Will Parkway Life REIT’s Japan Nursing Homes Break the 18-Year DPU Streak | PLife REIT 1Q | 🦖EP1586

When DPU jumps 15.1% but Japan NPI falls 2.7% and 5 Osaka homes sit vacant

Target Asset: Parkway Life Real Estate Investment Trust (SGX: C2PU) Event: 1Q 2026 Business Update

1. Introduction

Management celebrated a 15.1% spike in DPU this quarter. But they buried the uncomfortable fact that underlying organic revenue actually contracted by 2.1% down to S$38.2 million. If you are relying on this REIT to fund your CPF retirement payouts, you are currently buying into an asset that mathematically fails our absolute minimum yield hurdle. We are going to audit what the presentation slide deck masked behind cross-currency swaps and engineered distribution bumps.

In This Article:

The Slide-by-Slide Audit The Deep Dive

The Reality Check InvestingPro Integration

The Scorecard and Yield Spread

The Forward Outlook

Outro and Disclaimer

Iggy’s Forensic Disclaimer

2. The Slide-by-Slide Audit (The Deep Dive)

When we audit REITs, we lead strictly with Distribution Per Unit (DPU) and Gearing. Parkway Life REIT reported a 1Q 2026 DPU of 4.42 cents. This represents a 15.1% year-on-year growth rate. Management is pointing to their “strong balance sheet” and “uninterrupted DPU growth” as the core narrative.

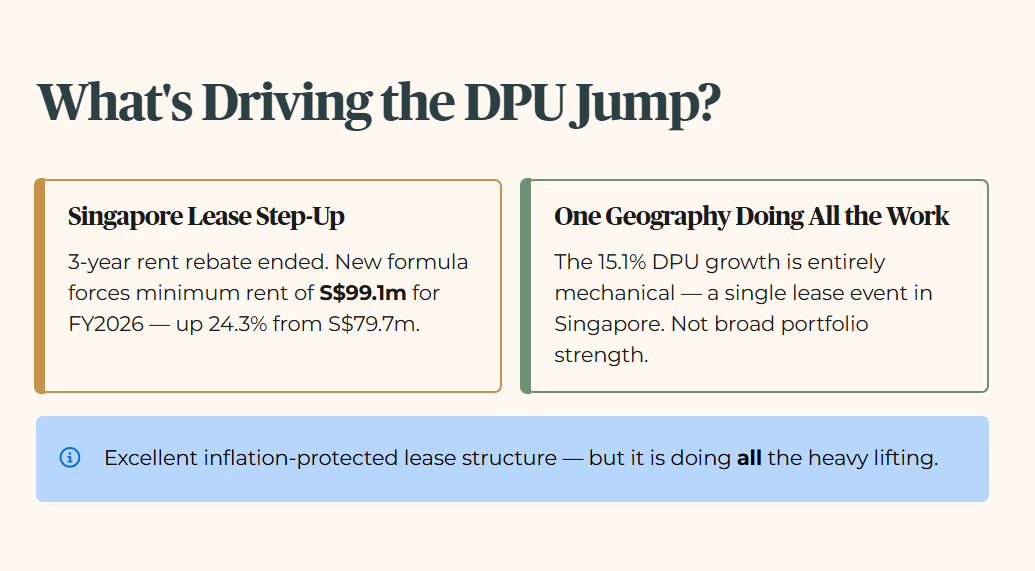

However, we must look at the mechanics driving this payout. The 15.1% DPU growth is not coming from broad portfolio strength. It is entirely engineered by a singular, mechanical lease event in Singapore. The three-year rent rebate program for their Singapore hospitals has ceased. The new annual rent review formula has kicked in. This forces the master lessee to pay a minimum rent of S$99.1 million for FY2026, guaranteeing a 24.3% jump in base cash flow from FY2025’s S$79.7 million. This is an excellent, inflation-protected lease structure — and it is doing all the heavy lifting.

