Keppel DC REIT: UOB Kay Hian Says Buy at S$2.99. Iggy's Screen Says Zone 4.

When Analyst Targets Meet Retirement Hurdles: Yield, Gearing, and the AI Growth Trade

You bought Keppel DC REIT for the AI story and the sponsor pipeline. Nobody mentioned that today’s yield sits below what Iggy’s framework treats as a minimum for retirement income, the 4.7% yield hurdle I require before any stock qualifies for a retirement drawdown portfolio. This is where the analyst’s target price and your CPF drawdown plan stop agreeing with each other.

Data centre REITs are having a moment, and Keppel DC REIT has been near the centre of that story for over a decade now. It’s the kind of stock that shows up in a lot of heartland portfolios precisely because it feels safe. So it’s worth actually checking whether the numbers still say what the narrative says.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips, the interest coverage, the gearing, the free cash flow sustainability, so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

Section 1: The Analyst’s Case

Section 2: Iggy’s Forensic Screen

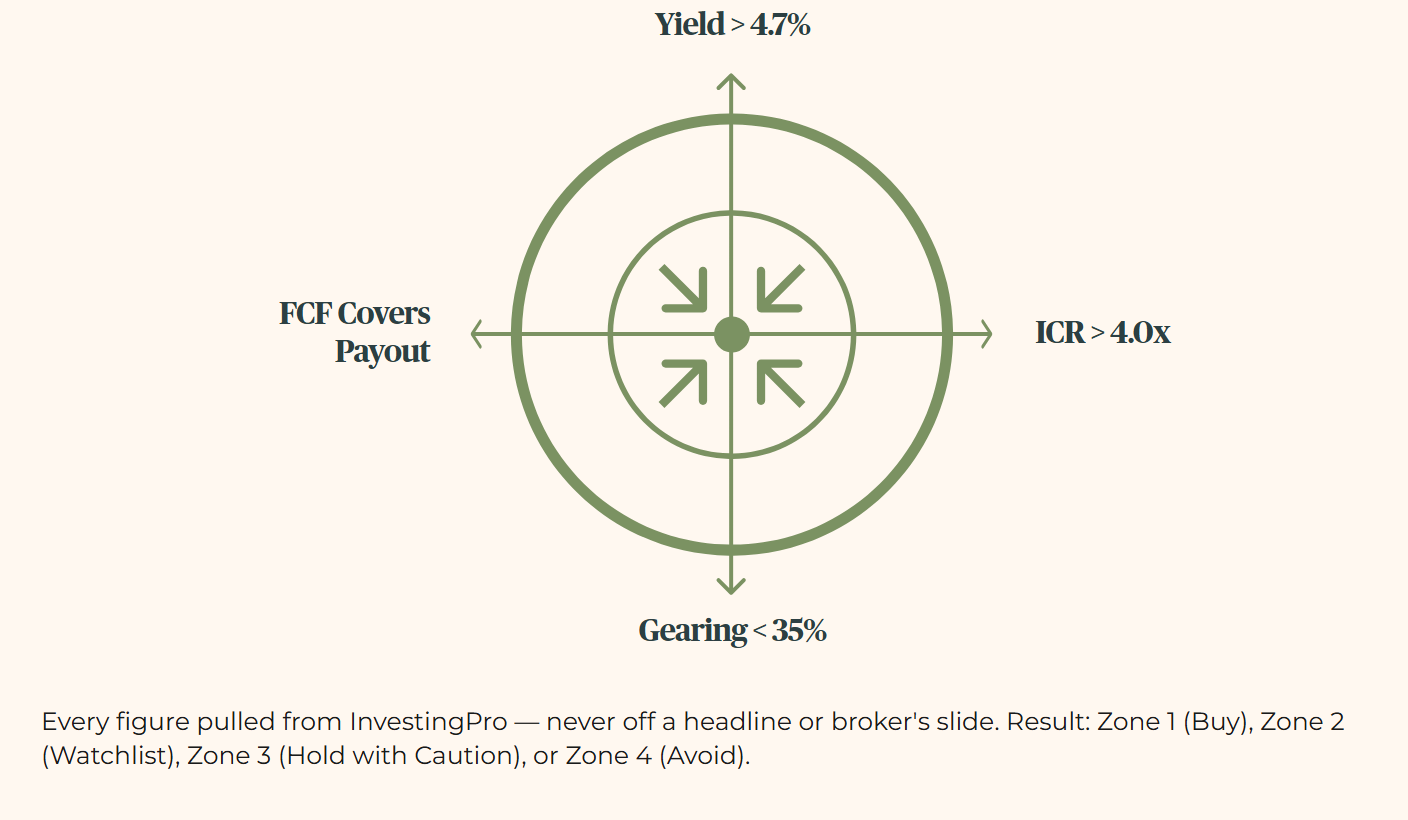

How Iggy Rates Every Stock

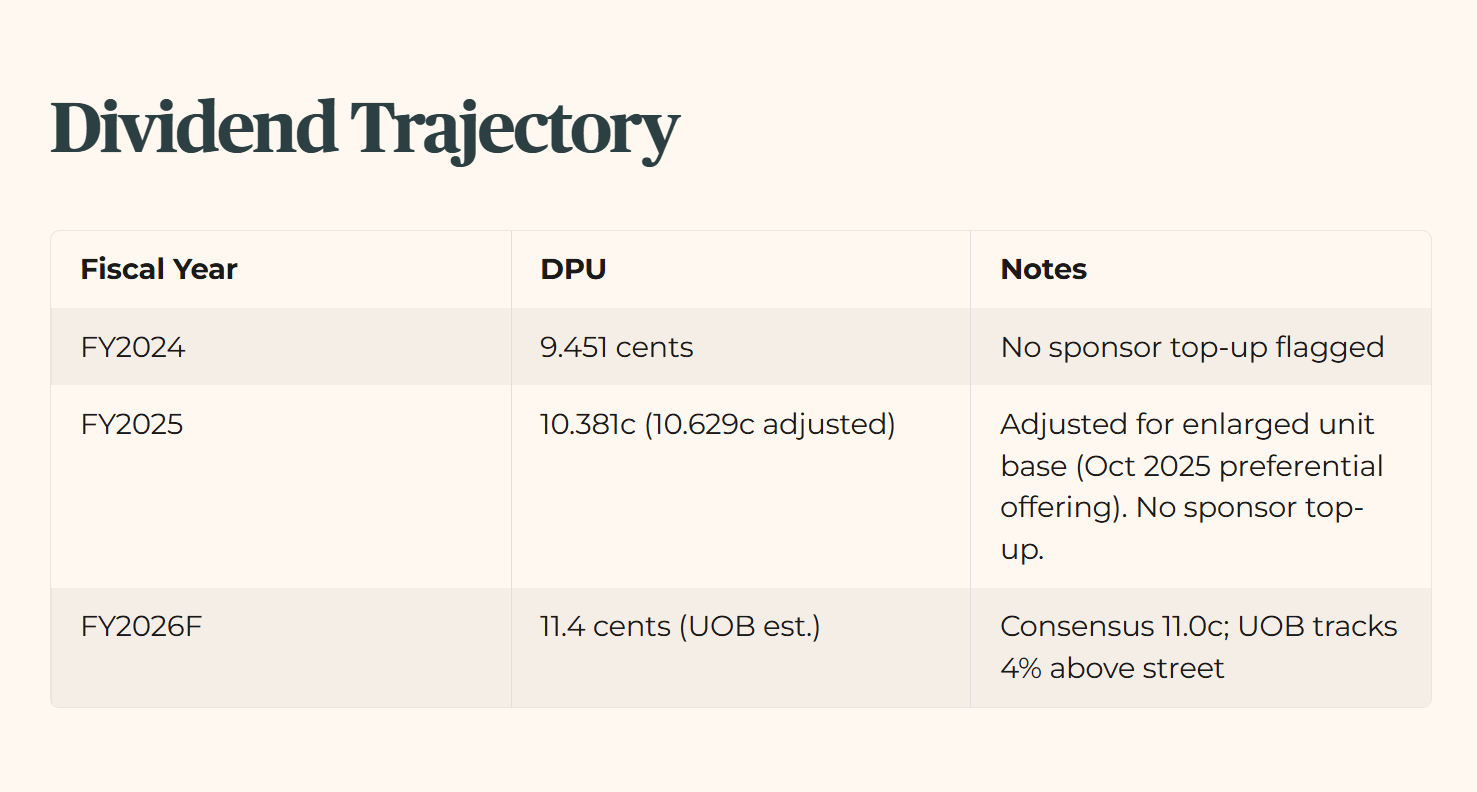

Section 3: The Dividend Trajectory

Dividend Trajectory

Section 4: The Forensic Gap

Forensic Gap

Iggy’s Insight Box 1

One Last Thing Before You Go

Section 5: What to Watch Next

Iggy’s Insight Box 2

Closing: The Forensic Stance

