Kasikornbank 7.11% Yield: Is This Thai Fortress A Trap For Your Retirement?

Your 7% payout might look steady, but Thai household debt is a debt wall waiting to collapse

Kasikornbank PCL (SGX:TKKD): 3 Good & 3 Red Flags

The market sees a regional banking titan with a fortress balance sheet and a dividend yield that makes Singapore’s “Big Three” look like conservative savings accounts. Yet, the forensic data reveals a paradox: KBANK is paying out record dividends while simultaneously shrinking its loan book and bracing for a structural compression in its core profit engine. It is the classic “Skeptical Arbitrator” dilemma. Is this a high-yield recovery play or a beautifully wrapped trap set within a stagnating Thai economy?

In This Article:

The Financial Snapshot (The Baseline)

The 3 Good (The Bull Case)

Good 1: The “Kopitiam King” Yield and Payout Pivot

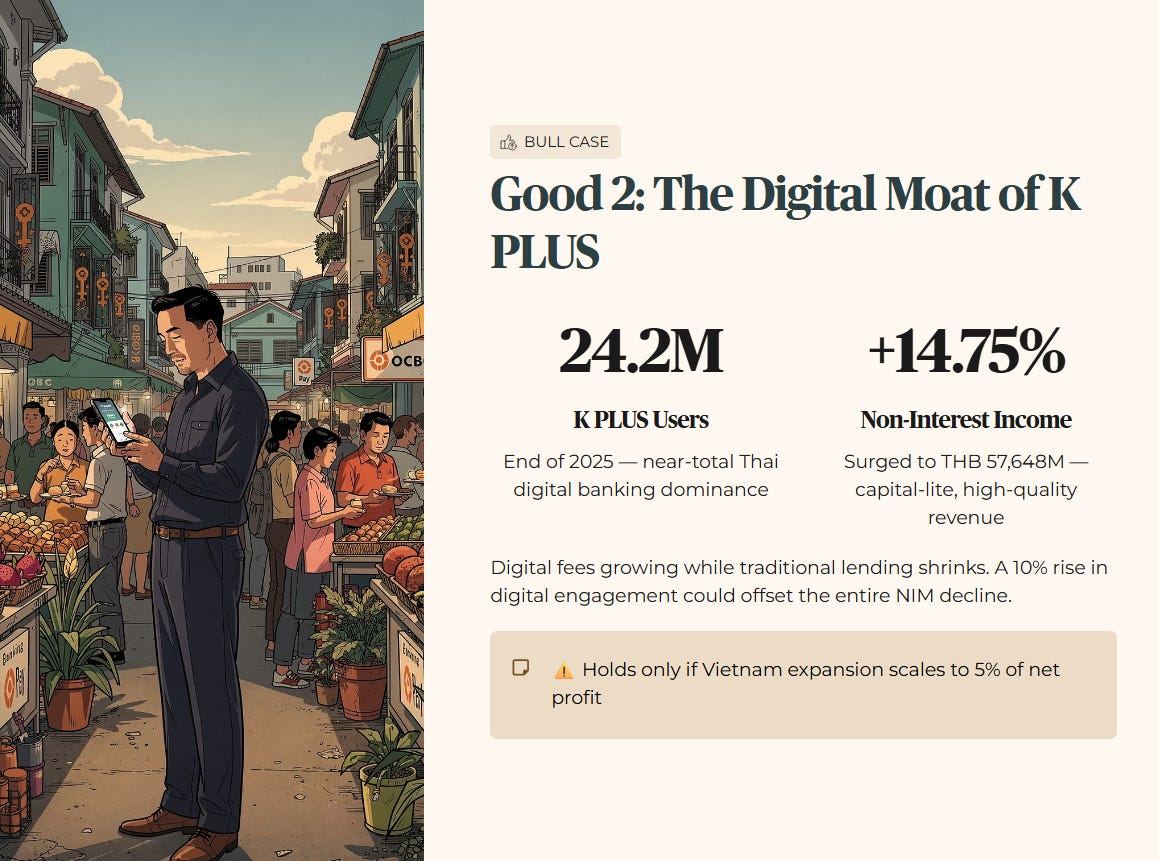

Good 2: The Digital Moat of K PLUS

Good 3: Superior NPL Coverage and Provisioning

The 3 Red Flags (The Bear Case)