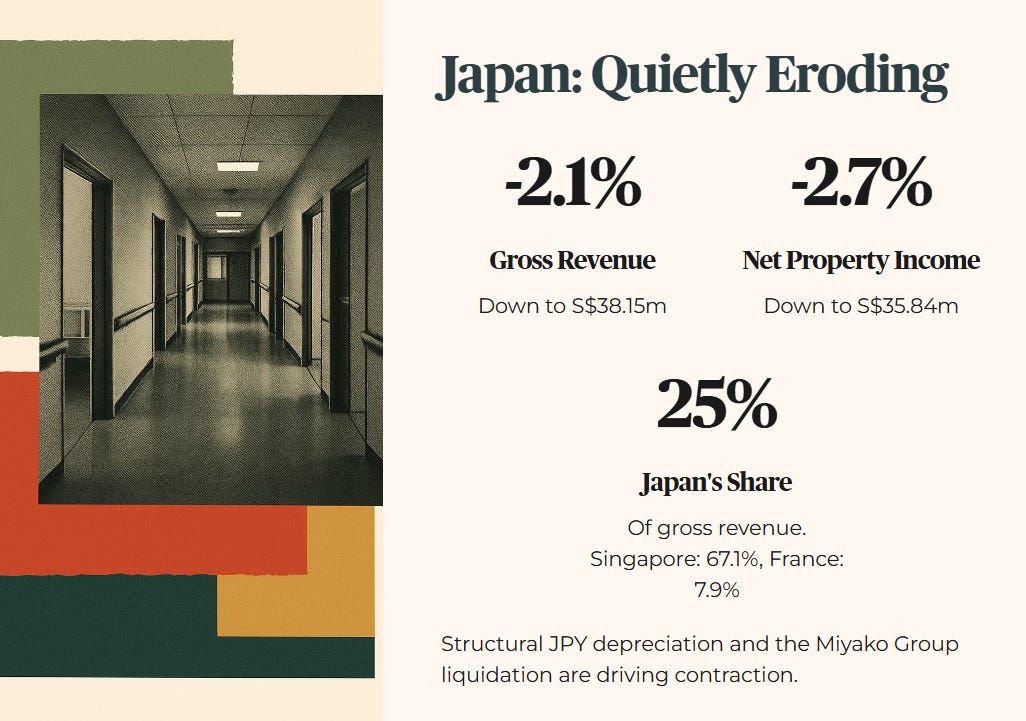

But here is the uncomfortable truth. While Singapore carries the portfolio, the Japan segment is quietly eroding. Gross revenue declined by 2.1% to S$38.15 million. Net Property Income dropped 2.7% to S$35.84 million. Looking at the revenue composition, Japan now contributes only 25.0% of gross revenue, with Singapore at 67.1% and France at 7.9%. This contraction is driven by structural Japanese Yen depreciation and the liquidation of a key Japan portfolio tenant, the Miyako Group, which directly affects five nursing home properties in Osaka, taken back by management in January and February 2026.

