Keppel DC REIT FY2025 Results: Real AI Growth or Just Hype?

Revenue is up 42%, DPU hit double digits, and portfolio reversions are a staggering 45%. But with leverage ticking up, is the growth priced in?

The Data Centre Giant Delivers a +9.8% DPU Jump. Here is the Reality Check.

Revenue is up 42%, DPU hit double digits, and portfolio reversions are a staggering 45%. But with leverage ticking up, is the growth priced in?

Download the Results Presentation Here:

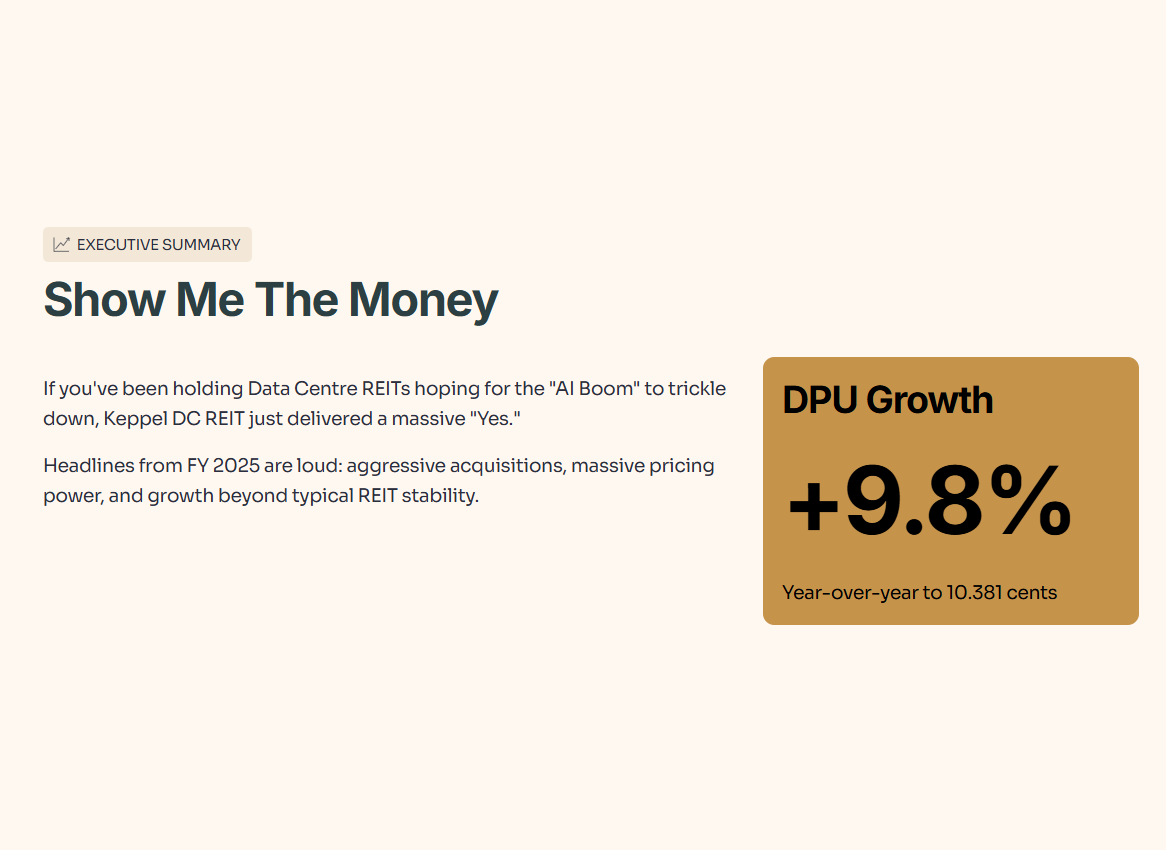

The Executive Summary: “Show Me The Money”

If you’ve been holding Data Centre REITs hoping for the “AI Boom” to trickle down into your dividend, Keppel DC REIT (KDCREIT) just slapped a massive “Yes” on the table.

The headlines from the FY 2025 Financial Results (dated 30 Jan 2026) are loud. We aren’t just seeing “stable” boring REIT growth here; we are seeing growth fueled by aggressive acquisitions and massive pricing power.

Here is the one number that matters most to your wallet: DPU is up 9.8% year-on-year to 10.381 cents.

Let’s tear apart the slides to see how they did it, and more importantly, if they can keep doing it.

Table of Contents

- Executive Summary

- About Iggy

- Membership Options

- Financial Results (P&L)

- Balance Sheet Highlights

- Valuation Insights

- Pricing Power & Portfolio Metrics

- AI Demand Outlook

- Iggy’s Scorecard

- Strategic Question

- Final Thoughts

- Disclaimers🦎 About Iggy & The “Elite 150”

Welcome to the Pit! I’m Iggy, your guide through the Singapore market jungle. We are 5,800+ subscribers strong, hunting the alpha that mainstream media misses.