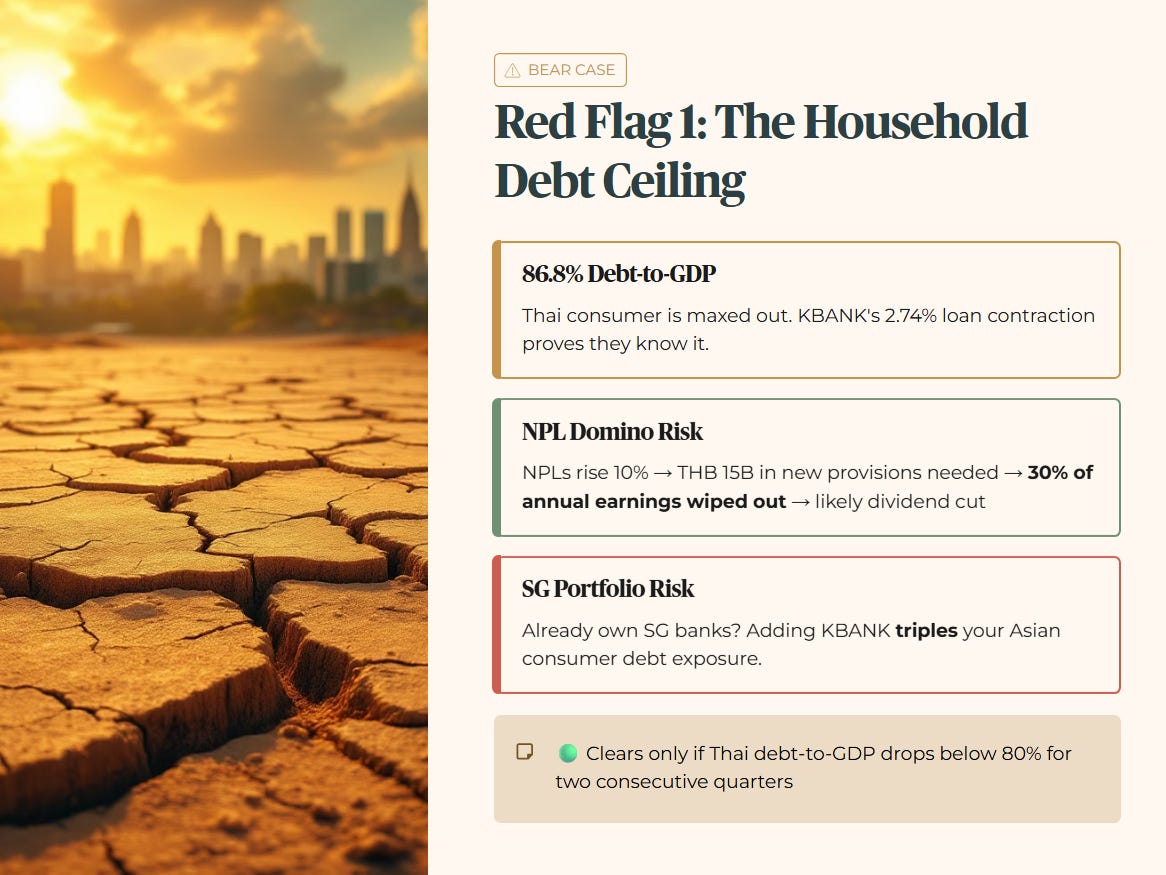

Red Flag 1: The Household Debt Ceiling

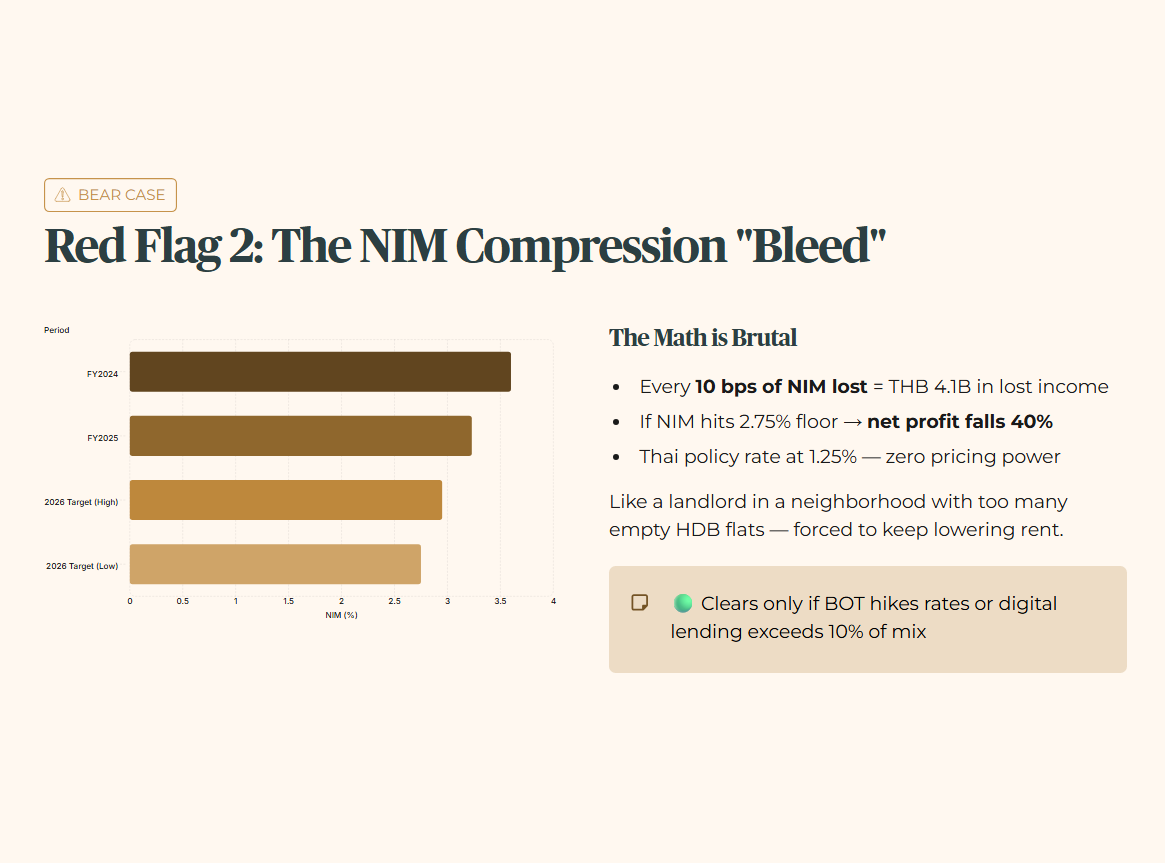

Red Flag 2: The NIM Compression “Bleed”

Red Flag 3: External Trade and Tariff Vulnerability

The Singaporean Context (The Local Lens)

