STI Hits 5,000 While Catalist Credit Risk Rises (SGX Daily Pulse 13 Apr)

Streats and Sukhothai are familiar, but the auditor’s report is more sour than tom yum. Don't play play with debt.

Daily Pulse: SGX Digest, April 13, 2026

The STI flirts with 5,000 while T-bill yields collapse to 1.47%, widening the forensic gap for income hunters.

The market moves at two speeds: a headline index testing all-time highs near 5,000 and a credit reality where Catalist minnows are drowning in net liabilities.

In This Article:

Market Snapshot

The Audit SGX Forensic Triage

Insight 1 Katrina Group SGX 1A0

Insight 2 CapitaLand Investment SGX 9CI

Insight 3 Hospitality REITs Sector View

Watchlist and Yield Spread

Iggy’s Take The Bottom Line

Iggy’s Forensic Compliance Standards Standard Disclaimer

Market Snapshot

Verdict: The STI is at record highs, but the safety of lazy capital in T-bills has evaporated, forcing investors back into the risk-premium hunt.

MetricLevelIggy ContextSTI Level4,968.80Testing the 5,000-point psychological ceilingCSOP iEdge S-REIT Leaders ETF (SRT)S$0.742 (11 Apr proxy — index level unavailable)ETF proxy only; live index level not retrievableT-Bill (6-Month, BS26107X)1.47%Significant drop from previous cyclesRequired Alpha3.23%Gap between T-bill and Iggy’s 4.7% Hurdle

The Audit: SGX Forensic Triage

1. Katrina Group (SGX: 1A0): Yield Trap Alert

Verdict: The auditor’s ink is redder than the balance sheet, signalling a business model that consumes more capital than it produces.

Layer 1: Raw Fact. EY issued a going concern warning for Katrina Group (report dated 10 April 2026). Net liabilities exceed net assets by S$6.7 million. Current liabilities exceed current assets by S$18.4 million. The going concern status hinges on a director letter of undertaking not to recall advances, valid for 15 months from the FY2025 financial statement date.

Layer 2: Benchmark. The negative P/B ratio, confirmed at negative 1.03x to negative 1.29x, is a total breach of the Fortress Balance Sheet standard. It marks a severe decline from the three-year historical baseline of marginal survival.

Layer 3: Peer Context. Compared to Kimly (SGX: 1D0), which maintains a net cash position and positive operating cash flow, Katrina is trapped behind the Debt Wall.

Layer 4: Forward Scenario. A 10% decline in foot traffic at core F&B outlets would likely exhaust remaining liquidity. The quantified impact is total capital impairment. The macro trigger is the sustained elevation of heartland commercial rents.

Layer 5: Wallet Impact. Consider the Ang Mo Kio archetype: a 65-year-old drawing CPF LIFE payouts and holding legacy F&B penny stocks. The consequence is a total write-off of invested principal if restructuring fails. Forensic Stance: Yield Trap.

Insight 1 — Katrina Group (SGX: 1A0)

Iggy’s Insight: The Going Concern Decoy A share price down 20.6% in a single session looks like a buying opportunity to someone running on hope instead of forensics. It is not. When net liabilities exceed net assets by S$6.7 million and the only thing keeping the lights on is a director’s personal letter of undertaking, you are not buying a recovery — you are funding someone else’s exit. Kimly runs a cleaner balance sheet selling chicken rice. Katrina runs a deficit selling the same. The forensic conclusion writes itself.

Forensic Punchline: The cheapest stock in the room is often the most expensive mistake you will ever make.

Verdict: When the auditor flags survival risk, the cheap share price is a decoy for a total loss event.