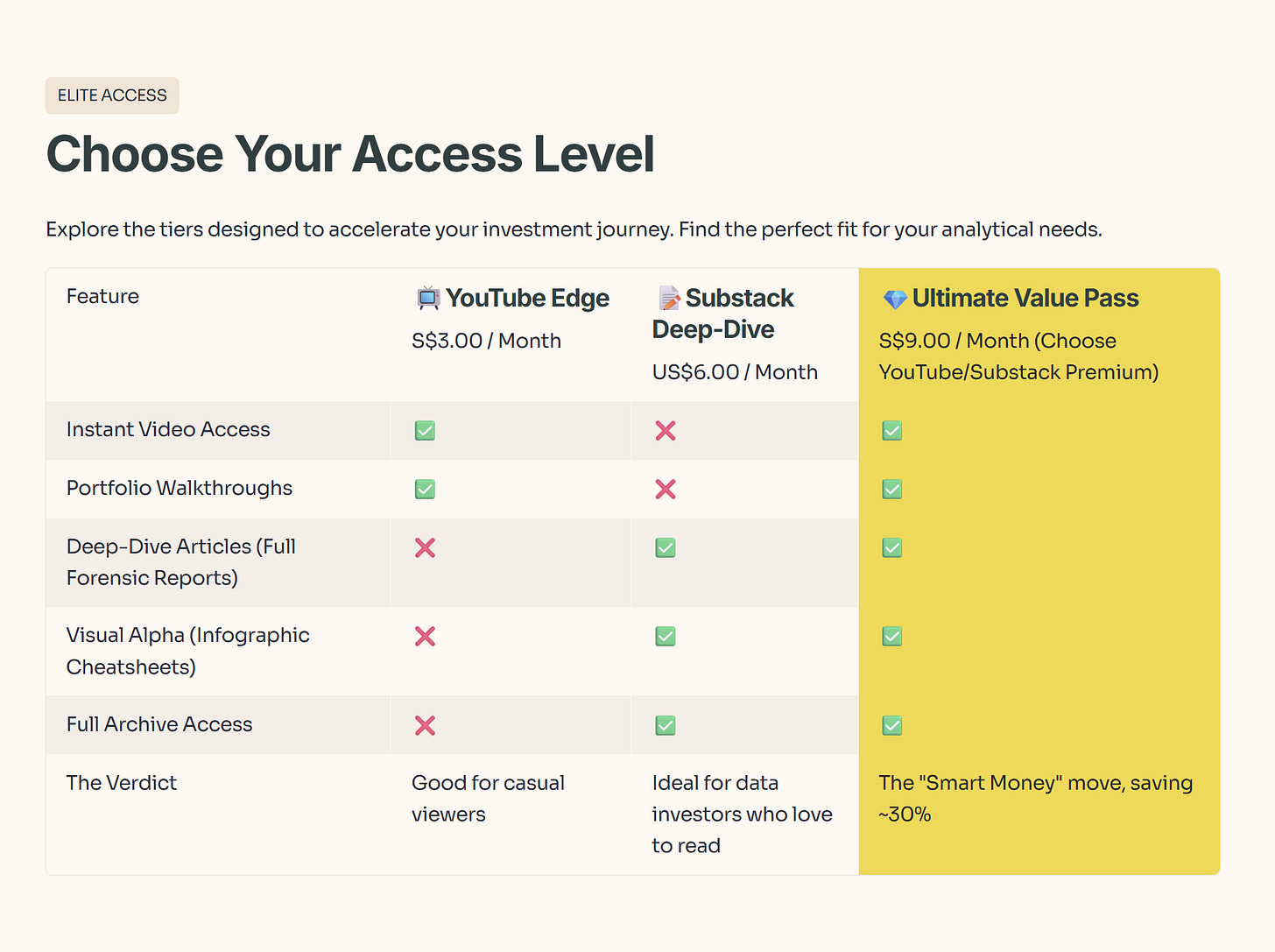

🚨 Stop Waiting 14 Days for “Old News” Free subscribers wait 2 weeks to see my videos. By then, the trade is often gone.

Join the 150+ Members in the Inner Circle:

⚡ Instant Access: Watch videos the moment they drop.

📝 The Full Vault: Unlock deep-dive articles & infographics.

💎 The “Smart Money” Move: Get the S$9/mo Bundle (YouTube + Substack) and save ~30%.

