CICT Fair Value $1.71? Analyzing JPMorgan’s "Lucky 7" Picks

Why the “Boring” Singapore Market Might Be the Smartest Play for the Next 18 Months.

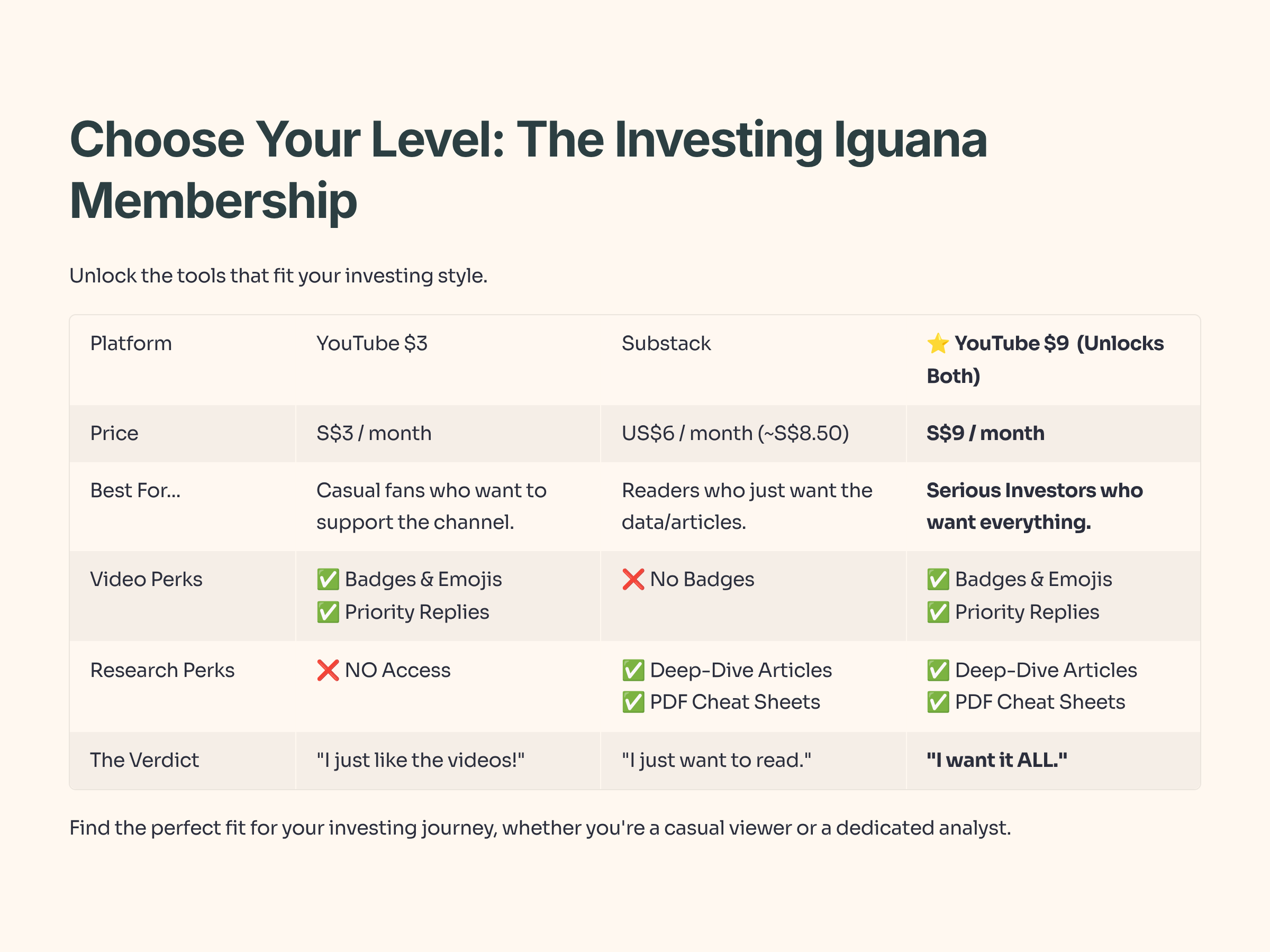

If you’re new here, welcome. I’m Iggy, your Singapore-based market analyst. Since 2025, we’ve produced over 1,300 videos and 400 articles with 1.1 million watch hours. We are also home to a growing community of over 60 YouTube Premium subscribers and 30 paid Substack members.

