JP Morgan Downgrades OCBC: Stop Buying For Growth? |🦖EP1375

The JP Morgan downgrade landed hard. But for dividend investors in OCBC, it may be noise masking a real opportunity.

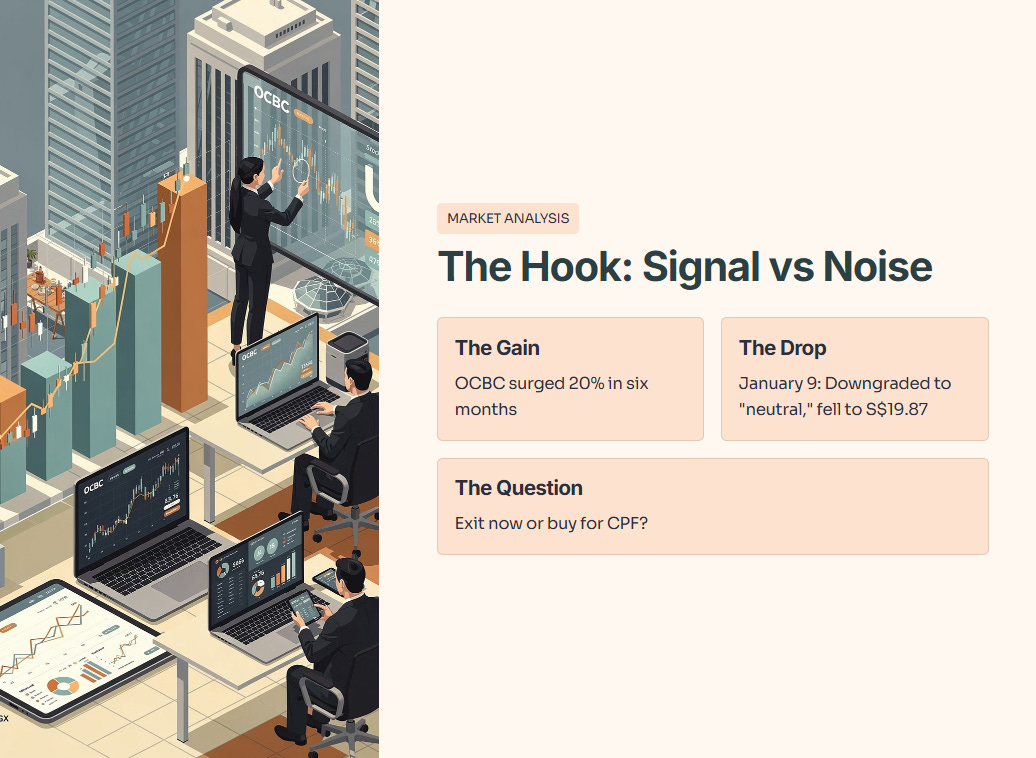

The Hook: Separating Signal from Noise

Your OCBC stake gained 20% in six months. Then, on January 9, JP Morgan downgraded the stock from “overweight” to “neutral.” The share price dipped from S$20.25 to S$19.87.

Now you’re asking: Did I miss my exit? Or is this a buying moment for my CPF portfolio?

The market loves to overreact to headlines. The answer isn’t “sell” or “hold.” It’s about understanding why the downgrade happened. JP Morgan analysts Harsh Wardhan Modi and Daniel Andrew Tan noted that “various positives driving the gain... have been priced in.”

💡 Iggy’s Insight:

What Does “Priced In” Actually Mean? Imagine buying a ticket to a concert. If you buy it early when nobody knows the band, it is cheap. Once the band is famous, the ticket price skyrockets. The concert is the same. The music is the same. But the price you pay for the experience is now at its peak.

That is what “priced in” means. The earnings growth and dividend hikes are known. The analysts aren’t saying the bank is broken; they are saying the “easy money” phase of the trade is over. The rocket ship engine has cut off, and we are now coasting.

