KLSE Dividends: Your No-BS Guide to 5–6% Yields That Actually Work

Think Malaysian dividends are just “nice to have”? Here’s why KLSE is a real dividend engine—and the four checks that separate sustainable 6% yields from traps.

Most income investors chase the highest yield. Then they get burned when the payout gets cut. Malaysia offers a better path. Its dividend culture is strong. Banks, REITs, and utilities pay out real cash from steady cash flows. The key is learning what keeps those payouts safe over time.

In this guide, we’ll build that filter together. I’ll show why KLSE works for income, the four pillars of sustainable payouts, which names deserve core slots, and how a Singapore investor can slot them into CPF/SRS plans or an SGD-first strategy. Clear, practical, and built for action.

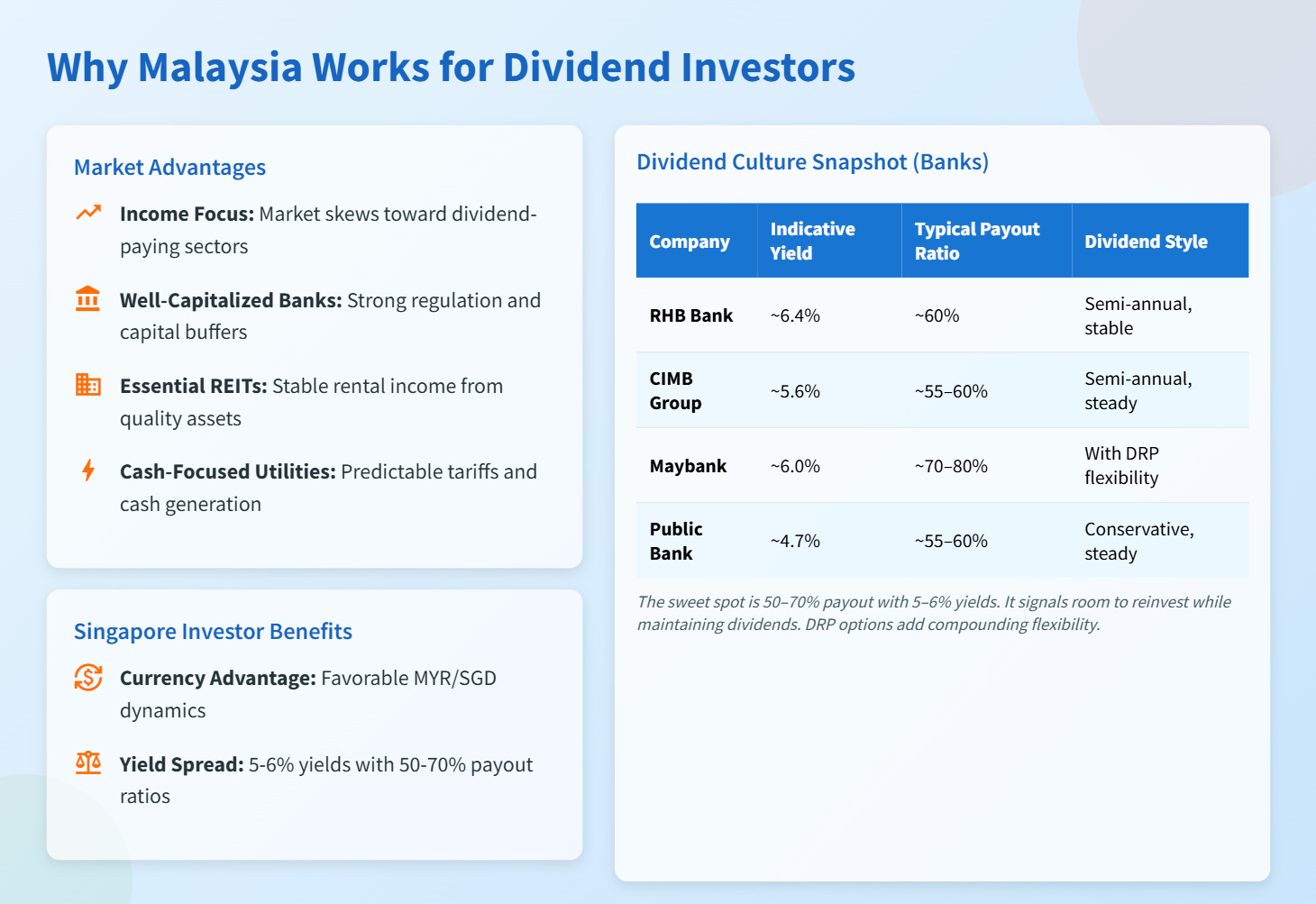

Why Malaysia Works for Dividend Investors

Malaysia’s market skews toward income. Banks are well-capitalized and regulated. REITs run essential assets. Utilities and staples focus on cash generation. This culture supports consistent payouts over cycle.

