S-REIT Warning: Why Most Dividends Are Still Dropping (Except These 4) 🦖 EP1286

Interest rates are finally easing, but only four REITs are showing meaningful distribution growth. Here is the breakdown for your SRS portfolio.

The “REIT Winter” has officially thawed.

For the last 24 months, Singaporean investors have watched their REIT portfolios bleed red ink. High interest rates crushed valuations, and rising financing costs ate into distributable income. It was a painful waiting game.

But the tide has turned. The Fed has moved, and the Singapore 10-Year Bond yield has dropped significantly from its peak.

However, if you think this means you should blindly throw money at the iEdge S-REIT Index, think again. The recovery is asymmetric. While the broad market breathes a sigh of relief, only a select few REITs are actually growing their payouts in a meaningful way.

Today, we look at the four names that are bucking the trend—and why one of them is leaving the others in the dust.

In This Article:

• The Winners’ Circle: A Data Snapshot

• Keppel DC REIT: The AI Growth Engine

• Frasers Centrepoint Trust (FCT): The “Sleep Well” Choice

• Mapletree Pan Asia Commercial Trust (MPACT): A Tale of Two Cities

• AIMS APAC REIT (AA): The Industrial Grinder

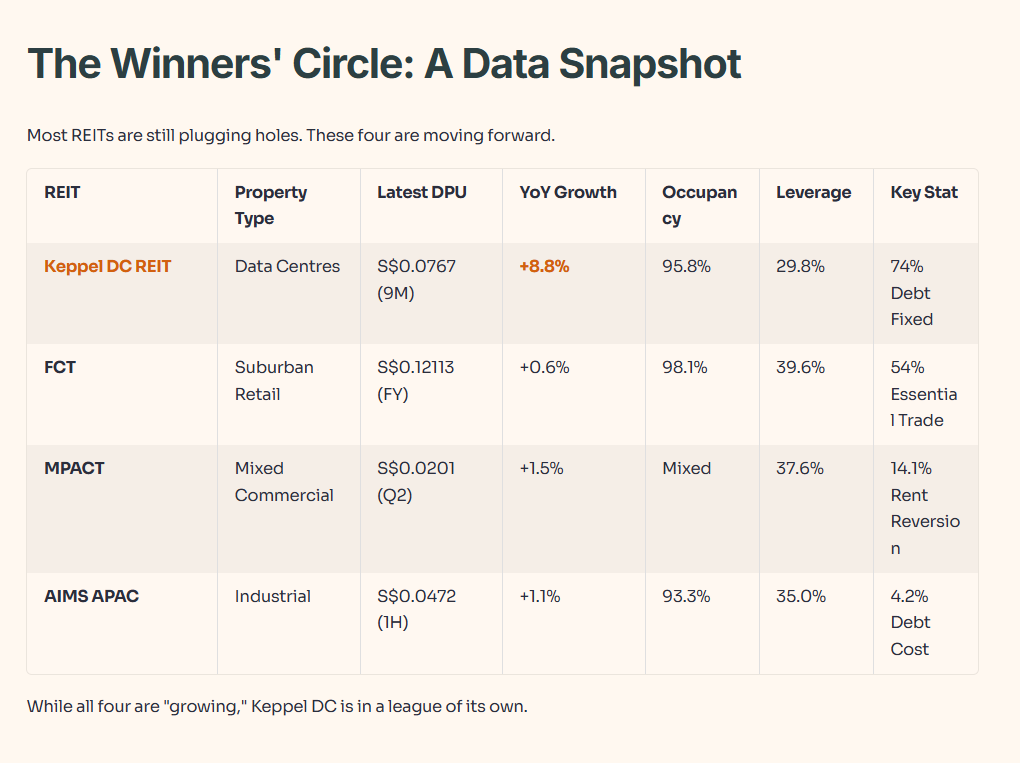

• The Bottom Line: Position for the DivergenceThe Winners’ Circle: A Data Snapshot

Most REITs are still trying to plug the holes left by high interest rates. These four are already moving forward.

What this table tells us is that while all four are “growing,” Keppel DC is in a league of its own. The others are grinding out gains; Keppel is capturing a structural shift.