Get the data while it’s fresh. 👉 Join the Inner Circle Here

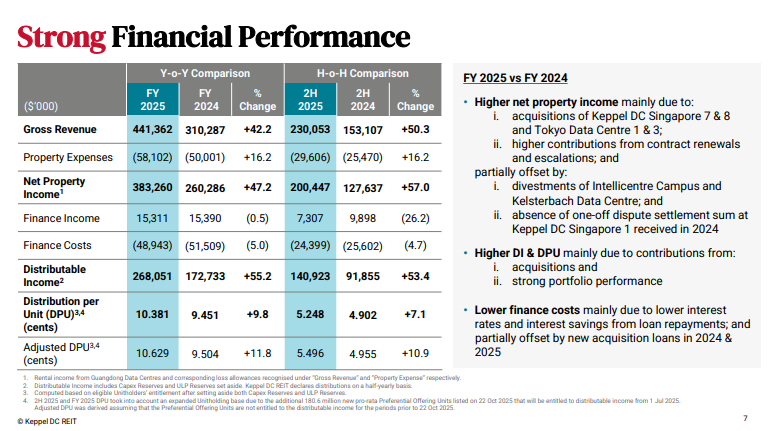

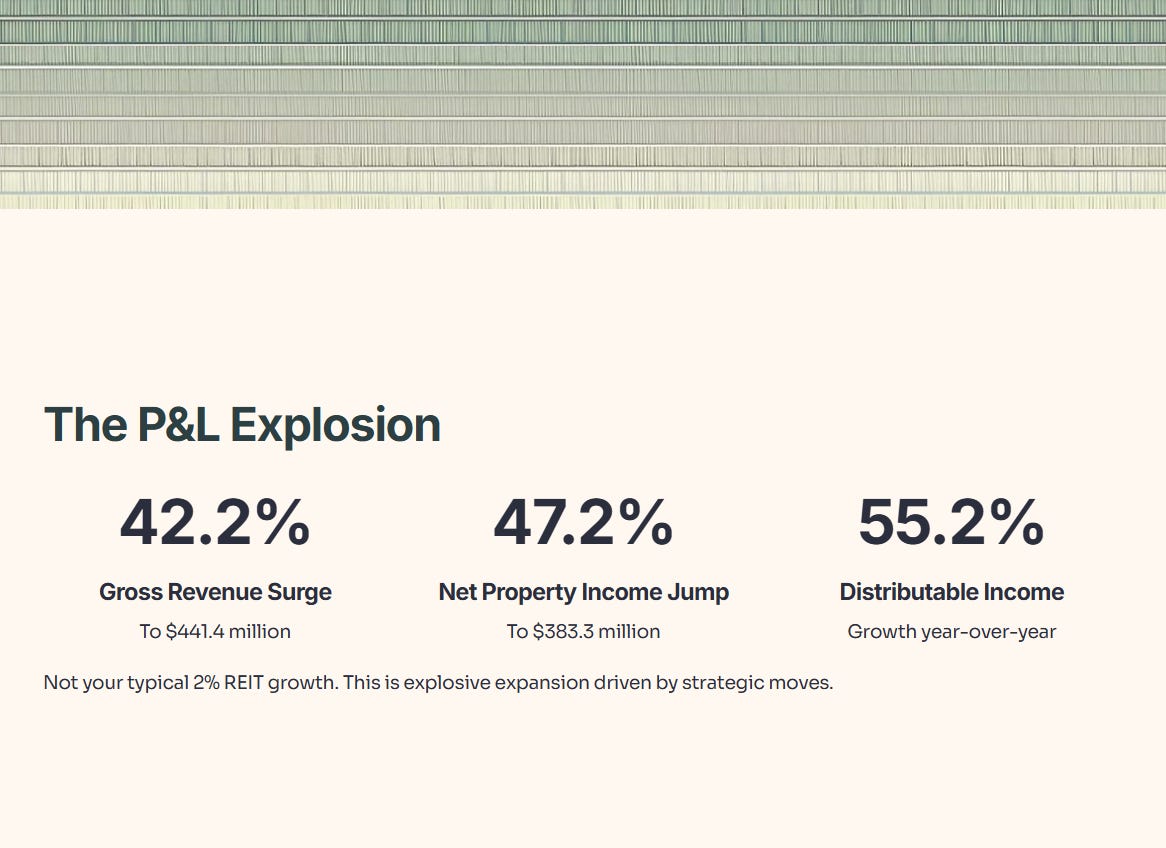

Slide 7: The P&L “Explosion”