Singapore investors also benefit from currency and yield spread thinking. Many KLSE names yield 5–6% while keeping payout ratios in the 50–70% zone. That balance gives room for reinvestment and cushions during shocks. It’s not hype. It’s policy, prudence, and track record.

This table highlights the balance Malaysia’s major banks strike between yield and payout. The sweet spot is 50–70% payout with 5–6% yields. It signals room to reinvest while maintaining dividends. DRP options add compounding flexibility.

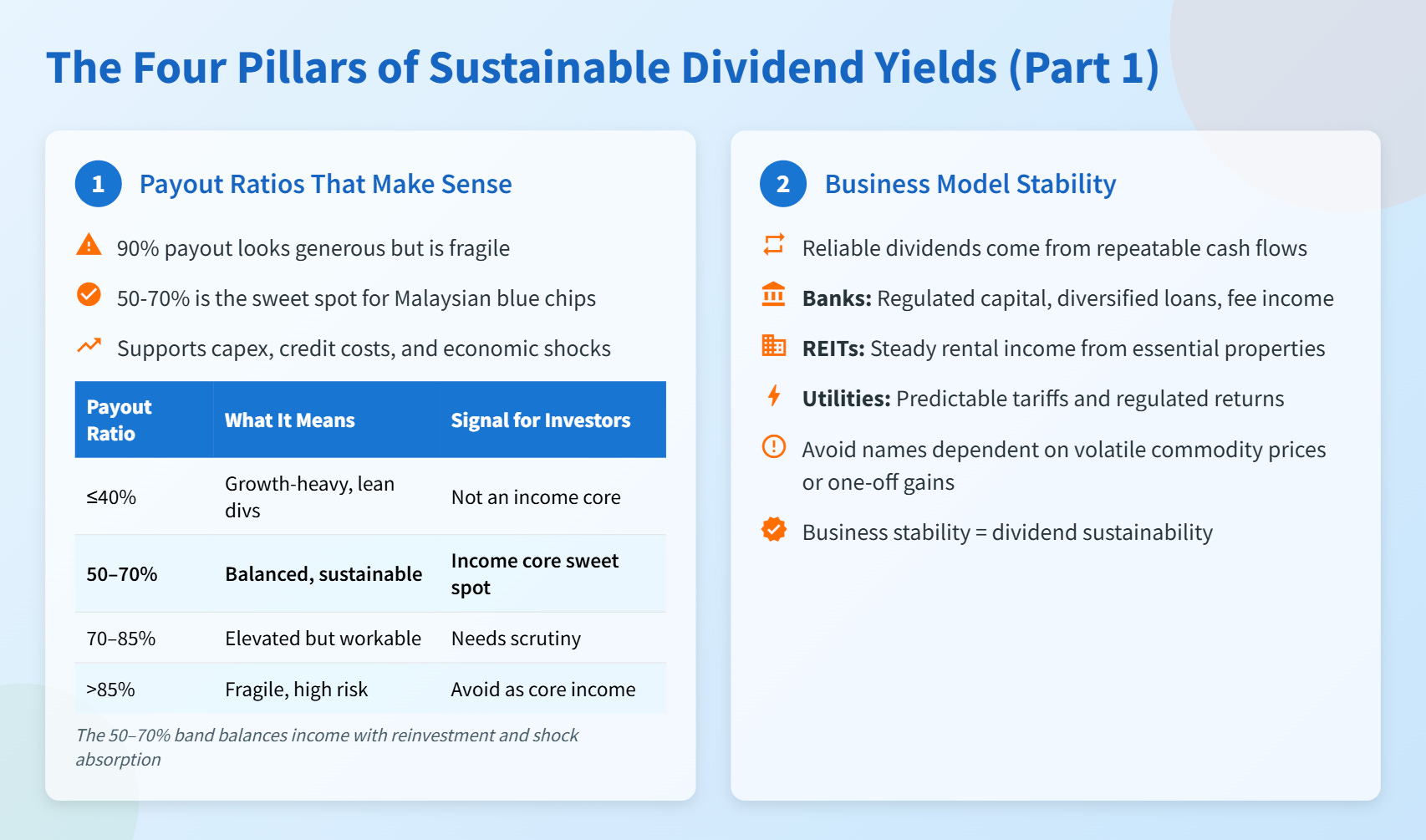

The Four Pillars of Sustainable Dividend Yields

Pillar 1: Payout Ratios That Make Sense

A 90% payout looks generous. It’s not. It’s fragile. For Malaysian blue chips, 50–70% is the lane. It supports capex, credit costs, and shocks. Public Bank and CIMB tend to sit in this zone. RHB is similar. Maybank runs higher but offsets with size, diversification, and a reinvestment plan.

Use this compass to score dividend resilience. The 50–70% band balances income with reinvestment and shock absorption. Above 80% needs caution unless the balance sheet is very strong and cash flows are ultra-stable.