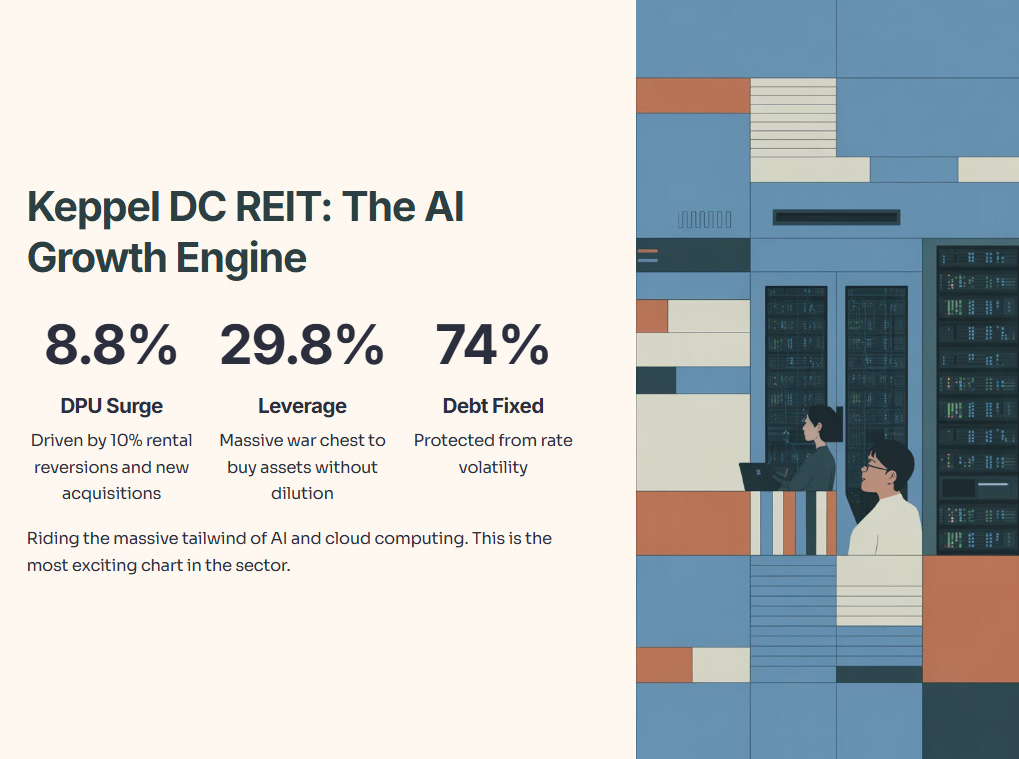

Keppel DC REIT: The AI Growth Engine

This is the most exciting chart in the sector right now. While other REITs struggle to pass on costs, Keppel DC is riding the massive tailwind of Artificial Intelligence and cloud computing.

Their DPU surged 8.8%, driven by strong rental reversions of 10% and the ramping up of acquisitions like Keppel DC Singapore 7 and 8. But the real magic is in the balance sheet: 29.8% leverage.

In a world where many REITs are flirting with 40% gearing limits, Keppel DC has a massive war chest to buy more assets without diluting shareholders.

Iggy’s Insight:

This is no longer just a yield play; it is a growth stock disguised as a REIT. The market knows this, which is why the yield is compressed compared to its peers.

My Verdict: I am treating KDREIT as a core growth holding. I am not waiting for a 6% yield here because it likely won’t happen. I am paying for the 8.8% DPU growth and the exposure to the AI infrastructure boom. If you are under 50 and building a portfolio, this is your overweight.