The Weighing Scale

Iggy’s Take: The Honest Verdict

InvestingPro Reality Check

Iggy's Verdict

Elite Authority Break

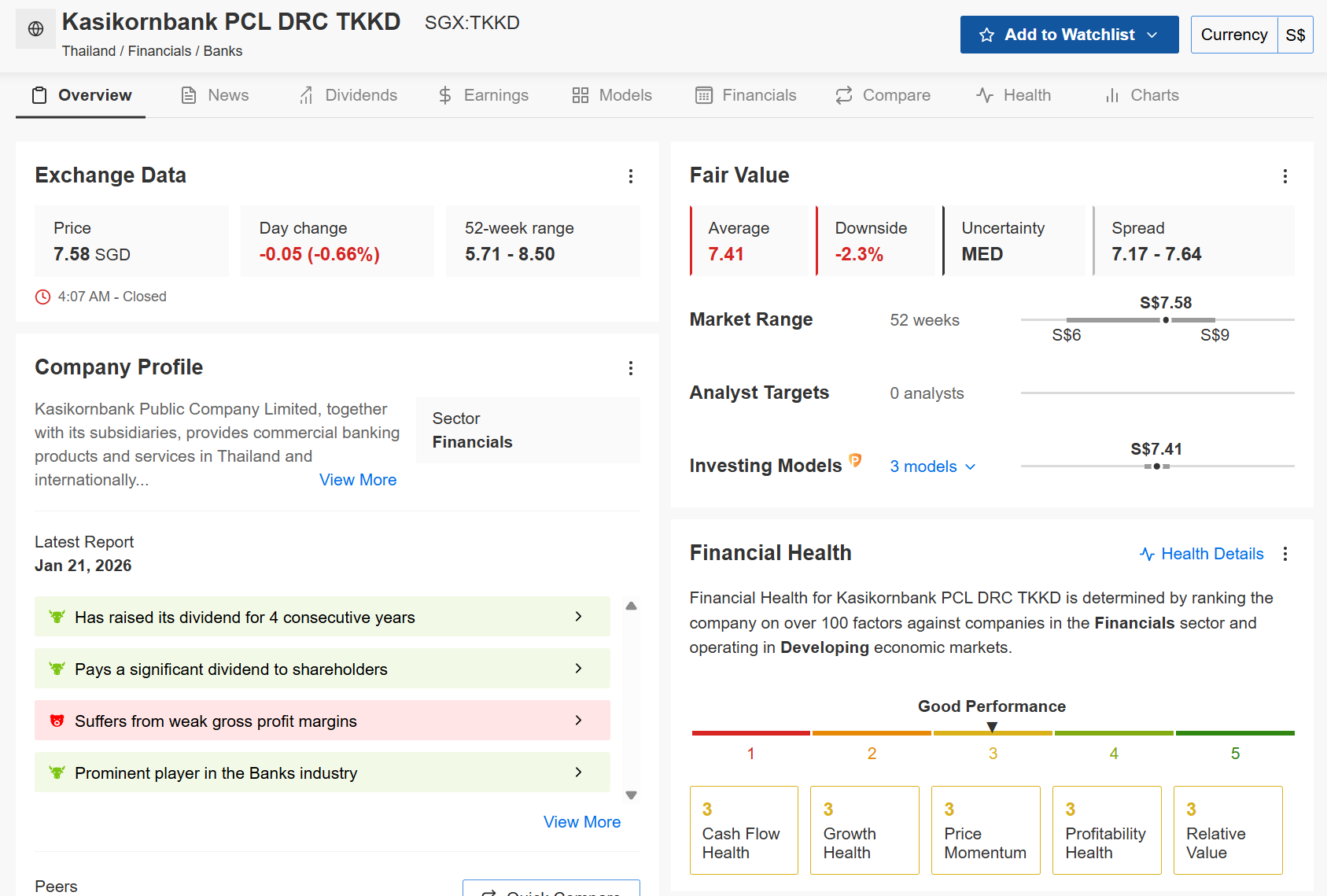

You are reading a forensic audit shared with 190 private members of the Iggy community. Today, we cover Kasikornbank (KBANK) — Thailand’s second-largest bank by assets, and one of the few Thai stocks accessible to Singapore investors via SGX as a Singapore Depositary Receipt (SDR: SGX:TKKD). We don’t look at the glossy annual report covers; we look at the debt maturity schedules and the yield spreads that the mainstream media ignores.

The Financial Snapshot (The Baseline)

To understand KBANK, you must first understand that this is no longer a “growth” bank; it is a “preservation” bank. The latest fiscal performance submitted on February 26, 2026, shows a net profit of THB 49,565 million. On paper, that looks stable compared to the prior year, but the “how” matters more than the “how much.”

The bank’s total assets grew by 5.01% to THB 4.56 trillion, yet net loans actually contracted by 2.74%. This is a massive forensic signal. KBank is intentionally turning away borrowers to park cash in low-risk investments. Why? Because the Thai consumer is tapped out. With household debt at 86.8% of GDP, the bank is choosing to shrink rather than risk a blow-up.

Financial Health Baseline

The metric that most encourages me is the CET1 Ratio of 18.00%. In forensic terms, this is a “Fortress” level of capital. It means for every dollar of risk, the bank has a massive stack of pure equity sitting in the vault. However, the metric that concerns me most is the 10.28% drop in NIM. When your core margin drops from 3.60% to 3.23% in a single year, your engine is losing oil.