2. CapitaLand Investment (SGX: 9CI)

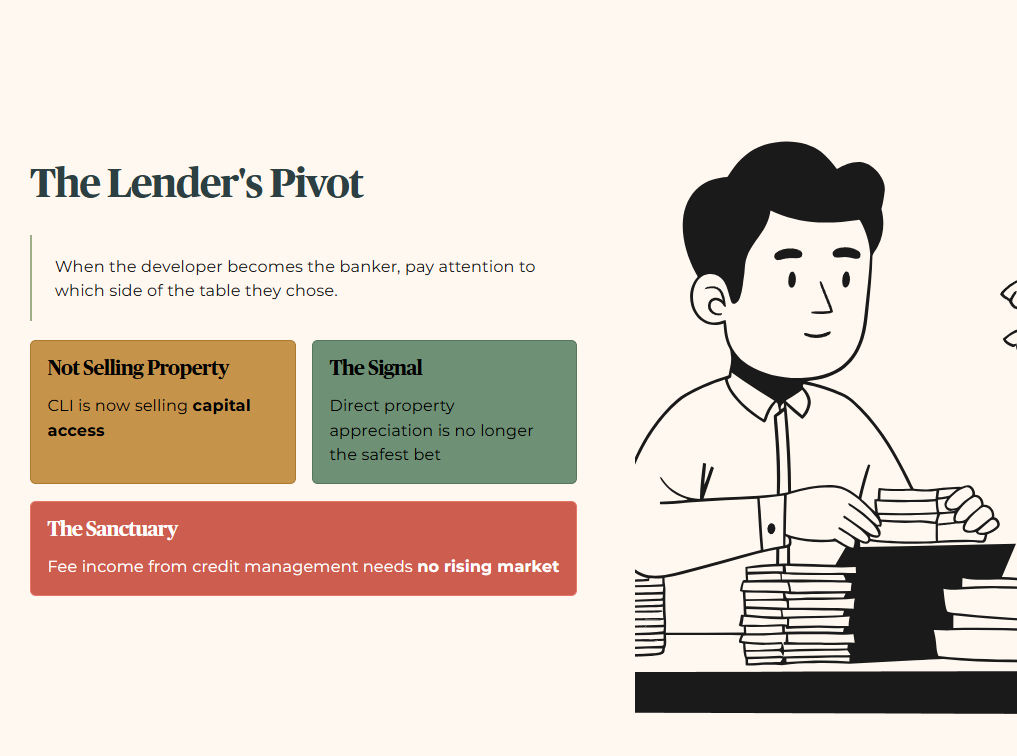

Verdict: CLI is pivoting into real estate credit as a service, leveraging its US$600M FUM expansion.

Raw Fact. CLI achieved a final close of US$320 million for its ACP II fund, which finances first mortgage loans for logistics and office assets in Sydney and Seoul.

Wallet Impact. For a 45-year-old Clementi HDB owner with a dividend portfolio, CLI’s shift to asset-light credit management provides a fee-income Sanctuary. It does not rely on direct property appreciation. Strategic Neutral.

Insight 2 — CapitaLand Investment (SGX: 9CI)

Iggy’s Insight: The Lender’s Pivot CLI is not selling property anymore — it is selling capital access. The ACP II final close at US$320 million tells you something important: when one of Asia’s largest real estate groups pivots into first mortgage lending against logistics and office assets in Sydney and Seoul, they are signalling that direct property appreciation is no longer the safest bet in the room. Fee income from credit management does not require a rising market. For the income investor, that is the Sanctuary characteristic worth tracking.

Forensic Punchline: When the developer becomes the banker, pay attention to which side of the table they chose.

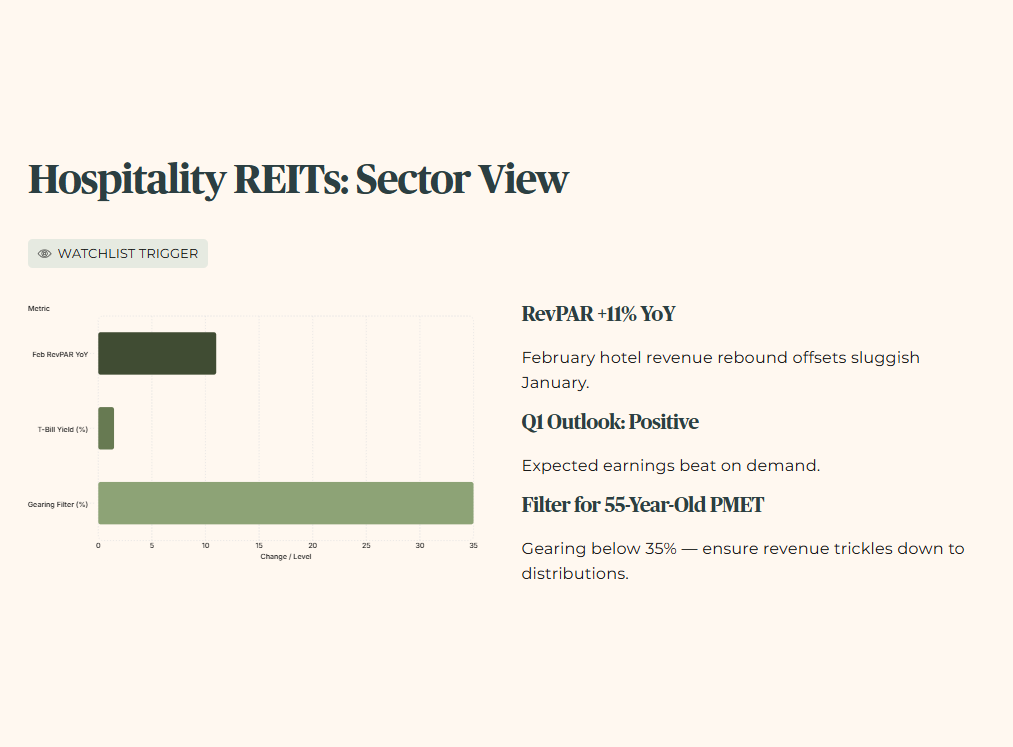

3. Hospitality REITs (Sector View)

Verdict: RevPAR is the engine room of the hospitality recovery, but a high ICR remains the gatekeeper.