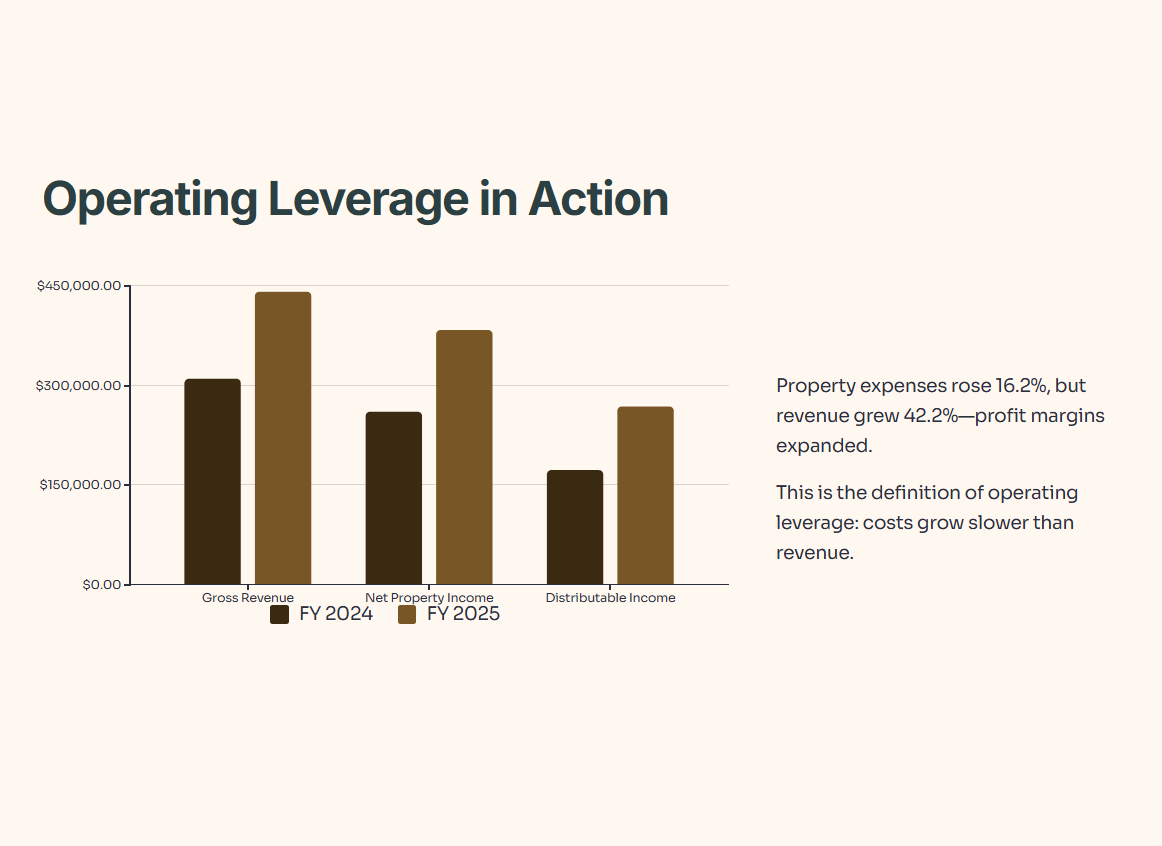

Usually, when I look at REIT results, I’m squinting to see a 2% rise in revenue. Not today. KDCREIT reported a Gross Revenue surge of 42.2% to $441.4 million.

Net Property Income (NPI) followed suit, jumping 47.2% to $383.3 million.

Why the massive jump? It wasn’t magic. It was a combination of opening the wallet and tightening the screws on existing tenants:

Acquisitions: The numbers were pumped by the purchase of Keppel DC Singapore 7 & 8 and Tokyo Data Centre 1 & 3.

Organic Growth: They squeezed higher contributions from contract renewals and escalations.

However, we need to respect the “Double-Entry Rule.” You can’t have revenue growth without cost growth. Property Expenses rose 16.2%, but since revenue grew much faster (42.2%), the profit margins actually expanded. That is the definition of operating leverage.

Iggy’s Take: The Distributable Income grew 55% while DPU only grew 9.8%. Why the gap? Dilution. They issued new units (Preferential Offering) to pay for those acquisitions. You own a smaller slice of a much bigger pie—but since your slice is worth 9.8% more cash, we won’t complain too loudly.

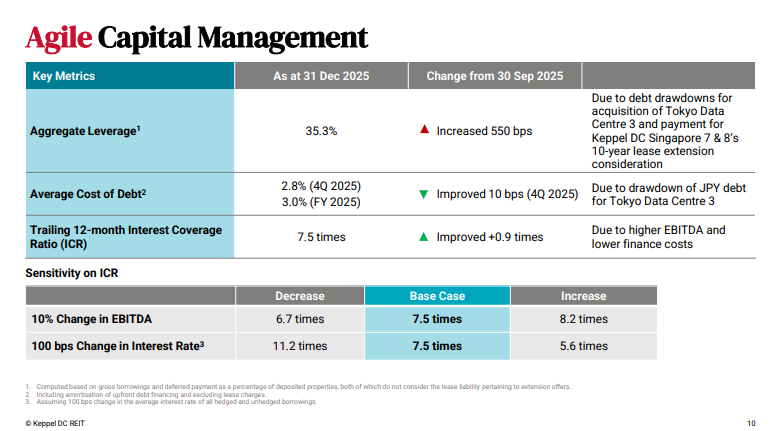

Slide 10: The Balance Sheet Reality Check

Growth costs money. KDCREIT has been shopping, and they put it on the credit card.

