It’s Not AI Boom. It’s 1.9% Venture Revenue | SGX Daily Pulse 6 May 2026 | 🦖EP1593

And it’s not AI infrastructure paying you. It’s a 1.9% crawl while T-Bill spreads thin to 1.40%

The 3.2% Floor Test: Why GE, Venture, and CAReit Just Triggered My Audit | SGX Daily Pulse 6 May 2026 | EP1593

The market focused on the 1.9% revenue climb. My forensic audit found the hidden pressure on the yield spread.

Most investors are cheering Venture’s AI growth story, but the forensic reality is that a 1.9% revenue crawl in a boom cycle is a red flag for your dividend safety. If you are relying on these blue chips to defend your SRS or CPF OA against firming inflation, you are currently operating without a stress-test buffer. Today, I audit the Q1 numbers to show you exactly where the yield spread is thinning before the market reacts.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips — the interest coverage, the gearing, the free cash flow sustainability — so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

In This Article:

Market Snapshot

The Audit

Great Eastern G01 Watchlist Trigger

Venture Corporation V01 Yield Trap Alert

Centurion Accommodation REIT CAReit Price Dependent Watch

Analyst Chatter

Watchlist and Yield Spread

Iggys Take The Bottom Line

Iggys Forensic Disclaimer

MARKET SNAPSHOT

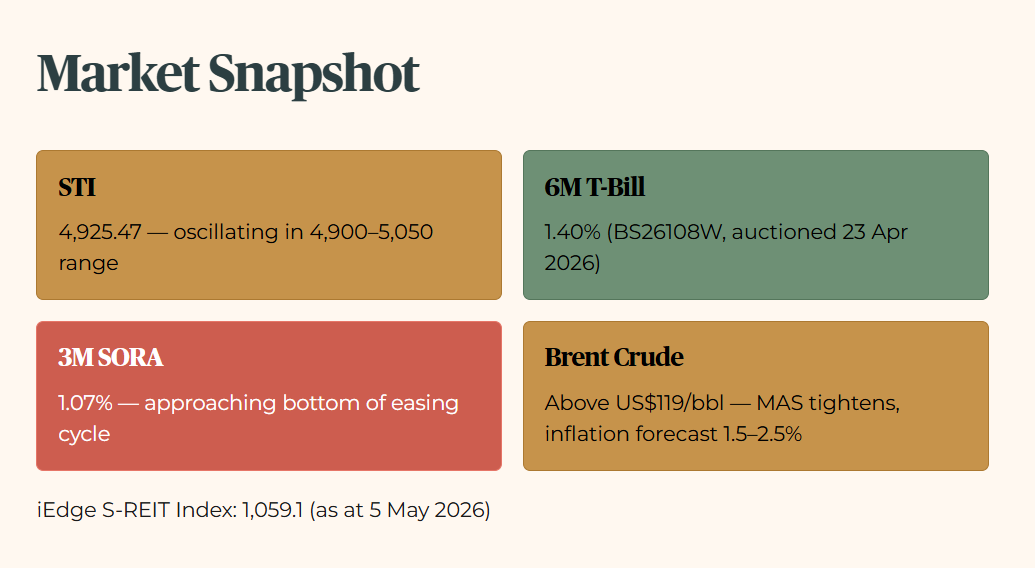

STI Level: 4,925.47. Oscillating within the 4,900–5,050 range as psychological resistance holds post-relief rally.

6-Month T-Bill: 1.40% (Issue: BS26108W, Auction: 23 Apr 2026). Yields continue to edge lower from previous issues.

3-Month SORA: 1.07% (mid-April 2026). Short-term benchmarks suggest we are approaching the bottom of the easing cycle.

iEdge S-REIT Index: 1,059.1 (as at 5 May 2026).

Macro Event: Brent Crude remains volatile above US$119/bbl, driving the MAS to pre-emptively tighten policy and lift 2026 inflation forecasts to 1.5–2.5%.

