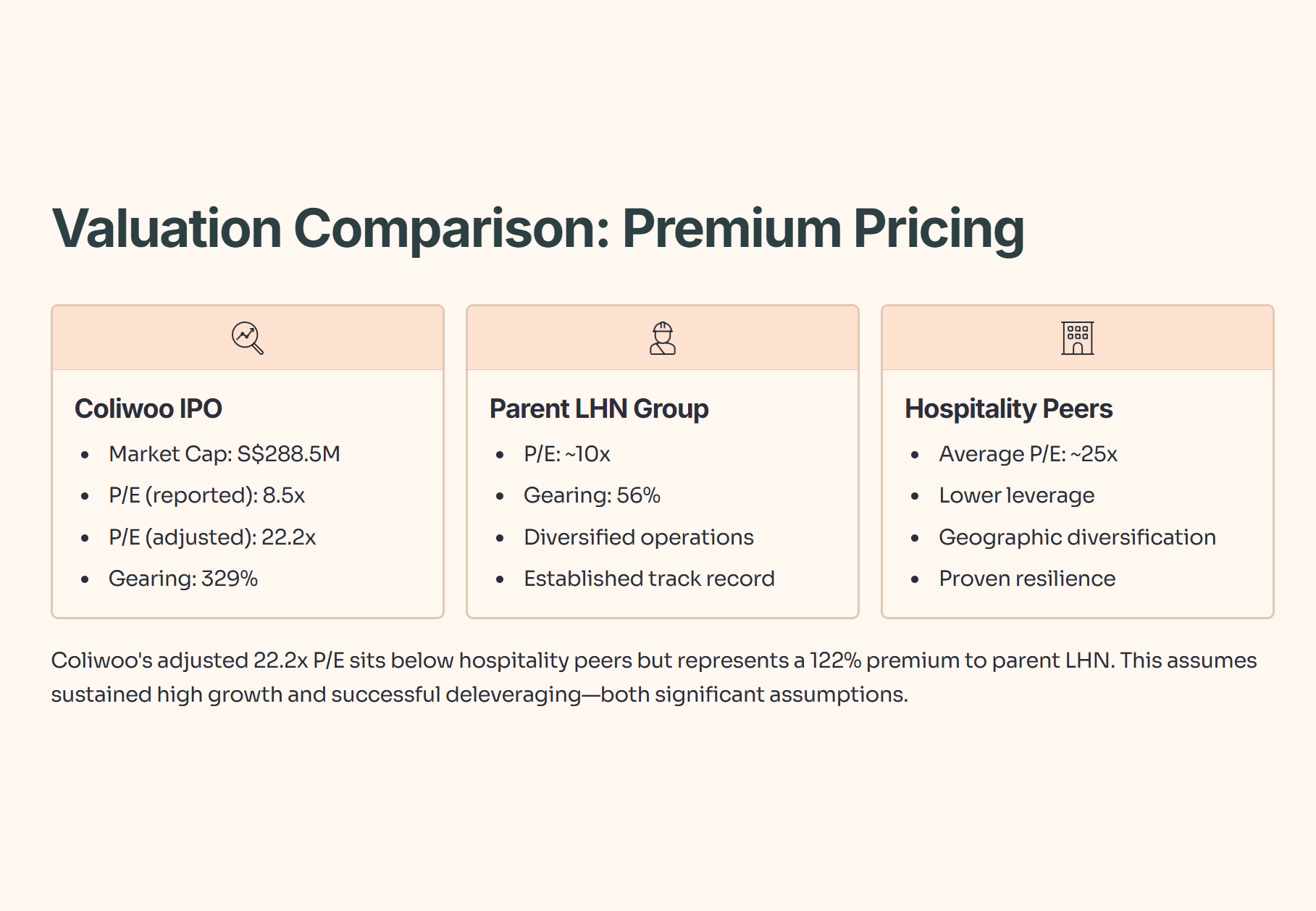

Coliwoo’s IPO pricing at S$0.60 per share creates a market capitalization of S$288.5 million. This valuation becomes problematic when you dig into the earnings numbers.

The company reported FY2024 net profit of S$33.9 million, which produces a price-to-earnings ratio of 8.5 times based on the IPO market cap. That sounds reasonable—even cheap—for a high-growth business. But analyst reports suggest using an “adjusted” FY2024 net profit of S$13 million for valuation purposes. This adjustment likely removes one-time gains or non-recurring items.