Aggregate Leverage increased by 550 basis points to 35.3%.

While 35.3% is higher than the super-conservative 29-30% we saw previously, it is still well within the safety zone (regulatory limit is 50%, internal threshold usually 40%). They cite the debt drawdown was specifically for the Tokyo Data Centre 3 acquisition and the lease extension for Singapore 7 & 8.

Here is the surprise: The Cost of Debt actually dropped.

FY 2025 Average Cost of Debt: 3.0%.

4Q 2025 Average Cost of Debt: 2.8%.

They managed to lower their interest costs by 10 basis points in the last quarter largely due to drawing down cheaper Japanese Yen (JPY) debt for the Tokyo acquisition. This is smart capital management—using Japan’s low-rate environment to hedge against higher global rates.

Key Stat: The Interest Coverage Ratio (ICR) is 7.5 times. This is incredibly healthy. Most REITs struggle to keep this above 3 or 4x. KDCREIT is not losing sleep over interest payments.

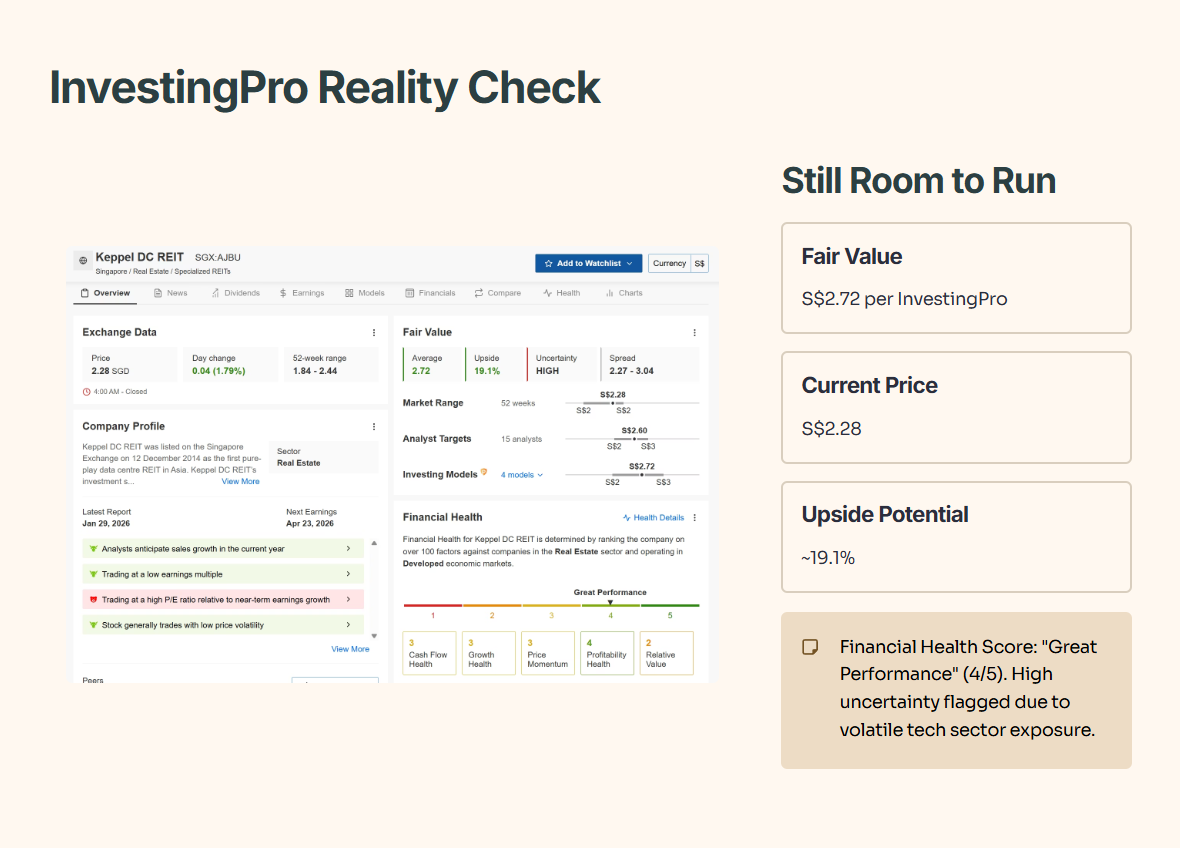

InvestingPro Reality Check: Valuation

The slides paint a rosy picture, and surprisingly, the institutional models agree that there is still room to run.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

Analysis: I checked the InvestingPro Fair Value model (which aggregates 4 financial models to remove human bias).