THE AUDIT

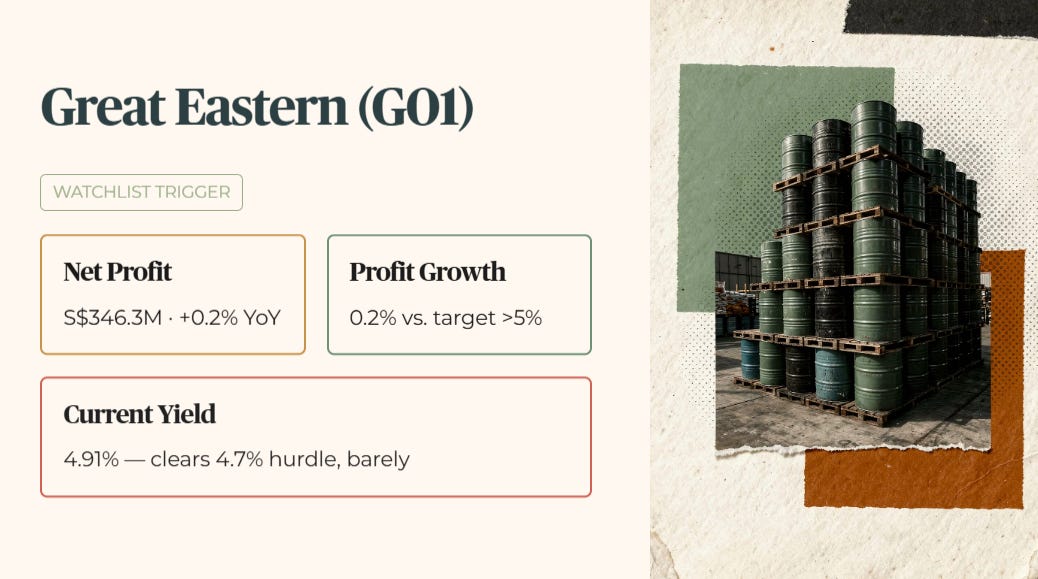

Great Eastern (G01) — WATCHLIST TRIGGER

Forensic Verdict: Steady profit masks a deteriorating investment environment that fails my risk-premium hurdle.

Layer 1 — Raw Fact: Net profit rose 0.2% to S$346.3 million, underpinned by insurance profits despite a less favourable investment environment.

Layer 2 — Benchmark: Profit growth of 0.2% sits far below Great Eastern’s own mid-teens annual average over the last three years, a period that includes the sharp 2023 rebound and double-digit gains in 2024 and 2025. Against core inflation now at 1.7%, this quarter represents effective stagnation.

Layer 3 — Peer Context: SGX-listed peer Prudential PLC (K6S) reflects broader regional volatility. Unlisted competitor Singlife targets higher growth margins in the protection segment, making GE’s 0.2% a structural outlier in its own cycle.

Layer 4 — Forward Scenario: A 10% decline in investment income would wipe out the marginal insurance profit gain, potentially dropping net profit by S$30 million or more. The named trigger is a sustained US interest rate hold compressing reinvestment yields.

Layer 5 — Wallet Impact: For a 60-year-old retiree in Toa Payoh managing an SRS drawdown, this 0.2% growth represents a real-term loss against headline inflation of 1.8%. The yield at 4.91% clears the 4.7% minimum hurdle, but the margin for error has thinned. Forensic stance: Watchlist Trigger as profit momentum stalls and the yield spread over the T-Bill compresses.

