Is Your Portfolio Paying You More? These 3+ SG Stocks Just Doubled Their Dividends

This isn't just a one-time bump. We dive into the fundamentals to separate the sustainable income powerhouses from the market flukes, revealing what drove their explosive growth.

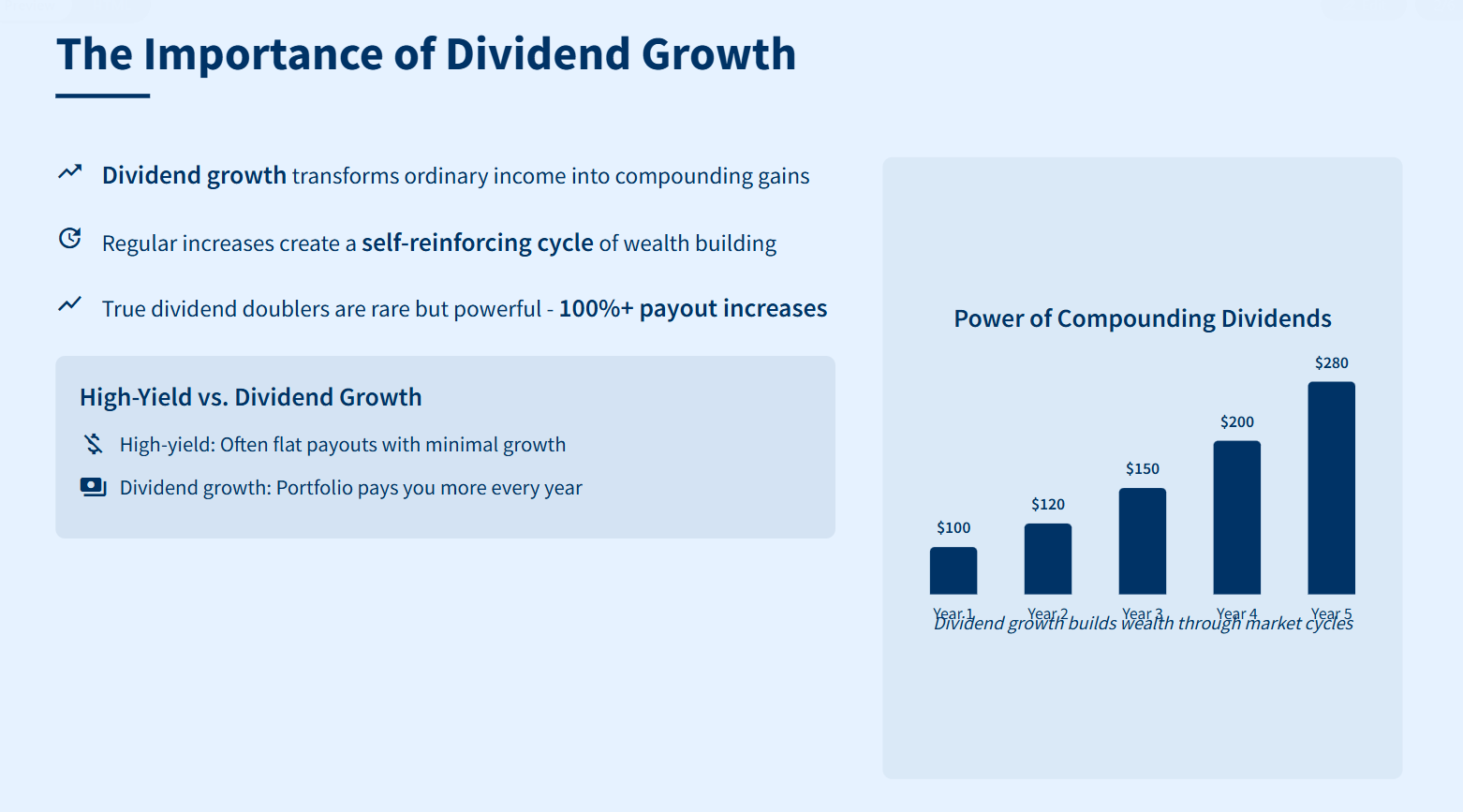

Chasing yield feels safe—after all, steady dividends are a comfort for any investor. But real wealth builds when those payouts grow year after year. Dividend growth is the engine that transforms ordinary income into compounding gains.

In Singapore, most blue-chip stocks reward shareholders with regular increases, but true dividend doublers—stocks that boost payouts by 100% or more—are rare. This year, one retailer shocked the market with a 1,200% surge in dividends, showing what’s possible when special asset sales or profit windfalls hit. At the same time, a handful of companies powered by strong profits delivered double-digit and even triple-digit dividend growth.