Using the adjusted earnings figure, Coliwoo’s P/E ratio jumps to 22.2 times. Suddenly the valuation doesn’t look cheap anymore. Industry research suggests co-living and hospitality peers trade at approximately 25 times P/E. Coliwoo’s valuation sits right in line with established players, despite the company’s early-stage status and elevated financial leverage.

The real comparison point is parent company LHN Group, which trades at roughly 10 times earnings on the Singapore Exchange. Coliwoo’s IPO pricing represents a 122% premium to its parent. Investors are essentially paying more than double LHN’s valuation multiple to own a business with higher debt, narrower geographic focus, and greater exposure to Singapore’s competitive co-living market.

First-half FY2025 results show net profit of S$9.3 million, suggesting annualized earnings around S$18.6 million. This represents a significant decline from FY2024’s adjusted S$13 million figure—not growth. At this run rate, Coliwoo trades at 15.5 times forward earnings, which removes much of the “growth premium” justification.

The Numbers Behind My Investment Decision

Financial Performance Table

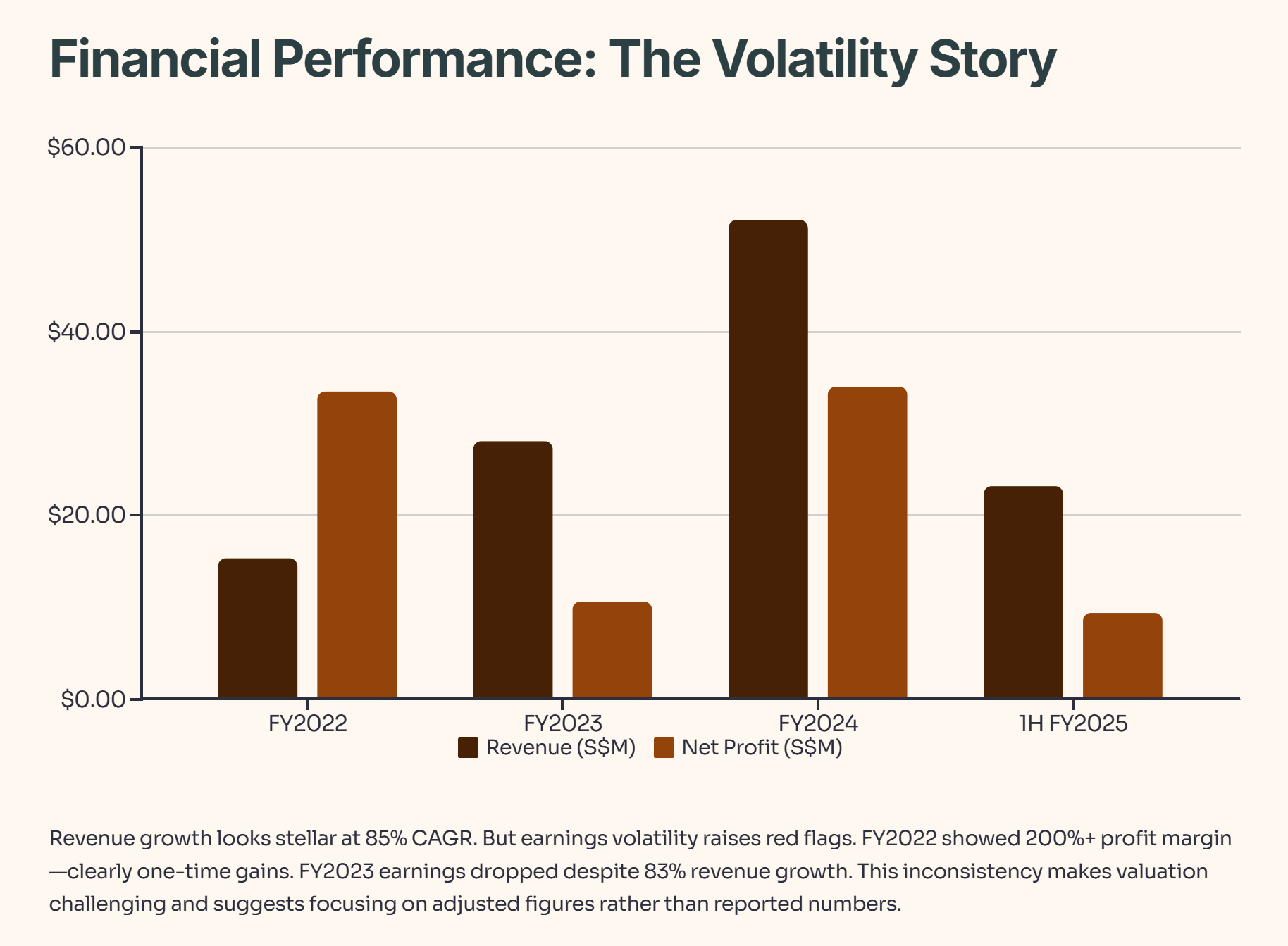

The revenue growth trajectory looks impressive with an 85% compound annual growth rate over three years. But the earnings volatility raises questions. FY2022 showed S$33.5 million in earnings on just S$15.3 million revenue—a profit margin exceeding 200%. This anomaly suggests one-time gains, asset revaluations, or accounting adjustments rather than sustainable operating profits.

FY2023 earnings dropped to S$10.5 million despite 83% revenue growth. FY2024 rebounded to S$33.9 million, then first-half FY2025 came in at S$9.3 million. This earnings inconsistency makes valuation challenging and suggests investors should focus on the adjusted S$13 million figure cited by analysts rather than reported numbers.

Valuation Comparison Table

The adjusted P/E of 22.2 times sits slightly below hospitality peers at 25 times but more than double parent LHN’s valuation. This premium assumes Coliwoo can maintain high growth rates and successfully deleverage—both significant assumptions given market conditions.

Capital Structure Red Flags

The post-IPO debt reduction from S$224 million to approximately S$162 million helps, but gearing remains above 200% even after the offering. The company needs several years of strong cash flow generation to reach comfortable leverage levels.

Master Lease Model: High Returns or High Risk?

