Keppel 82% Gearing Alert: AGM 2026 Dividend Hikes Mask Legacy Debt

Management shows you the 18.7% ROE "Ferrari," but our forensic audit reveals the 7.4% reality dragging your capital.

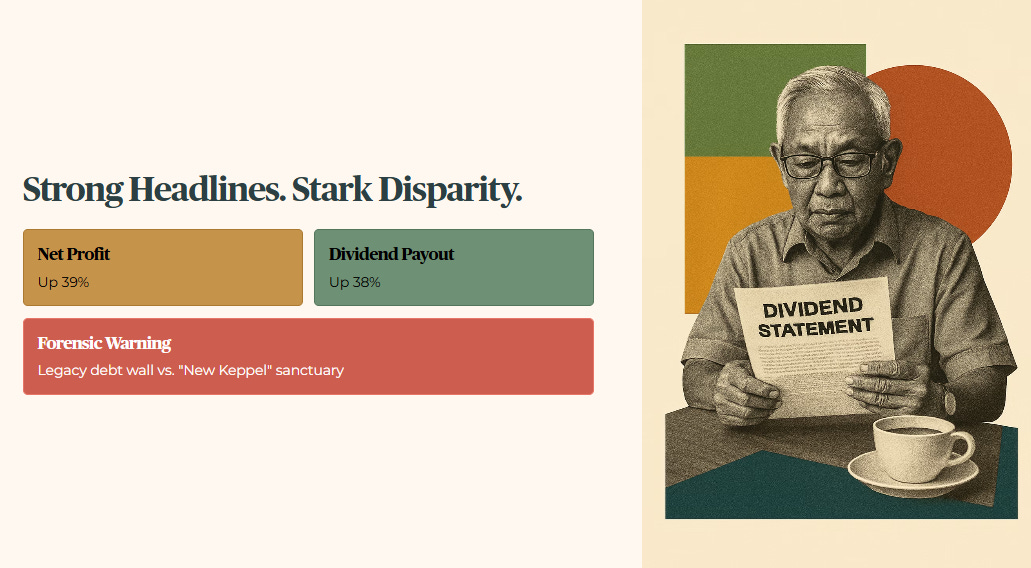

Net profit up 39%. Dividend payout up 38%. Management is calling it a strong performance for the New Keppel. If you are holding this for retirement income, the forensic audit reveals a stark disparity between the “New Keppel” sanctuary and the legacy debt wall.

In This Article:

The Asset Management Engine

Infrastructure The Record Pillar

The Monetisation Wall

The Yield Floor Test Where the Ordinary Dividend Fails

The Stress Test Buffer

Forward Risk The Middle East Watch Item

Forensic Stance Watchlist Trigger

Iggy’s Bottom Line

Iggy’s Forensic Compliance Standards Standard Disclaimer

The Asset Management Engine

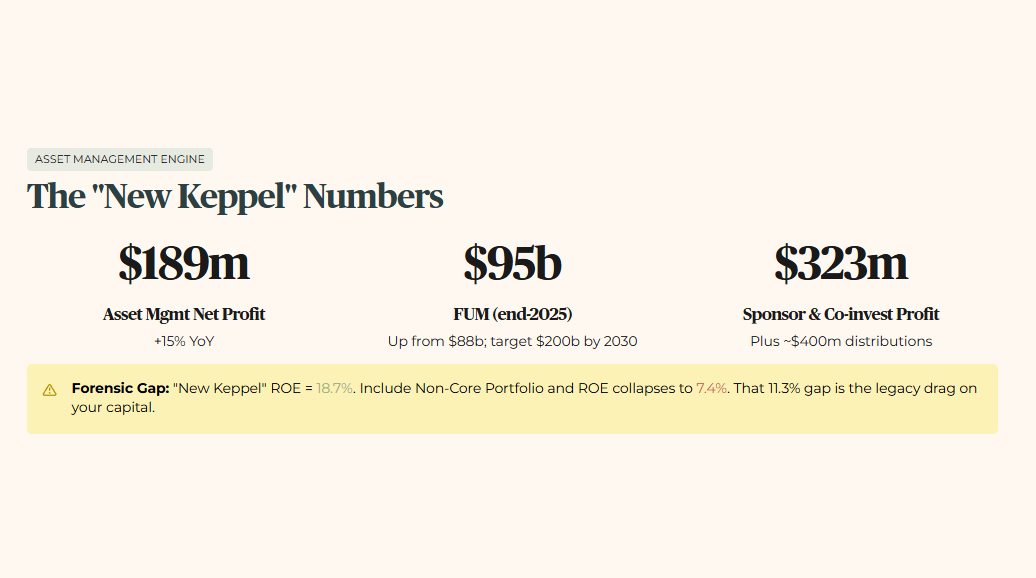

Keppel’s transition into a global alternative asset manager is focused on energy transition and digitalisation. In FY25, Asset Management net profit rose 15% year-on-year to $189m. Beyond these profits, returns from sponsor stakes and co-investments contributed $323m in net profit and distributions of approximately $400m in FY25. For a 55-year-old investor using SRS, this shift toward fee-based income is the core thesis for distribution sustainability.

