Kimly | DBS Research BUY at $0.52 | Analyst Ratings Review

DBS Says Buy. Here's the Number That Changes the Conversation.

S$147,840,000. That is the total weight of the debt sitting on the balance sheet of a company that primarily makes its money selling S$1.50 kopi and S$5.00 minced meat noodles.

For a retail investor looking for a quiet retirement sanctuary, this number is a pattern interrupt that demands a closer look before we chase a 4.88% yield.

Today, I am auditing whether the defensive food and beverage thesis from DBS holds up when I run it through my forensic screen.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips — the interest coverage, the gearing, the free cash flow sustainability — so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

The coffee shop is one of the most familiar sights in Singapore — every HDB estate has one, every morning starts there. What most people do not realise is that behind the S$1.50 kopi and the steaming plates of noodles, there is a corporate balance sheet that most Singaporeans have never looked at. Today we are going to look at it together.

In This Article:

Section 1 — The Analyst’s Case

Section 2 — Iggy’s Forensic Screen

Dimension One — Valuation

Dimension Two — Income

Dimension Three — Execution Risk

Dimension Four — Ownership Signal

Dimension Five — Who Is This For

Financial Health Checklist

Section 3 — The Dividend Trajectory

Section 4 — The Forensic Gap

Iggy’s Insight — The Net Cash Illusion

The Window Is Already Open

Section 5 — What To Watch Next

Iggy’s Insight — The Watchlist Case

The Dual Verdict

Iggy’s Forensic Disclaimer

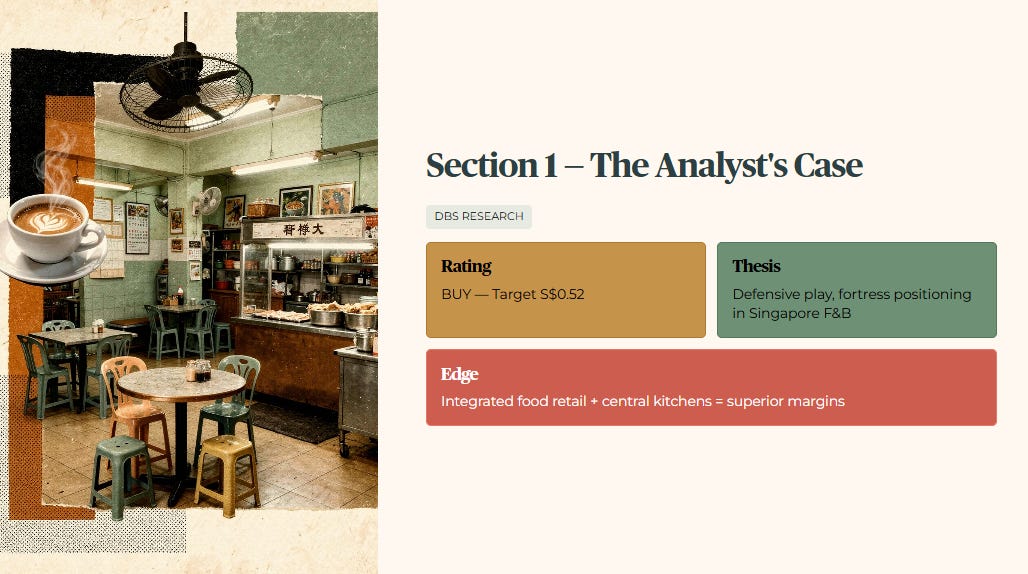

Section 1 — The Analyst’s Case

DBS has initiated coverage on Kimly Ltd with a BUY rating and a target price of S$0.52.

Their thesis is built on the premise that Kimly is a defensive play with a fortress-like positioning in the Singapore food and beverage sector. The analyst highlights Kimly as a leader in the coffee shop space, using integrated food retail and central kitchens to squeeze out better margins than the independent operators.

The core of the institutional argument rests on three pillars.

First, a strong balance sheet characterised as having S$63.05 million in net cash, which DBS believes provides the ammunition for mergers and acquisitions.