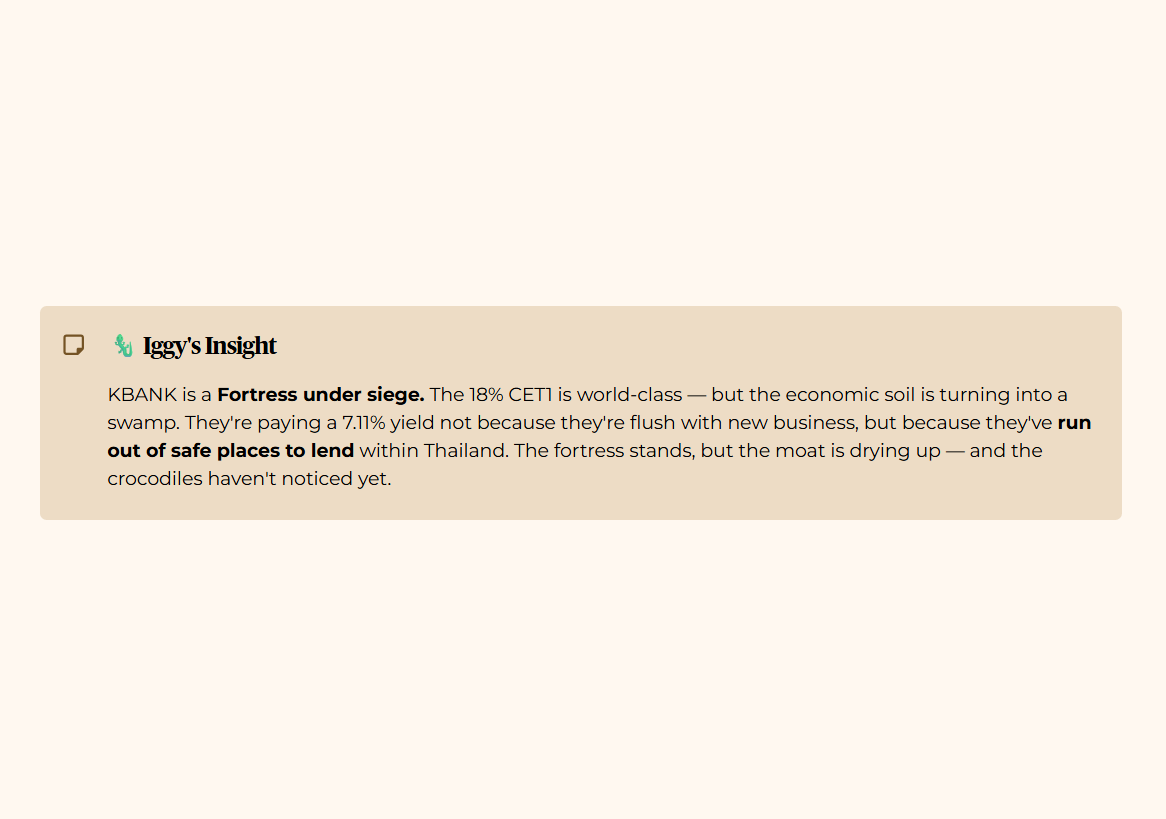

🦎 Iggy’s Insight

KBANK is currently a Fortress under siege. Management has built a massive wall of capital—that 18.00% CET1 ratio is world-class—but the surrounding economic soil is turning into a swamp. They are paying out a 7.11% yield not because they are swimming in extra cash from new business, but because they’ve run out of safe places to lend it within Thailand. It’s a strategic retreat disguised as a dividend bonanza. The fortress is standing, but the moat is drying up—and the crocodiles have not noticed yet.

The 3 Good (The Bull Case)

Good 1: The “Kopitiam King” Yield and Payout Pivot

The strongest bull argument is the dividend yield, which currently sits at 7.11%. Historically, KBANK was stingy, but they have pivoted to a progressive payout policy. In 2025, the bank paid out THB 12.00 per share, representing a 66.67% increase over the previous year.

Compared to Singapore peers like DBS (4.96%) or OCBC (4.89%), KBANK offers a massive premium. For a Singaporean investor, this is like finding a hawker stall selling Michelin-star chicken rice for $2.50—it feels too good to be true, but the math checks out because the bank’s Dividend Payout Ratio has climbed to 60.0%. If conditions improve by 10% and fee income accelerates, we could see the yield touch 8%. If they deteriorate 10%, the bank’s capital buffer is so thick it could likely maintain the current THB 12.50 payout for at least two years without sweating.

“I don’t just guess at valuations. I check the institutional models.” Source: InvestingPro Data. Unlock these institutional tools for your own portfolio: Use code INVESTINGIGUANA for an exclusive 50% Discount.