Contrary to the belief that AI stocks are “overhyped,” the models suggest KDCREIT hasn’t fully priced in its potential yet.

The Upside: InvestingPro calculates a Fair Value of S$2.72.

The Gap: With the price currently at S$2.28, the models imply a potential upside of ~19.1%.

The Health: The proprietary Financial Health Score remains “Great Performance” (4/5), anchored by that strong Profitability health.

Note on Risk: The model flags the “Uncertainty” as HIGH. This means while the potential is there, the range of outcomes is wide—likely due to the volatile nature of the tech sector it serves.

Concept Corner: What Is Rental Reversion?

Before we talk about that crazy 45% number, we need to make sure we’re speaking the same language. If you don’t understand rental reversion, you cannot understand why KDCREIT’s numbers look like this.

Imagine you own a rental flat. You sign a tenant on a 2‑year lease at S$2,000 a month. For two years, that price is locked. Even if the market explodes and every other unit in the block is renting at S$3,000, you are still stuck at S$2,000. You are missing the market upside.

The magic only happens when the lease expires. You sit down with the tenant and say: “Look at market prices. If you want to stay, the new rent is S$3,000.” If the tenant agrees, you’ve just achieved a 50% positive rental reversion. The walls didn’t change. The floor didn’t change. But the cash flow from that same asset jumped 50% overnight because the contract caught up with reality.

In traditional commercial real estate like malls or offices, landlords are happy with 3–5% positive reversion after a few years. If a mall landlord squeezes 5% more rent from a tenant, they pop the champagne. It’s a slow grind.

Data centres are a different beast. Switching is painful and expensive. If you run a coffee shop and rent goes up, you can move down the street. It hurts, but it’s possible. If you are Microsoft, Amazon, or any cloud provider with millions of dollars of servers, cabling, and cooling installed in a data centre, you cannot just “move on Tuesday”. You are physically and technically stuck.

So when the lease expires and the landlord says, “Your rent is going up 45% because there is basically zero vacancy anywhere else,” you have no real choice but to pay. That is pricing power in a landlord’s market.

This is why KDCREIT’s reported ~45% portfolio reversion is such a big deal. It is the cleanest signal we have that data centre supply is tight and tenants are desperate for space. This positive reversion is the engine under the hood of the numbers you’re seeing in this report.