Iggy’s Insight

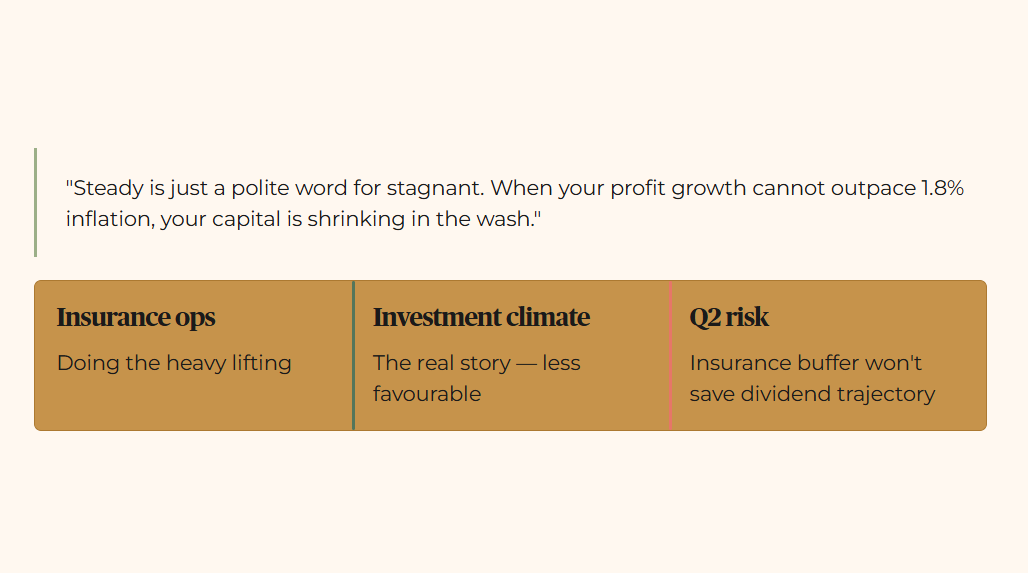

Great Eastern is puffing its chest over a 0.2% profit increase, but that is essentially a flatline in this economy. Insurance operations are doing the heavy lifting, but the less favourable investment climate is the real story here. When your profit growth cannot outpace the 1.8% headline inflation rate, your capital is shrinking in the wash. The 4.91% yield clears my minimum hurdle — but clearing the floor is not the same as earning conviction. If investment income takes even a minor hit in Q2, that insurance buffer will not save the dividend trajectory. Steady is just a polite word for stagnant.

Venture Corporation (V01) — YIELD TRAP ALERT

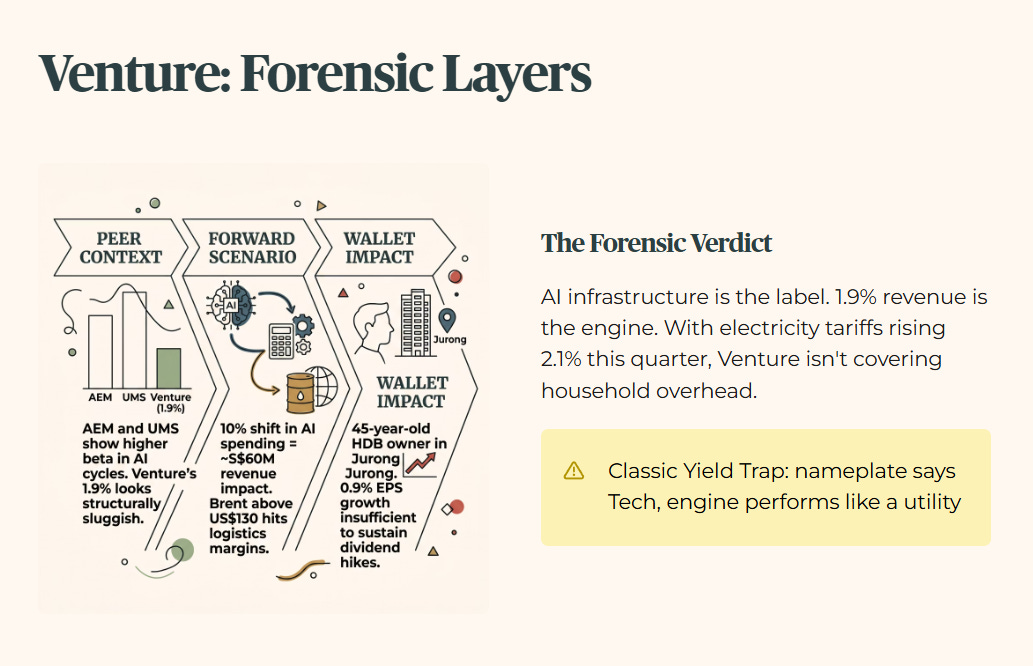

Forensic Verdict: AI infrastructure demand is the headline, but the 1.9% revenue growth is a forensic whisper.