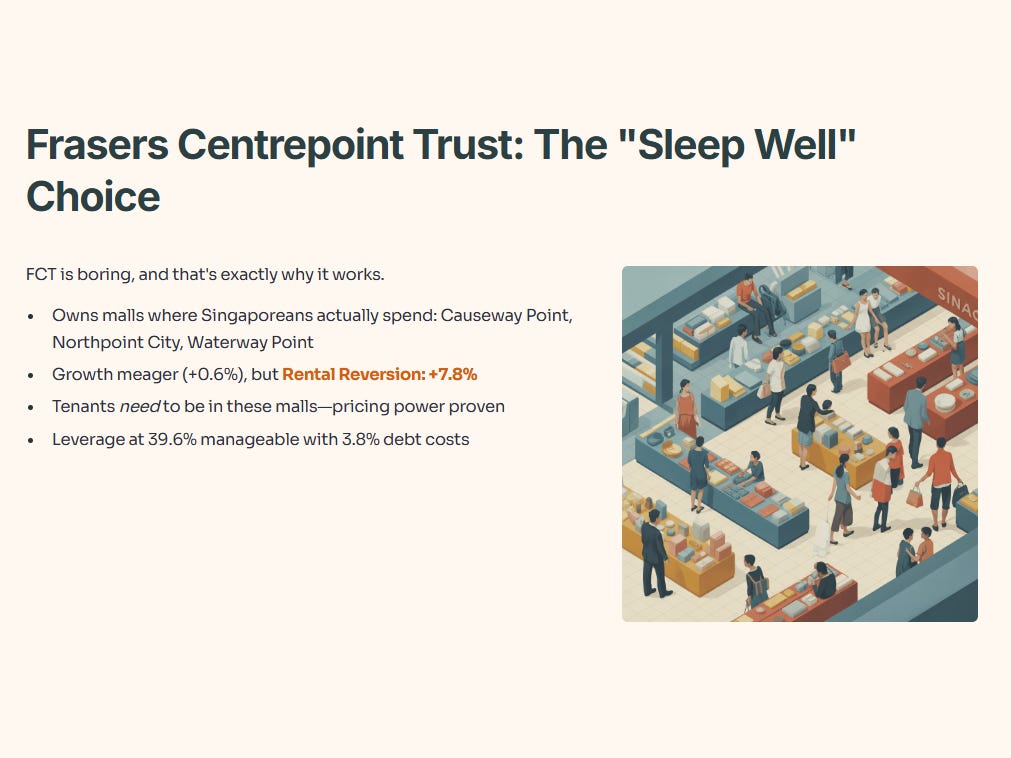

Frasers Centrepoint Trust (FCT): The “Sleep Well” Choice

FCT is boring, and I love it for that. It owns the malls where Singaporeans actually spend money—Causeway Point, Northpoint City, Waterway Point.

The growth is meager (+0.6%), but look at the Rental Reversion: +7.8%. This proves that even with inflation, tenants need to be in these malls. They have pricing power. The slight uptick in leverage to 39.6% is manageable given their ability to lock in debt costs at 3.8%.