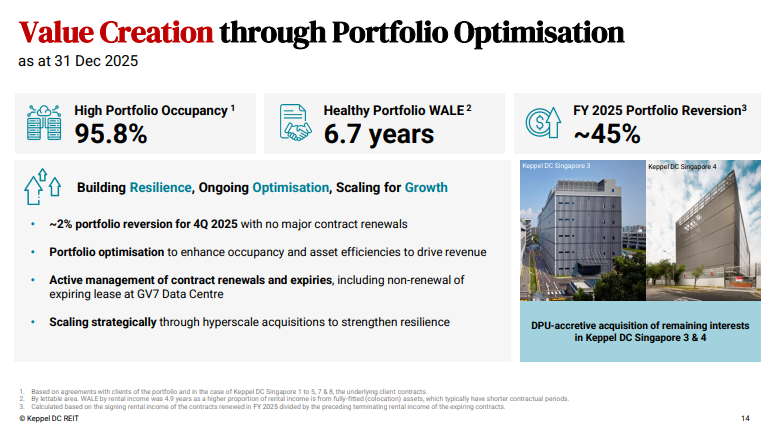

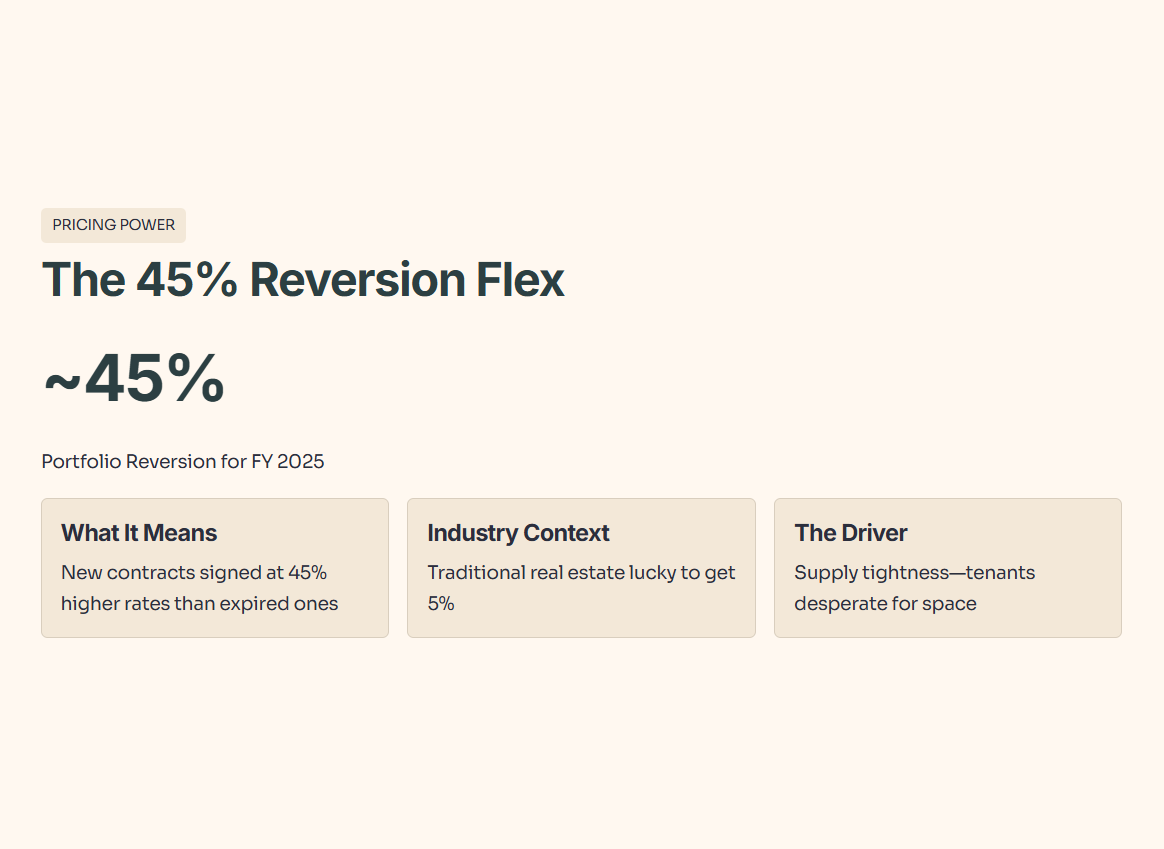

Slide 14 & 15: The “Pricing Power” Flex

If you take nothing else away from this article, memorize this number: ~45%.

That is the Portfolio Reversion for FY 2025. For the uninitiated, “Positive Reversion” means when an old contract expires, the new contract is signed at a higher rate. A 45% jump is unheard of in traditional real estate like malls or offices (where you’re lucky to get 5%).

This confirms the “Supply Tightness” narrative. Tenants are desperate for space, and KDCREIT is charging them a premium for it.