Layer 1 — Raw Fact: Venture reported a net profit of S$56.3 million on revenue of S$628.5 million, up 1.9% year-on-year.

Layer 2 — Benchmark: The 1.9% revenue lift is a deceleration from historical AI-cycle benchmarks and barely covers the 1.7% MAS Core Inflation floor. In a boom cycle, this is not growth — it is drift.

Layer 3 — Peer Context: Sector peers AEM (AWX) and UMS (558) typically show higher beta in semiconductor and AI cycles. Against that backdrop, Venture’s 1.9% looks structurally sluggish, not conservatively positioned.

Layer 4 — Forward Scenario: A 10% shift in global AI infrastructure spending would impact revenue by roughly S$60 million. The named trigger is a Brent Crude oil price shock above US$130, hitting logistics costs and compressing margins further.

Layer 5 — Wallet Impact: A 45-year-old HDB owner in Jurong supplementing a salary would see Venture’s 0.9% EPS growth as insufficient to sustain long-term dividend hikes. Forensic stance: Yield Trap if the stock continues to trade at a premium to fair value while growth stalls.

Iggy’s Insight

The market is obsessed with the AI Infrastructure label, but the numbers tell a much more boring story. A 1.9% increase in revenue during a global AI boom is like bringing a bicycle to an F1 race. Venture is surviving on its reputation, but the forensic math shows EPS barely moving at 0.9%. With cost-of-living anchors like electricity tariffs rising 2.1% this quarter, this stock is not even covering household overhead. We are looking at a classic Yield Trap where the name plate says Tech but the engine performs like a utility. Activity is not the same as progress.