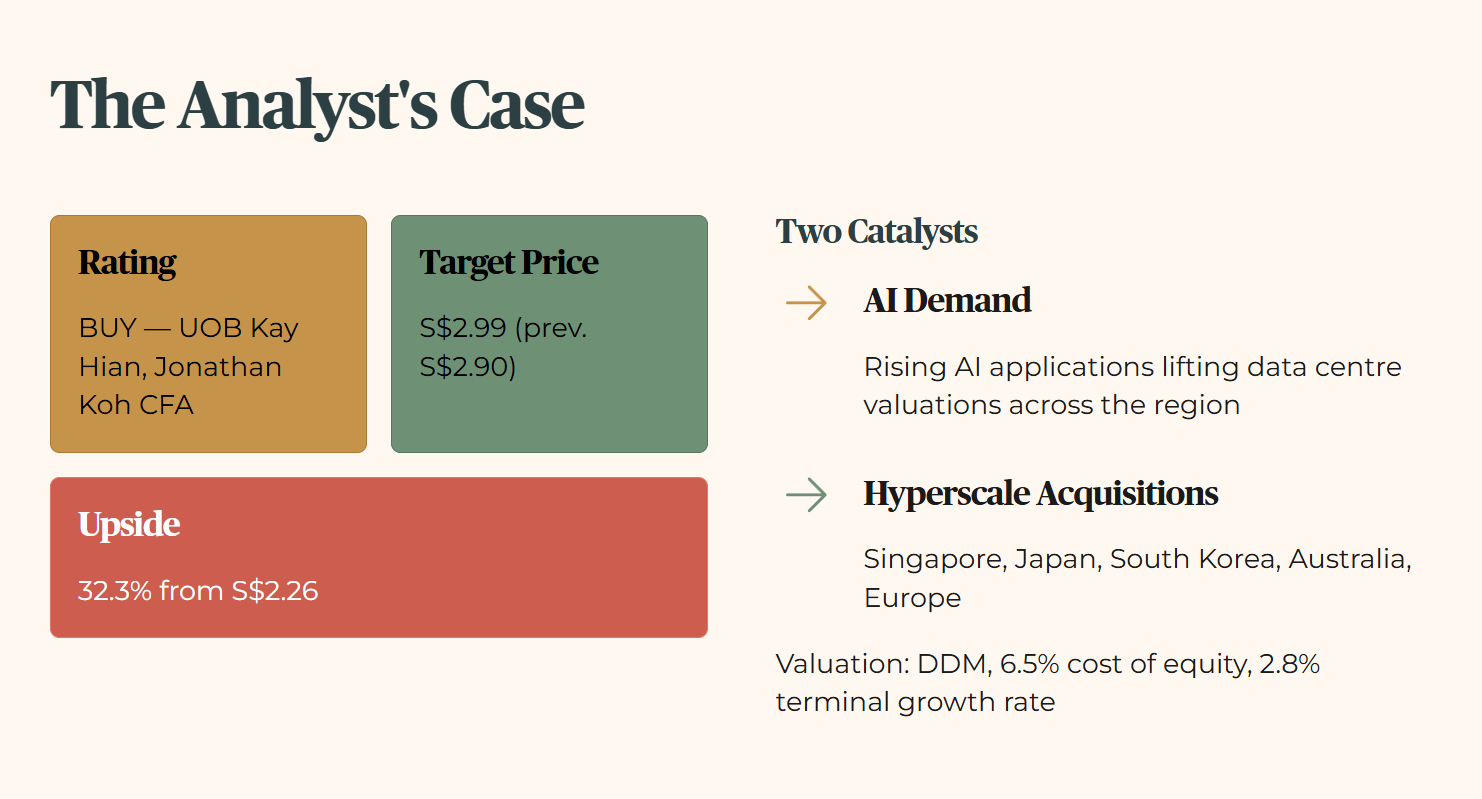

Section 1: The Analyst’s Case

UOB Kay Hian, via analyst Jonathan Koh, CFA, maintains a BUY rating on Keppel DC REIT (SGX: AJBU) with a target price of S$2.99, up from a previous S$2.90. At the current share price of S$2.26, that implies 32.3% upside. The valuation is built on a dividend discount model, using a cost of equity of 6.5% and a terminal growth rate of 2.8%.

The thesis rests on two catalysts. First, rising demand driven by AI applications, the same tailwind lifting data centre valuations across the region. Second, acquisitions of hyperscale data centres across Singapore, Japan, South Korea, Australia, and Europe, an expansion story that goes well beyond the REIT’s existing footprint.