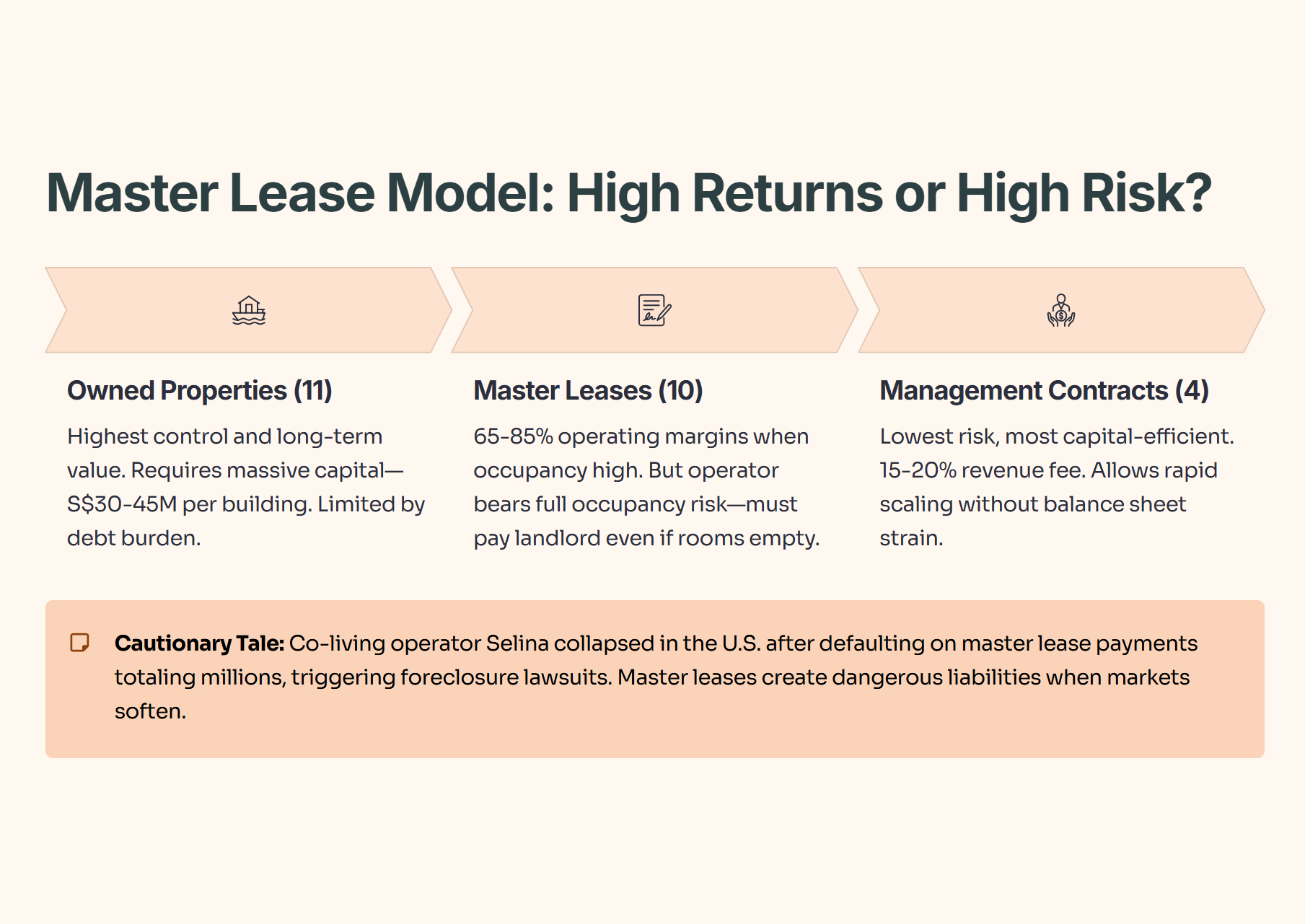

Coliwoo operates through three primary models. The company owns 11 properties outright, leases 10 properties under master lease agreements, and manages 4 properties for third-party owners. Each model carries different risk profiles and capital requirements.

Owned properties provide the highest control and long-term value capture. But they require massive upfront capital. With property prices in Singapore averaging S$30-45 million for suitable co-living buildings, ownership demands either heavy debt or dilutive equity raises. Coliwoo’s existing debt burden limits its ability to pursue additional acquisitions without further straining the balance sheet.

Master leases offer an attractive middle ground. The operator signs long-term lease agreements with property owners, guaranteeing fixed rental payments regardless of occupancy. The operator then sublets individual rooms to tenants, pocketing the spread between lease cost and rental income. This model generates strong returns when occupancy and room rates remain high—which explains the 65-85% operating margins achieved by successful operators.

But master leases create significant downside risk. The operator bears full occupancy risk and must pay the landlord even if rooms sit empty. When markets soften, master lease obligations become dangerous liabilities. Co-living operator Selina’s collapse in the United States provides a cautionary tale—the company defaulted on master lease payments totaling several million dollars, triggering foreclosure lawsuits and property takeovers.

Singapore’s co-living market showed resilience during the pandemic, with occupancy rates remaining between 85-95% market-wide. However, the sector has entered a “maturation phase” following a 17% increase in room supply between 2023 and 2025. Private residential supply surged with nearly 30,000 new units completing in 2022-2023. This supply influx has caused rental growth to stabilize after years of rapid increases.