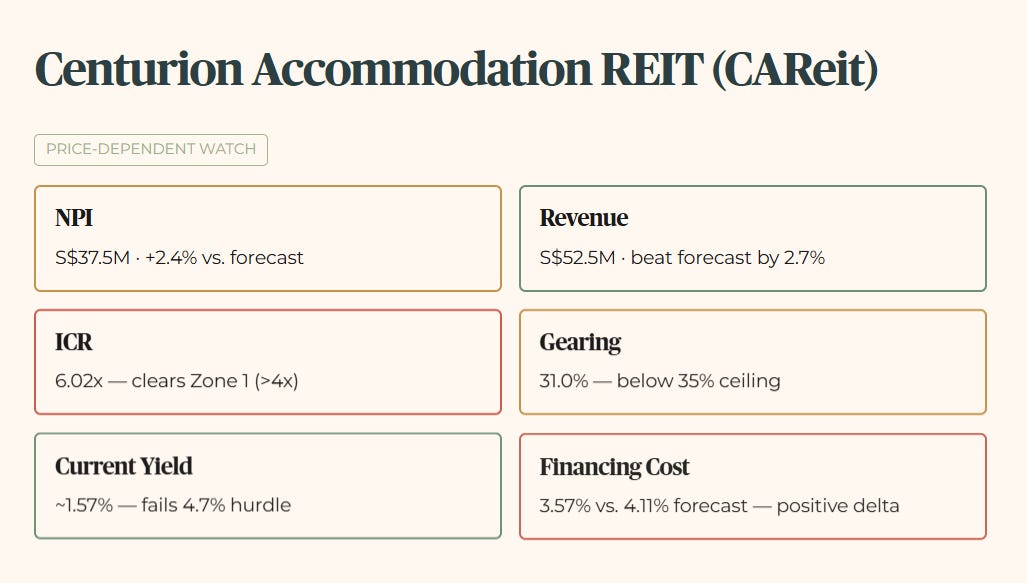

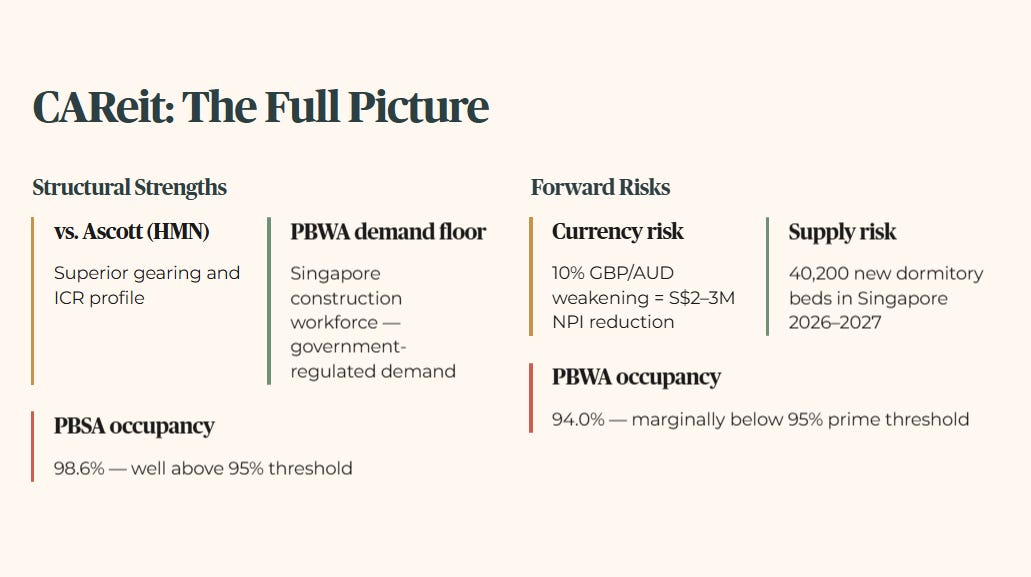

Centurion Accommodation REIT (CAReit) — PRICE-DEPENDENT WATCH

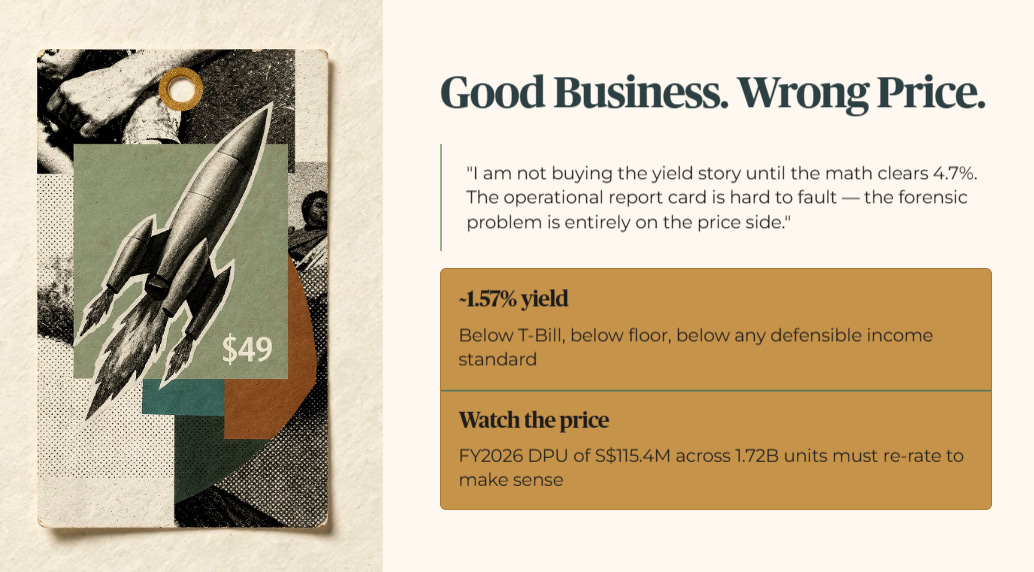

Forensic Verdict: Strong operational debut, but current market pricing has pushed the yield below my forensic floor. This is a business worth watching — not a yield play at today’s price.