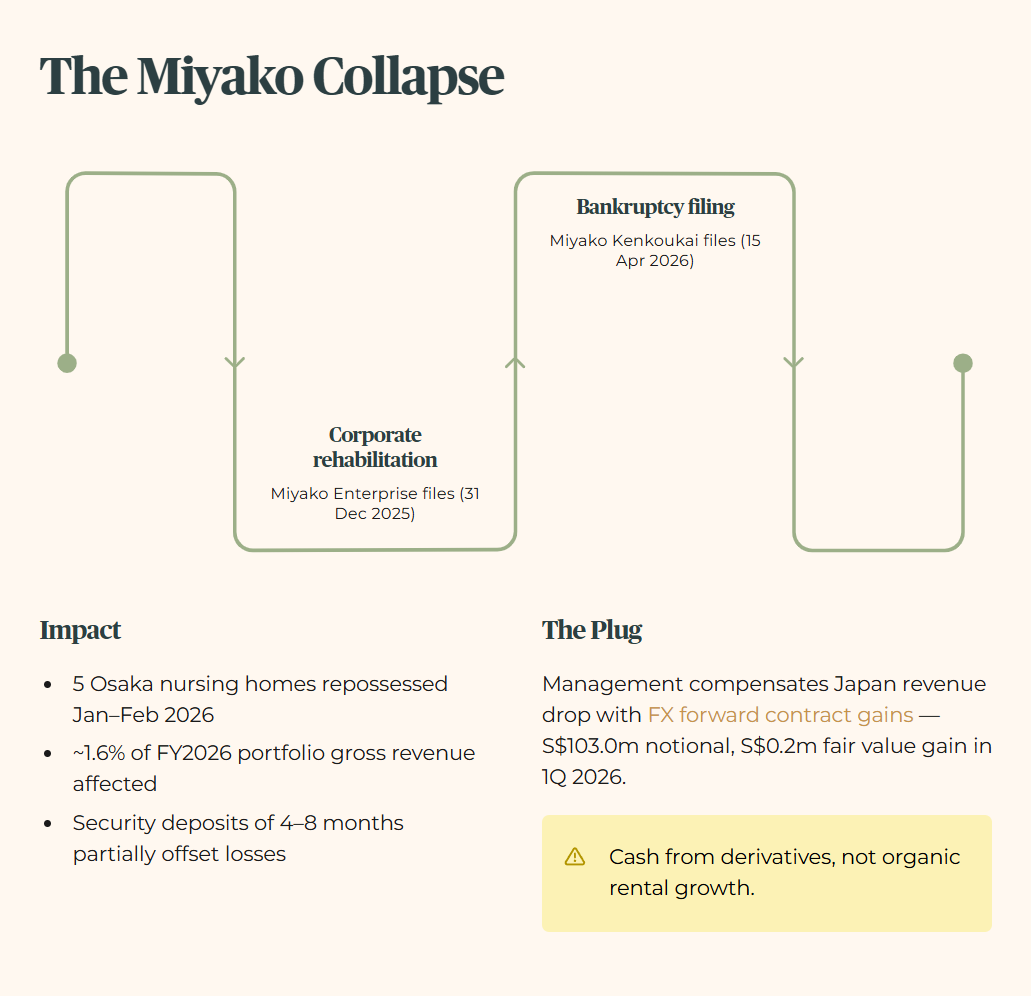

The Miyako situation deserves specific forensic attention. Miyako Enterprise filed for corporate rehabilitation on 31 December 2025. Miyako Kenkoukai subsequently filed for bankruptcy on 15 April 2026. Management states that the rental income from these five properties represents approximately 1.6% of FY2026 portfolio gross revenue, and that security deposits of four to eight months are largely sufficient to offset outstanding rental obligations. Leasing discussions for the repossessed properties are ongoing.

Management explicitly states that the drop in Japan revenue will be compensated by FX gains from the settlement of forward contracts. The REIT holds outstanding forward exchange contracts with aggregate notional amounts of approximately S$103.0 million, generating a fair value gain of S$0.2 million in 1Q 2026. They are generating cash from financial derivatives, not organic property rental growth. The raw, organic rental revenue of the Japan portfolio is actively contracting in Singapore Dollar terms.