Why does this matter? If you rely only on high-yield stocks, you might get stuck with flat payouts and minimal growth. But if you find companies that can grow their dividends for years, you’ll build a portfolio that pays you more every year—no matter how markets swing.

This article spotlights Singapore stocks with real payout momentum. We break down what fueled their explosive growth and separate one-off windfalls from sustainable, long-term dividend engines. Let’s uncover which dividend payers are worth chasing—and which ones are best left as a one-time surprise.

In This Article:

• Finding the Real Dividend Doublers

• The One-Time Giant: DFI Retail Group

• Iggy’s Take: DFI Retail Group

• Sustainable Engine: iFAST Corporation

• Iggy’s Take: iFAST Corporation

• Property Rebound: PropNex

• Iggy’s Take: PropNex

• Telco Turnaround: Singtel

• Iggy’s Take: Singtel

• Banking Giants

• Iggy’s Take: DBS, UOB, OCBC

• Industrial and Defence: Steady Growers

• Iggy’s Take: Industrial & Defence

• Exchange and Other Sectors

• Iggy’s Take: Exchange & Other Sectors

• Key Risks

• Conclusion & RecommendationsFinding the Real Dividend Doublers

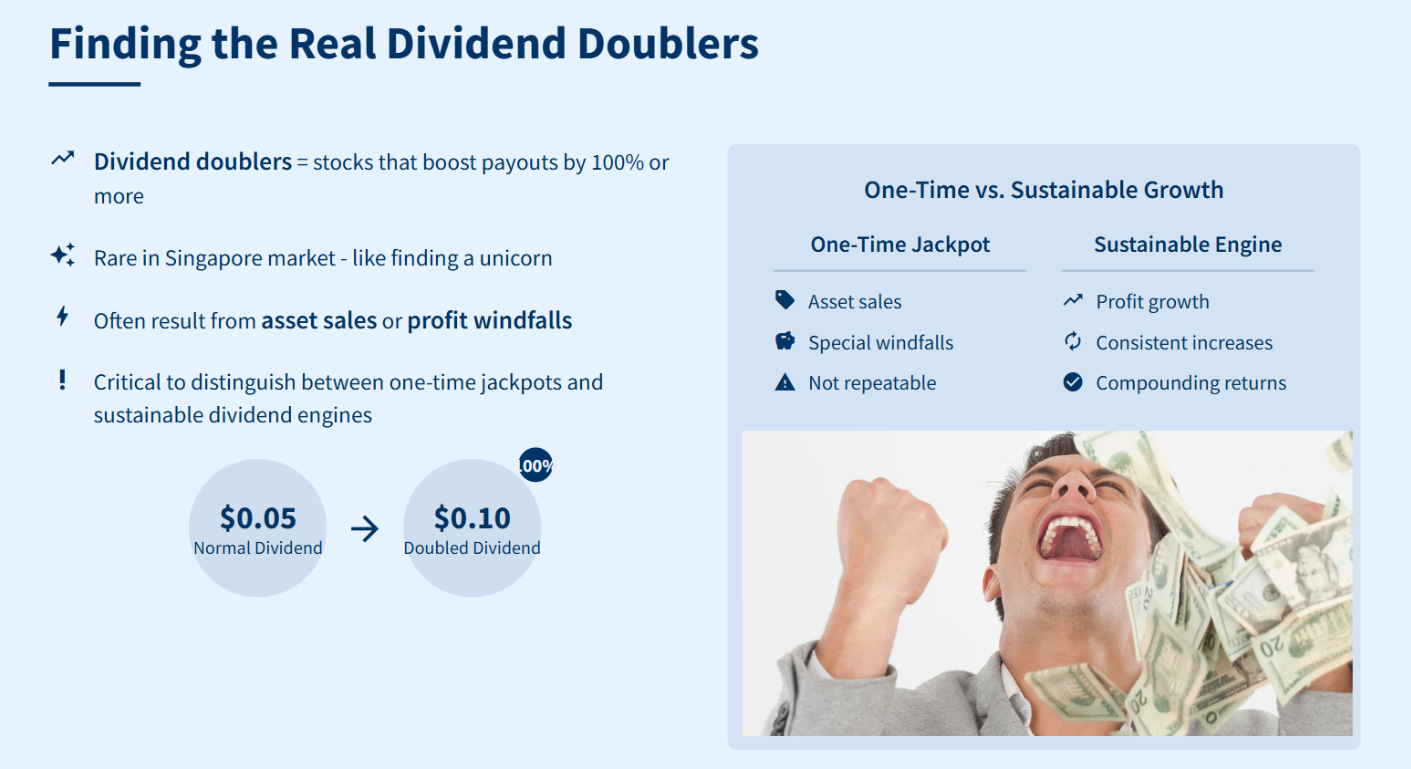

Most Singapore blue-chips raise payouts by low double digits each year—think small bumps you can count on. But true dividend doublers, where payouts jump by 100% or more, are almost mythical. It’s like finding a unicorn in the stock market—a rare sight, unless special circumstances line up.