Funds Under Management grew from $88b to $95b as at end-2025. Management is targeting $200b by 2030. The “New Keppel” ROE rose to 18.7% in FY25 from 14.9% in FY24. However, including the Non-Core Portfolio for Divestment, the ROE was only 7.4% in FY25. This 11.3% forensic gap represents the drag of legacy assets on your capital efficiency.

Infrastructure: The Record Pillar

The Infrastructure Division delivered record earnings, with recurring income growing at a 51% CAGR from FY21 to reach $703m in FY25. Integrated Power Business EBITDA was $661m, remaining resilient against softening spark spreads. Spark spreads refer to the difference between the market price of electricity and its fuel cost. For the heartland investor, this is like a chicken rice stall owner hedging the cost of poultry to keep margins steady even when gas prices spike.

🦎 Iggy’s Insight Block 1

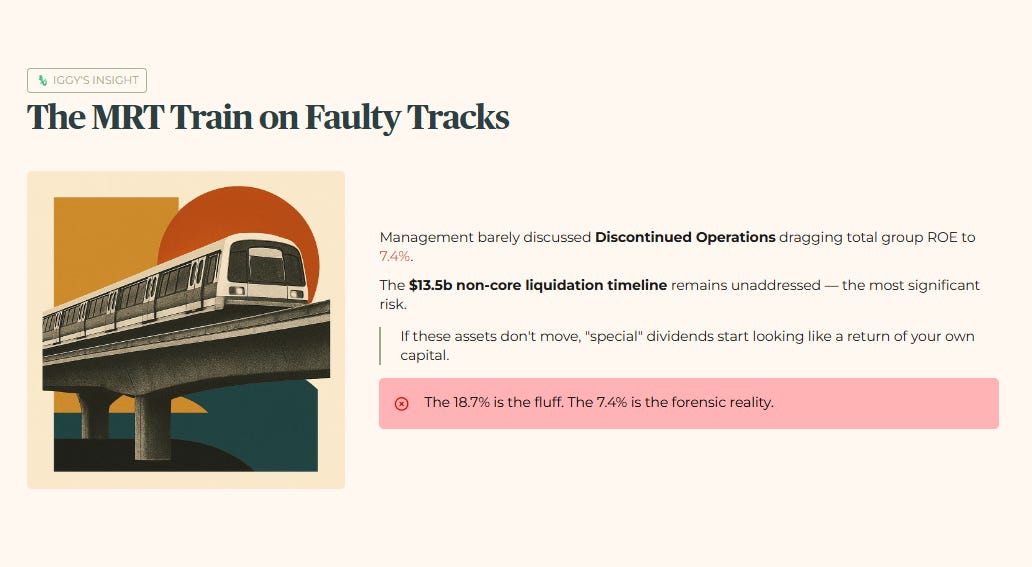

Management spent very little time discussing the “Discontinued Operations” impact on the total group ROE, which stands at a dismal 7.4%. While the “New Keppel” 18.7% ROE looks like a sleek MRT train, the legacy assets are the faulty tracks dragging the entire system down. The silence on the specific timeline for the $13.5b non-core liquidation is the most significant risk. If these assets do not move, your “special” dividends stop being special and start looking like a return of your own capital. The fluff is the 18.7%; the forensic reality is the 7.4%.

Forensic Punchline: Don’t let the New Keppel’s perfume mask the smell of the legacy rig assets.

The Monetisation Wall

Asset monetisation announced in 2025 reached $2.9b, bringing the total to $14.5b since October 2020. This includes $1.3b from the proposed sale of M1’s telco business, which is still pending IMDA approval.

Raw Fact: Total monetisation announced since October 2020 is $14.5b.

Historical Benchmark: Keppel’s pace of divestment has accelerated significantly since the 2023 Keppel O&M divestment of $4.7b.

Peer Context: Compared to Sembcorp Industries, which has more aggressively pivoted to renewables, Keppel remains more diversified but carries higher legacy baggage.

Forward Scenario: A 10% delay in the M1 sale or commercial project divestments would stall approximately $290m in anticipated cash flow, potentially reducing the special dividend payout by $0.01 per share. A macro trigger would be further tightening of Singapore’s regulatory environment for telco consolidation.

Wallet Impact: For a retiree relying on the special dividend, this is the difference between a bonus and a flat yield. Your income is now explicitly tied to management’s ability to find buyers for old assets.