In This Article:

• The Iggy Audit: The Numbers That Actually Matter

• The Earnings Pivot (The Hidden Bull Case)

• Asset Quality: The Safety Net

• The InvestingPro Data Check

• The Verdict: Your CPF Playbook

• SummaryAbout Iggy the Investing Iguana Channel

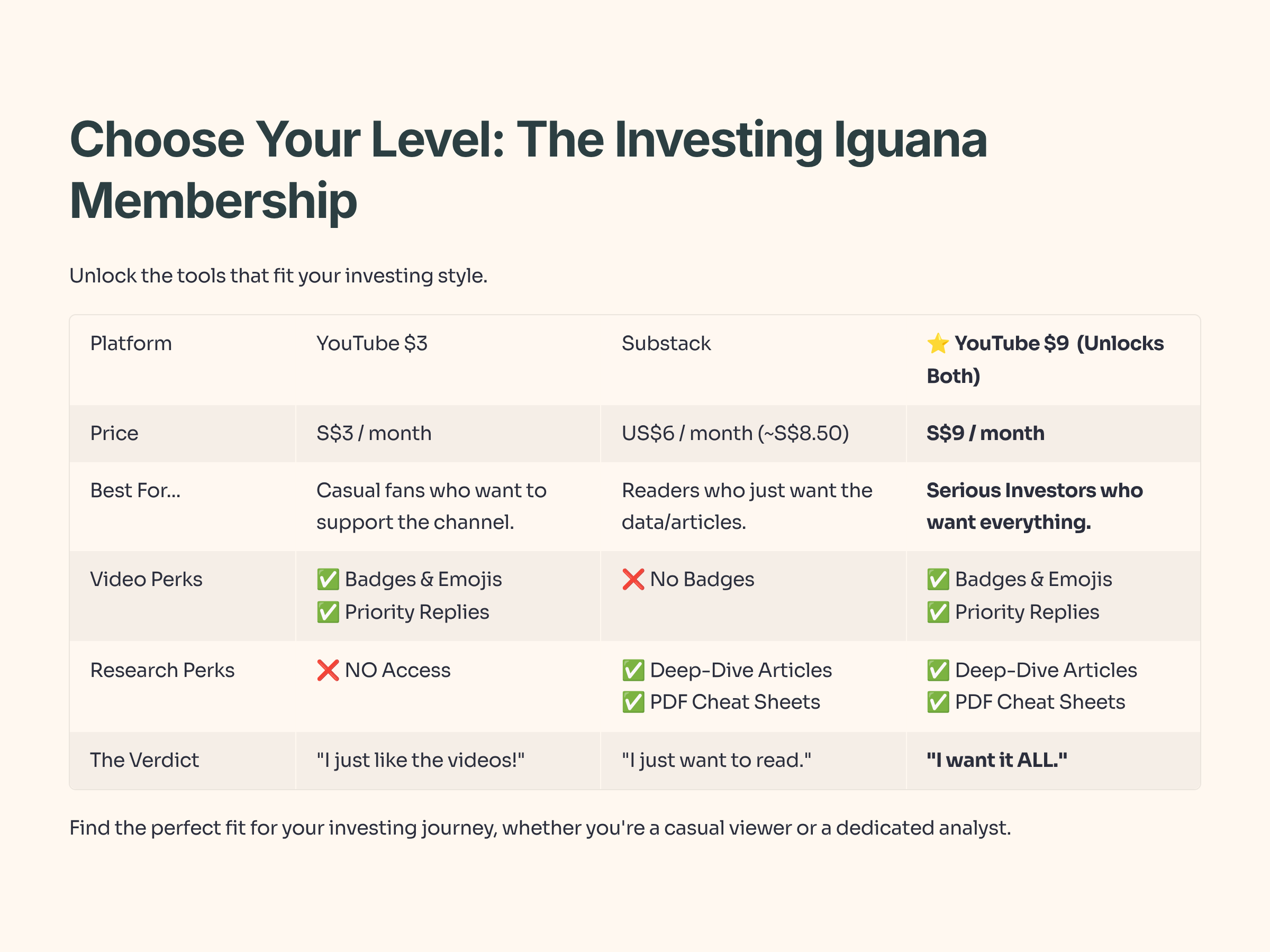

If you’re new here, welcome. I’m Iggy, your Singapore-based market analyst. Since October 2025, we’ve produced over 1,300 videos and 400 articles with 1.1 million watch hours. We are also home to a growing community of over 90 YouTube Premium subscribers and 37 paid Substack members.