Layer 1 — Raw Fact: Net Property Income reached S$37.5 million, up 2.4% against the prospectus forecast of S$36.6 million, driven by higher occupancy, stronger rental rates, and a favourable GBP and AUD against the SGD. Revenue of S$52.5 million also beat forecast by 2.7%.

Layer 2 — Benchmark: The NPI beat is genuine and the capital structure is clean. ICR at 6.02x clears Zone 1. Gearing at 31.0% sits comfortably inside the 35% ceiling with S$340.8 million of debt headroom remaining. The weighted average financing cost of 3.57% came in well below the prospectus forecast of 4.11% — a meaningful positive delta on interest expense management. On every operational metric, this is an above-average debut quarter.

Layer 3 — Peer Context: Against CapitaLand Ascott Trust (HMN), CAReit’s gearing and ICR profile is superior. The structural difference is asset class — worker dormitories and student accommodation carry different demand drivers than hospitality. CAReit’s PBWA segment, anchored by Singapore’s construction and marine sector workforce, benefits from a government-regulated demand floor that Ascott does not have.

Layer 4 — Forward Scenario: A 10% weakening of the GBP and AUD against the SGD would reduce NPI by approximately S$2 to 3 million. The named trigger is MAS steepening the S$NEER slope, which would work against currency-driven outperformance. On the supply side, 40,200 new dormitory beds are scheduled for delivery across Singapore in 2026 and 2027, which could soften PBWA occupancy from the current 94.0% — already marginally below the 95% prime asset threshold.

Layer 5 — Wallet Impact: For a 55-year-old PMET in Punggol considering CAReit for a CPF OA portfolio, the operational story is encouraging. The balance sheet is conservative, the income is beating forecast, and the demand fundamentals across Singapore, the UK, and Australia all point in the right direction. The problem is price. At approximately 1.57% yield on current market pricing, CAReit does not clear the 3.2% forensic floor — let alone the 4.7% minimum hurdle. This is not a yield play today. It becomes one only if the unit price corrects toward a level where the projected FY 2026 distribution of S$115.4 million across 1.72 billion units starts to make sense for an income investor. Watch the price, not just the business.

Iggy’s Insight

The operational report card for CAReit is hard to fault. NPI beat, ICR above 6x, gearing at 31%, financing cost below forecast — this management team has delivered a clean debut quarter. The PBWA occupancy at 94.0% is the one number I am watching, sitting just below my 95% prime asset threshold, but the demand backdrop from Singapore’s construction pipeline gives me comfort that this is a ramp-up issue, not a structural one. The forensic problem is entirely on the price side. The market has bid this up to a point where the yield sits at roughly 1.57% — below the T-Bill, below my floor, below any defensible income standard. Good business. Wrong price. I am not buying the yield story until the math clears 4.7%.