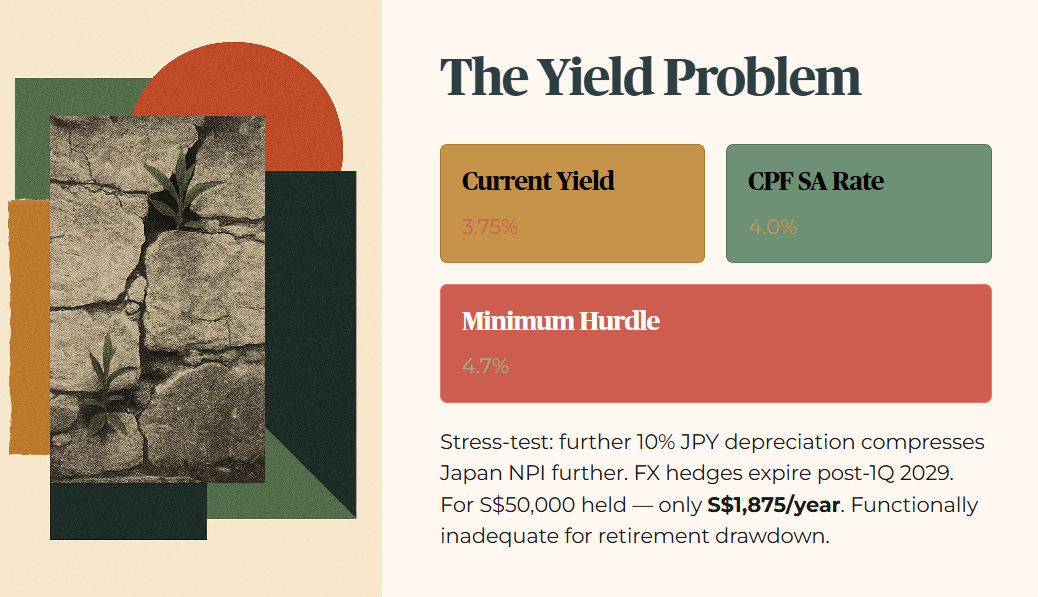

Let us apply the Five-Layer Audit to the most critical breach in this report. The current dividend yield stands at 3.75%. Historically, this REIT has delivered a 3-year average yield of approximately 4.10%. Compare this against a direct SGX peer like First REIT, which sits on an optical yield of 8.40%. While First REIT is a definitive yield trap failing multiple safety metrics, Parkway Life’s yield represents the opposite extreme. If we stress-test a further 10% depreciation in the Japanese Yen over the next 12 months, the organic net property income from the Japan portfolio will compress further. Management will be forced to rely entirely on finite forward contracts — hedged only until 1Q 2029 for JPY income — to maintain this 3.75% payout level. For a 55-year-old heartlander holding S$50,000 in this counter, this translates to roughly S$1,875 a year in distributions. This falls critically short of our absolute minimum yield requirement for sustainable retirement funding. The yield is functionally inadequate for the drawdown phase.

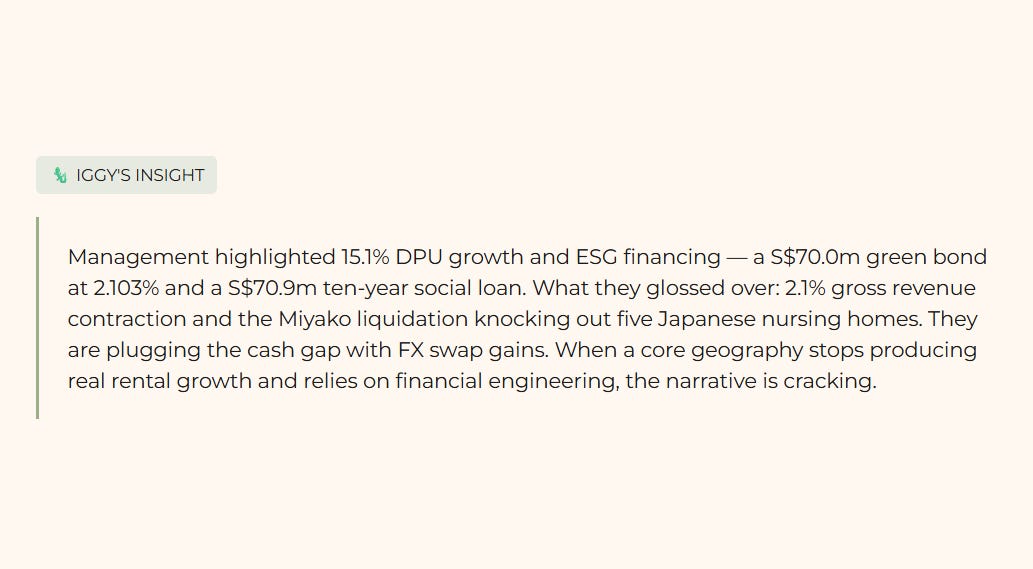

🦎 Iggy’s Insight Block 1 Management spent considerable time highlighting the 15.1% DPU growth and their new ESG financing frameworks — a S$70.0 million green bond at 2.103% and a S$70.9 million ten-year social loan. What they glossed over was the 2.1% contraction in gross revenue, dragging it down to S$38.2 million.