Raw Fact. Hospitality REITs are eyeing Q1 earnings beats following an 11% year-on-year jump in February hotel revenue, offsetting a sluggish start to the year.

Wallet Impact. A 55-year-old Bedok PMET approaching retirement should use this RevPAR strength to filter for trusts with gearing below 35%, where the revenue trickles down to distributions. Watchlist Trigger.

Insight 3 — Hospitality REITs (Sector View)

Iggy’s Insight: RevPAR Is Not a Dividend An 11% year-on-year jump in February hotel revenue is a strong operating signal, but RevPAR flows to distributions only after gearing costs, management fees, and refinancing obligations are settled first. With T-bills at 1.47%, the temptation to rotate from cash into hospitality REITs is real — but the filter must still be gearing below 35% and an ICR that can absorb a rate reversal. Revenue momentum without balance sheet discipline is just a nicer way to walk into a Yield Trap.

Forensic Punchline: A full hotel means nothing if the mortgage payment arrives before the distribution does.

Iggy’s Insight: The T-Bill Trap

The collapse of the 6-month T-bill yield to 1.47% is a massive MRT Door Paradox: everyone was rushing into safe cash when yields were at 3.7%, but now the doors are closing and the yield is halved. For the income investor, this widens the Forensic Gap. You now need 323 basis points of alpha just to hit my 4.7% hurdle.

This is where people get desperate and buy Yield Traps like Katrina Group just because they are cheap. Do not do it. A 1.47% T-bill is boring, but a going concern warning is a heartland horror story.

Forensic Punchline: A low yield is a headache. A zero-equity restructuring is a funeral.

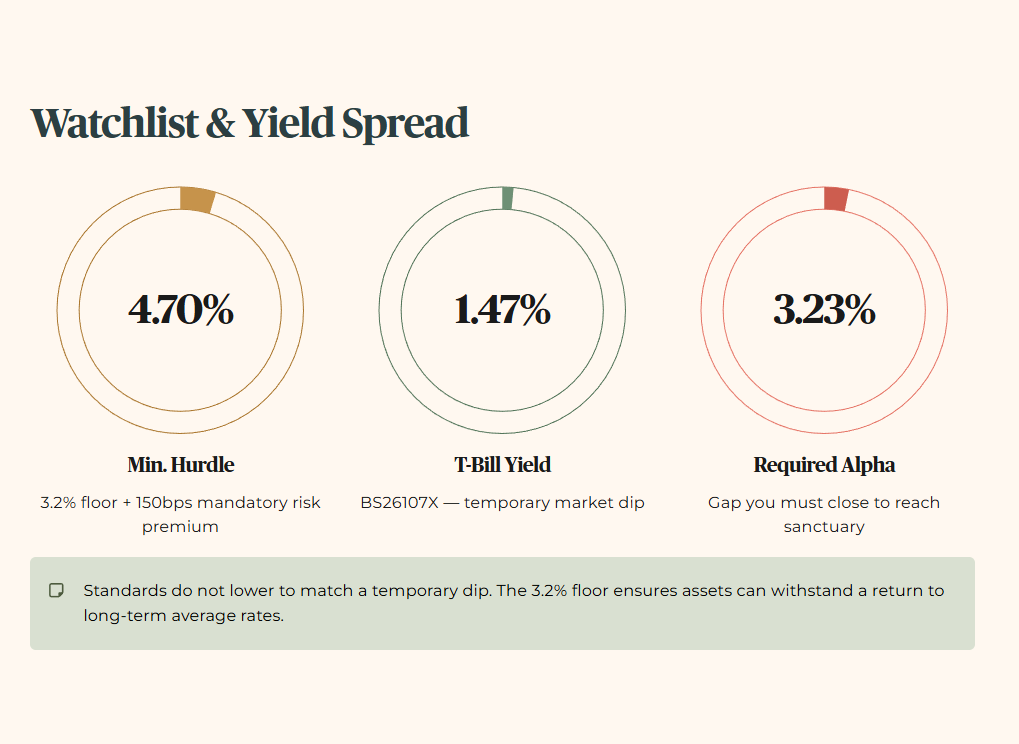

Watchlist and Yield Spread

4.70% (Min. Hurdle) minus 1.47% (T-Bill BS26107X) = 3.23% Required Alpha.