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the “smart money” move. Now, let’s get to the numbers.

The Macro Bull Case: Why 2026 is Different

For years, the Singapore market has been viewed as a “yield trap”—great for dividends, terrible for capital appreciation. But JPMorgan’s latest analyst note suggests a structural shift is underway.

They have named seven top picks for 2026—DBS, Keppel, City Developments (CDL), CapitaLand Integrated Commercial Trust (CICT), ST Engineering, Sea Ltd, and Singtel.

But the tickers aren’t the most important part of this report. The real story is the Return on Equity (ROE). JPMorgan forecasts Singapore’s market ROE rising from 10% toward a historic 12%.

Iggy’s Insight:

Why does ROE matter? Because historically, Singapore stocks trade at a discount because they are “lazy” with capital. If ROE hits 12%, we aren’t just looking at earnings growth; we are looking at a valuation re-rating. When efficiency goes up, the Price-to-Book multiple the market is willing to pay goes up. That is the “double engine” of total return: Dividends + Multiple Expansion.

The catalysts driving this are specific policy moves:

The S$5b Equity Market Development Programme (EMDP).

The SGX–Nasdaq dual-listing bridge.

Rotation of domestic cash from fixed deposits back into equities as T-bill yields stabilize.

The “Lucky 7” Breakdown: A CPF/SRS Perspective

JPMorgan’s list is a mix of aggressive growth and defensive fortresses. I’ve re-organized them into three specific “buckets” based on how they should function in your portfolio.

Bucket 1: The “Fortress” Income Anchors (DBS, CICT, Singtel)

These are your CPF/SRS core holdings. The thesis here is visibility and yield preservation.

DBS (The Bellwether): Even as rates plateau, wealth management flows and deposit dynamics remain superior. The bank is a proxy for the entire economy.