The silence around the Miyako Group liquidation, which knocked out rental income from five Japanese nursing homes, is deafening. They are plugging the cash gap with FX swap gains and pointing to the Singapore hospital rent step-up to mask the organic decay in Japan. When a core geography stops producing real rental growth and relies on financial engineering to maintain distributions, the narrative is cracking. That is the reality.

3. The Reality Check (InvestingPro Integration)

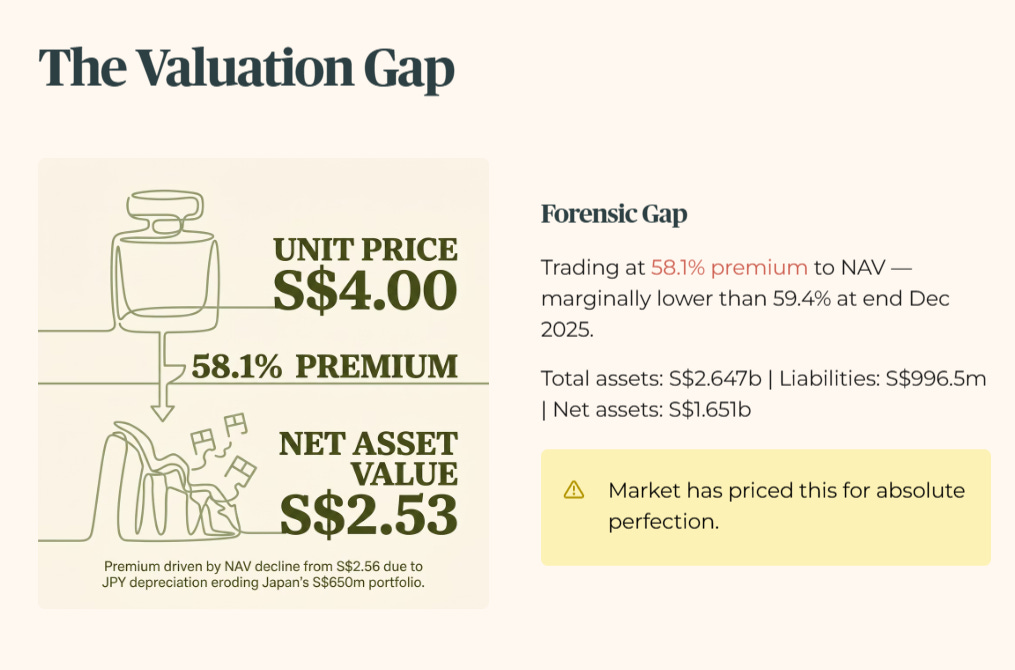

We must always contrast the management narrative with the cold mathematics of valuation. Currently, Parkway Life REIT is trading at a unit price of S$4.00. The stated Net Asset Value per unit is S$2.53, down from S$2.56 at end December 2025. The decline itself is telling — the JPY depreciation is already eroding the book value of Japan’s S$650.0 million portfolio in Singapore Dollar terms.

This creates a significant Forensic Gap. The stock is trading at a 58.1% premium to its Net Asset Value, marginally lower than the 59.4% premium recorded at end December 2025 but still at an extreme level. Total assets stand at S$2.647 billion against total liabilities of S$996.5 million, leaving net assets of S$1.651 billion. Management points to an uninterrupted 18-year streak of DPU growth — 141.9% total growth since IPO in 2007 — to justify this premium. The market has effectively priced this asset for absolute perfection, assuming the Singapore hospital leases will perpetually insulate the portfolio from any external shocks.