Management contracts represent the lowest-risk, most capital-efficient model. The operator manages properties for third-party owners in exchange for a management fee, typically 15-20% of revenue. This “asset-light” approach allows rapid scaling without balance sheet strain. Larger co-living operators are increasingly shifting toward management contracts to improve capital efficiency.

Coliwoo manages just 4 properties under this model—far fewer than its 11 owned and 10 leased properties. This suggests the company remains committed to capital-intensive strategies despite the elevated debt levels. The IPO proceeds allocation confirms this, with S$40 million earmarked for additional master leases rather than accelerating the shift to asset-light management.

Competition Intensifies as Market Matures

The Singapore co-living sector has attracted over S$1.4 billion in transaction volume since 2022, signaling institutional recognition of the asset class. Major players include private equity firms, real estate developers, hospitality groups, and family offices.

The Assembly Place holds 23% market share and is aggressively expanding. Bespoke Habitat controls 12% and targets middle-income professionals. Established operators Hmlet (now rebranded as Habyt after a 2022 merger) and Dash Living bring international expertise and capital.

Perhaps most concerning for Coliwoo, hospitality giant Ascott—a CapitaLand subsidiary—operates the lyf brand with 17% market share. Ascott completed the acquisition and conversion of Hotel G into lyf Bugis for S$240 million in August 2024. This demonstrates the capital firepower available to well-funded competitors.