Often, these explosive payout bursts happen when a company makes a big asset sale, receives a one-off windfall, or enjoys a sudden surge in profits. Shareholders can celebrate a fat dividend, but these moments don’t come around often. If you’re building a portfolio that pays you more every year, the challenge is to spot the difference between a one-time jackpot and a steady dividend engine.

Knowing which companies are likely to keep growing their payouts year after year—versus those handing out special gifts—is key. That understanding helps turn regular investments into compounding returns you can rely on, through up markets and down.

The One-Time Giant: DFI Retail Group

DFI Retail Group tops the list with an eye-popping 1,265% dividend increase in FY2025. The company declared its first special dividend in 18 years: US$0.443 alongside a regular US$0.035 interim payout, for US$0.478 per share total.

This extraordinary jump stemmed from portfolio simplification moves. DFI sold its stakes in Yonghui Superstores and Robinsons Retail for about US$900 million, then divested its Singapore food arm for US$93 million. These transactions transformed DFI’s balance sheet from net debt to net cash of US$442 million. Meanwhile, underlying profit rose 38.9% to US$105 million in H1 2025, driven by 4% like-for-like growth in its Health & Beauty segment and improved Food margins. Management now guides full-year underlying profit to US$250–270 million.

Table 1: DFI Retail’s Dividend Transformation

This table illustrates how strategic asset sales enabled DFI to return a massive one-time dividend beyond its regular interim payout. Future growth will hinge on ordinary dividends once the one-off proceeds are spent.

Iggy’s Take: DFI Retail Group

DFI’s monster dividend this year is like hitting the jackpot at the casino—exciting, but not something you can count on every trip. The surge came from selling big assets, not regular business growth. Once those extra funds are used up, dividends likely go back to normal.

For long-term income, skip DFI if you want steady, growing payouts. Hold only if you’re after a one-time windfall. Treat this year’s dividend like a durian season—delicious while it lasts, but don’t expect it every year.