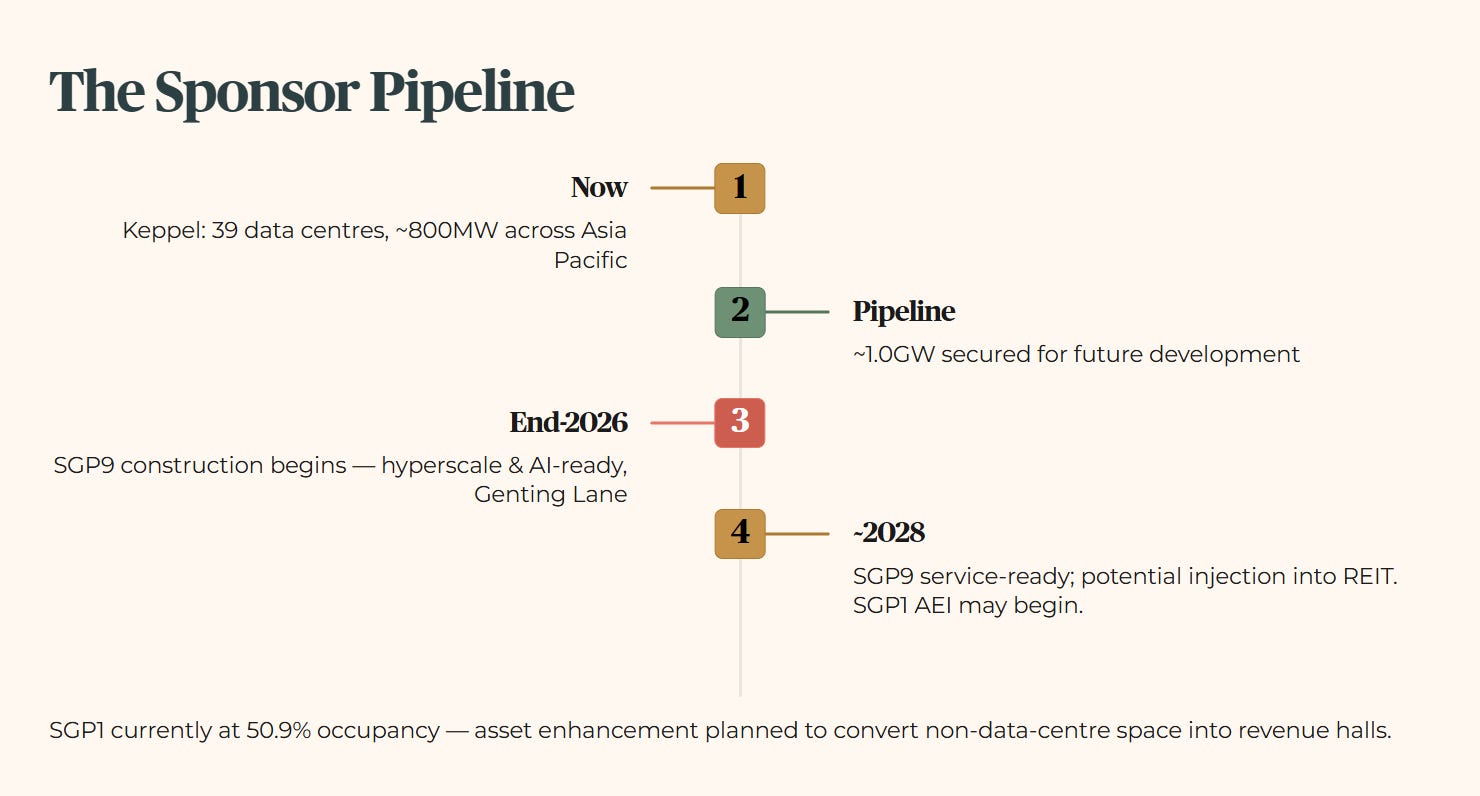

Underneath both catalysts sits a sponsor-level detail worth understanding on its own terms. Keppel, the sponsor, operates 39 data centres totalling approximately 800MW of capacity across Asia Pacific, with a further pipeline of roughly 1.0GW secured for future development. Within Singapore specifically, Keppel is developing SGP9, a third data centre at the Keppel Data Centre Campus in Genting Lane, built for hyperscale and AI-ready demand. Construction is slated to begin by end-2026, with service readiness expected around 2028.

Once stabilised, the note suggests SGP9 could eventually be injected into the REIT itself, enlarging its portfolio. A separate asset enhancement is also on the table: SGP1, currently 50.9% occupied, could be upgraded to convert non-data-centre space into revenue-generating halls, with work potentially starting in early 2028.