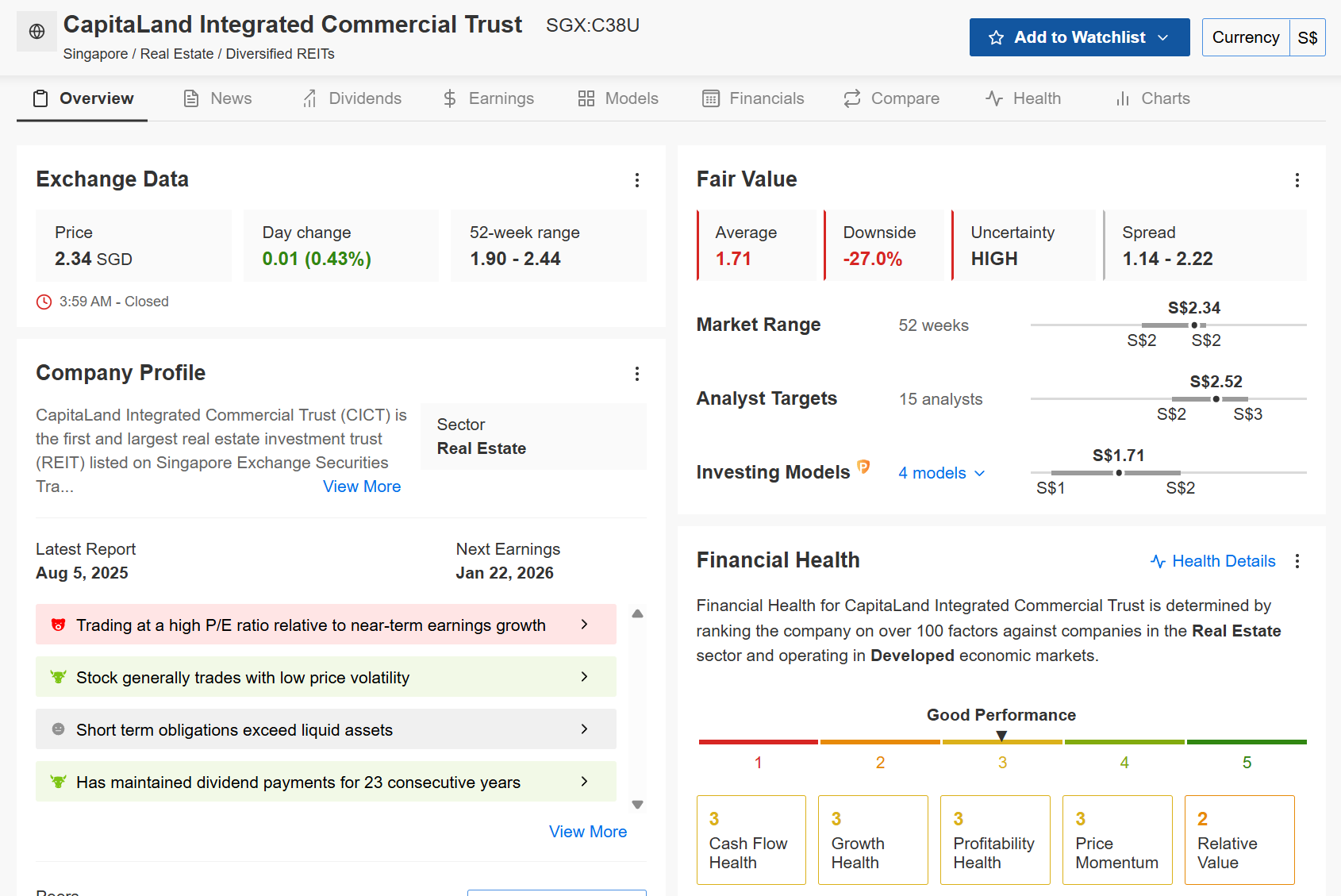

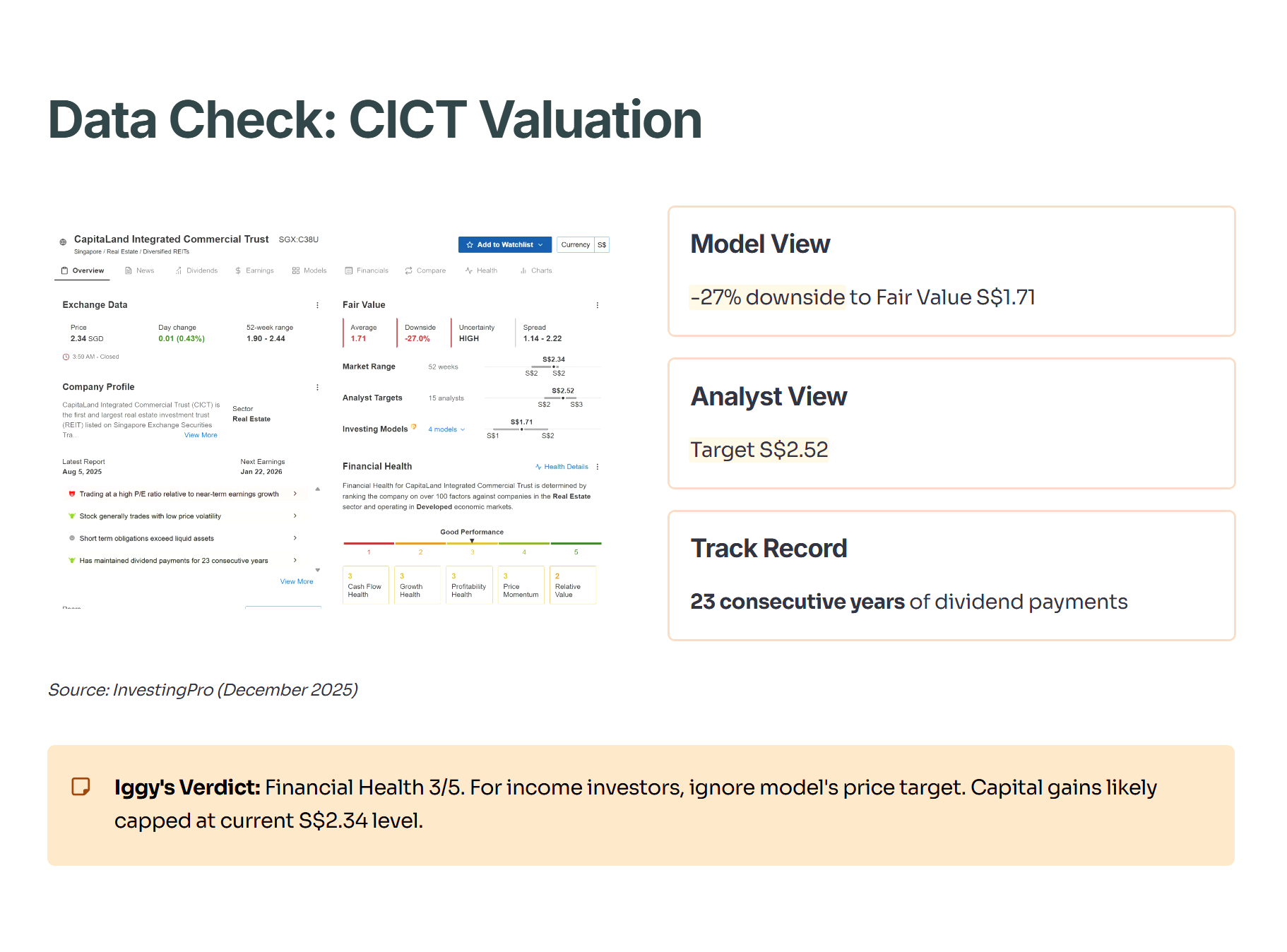

CICT (The Landlord): As the largest commercial REIT, CICT has the scale to secure lower funding costs than its smaller peers.

Data Check: Valuation & Dividend Safety (CICT)

I don’t just guess at valuations. I check the institutional models.

Source: InvestingPro (Data as of December 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

Iggy’s Analysis:

This is a classic “Model vs. Human” conflict.

The Models: They are flagging a -27% downside to a Fair Value of S$1.71. Why? Models often penalize REITs for “Short term obligations exceeding liquid assets” (a common REIT trait) and high P/E relative to growth.

The Analysts: Humans see a target of S$2.52. They are pricing in the stability of the assets and the “23 consecutive years of dividend payments” (a rare feat).

The Verdict: The “Financial Health” score is a solid 3/5. For income investors, the key metric here is that 23-year streak. Ignore the model’s price target if your goal is income, but be aware that capital gains might be capped at the current S$2.34 level.

Bucket 2: The “Structural Change” Plays (Keppel, ST Engineering)

These companies are transitioning their business models. This is where the capital appreciation potential lies.

Keppel: This is no longer a rig builder. It is an asset manager and clean energy play. JPMorgan likes the “asset-light” model because it boosts ROE (less capital tied up in heavy machinery, more fee income).

ST Engineering (STE): This is your defense against volatility. With geopolitical tensions high, defense spending is non-discretionary. STE’s massive order book provides earnings visibility through 2027.

Iggy’s Insight:

Keppel is my preferred pick for “Growth at a Reasonable Price” (GARP). The market still partially prices it like a conglomerate, not fully crediting it as an asset manager. If they execute their 2030 targets, the multiple expansion here could be significant.

Bucket 3: The “Deep Value & Optionality” (CDL, Sea Ltd)

This is the high-risk, high-reward bucket. Proceed with caution.

City Developments (CDL): The thesis is “Value Unlocking.” Developers often trade at steep discounts to their Revalued Net Asset Value (RNAV).

Sea Ltd: The odd one out. It’s not a dividend stock. It’s a bet on regional consumption and gaming recovery.