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the ‘smart money’ move. Now, let’s get to the numbers.

The Iggy Audit: The Numbers That Actually Matter

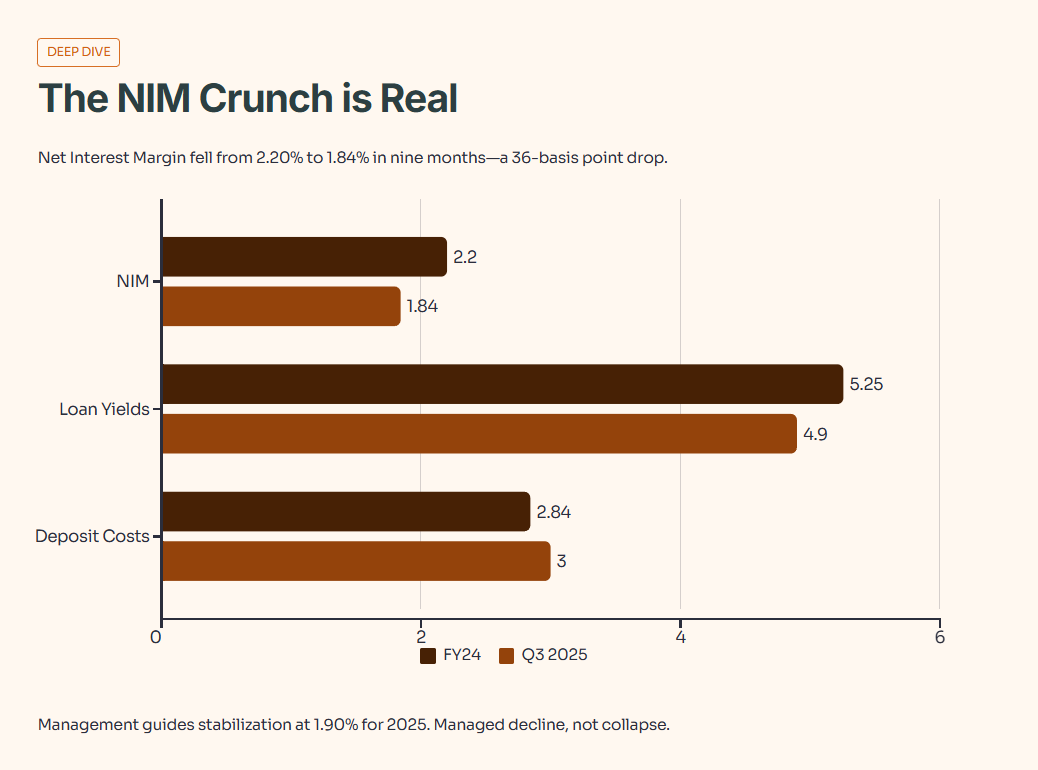

The headline is the downgrade. The reality is the Net Interest Margin (NIM) crunch. This is the mechanism that determines if your dividend is safe.

1. The NIM Crunch is Real

Banks are essentially shops that buy money (deposits) and sell money (loans). OCBC’s margin on this trade is shrinking.

Net Interest Margin: Fell from 2.20% (FY24) to 1.84% (Q3 2025).

The Trap: Loan yields dropped to ~4.9% (because of falling rates), but deposit costs rose to ~3.0% (to keep your cash).

This is classic cycle mechanics. Banks mint money when rates rise (the “free lunch” era of 2022-2024). When rates fall, the free lunch ends. If you hold this stock expecting NIM to bounce back to 2.2% next quarter, you are driving while looking in the rearview mirror.

When rates in Singapore and Hong Kong drop, OCBC’s floating-rate loans yield less, but they still have to pay up to keep your deposits. Management has guided for stabilization around 1.90% for 2025. This is a managed decline, not a collapse.

💡 Iggy’s Insight:

This is classic cycle mechanics. Banks mint money when rates rise (2022-2024). When rates fall, the “free lunch” ends. However, the market often forgets that banks have other levers. If you sell now solely because NIM is down, you are driving looking in the rearview mirror.

2. The Earnings Pivot (The Hidden Bull Case)

While the “interest” business slows down, the “fee” business is waking up.

Trading income: +53%

Wealth management fees: +22%

Insurance income: +14%