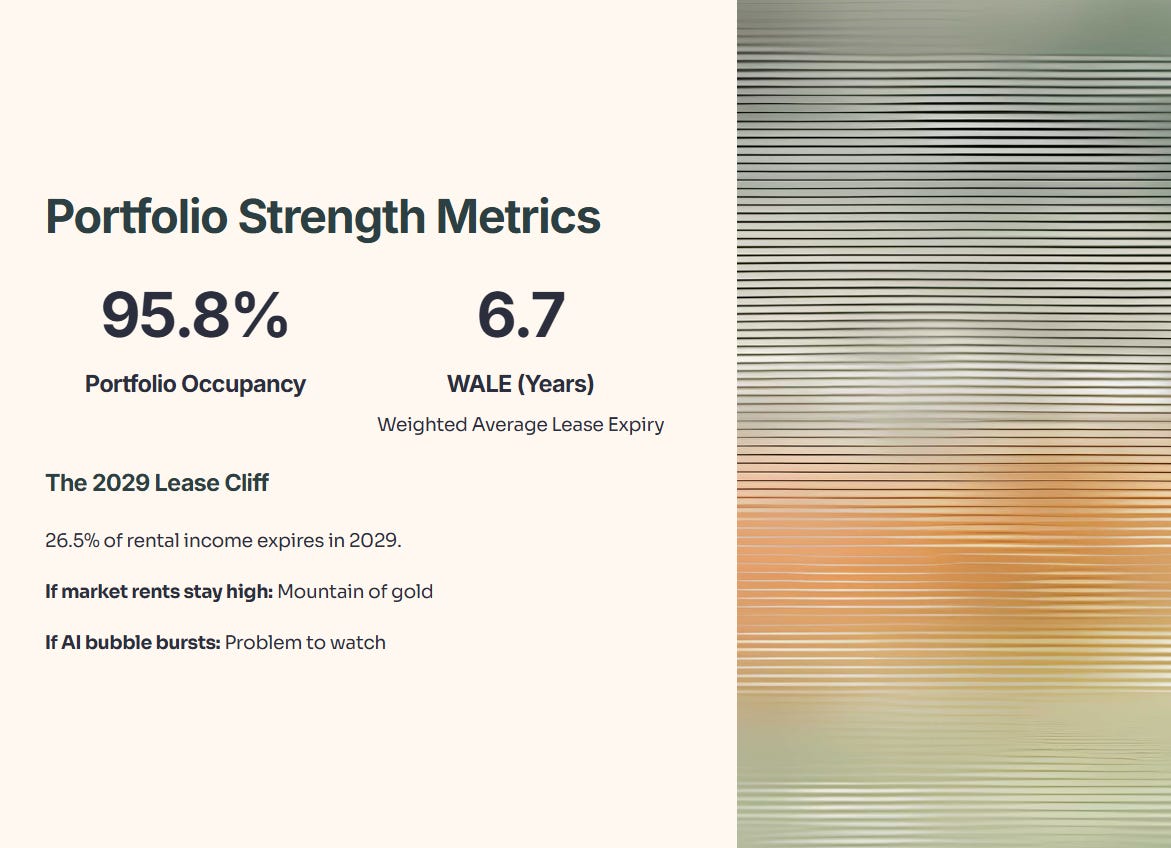

Portfolio Occupancy: High at 95.8%.

WALE (Weighted Average Lease Expiry): Long at 6.7 years.

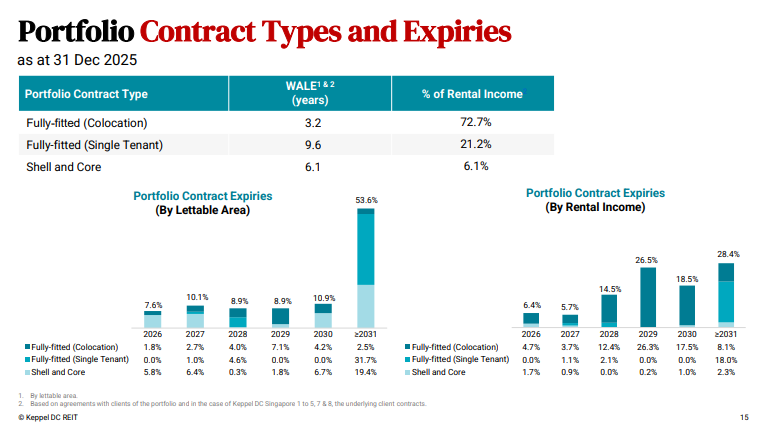

The Risk to Watch: Look at the expiry profile on Slide 15. In 2029, 26.5% of their rental income expires. That is a “lease cliff.” However, if market rents stay this high, that cliff turns into a mountain of gold. If the AI bubble bursts by 2029, it becomes a problem.

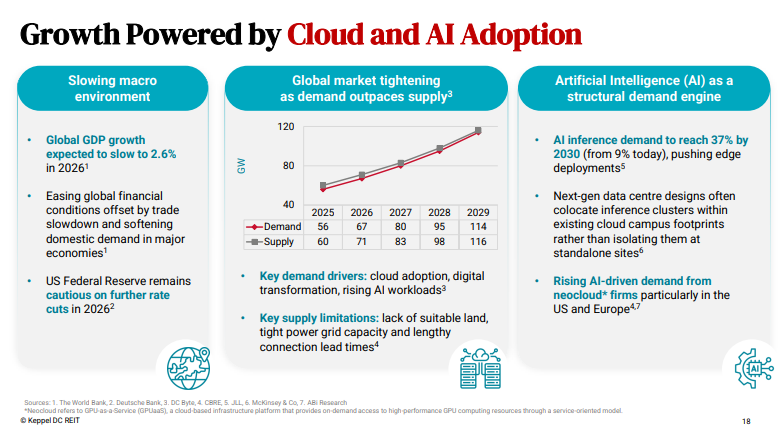

Slide 18: The Outlook (The AI Narrative)

Management is leaning hard into the AI story. They explicitly cite “Artificial Intelligence (AI) as a structural demand engine”.

They note that AI inference demand is expected to jump from 9% today to 37% by 2030.

Why does this matter?

Demand: It outpaces supply. They project global demand (114 GW) to nearly match supply (116 GW) by 2029, keeping vacancy tight.

Constraints: They list “tight power grid capacity” as a key limitation. If you already have the data centre with power (like KDCREIT does), your asset becomes significantly more valuable because competitors can’t just build a new one next door easily.

Iggy’s Scorecard: FY 2025 Results

I don’t give “Buy/Sell” calls, but I do keep score.

Here’s how KDCREIT actually scores on my system—and what that implies for upside, downside, and position size in a real portfolio.