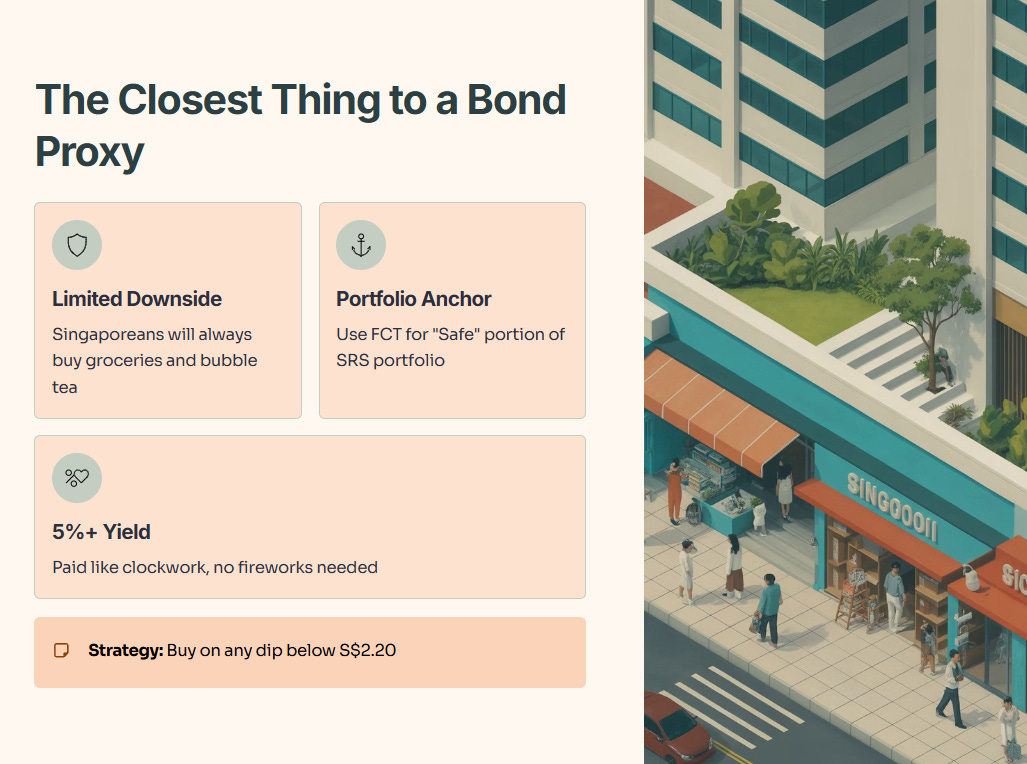

Iggy’s Insight:

FCT is the closest thing we have to a “Bond Proxy” in the equity market right now. The downside is limited because Singaporeans will always buy groceries and bubble tea.

Strategy: I use FCT to anchor the “Safe” portion of my SRS portfolio. I am not expecting capital appreciation fireworks, but I am expecting that 5%+ yield to be paid like clockwork. Buy on any dip below S$2.20.

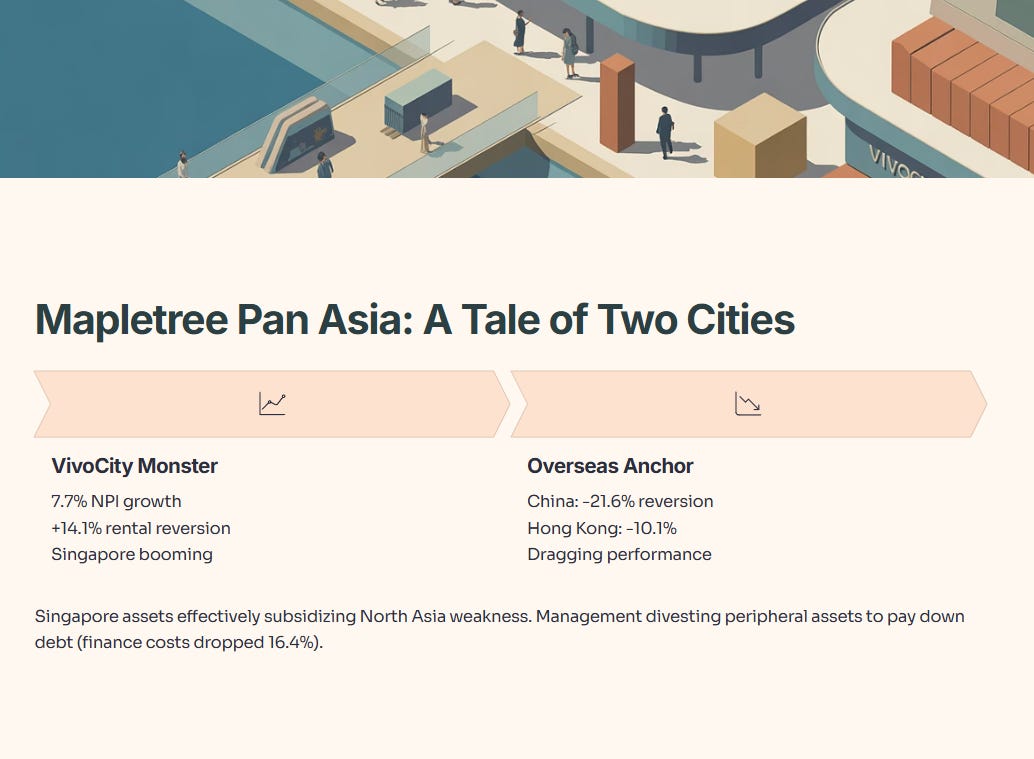

Mapletree Pan Asia Commercial Trust (MPACT): A Tale of Two Cities

MPACT is the most complex story here. If you look at VivoCity, it’s a monster: 7.7% Net Property Income growth and +14.1% rental reversion. Singapore is booming.

