StarHub $115M Deal and the 5.74% Yield Floor | SGX Daily Pulse 16 Apr 2026

Keppel DC gives a 13% "pay raise" but the debt wall is rising faster than hawker prices.

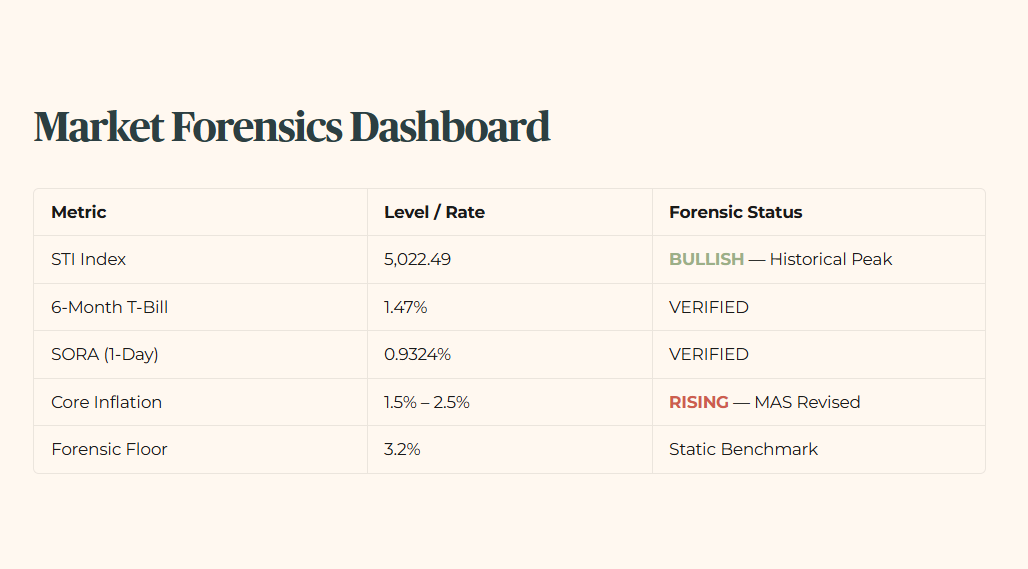

Yield is a liability if it does not outrun inflation. With MAS revising core inflation forecasts to 2.5%, the 4.7% Yield Hurdle is no longer a suggestion. It is a survival metric. Today we audit whether Keppel DC REIT’s 13.2% jump is a true sanctuary or just a temporary peak.

In This Article:

Counter 1 Keppel DC REIT

Box 1 The AI Rent Escalator

Counter 2 StarHub

Box 2 The Temasek Hand off

Counter 3 Yangzijiang Shipbuilding

The Window Is Already Open

The Bottom Line

Iggys Forensic Compliance Standards Standard Disclaimer

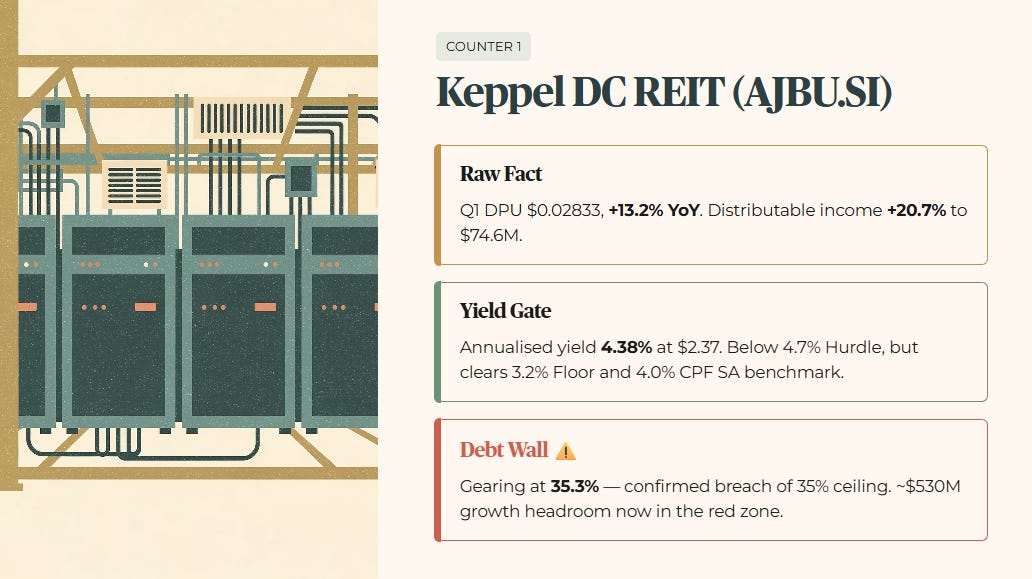

Counter 1: Keppel DC REIT (AJBU.SI)

Layer 1 (Raw Fact): Q1 DPU of $0.02833, up 13.2% YoY. Distributable income rose 20.7% to $74.6M.

Layer 2 (Yield Gate): Annualised yield is 4.38% at the $2.37 live price. This falls short of the 4.7% Yield Hurdle but clears the 3.2% Forensic Floor and remains above the 4.0% CPF SA Sanctuary benchmark.

Layer 3 (The Debt Wall): At 35.3%, gearing has officially breached the 35% Forensic Triage ceiling. This is a confirmed breach, not a technicality, and requires immediate scrutiny on capital recycling capacity. The manager carries roughly $530M in growth headroom, but that buffer is now operating inside the red zone.

Layer 4 (Forward Scenario): A 10% hike in energy costs driven by the fuel crisis could pressure NPI. The partial offset: 45% portfolio reversions in FY25 confirm strong pricing power to pass costs to hyperscalers.

Layer 5 (Wallet Impact): For a retiree in Tanjong Pagar using dividends for monthly conservancy fees, a 13.2% DPU bump comfortably outpaces the 2.5% inflation ceiling. This does not merely preserve purchasing power — it actively grows it, widening their safety margin for the year.

Box 1: The AI Rent Escalator

Keppel DC REIT’s 45% rental reversion is not a fluke. It is the AI Tax in action. Hyperscalers need the space, and Keppel has the power capacity. Even with a yield of 4.38%, sitting just below the Iggy Hurdle, the counter’s role as a long-term Sanctuary is bolstered by DPU growth running nearly five times the current inflation forecast. The confirmed gearing breach at 35.3% is the counter-weight that cannot be ignored. Strong income growth on one side, a balance sheet in the red zone on the other.

Forensic Punchline: Sometimes you pay a premium for a moat that actually works — just make sure the drawbridge is still up.

Counter 2: StarHub (CC3.SI)

Layer 1 (Raw Fact): Ceding majority control of Ensign InfoSecurity to Temasek for $115M, booking a $200M fair-value gain by 2026.

Layer 2 (Yield Gate): At the $1.08 live price, TTM dividend yield is 5.74%. This clears both the 3.2% Forensic Floor and the 4.7% Yield Hurdle decisively.

Layer 3 (Risk Audit): Exiting the cybersecurity majority stake narrows the enterprise moat. If core telco and broadband margins face pricing wars, fewer adjacent revenue pillars remain to absorb the shock.

Layer 4 (Forward Scenario): The $115M cash injection provides a buffer. The stress-test question is execution: will management recycle this capital into higher-yielding 5G infrastructure, or return it to shareholders via special dividends to defend the 5.7% yield floor?

Layer 5 (Wallet Impact): For a 50+ investor in Bedok, this is a de-risked balance sheet play. The cash injection supports redeployment into core 5G and broadband, and the yield holds well above the forensic threshold for now.

Box 2: The Temasek Hand-off

StarHub’s $115M deal with Temasek is a capital discipline move that retail investors often read too quickly. By booking a $200M fair-value gain, management is clearing the path for a leaner FY2026. A 5.74% yield that clears the forensic hurdle makes this worth watching. The real question is not what they sold — it is what they do with the proceeds. Cash on the balance sheet is only as good as the decision-making behind it.

Forensic Punchline: In a high-inflation environment, cash is a better weapon than a complex subsidiary — but only if management knows how to use it.

Counter 3: Yangzijiang Shipbuilding (BS6.SI)