For this audit, I apply a conservative floor of 3.2%. We audit for the storm, not just the sunny day. While the T-bill sits at 1.47%, I do not lower my standards to match a temporary market dip. My floor remains at 3.2% to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7%. That is the 3.2% floor plus 150 basis points of mandatory risk premium.

Iggy’s Take: The Bottom Line

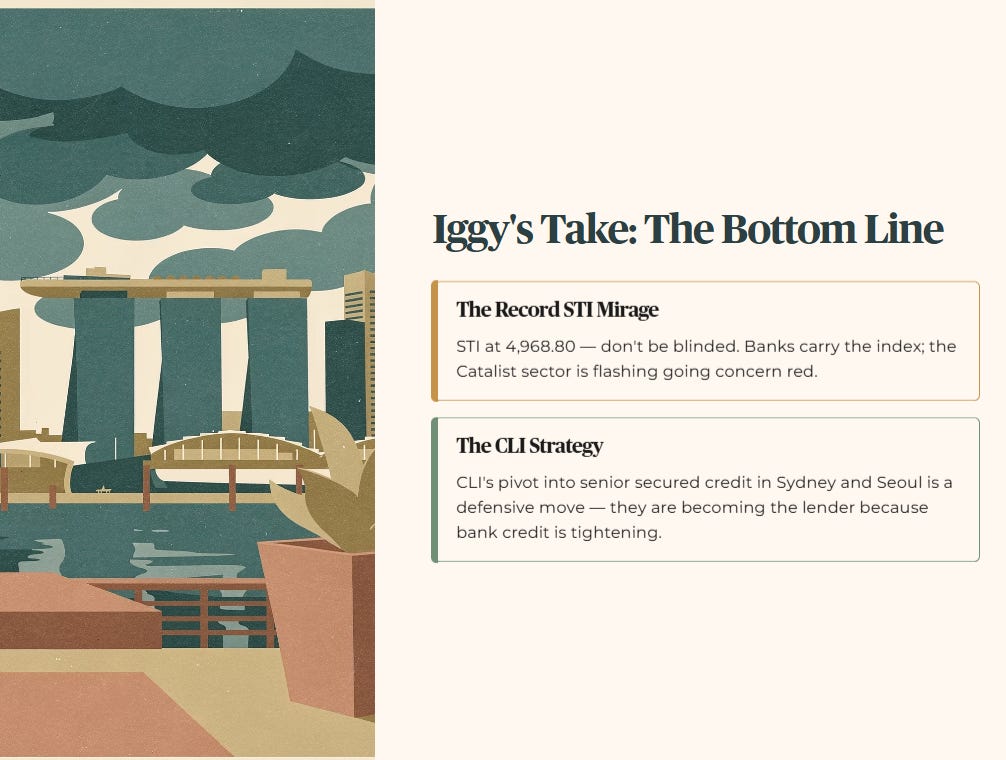

The Record STI Mirage. Do not let the STI at 4,968.80 blind you to the credit stress in the micro-cap space. The banks carry the index, but the Catalist sector is flashing going concern red.

The CLI Strategy. CapitaLand Investment’s move into senior secured credit in Sydney and Seoul is a defensive pivot. They are becoming the lender because they know bank credit is tightening.

Recalculated Risk. With T-bills at 1.47%, your required alpha is now 3.23%. If your REIT or dividend play is not yielding at least 4.7% with a clean balance sheet, you are taking equity risk for T-bill returns.

Neighbourhood Pairing. Over at the Yishun coffee shop, the 50-year-old managing SRS and CPF SA simultaneously needs to understand that cheap does not mean value. Buying into a net-liability name like Katrina is like buying a FairPrice house brand item where the expiry date was yesterday.

Is your portfolio anchored in cash-flow reality, or are you just riding a headline index high?

The higher the STI climbs, the harder the forensic audit must strike.

The Window Is Already Open

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

Iggy’s Forensic Compliance Standards — Standard Disclaimer

This content is produced for educational and informational purposes only. I am not a financial advisor — I am a retail investor who applies forensic analysis to my own portfolio and shares that process publicly. Nothing here constitutes a recommendation to buy, sell, or hold any security, and no specific target prices or personalised financial advice are offered. All data is sourced from public filings and verified sources; where data is unverified it is explicitly flagged. All investments carry risk, including the potential loss of principal, and past performance is not indicative of future results. If you are making investment decisions involving CPF, SRS, or personal capital, please conduct your own due diligence or consult a MAS-licensed financial adviser before committing funds.