But the overseas portfolio is an anchor. China rental reversions are negative 21.6%. Hong Kong is negative 10.1%. The Singapore assets are effectively subsidizing the weakness in North Asia.

Management is doing the right thing—divesting peripheral assets to pay down debt (finance costs dropped 16.4%)—but the drag is real.

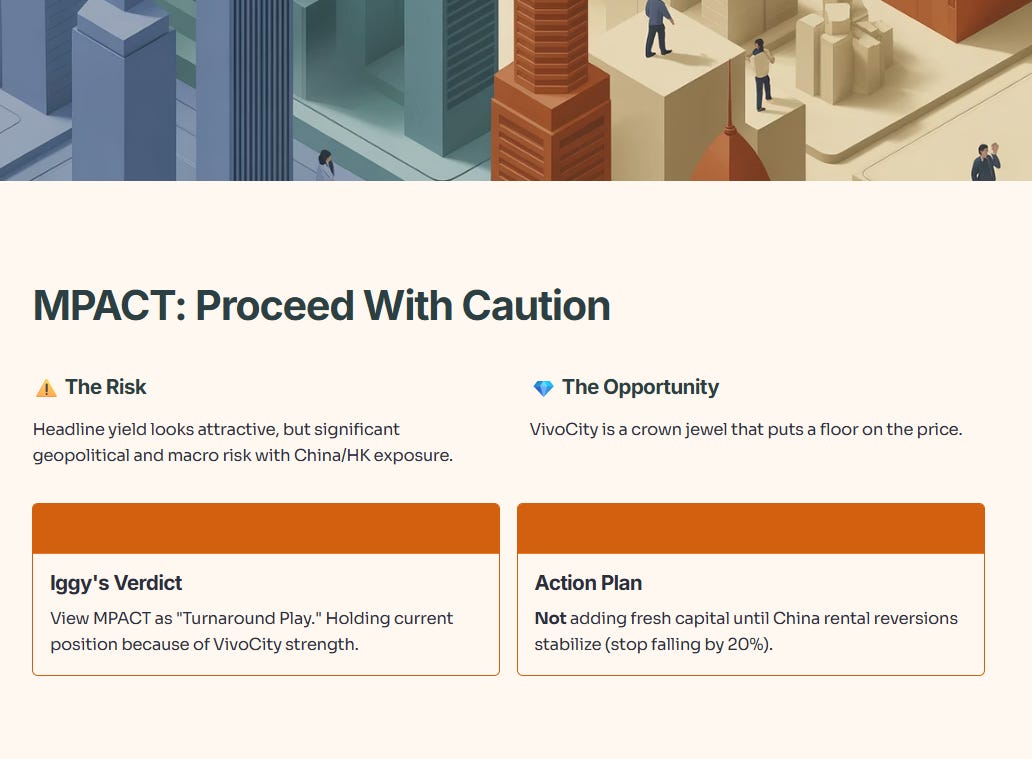

Iggy’s Insight:

Be careful here. The headline yield looks attractive, but you are taking on significant geopolitical and macro risk with the China/HK exposure.

My Verdict: I view MPACT as a “Turnaround Play.” I am holding my current position because VivoCity is a crown jewel that puts a floor on the price. However, I am not adding fresh capital until I see the China rental reversions stabilize (i.e., stop falling by 20%).

AIMS APAC REIT (AA): The Industrial Grinder

AA REIT is the quiet achiever. A 1.1% DPU hike isn’t headline news, but it signals stability. The key for AA is the Refinancing Pivot. As interest rates drop, their blended debt cost (currently 4.2%) will stop rising and potentially drift lower, widening their margins.

However, with a WALE (Weighted Average Lease Expiry) of 4.2 years, they have a lot of leases coming up for renewal. In a slowing economy, that’s a risk.

Iggy’s Insight:

AA is a solid diversifier, but it lacks the “Moat” of FCT or the “Growth” of Keppel DC. It belongs in a large, diversified portfolio (15+ stocks), but if you only have capital for 3-5 REITs, this one probably doesn’t make the cut over the big boys.