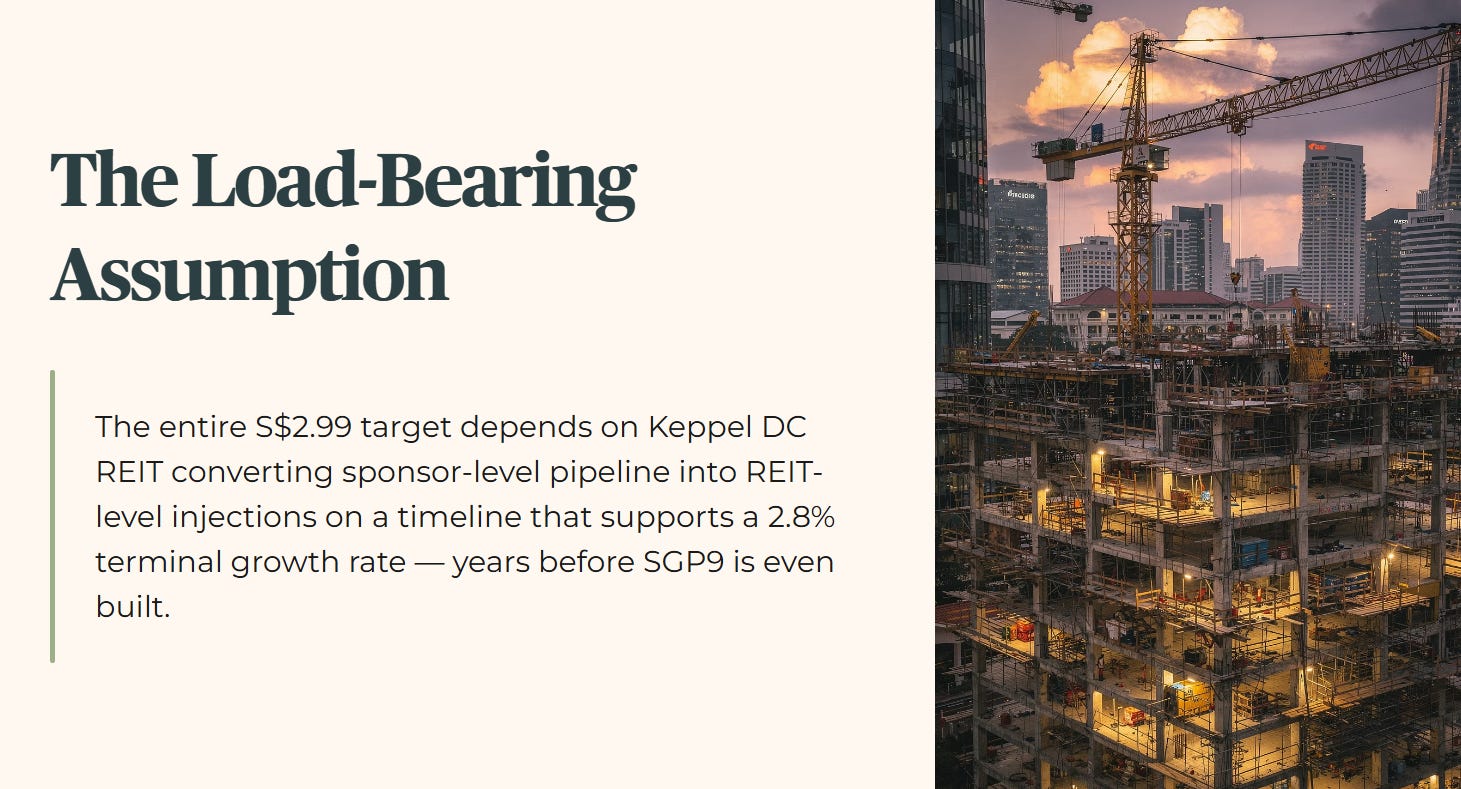

THE LOAD-BEARING ASSUMPTION: The entire S$2.99 target depends on Keppel DC REIT continuing to convert sponsor-level pipeline growth into REIT-level asset injections on a timeline that supports a 2.8% terminal growth rate, years before SGP9 is even built.

Section 2: Iggy’s Forensic Screen

Here’s where the analyst’s growth story meets Iggy’s forensic floor. Two figures matter more than any pipeline slide: what the REIT yields today, and how it’s actually funded.