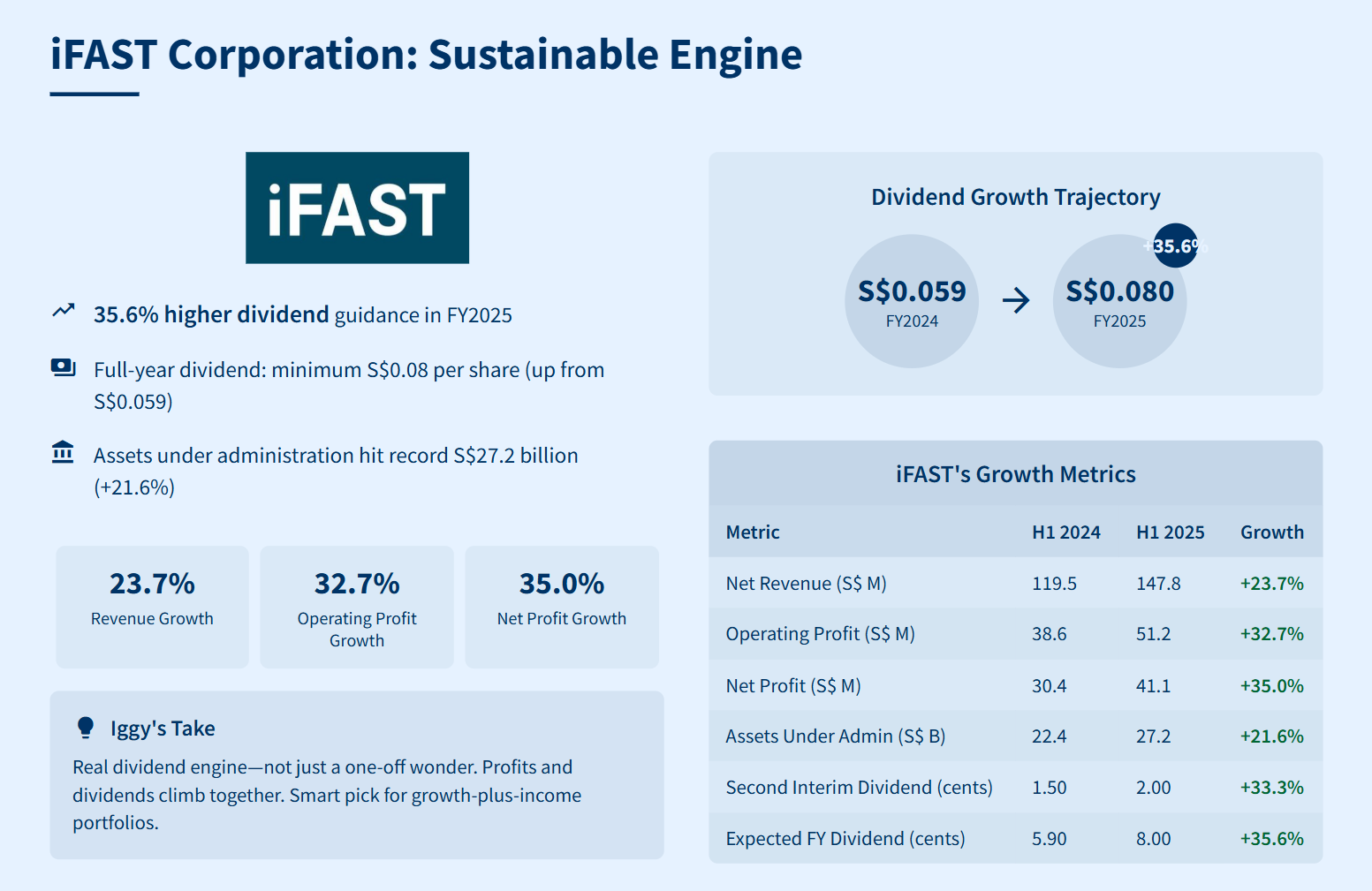

Sustainable Engine: iFAST Corporation

iFAST leads organic dividend growth, guiding shareholders to at least 35.6% higher payouts in FY2025. Its full-year dividend is set at a minimum of S$0.08 per share, up from S$0.059 in FY2024. The second interim dividend alone rose 33.3% to 2.0 cents.

Behind the scenes, H1 2025 results reveal robust expansion: revenue climbed 23.7% to S$147.8 million, operating profit surged 32.7% to S$51.2 million, and net profit jumped 35% to S$41.1 million. Assets under administration hit a record S$27.2 billion, up 21.6%, and the digital bank now holds S$1.5 billion in deposits while serving over 1 million accounts.

Table 2: iFAST’s Growth Metrics

The direct link between iFAST’s profit and dividend growth highlights its shift from pure reinvestment to balanced shareholder returns, making it a prime pick for growth-plus-income portfolios.

Iggy’s Take: iFAST Corporation

iFAST stands out as a real dividend engine—not just a one-off wonder. The company’s profits and dividends keep climbing together, like adding more fuel to a growing fire. Management guides for at least 35% higher payouts this year, backed by strong profits and record assets.

For investors who want both growth and income, iFAST is a smart pick. This is the kind of stock that can turn regular payouts into a solid compounding machine, year after year. If you’re building a portfolio for steady income growth, iFAST deserves a spot near the top of your list.