Let us use some Kopitiam Logic here. Imagine your favourite chicken rice stall. The actual ingredients, the plate, and the stall space have a tangible book value of S$2.50. But because the uncle has never missed a day of work in 18 years, there is a massive queue, and people are willing to pay S$4.00 for that exact same S$2.50 plate. You are paying a premium for reliability. But if the uncle’s supplier suddenly raises chicken prices — or in this case, if the Japanese Yen collapses and Japanese nursing home operators go bankrupt — that S$4.00 price tag offers you absolutely zero margin of safety.

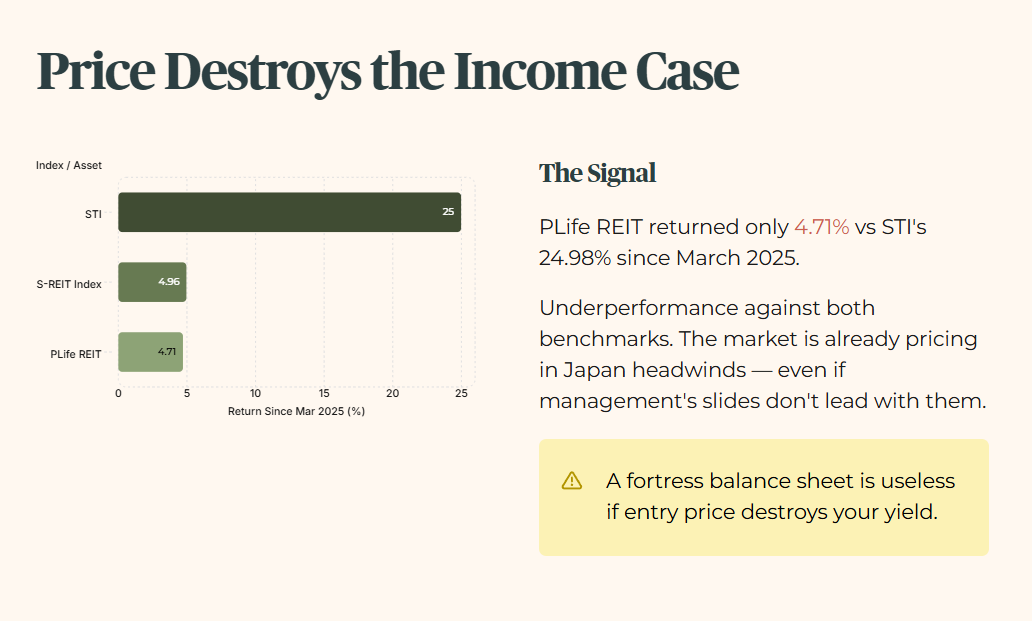

Because you are paying a 58.1% premium to the underlying assets, your forward yield is completely crushed. A fortress balance sheet is useless for retirement income if the entry price mathematically destroys your ability to generate meaningful distributions. The institutional money knows this. Unit price performance since March 2025 shows PLife REIT returning only 4.71%, against the STI’s 24.98% and the S-REIT Index’s 4.96% over the same period. The underperformance against both benchmarks signals that the market is already pricing in the Japan portfolio headwinds, even if management’s slide deck does not lead with them.