ANALYST CHATTER

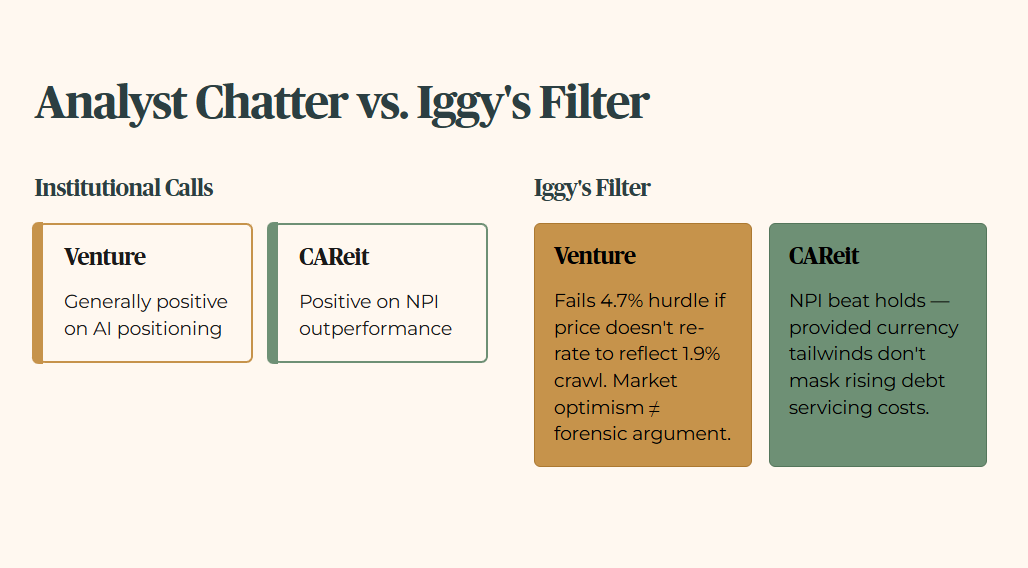

Institutional call: Analysts are generally positive on Venture’s AI positioning.

Iggy’s Filter: This call fails the 4.7% minimum yield hurdle if the stock price does not re-rate to reflect the actual 1.9% revenue crawl. Market optimism is not a forensic argument.

Institutional call: Positive sentiment on CAReit due to NPI outperformance.

Iggy’s Filter: This holds up against the 3.2% floor, provided the currency tailwinds are not used to mask a rise in debt servicing costs.

WATCHLIST AND YIELD SPREAD

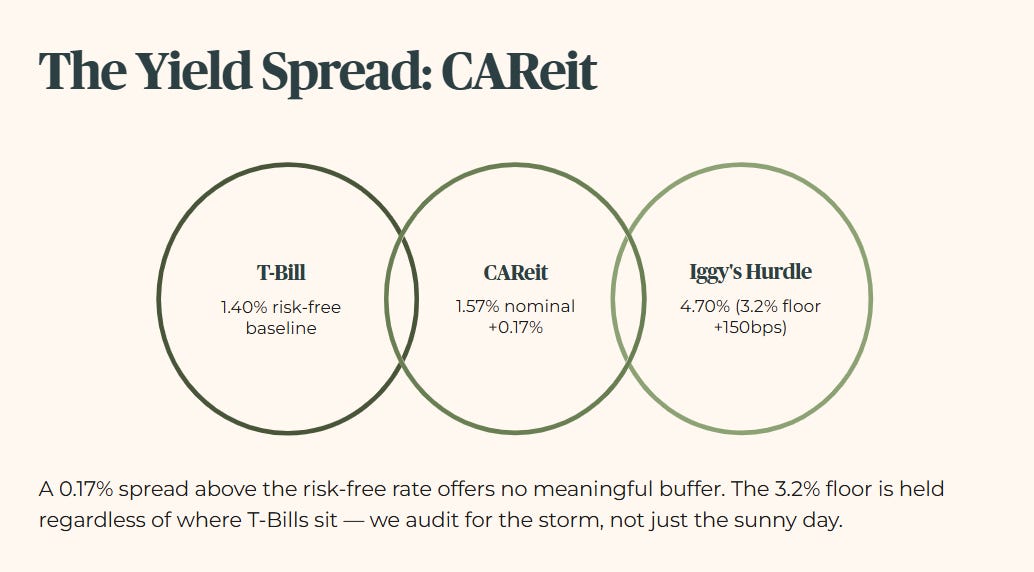

The Calculation: CAReit’s current market yield of approximately 1.57% against the T-Bill at 1.40% (BS26108W) produces a nominal risk premium of just 0.17% — a spread so thin it offers no meaningful buffer above the risk-free rate and sits far below the 4.7% forensic minimum hurdle. The operational business clears every structural gate. The price does not.