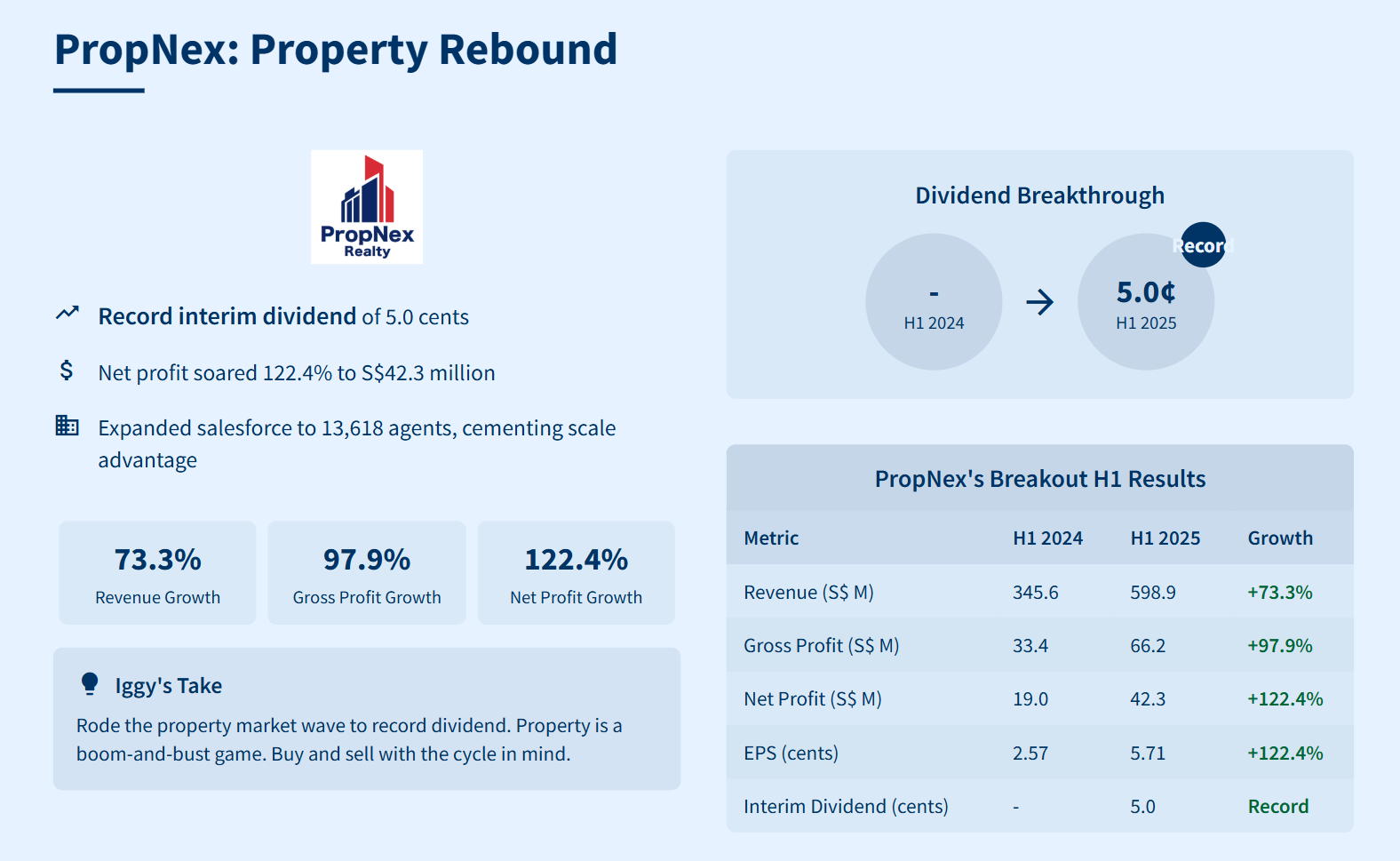

Property Rebound: PropNex

PropNex’s profit boom translated into a record interim dividend of 5.0 cents, its highest ever. H1 2025 net profit soared 122.4% to S$42.3 million, while revenue leapt 73.3% to S$598.9 million and gross profit nearly doubled to S$66.2 million. Earnings per share climbed from 2.57 cents to 5.71 cents as the property market recovery drove transaction volumes. PropNex also expanded its salesforce to 13,618 agents, cementing its scale advantage.

Table 3: PropNex’s Breakout H1 Results

PropNex’s dividends mirror its profit surge from Singapore’s property upswing. Investors should time entries and exits around market cycles.

Iggy’s Take: PropNex

PropNex rode the property market wave to a record dividend—a huge boost fueled by a strong recovery and bigger deal volumes. This year’s payouts are sky-high, but remember, property is a boom-and-bust game. The numbers look great when the market is hot, but future dividends will rise or fall with transaction cycles.

If you want a shot at big payouts, PropNex is worth watching when the market is roaring. But for steady, compounding income, be careful—this stock depends on Singapore’s property swings. Buy and sell with the cycle in mind; don’t expect every year to be a jackpot.

Telco Turnaround: Singtel

Singtel posted a 13.3% dividend increase after years of slow payout growth. This jump was thanks to better results from its partner companies and tighter day-to-day operations, which made the business run smoother and more profitably. That’s a good sign—the company found ways to make more money across its network.

However, it’s important to look at the bigger picture. Singtel does not have a long history of raising dividends year after year. Unlike some “dividend engines” that grow their payouts every year, Singtel’s track record has been patchy. This year’s increase might be a one-off—not the start of a reliable, long-term dividend growth story.

Think of it like a food stall that suddenly improves its dishes for a season—you’ll enjoy the boost right now, but there’s no promise the quality will always keep getting better. So if you’re looking for a stock that grows your income steadily year after year, Singtel may not be your best pick. This jump is worth celebrating, but only for investors who are comfortable with ups and downs.

Iggy’s Take: Singtel

Singtel’s bump looks promising, but reliability is still a question mark. For tactical investors, short-term exposure makes sense when results improve. But if you’re seeking stable, rising payouts for years, Singtel may still be a sketchy pick. Treat it like a pop-up stall—good for a quick bite, but not a long-term staple in your dividend portfolio.