🏛️ [Claim Your 50% Discount Here]

Forensic Caveat: This bull case only holds if the CET1 ratio remains above 15% to satisfy Bank of Thailand regulators.

Good 2: The Digital Moat of K PLUS

KBank isn’t just a bank; it’s the dominant digital ecosystem in Thailand. The K PLUS user base reached 24.2 million at the end of 2025. In Singapore terms, imagine if one bank’s app was used by nearly every single person from Jurong to Pasir Ris for everything from buying 4D to paying for groceries.

This digital dominance allowed non-interest income to surge 14.75% to THB 57,648 million. This “capital-lite” revenue is the holy grail. While traditional lending is shrinking, digital fees are growing. If digital engagement increases by 10%, fee income could offset the entire decline in interest margins. For a 50+ investor, this digital lead is the insurance policy against the death of traditional banking. It ensures the bank stays relevant even as the neighborhood “uncles” start using QR codes for everything.

Forensic Caveat: This bull case only holds if regional expansion into Vietnam successfully scales to 5% of net profit.

Good 3: Superior NPL Coverage and Provisioning

While the “bad” news is that loans are risky, the “good” news is that KBANK is a pessimist. Their NPL Coverage Ratio rose to 162.75% in 2025. This means for every $1 of potentially bad loans, they have $1.62 set aside.

Compared to the sector benchmark of 150%, KBANK is being extra cautious. This is like a Singaporean family keeping two years of expenses in their CPF Ordinary Account “just in case.” If the economy improves 10%, the bank can “write back” these provisions, creating a massive one-time profit spike. For the investor, this means the current 0.80x P/B ratio provides a significant margin of safety. You are buying the bank’s assets for 80 cents on the dollar, while getting a 162% safety net on the bad stuff.

Forensic Caveat: This bull case only holds if the gross NPL ratio stays below the 3.50% threshold.

The 3 Red Flags (The Bear Case)

Red Flag 1: The Household Debt Ceiling

The most dangerous risk is the 86.8% household debt-to-GDP ratio in Thailand. The Thai consumer is maxed out, and KBANK’s 2.74% loan contraction proves they know it.

So what does this mean for you? If refinancing becomes difficult for Thai families, NPLs won’t just stay at 3.20%; they will spike. If NPLs rise by just 10% (to roughly THB 103 billion), the bank would need to find THB 15 billion in new provisions. This would wipe out 30% of your annual earnings and likely force a dividend cut. For a Singaporean portfolio, this represents a major concentration risk. If you already own SG banks, adding KBANK triples your exposure to “Asian Consumer Debt.”

Forensic Condition: This red flag clears only if Thai debt-to-GDP drops below 80% for two consecutive quarters.

Red Flag 2: The NIM Compression “Bleed”

The bank is facing a severe margin squeeze. Management’s 2026 target for Net Interest Margin is 2.75% to 2.95%, down from 3.23%. This is a potential 48 basis point drop.

In the banking world, 48 basis points is not a “trim”; it’s a “haircut.” For every 10 bps of NIM lost, interest income drops by THB 4.1 billion. If the bank hits the bottom of their target (2.75%), net profit could fall by 40%. And let’s be honest, they are not wrong to be worried. With the Thai policy rate at 1.25%, the bank has no “pricing power.” They are like a landlord in a neighborhood with too many empty HDB flats—they have to keep lowering the rent just to keep the tenants.

Forensic Condition: This red flag clears only if the Bank of Thailand begins a rate-hiking cycle or digital lending exceeds 10% of the mix.

Red Flag 3: External Trade and Tariff Vulnerability

KBANK is a proxy for the Thai economy, and the Thai economy is a proxy for global trade. With US tariffs looming in 2026, Thailand’s export-heavy manufacturing sector is in the crosshairs. Manufacturing loans make up 28% of the corporate book.

If Thai exports contract by 5%, these corporate borrowers will struggle. A mere 50 bps rise in corporate credit costs would eat THB 12 billion in profit. For a retiree in Toa Payoh, this is the “silent killer.” You think you are buying a local bank, but you are actually betting on the US-China trade war. If the global trade environment worsens by 10%, KBANK’s capital buffers will be tested, not for growth, but for survival.

Forensic Condition: This red flag clears only if Thai export growth to non-US markets exceeds 15% YoY.