The top five co-living operators control approximately 65% of the market, up slightly from 2023. This concentration suggests the industry is consolidating, with weaker players getting acquired or exiting. Coliwoo’s market leadership provides some protection, but maintaining dominance requires continuous capital investment—exactly what the company’s debt burden constrains.

Competitive dynamics are evolving beyond simple room supply. Operators are differentiating through pricing models, target demographics, and amenity packages. Some brands have moved from all-inclusive pricing to unbundled models that charge separately for utilities and services. Others focus on specific communities like international students, healthcare workers, or young professionals.

Government support has increased with state properties being converted to co-living use and demographic-specific projects receiving backing. This partnership approach helps mitigate investment risk but also signals government recognition of housing shortages—a double-edged sword that validates the business model while attracting more competition.

Foreign Demand: The Critical Growth Driver

Understanding who rents co-living spaces matters enormously for investment analysis. Foreigners comprise 70-90% of co-living tenants in Singapore, primarily from China, Malaysia, and India. The non-resident population represents 30% of Singapore’s total population and grew 5% year-over-year through June 2024, maintaining a five-year compound annual growth rate of 1.1%.

International students represent a significant and growing segment. Singapore’s universities continue attracting foreign enrollment, creating steady demand for flexible, affordable housing near campuses. Government initiatives specifically target student accommodation through converted state properties.

Young professionals on employment passes form another core demographic. About 60% of co-living residents fall under age 35. These individuals often lack the capital or desire for long-term rental commitments. Companies increasingly exclude accommodation from expatriate packages, pushing professionals toward co-living as a cost-effective alternative.

This foreign-heavy tenant base creates both opportunity and vulnerability. Singapore’s economic health directly impacts foreign worker inflows. A regional recession, technology sector downturn, or policy changes restricting foreign employment could rapidly decrease demand. The co-living business model’s dependence on continuous immigration and foreign student enrollment represents a systemic risk that property owners can’t fully control.

IPO Structure and Cornerstone Commitment

The offering comprises 75 million placement shares to institutional and accredited investors, plus 5.3 million public offer shares for retail investors. This structure heavily favors institutions—retail investors can access just 6.6% of the offering.

Nine cornerstone investors committed to 88 million shares at the offering price, representing 18.3% of total shares issued at listing. These cornerstones include Avanda Investment Management, Maybank Asset Management Singapore, UOB Asset Management, Value Partners Hong Kong, and others. The cornerstone participation totals approximately S$52.8 million and demonstrates institutional confidence.

However, cornerstone investors often negotiate lock-up periods shorter than management. After their restriction expires, these large holders may sell, creating downward price pressure. Retail investors should expect elevated volatility once cornerstone lock-ups end.

Maybank Securities serves as issue manager and global coordinator, alongside DBS Bank and RHB Bank as joint bookrunners and underwriters. This top-tier banking support suggests the deal will price and list successfully, but says little about post-IPO performance.

Parent LHN Group retains approximately 65% of Coliwoo after the offering. This controlling stake ensures alignment between parent and subsidiary shareholders. But it also means LHN can block major corporate actions and potentially pursue strategies benefiting the parent at minority shareholders’ expense.

The Expansion Plan That Determines Success or Failure

Coliwoo targets 4,000 rooms by end-2026, up from 2,933 currently—a 36% increase requiring roughly 1,067 additional rooms. At an annual addition rate of 800 rooms, the company needs aggressive execution across multiple properties simultaneously.

The S$40 million allocated for expansion through master leases and property acquisitions provides some context. Assuming average master lease deposits and fit-out costs of S$50,000-100,000 per room, this capital supports 400-800 new rooms. The company will need additional debt or partnership arrangements to hit the 1,067-room target.

Coliwoo plans to pursue regional expansion into “high-potential Southeast Asian markets” including Jakarta, Bangkok, Kuala Lumpur, and Johor Bahru. International expansion adds complexity, regulatory risk, and foreign exchange exposure. These markets have different tenant demographics, regulatory frameworks, and competitive landscapes compared to Singapore’s mature co-living sector.

The regional expansion strategy conflicts with the deleveraging imperative. Each new market requires substantial investment in brand building, property sourcing, regulatory compliance, and operational infrastructure. Spreading capital across five countries while carrying S$250 million in debt creates execution risk that could derail the entire story.

Realistic Scenarios for Investors