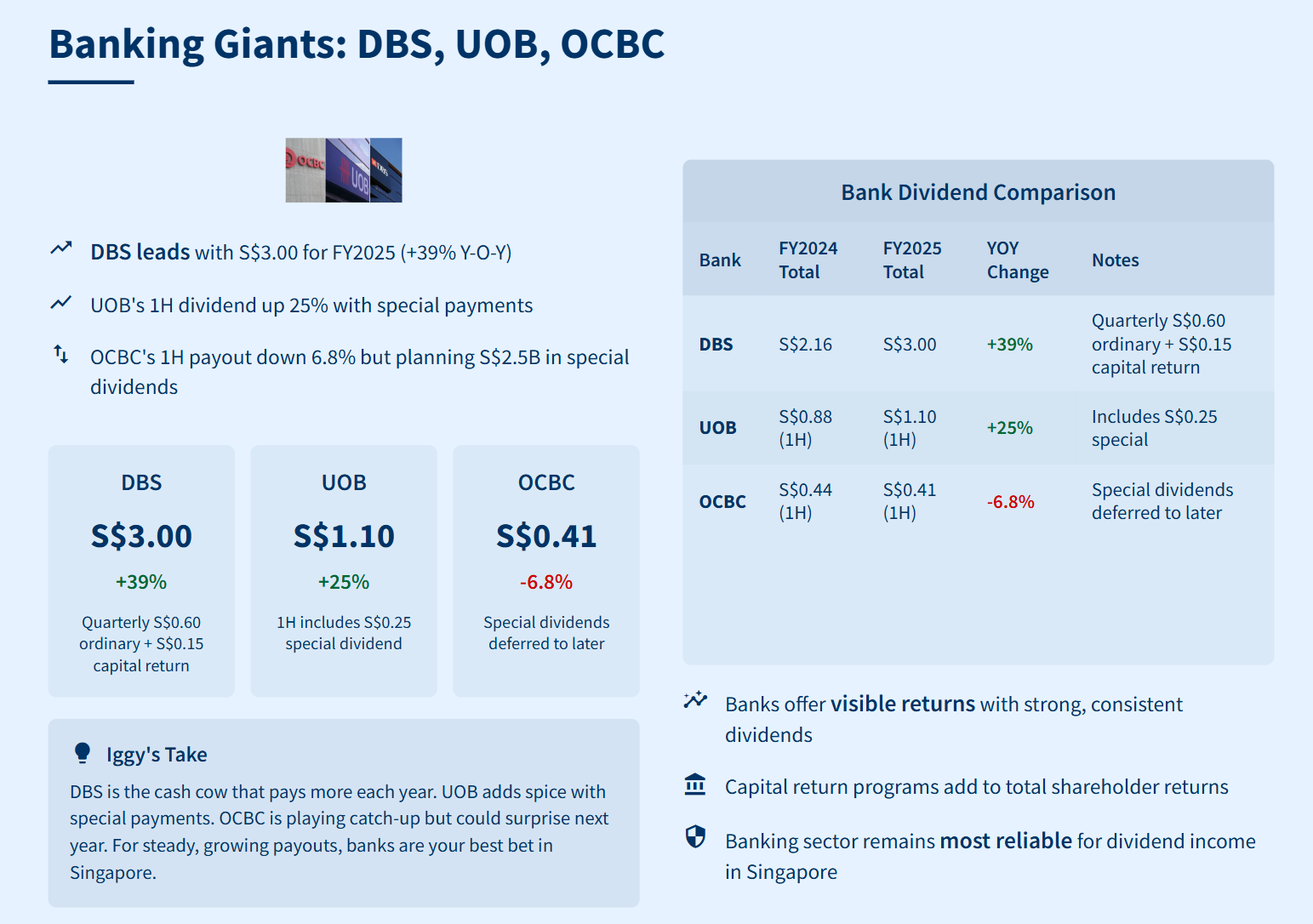

Banking Giants

DBS is setting the pace for Singapore banking dividends, handing out S$0.75 every quarter—split into S$0.60 as the regular payout and S$0.15 as a capital return. If you add it up, that’s S$3.00 for FY2025, way ahead of last year’s S$2.22. The ordinary dividend alone grew by 11% year-on-year, showing that DBS isn’t just returning cash; it’s also building on its profitability. The extra capital return acts like a festival bonus—an added reward for loyal shareholders.

UOB isn’t sitting still either. In the first half of 2025, UOB’s shareholders received S$1.10—a blend of S$0.85 regular payout and S$0.25 special dividend. That’s a 25% boost, fueled by stronger performance across its banking business. UOB’s approach mixes dependable payouts with the occasional surprise, keeping things dynamic for income-focused investors.

OCBC had a slightly different story. Its first half payout dipped 6.8% to 41 cents—a modest step down. But don’t count OCBC out. The bank’s management is planning S$2.5 billion in special dividends and buybacks over the next two years. These moves can act as a powerful catalyst for future returns, compensating for any short-term slowdown.