4. The Scorecard and Yield Spread

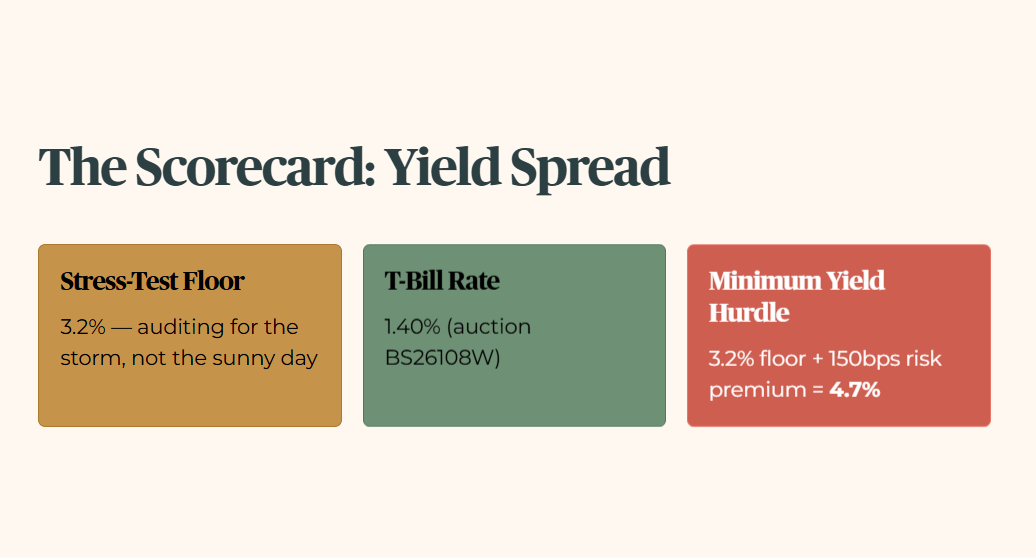

Note on the Stress-Test Buffer: For this audit, I apply a conservative floor of 3.2%. We audit for the storm, not just the sunny day. The latest confirmed T-Bill rate is 1.40% from auction BS26108W. I do not lower my standards to match a temporary market dip. My floor remains at 3.2% to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7% — that is the 3.2% floor plus 150 basis points of mandatory risk premium.

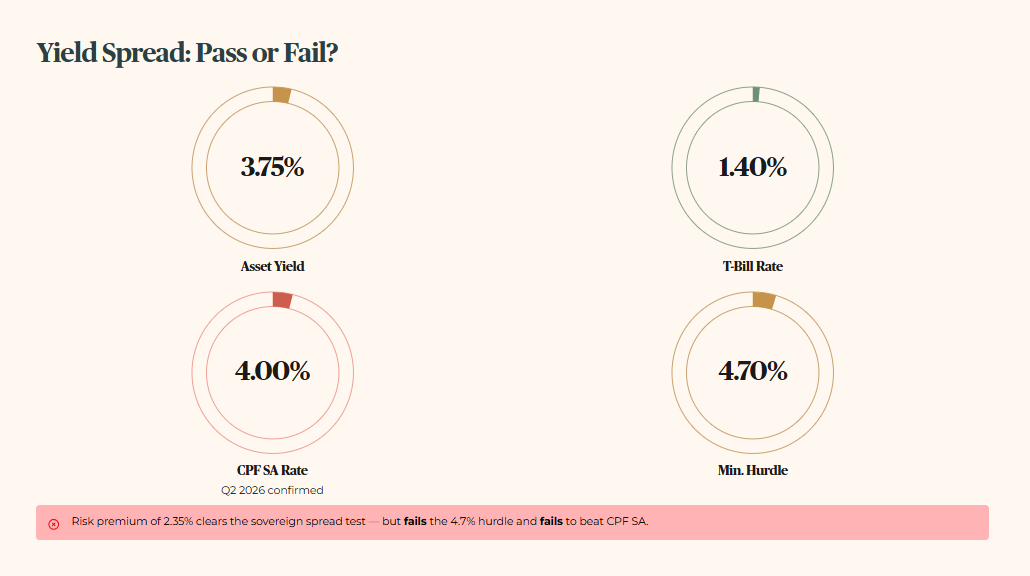

The current asset yield is 3.75%. When we subtract the T-Bill rate of 1.40%, the risk premium on offer is 2.35 percentage points above the sovereign curve. This asset mathematically clears the risk-free spread test against the sovereign curve. However, it completely fails the Minimum Yield Hurdle of 4.7%. Note also that the CPF Special Account currently pays 4.0% — confirmed for Q2 2026. Parkway Life REIT’s yield of 3.75% does not even clear the risk-free CPF SA rate. For a heartlander in the drawdown phase, this is the single most important number on the page.

The cliff-edge question is whether Parkway Life’s 3.75% yield can still survive once we layer your full Income Sustainability table over the refinancing wall and Japan’s vacancy drag — and that is exactly what we quantify next.