Financial Health Checklist

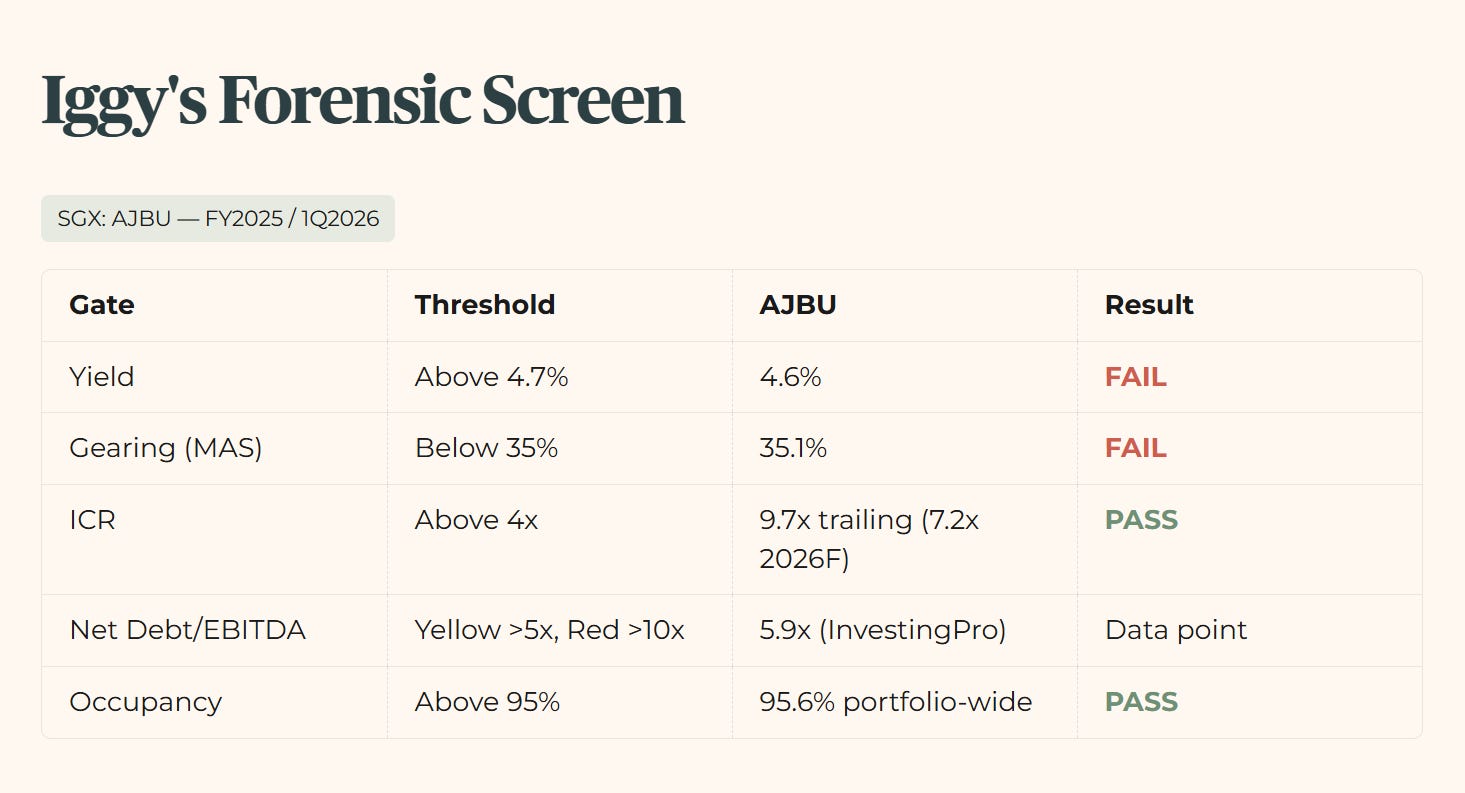

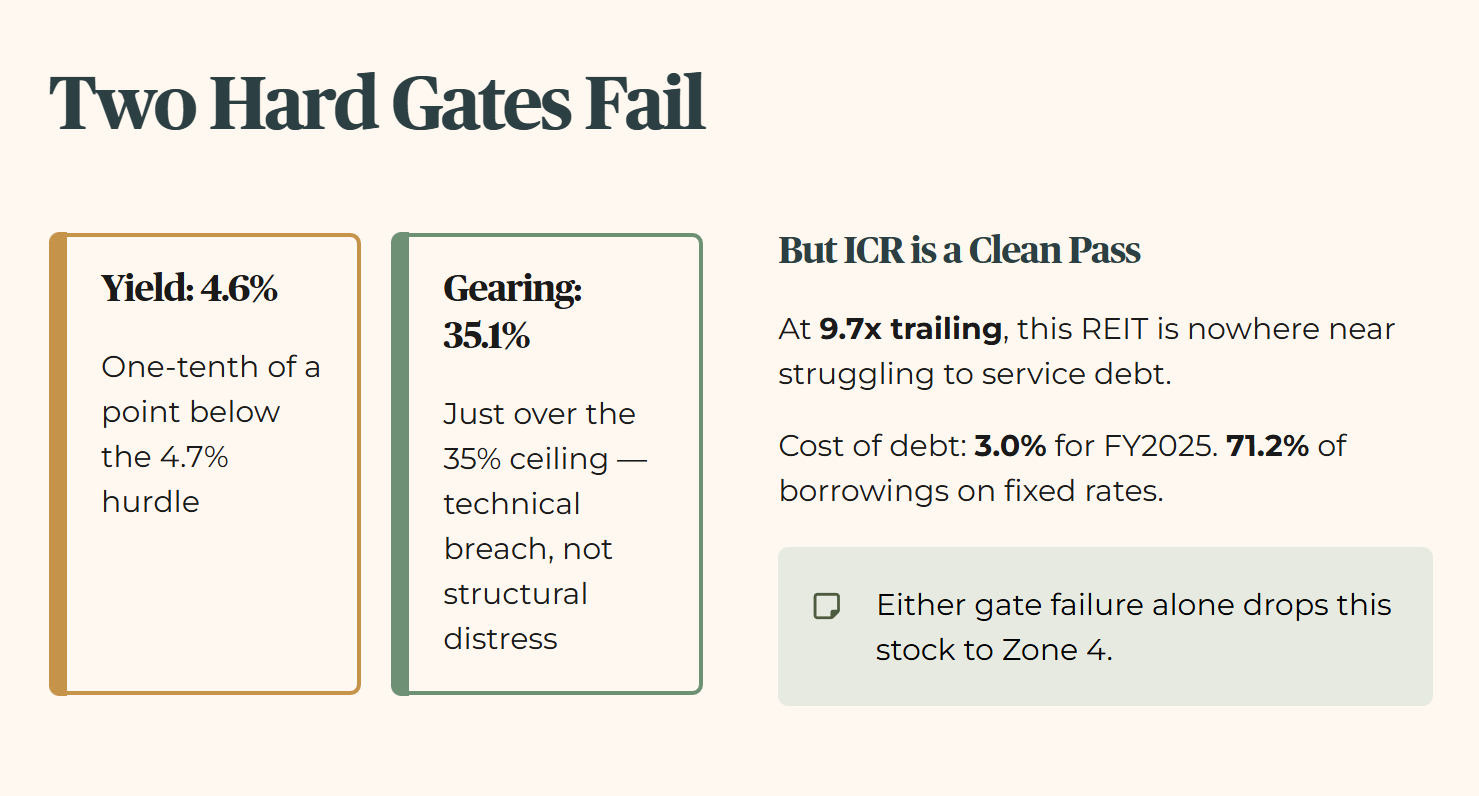

Two hard gates fail here. Either one alone is enough to drop this stock to Zone 4. The yield is one-tenth of a percentage point below the 4.7% hurdle. Gearing sits at 35.1%, just over the 35% ceiling and into the 35–45% band. This is worth being precise about: at 0.1 percentage points over the line, this is a technical breach, not a structural one. The balance sheet is not in distress. It is just barely on the wrong side of a threshold Iggy holds firmly.

ICR is a clean pass by a wide margin. At 9.7x trailing, this REIT is nowhere near struggling to service its debt. Cost of debt is a reasonable 3.0% for FY2025, with 71.2% of borrowings on fixed rates. This is not a REIT with a financing crisis. It’s a REIT where the yield and the leverage haven’t caught up to the price the market, and now UOB Kay Hian, is paying for the growth story.

On occupancy, the portfolio-wide figure of 95.6% technically clears the threshold. But averages can hide concentration. SGP1 stands out at 50.9% occupancy, contributing S$16.5m in rental income in 2025 despite being roughly half empty. Most of the remaining portfolio sits close to full. That means