Bottom line:

DBS leads with predictable, growing payouts baked in.

UOB offers steady income with a dash of extra.

OCBC may have tripped in the short term, but it has a plan to reward shareholders going forward.

For investors seeking compounding income, banks like DBS should be a core holding. If you want a little more excitement, add UOB for its bonus payouts. OCBC may be for the patient investor who’s willing to wait for its buyback and special dividend play to kick in.

Table 4: Bank Dividend Comparison

This table clarifies each bank’s dividend framework, highlighting DBS’s leadership in total shareholder returns.

Iggy’s Take: DBS, UOB, OCBC

DBS leads the pack with strong, consistent dividends and bonus capital returns—like owning a cash cow that pays you more each year. If you want stability and reliable income, DBS is a top pick. UOB has stepped up payouts too, including special dividends, making it a strong contender for both growth and bonuses. OCBC lags this round but is still planning special dividends and buybacks, so don’t write it off yet.

For steady, growing payouts, banks are your best bet in Singapore. DBS is the go-to for visible returns. UOB adds extra spice with special payments. OCBC is playing catch-up, but could surprise next year. If your goal is compounding income, banking giants deserve prime slots in your portfolio.

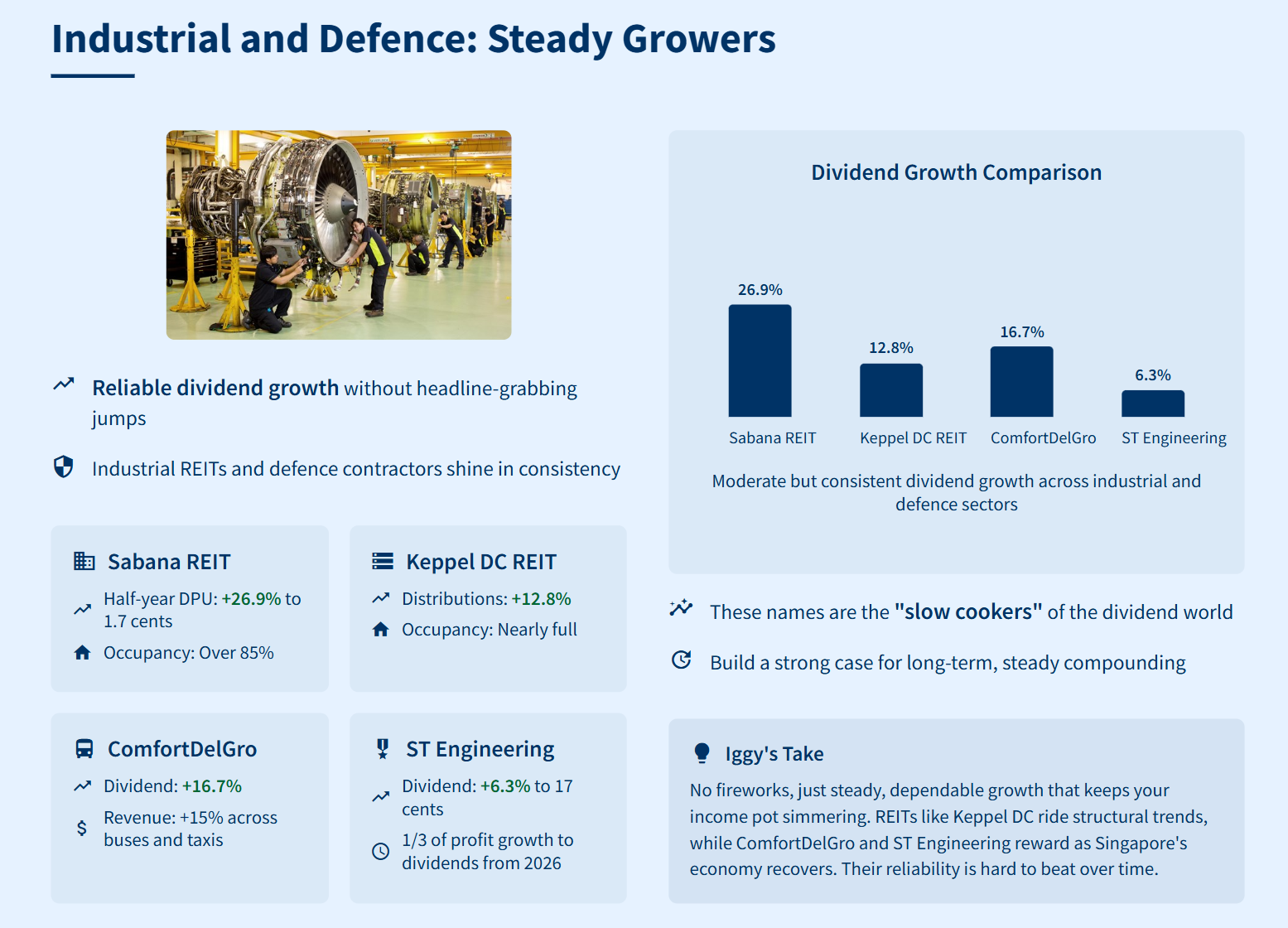

Industrial and Defence: Steady Growers

Industrial REITs and defence stocks may not make headlines with wild jumps, but their strength is reliability. Sabana REIT lifted its half-year DPU by 26.9% to 1.7 cents. The jump came from solid profits and over 85% occupancy—showing its buildings are filled and earning well.

Keppel DC REIT keeps raising the bar too. Its distributions jumped 12.8%, supported by near-full occupancy and steady rental growth. This shows the benefit of being in the data-centre business—riding a wave of growing demand for storage and cloud services.

ComfortDelGro, Singapore’s top transport group, gave investors a 16.7% dividend boost. This rebound was powered by a 15% rise in revenue from buses and taxis, climbing back after the pandemic hit public transport hard.

ST Engineering, a heavyweight in defence and engineering, nudged its dividend up 6.3% to 17 cents. The key? Management is now promising to pay out a third of future profit growth as dividends starting in 2026. That’s a clear sign of shareholder commitment.

These might not be blockbuster jumps, but they lay a strong foundation for compounding over time. Think of these stocks as steady “income engines.” They help you build up returns year after year, without relying on risky leaps. For investors who value stability and long-term growth, these names are essential in any dividend portfolio.

Iggy’s Take: Industrial & Defence

These names are the “slow cookers” of the dividend world—no fireworks, just steady, dependable growth that keeps your income pot simmering. REITs like Keppel DC are great for riding structural trends (think data centres), while ComfortDelGro and ST Engineering reward you as Singapore’s economy recovers and grows. If you want extra security in your portfolio, mix in these steady growers. They may not wow you in any single year, but over time, their reliability is hard to beat.