Second, a clear growth runway provided by 43 new HDB coffee shops slated for completion by 2030.

Third, a strategic pivot into the Halal food and beverage market through the Tenderfresh acquisition and the Kedai Kopi joint venture, targeting a market worth roughly S$1 billion.

DBS expects Kimly to deliver steady 3% to 5% earnings growth through operating leverage and modest outlet expansion. They value the stock at 18x forward price-to-earnings, noting that a 4% forward yield is attractive for a defensive consumer name.

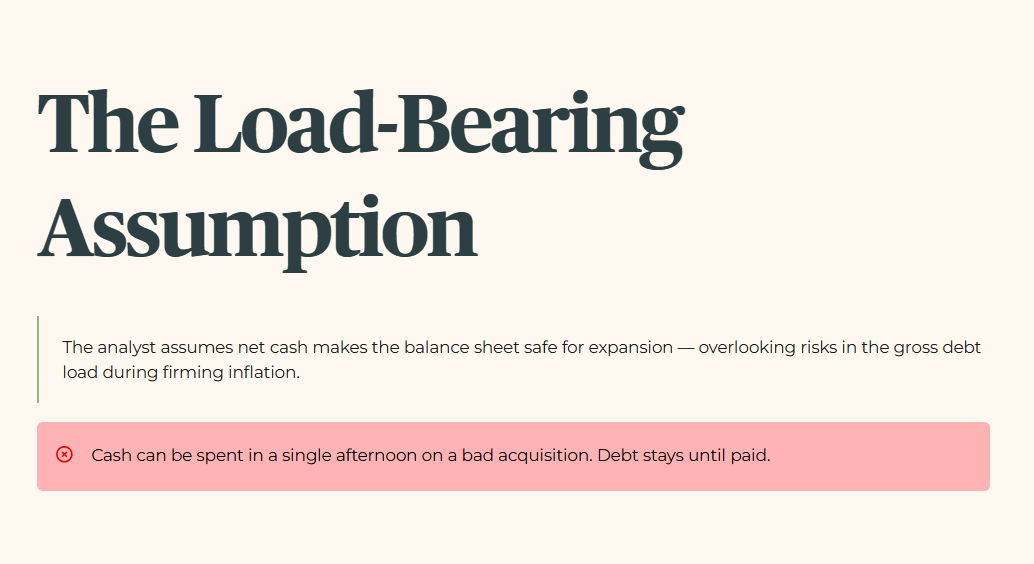

THE LOAD-BEARING ASSUMPTION: The analyst assumes that Kimly’s net cash position makes the balance sheet safe for expansion, overlooking the risks inherent in the gross debt load during a period of firming inflation.

Section 2 — Iggy’s Forensic Screen

I do not look at “net cash” because cash can be spent in a single afternoon on a bad acquisition. Debt stays with you until it is paid or refinanced.

We apply the five forensic dimensions to the verified data.

Dimension One — Valuation

Raw Fact

The verified gearing (the proportion of the company’s assets funded by debt) for Kimly is 37.09%. Total debt stands at S$147.84 million against total assets of S$398.60 million. The current yield is 4.88%, and the Interest Coverage Ratio (ICR — the number of times operating profit covers interest expense) is 7.36x.

The income case is not the primary concern here. A yield of 4.88% clears my 4.7% minimum yield hurdle — the income threshold I require before any stock qualifies for a retirement portfolio. What fails is the structural gate: gearing of 37.09% breaches my 35% forensic ceiling.

The analyst values Kimly at 18x forward earnings, arriving at a target of S$0.52. InvestingPro’s fair value estimate is S$0.45. The gap of S$0.07 — approximately 13.5% above forensic fair value — is filled not by verified cash flows but by growth assumptions dependent on tender wins and margin expansion that have yet to materialise.

The gap between DBS’s S$0.52 target and the S$0.45 forensic fair value is where the real audit begins — because in the next section we follow that S$0.07 premium through Kimly’s declining profits, flat dividends, and rising gearing to see whether the numbers can actually carry it.