Note on the Stress-Test Buffer: For this audit, I apply a conservative floor of 3.2%. We audit for the storm, not just the sunny day. While the T-Bill sits at 1.40%, I do not lower my standards to match a temporary market dip. My floor remains at 3.2% to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7% — the 3.2% floor plus 150 basis points of mandatory risk premium.

The Window Is Already Open

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

IGGY’S TAKE: THE BOTTOM LINE

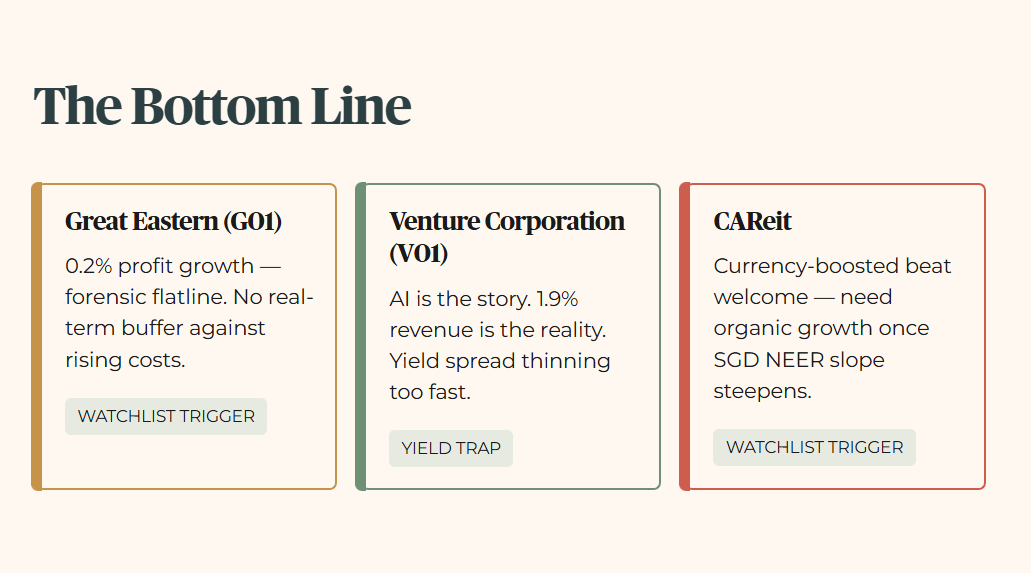

Great Eastern (G01): The 0.2% profit growth is a forensic flatline that fails to provide a real-term buffer against rising costs. Watchlist Trigger.

Venture Corporation (V01): AI demand is the story, but 1.9% revenue growth is the reality. The yield spread is thinning too fast for comfort. Yield Trap.

Centurion Accommodation REIT (CAReit): A currency-boosted beat is welcome, but we need to see organic growth once the SGD NEER slope steepens. Watchlist Trigger.

The market is currently pricing in a soft landing, but when I look at the cost of capital benchmarks in Clementi — where bank mortgages are hitting the high-1% range — the margin for dividend error is disappearing. If your assets are not clearing the 4.7% hurdle, you are not investing. You are subsidising the bank’s balance sheet.

Iggy’s Forensic Disclaimer

This content is produced for educational and informational purposes only. I am not a financial advisor — I am a retail investor who applies forensic analysis to my own portfolio and shares that process publicly. Nothing here constitutes a recommendation to buy, sell, or hold any security, and no specific target prices or personalised financial advice are offered. Stocks assessed under Iggy’s Forensic Yield Standard are benchmarked against a 4.7% minimum yield hurdle; stocks flagged as Growth Watch fall below this threshold but demonstrate clean balance sheet metrics and an identifiable growth catalyst — these carry a materially different risk profile and are not suitable as yield replacements for income-dependent investors. All data is sourced from public filings and verified sources; where data is unverified it is explicitly flagged. All investments carry risk, including the potential loss of principal, and past performance is not indicative of future results. If you are making investment decisions involving CPF, SRS, or personal capital, please conduct your own due diligence or consult a MAS-licensed financial adviser before committing funds.