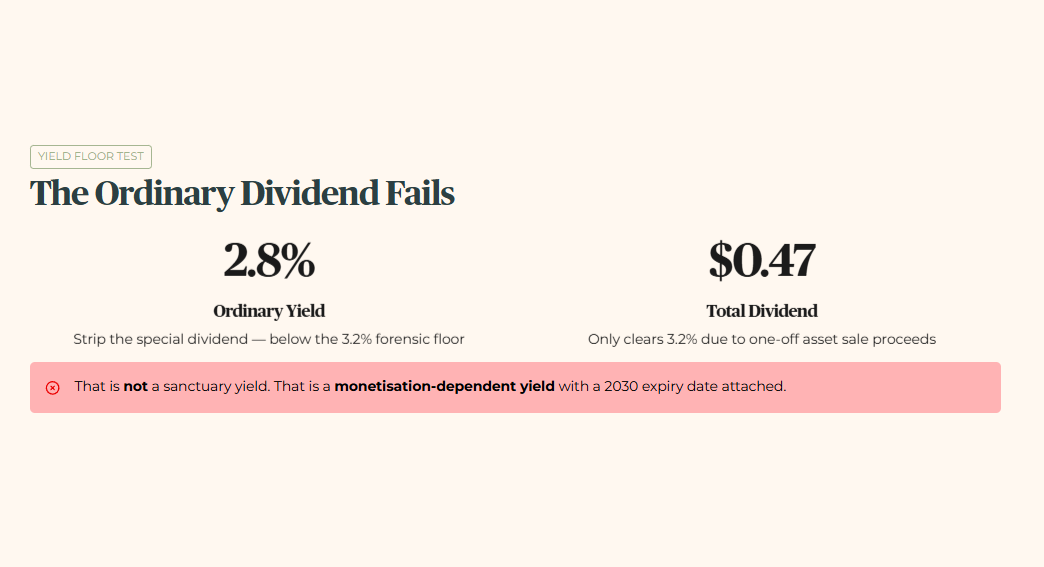

The Yield Floor Test: Where the Ordinary Dividend Fails

Before the tables, one number demands your attention. Strip away the special dividend and Keppel’s ordinary dividend yield is 2.8% at current prices. That figure sits below the 3.2% forensic floor — the threshold I apply to determine whether an asset even qualifies for serious consideration as a retirement income holding. The headline $0.47 total dividend only clears 3.2% because of one-off asset sale proceeds. That is not a sanctuary yield. That is a monetisation-dependent yield with a 2030 expiry date attached.

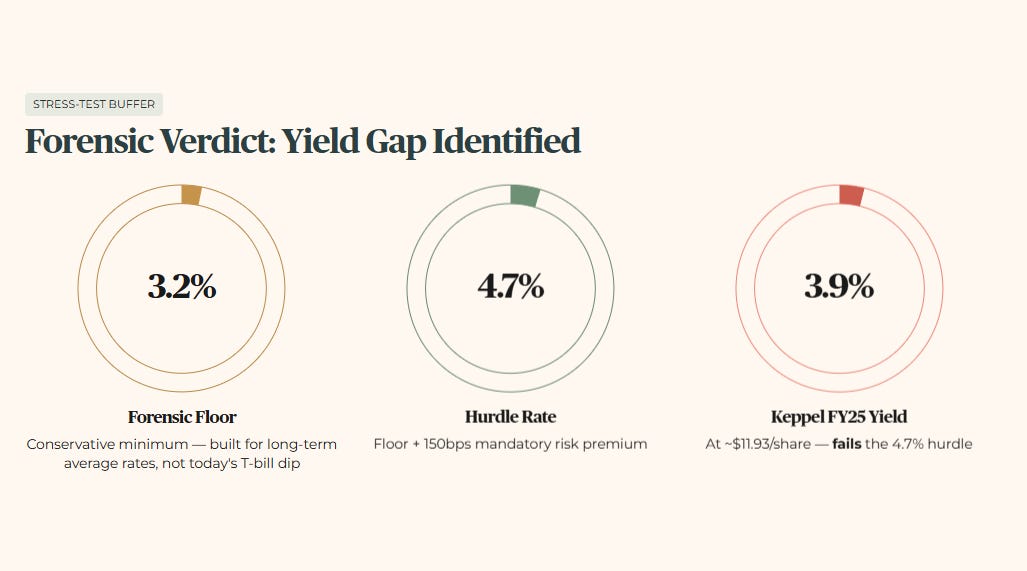

The Stress-Test Buffer

For this audit, I apply a conservative floor of 3.2%. I audit for the storm, not just the sunny day. While the T-bill sits at approximately 1.47% (source: MAS, public data, 9 April 2026), I do not lower my standards to match a temporary market dip. My floor remains at 3.2% to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7% — the 3.2% floor plus 150 basis points of mandatory risk premium.

Forensic Verdict: Yield Gap Identified. Keppel’s FY25 total dividend is approximately $0.47 per share. At a share price of approximately $11.93, this is a trailing yield of 3.9%. This fails the 4.7% hurdle.

The ordinary-versus-total yield math is only the first cut — once you layer this 3.9% headline against the 82% gearing and the $13.5b divestment overhang in the next section, the true sanctuary scorecard for Keppel’s dividend looks very different.