Exchange and Other Sectors

Singapore Exchange (SGX) is showing its leadership with a solid 8.7% dividend hike, bringing payouts to S$0.375. Even better, SGX has set a clear dividend roadmap—S$0.25 per quarter, locked in through 2028. For investors who plan their income flows, this kind of guarantee is rare and valuable. It’s almost like having a paycheck from the market, letting you budget with confidence.

Oiltek sits on the other end of the spectrum. The company boosted its interim dividend by 66.7%. That jump came from strong demand for fats and oils, plus an adjusted payout after a bonus issue. These numbers are exciting, but let’s remember: small-cap stocks like Oiltek can be a wild ride. Today’s big payout might not repeat tomorrow if demand shifts or costs climb.

These companies broaden your options beyond the usual dividend players. SGX gives you a steady income stream with future certainty—perfect for cautious, income-focused investors. Oiltek is proof that niche players can win big when the stars align, though the risks are higher.

Iggy’s Take: Exchange & Other Sectors

SGX is the dependable train—slow but always on schedule. If you want steady income and less drama, SGX gives you predictability all the way to 2028. Oiltek is an exciting ride for thrill-seekers, but small-cap risks mean wild swings. For most investors, SGX is the safer pick. Only jump into names like Oiltek if you’re okay with twists and turns

Key Risks

Economic downturns: If Singapore or global economies slow down, company profits may fall and dividends could be cut. Even strong performers are not immune—watch for changes in growth momentum.

Rising interest rates: Higher rates are a problem for property stocks and REITs. Financing costs go up and assets may lose value, meaning companies might trim payouts to stay afloat.

Property cycles: Stocks like PropNex boom when transaction volumes rise, but slow markets can shrink profit and dividends. Investors need to watch property trends and avoid getting caught after the peak.

Telco and fintech competition: Heavy spending on infrastructure (capex) and fierce competition make it tough for companies like Singtel and new tech players to reliably grow payouts.

Geopolitical tensions: Many of these companies operate across Asia. Trade wars, regulatory changes, or political unrest can disrupt profits and dividends.

High payout ratios: When companies return most profits as dividends, they have less room to adjust if earnings fall. In tough years, there’s a higher chance of cuts.

Takeaway:

Dividends are not guaranteed. Even strong companies face risks from economic swings, interest rates, and competitive or global shocks. It’s wise to diversify and keep an eye on market cycles—what looks safe today might not be tomorrow.

Conclusion & Recommendations

If your goal is to grow your income year after year, focus on stocks with sustainable dividend growth—not just the flashiest yields.