The Singaporean Context (The Local Lens)

For a Singaporean investor, the decision to hold KBANK isn’t just about the bank; it’s about the Yield Spread.

At 602 basis points, you are being paid a massive premium. But remember: KBANK is NOT CPFIS or SRS eligible. You have to use hard cash.

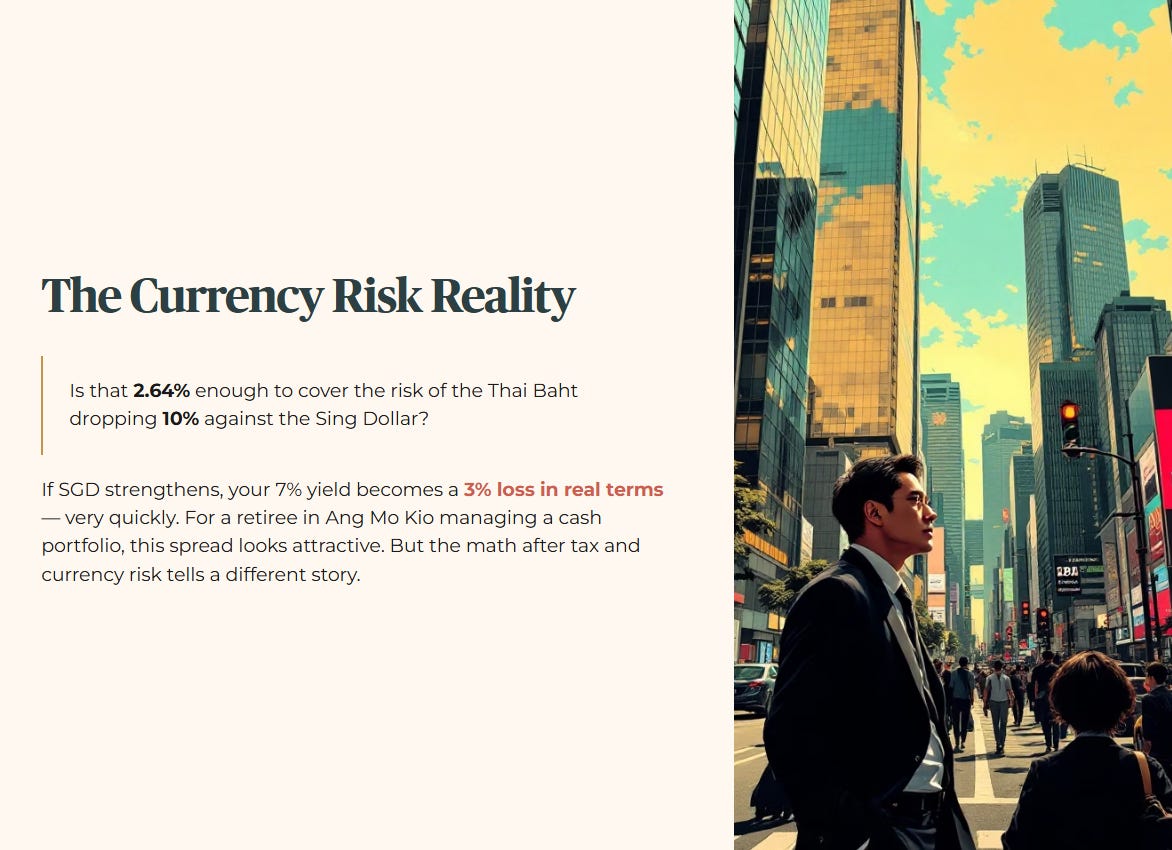

For a retiree in Ang Mo Kio managing a cash portfolio, this spread looks like a “must-buy.” However, apply the Five-Layer Rule to that yield. You must subtract the 10% Thai Withholding Tax, bringing your net yield to 6.64%. Then, compare it to the 4.0% risk-free rate of the CPF Special Account. You are taking “Emerging Market” risk for a net “extra” return of only 2.64%.

Is that 2.64% enough to cover the risk of the Thai Baht dropping 10% against the Sing Dollar? Probably not. If the SGD strengthens, your 7% yield becomes a 3% loss in real terms very quickly.

Here’s the exact 2-trigger checklist (NIM + household debt) I use to decide whether KBANK is a “7% trap” or a rare Thailand recovery payout—and the one number that would flip my verdict immediately.