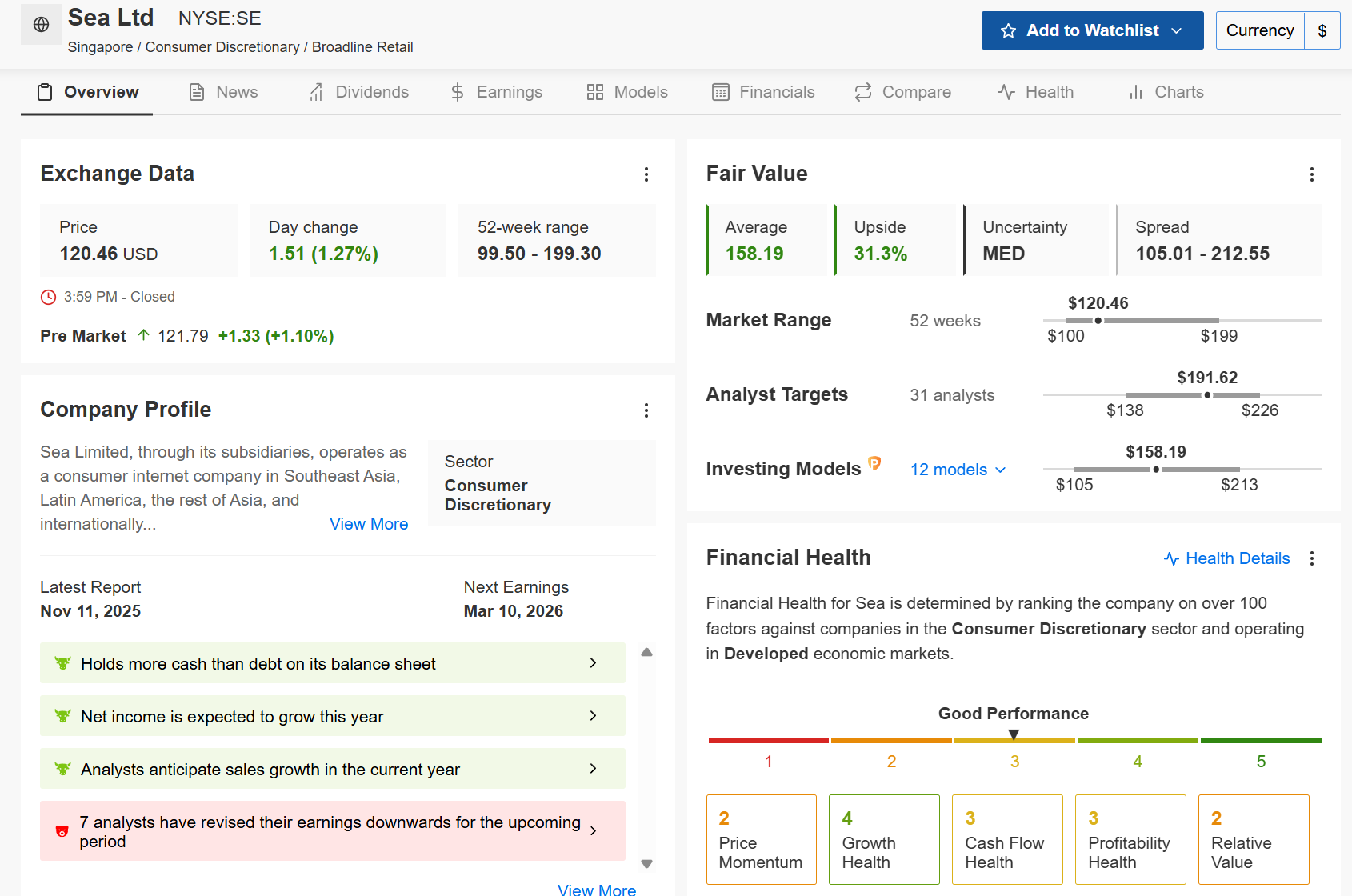

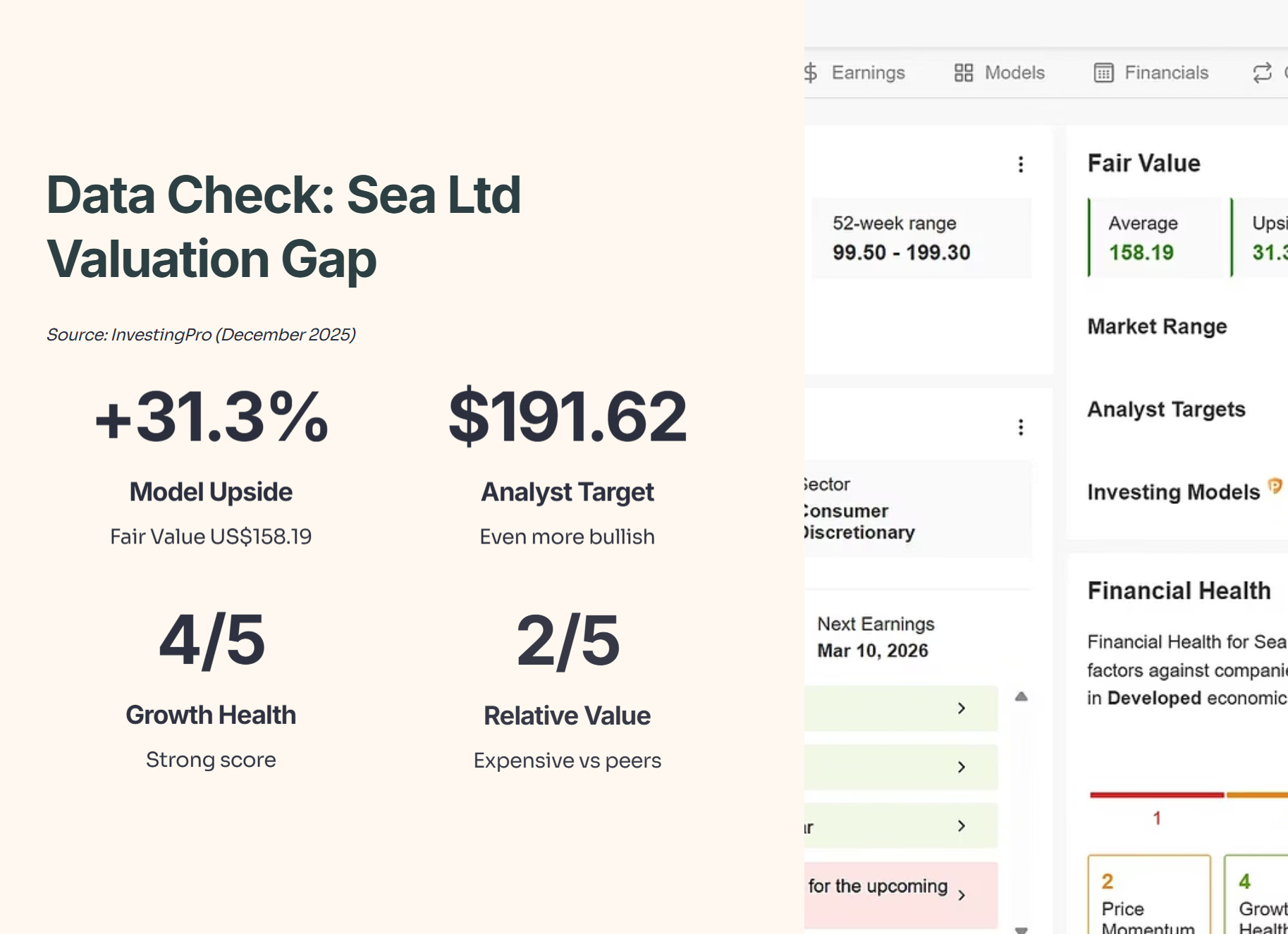

Data Check: Valuation Gap (Sea Ltd)

I don’t just guess at valuations. I check the institutional models.

Source: InvestingPro (Data as of December 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

Iggy’s Analysis:

Here, the models and the analysts actually agree on the direction—Up.

Upside: The Fair Value model predicts a +31.3% upside to US$158.19. Analysts are even more bullish, targeting US$191.62.

Growth: The “Growth Health” score is a strong 4/5, supported by expectations of net income and sales growth this year.

The Risk: Note the “Relative Value” score is a low 2/5. This stock is expensive compared to its peers, but cheap compared to its own potential growth. The “7 analysts revising earnings downwards” warning is your red flag—volatility is guaranteed.

Iggy’s Take:

Be very careful with Sea Ltd in a CPF/SRS portfolio. Despite the green numbers, it does not fit the mandate of capital preservation. I treat Sea Ltd as “Casino Money”—only allocate what you can afford to see drop 20% in a week.

The Strategy: How to Deploy This List

JPMorgan’s bullishness is based on a 2026 horizon. This means you do not need to rush in tomorrow morning at market open.