the healthy headline number is being carried by strong performance elsewhere in the book, while this asset sits meaningfully underutilised, even as an asset enhancement plan is on the table to fix it from 2028.

Two soft flags apply here, per the current zone registry. First, JPY debt exposure at 39.6% of the borrowing base, with the Bank of Japan’s rate normalisation underway, a genuine watch item given Keppel DC REIT’s Japan exposure sits at 13.6% of AUM and growing. Second, sponsor concentration: Keppel holds approximately 19.2% of units, which cuts both ways, deep alignment with the sponsor’s own capital, but also a governance concentration worth naming plainly.

Iggy’s Forensic Zone: Zone 4, Caution

How Iggy Rates Every Stock

Every stock that crosses Iggy’s desk goes through the same forensic checklist, no exceptions — whether it’s a blue chip you’ve held for twenty years or a REIT you’re eyeing for the first time. Four numbers matter most: a dividend yield that clears the 4.7% hurdle, an interest coverage ratio above 4.0x, gearing kept under the 35% ceiling, and free cash flow that actually covers the payout — because a dividend that isn’t backed by cash isn’t income, it’s a refund of your own capital.

Every figure is pulled from InvestingPro and LongBridge, never eyeballed off a headline or a broker’s slide. Based on how a stock clears these tests, it lands in one of four zones: Zone 1 (Buy), Zone 2 (Watchlist), Zone 3 (Hold with Caution), or Zone 4 (Avoid). This isn’t a stock tip — it’s the same health check a forensic auditor would run before signing off on a company’s books, so you can see exactly what you’re buying before you buy it.

Section 3: The Dividend Trajectory

The direction here is genuinely constructive. DPU (distribution per unit, the actual cash paid out per unit held) grew year on year into FY2025 and is forecast to keep growing into FY2026, and there’s no sponsor top-up propping up the number. The growth appears to reflect actual operating performance, including continued contributions from the M1 NetCo bonds, an income-generating investment in telecom infrastructure that was slated for divestment but had that sale terminated in May 2026, keeping an S$11m annual income stream (a 9% internal rate of return) on the books.

The next calculation takes that growing DPU, layers in the enlarged unit base, and measures exactly how far a 4.6% yield still falls short of Iggy’s 4.7% retirement-income hurdle once the refinancing and growth trade are priced in.