Lendlease REIT (LREIT) 1H FY2026 Results Deep Dive

The Financial Engineering Shield Meets the Valuation Wall

The 1H FY2026 results for Lendlease Global Commercial REIT (LREIT) present a notable divergence: while the distribution metrics have expanded, institutional quantitative models suggest a valuation premium that warrants forensic scrutiny.

Addressing our Elite 170 high-conviction investors, we are navigating the “Year of the Fire Horse.” In a market where momentum can mask structural fragility, your “Institutional Asian Uncle” is here to audit the fortress. We don’t just look at the dividends; we evaluate the structural capacity of the balance sheet to absorb 2026 interest rate volatility.

In This Article:

The Slide-by-Slide Audit (Deep Dive)

The P&L Pivot: Magic in the Margins

Portfolio Reshuffle: Trading Stability for Retail Beta

The Capital Audit: Thin Ice on Interest Coverage

The “Reality Check” (InvestingPro Analysis)

The Performance Scorecard

InvestingPro Reality Check

Iggy's VerdictAbout Iggy & the Elite 170

🦎 Join the Inner Circle: Optimize Your Informational Latency: In the Singapore market, the gap between a calculated entry and becoming a liquidity provider for others is often just 48 hours. While 5,800+ readers wait two weeks for the “Old News” version, my Inner Circle observes the data while the market structure is still evolving.

🚨 Mitigate Informational Lag: Free subscribers wait 14 days to see my analysis. In this jungle, informational asymmetry is a primary driver of portfolio variance. Access the data while the market dynamics are still being priced in.

Choose Your Edge:

⚡ Zero-Day Access: Observe every deep-dive video the second it’s rendered. No delays, no missed data points.

📂 The Forensic Vault: Access the full forensic reports and portfolio walkthroughs where I strip away the corporate hype to reveal the hard math behind every Singapore blue chip.

💎 The “Smart Money” Bundle: Secure the full S$9/mo Pass (YouTube + Substack).

It’s a nominal overhead—less than the cost of two coffees at Toast Box—to analyze the market with the same datasets as institutional participants.

Get the data while it’s fresh. 👉 Join the Inner Circle Here

The Slide-by-Slide Audit (Deep Dive)

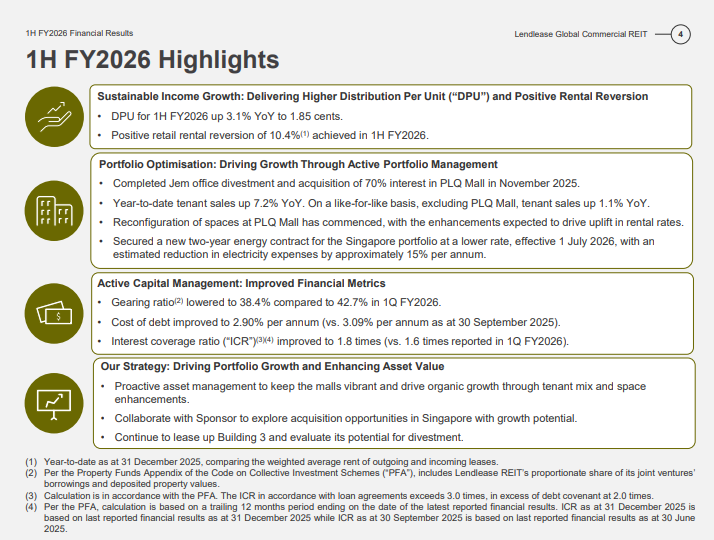

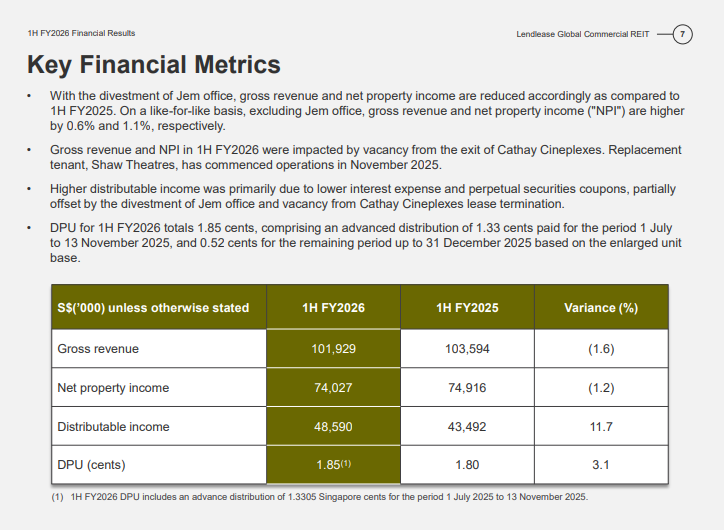

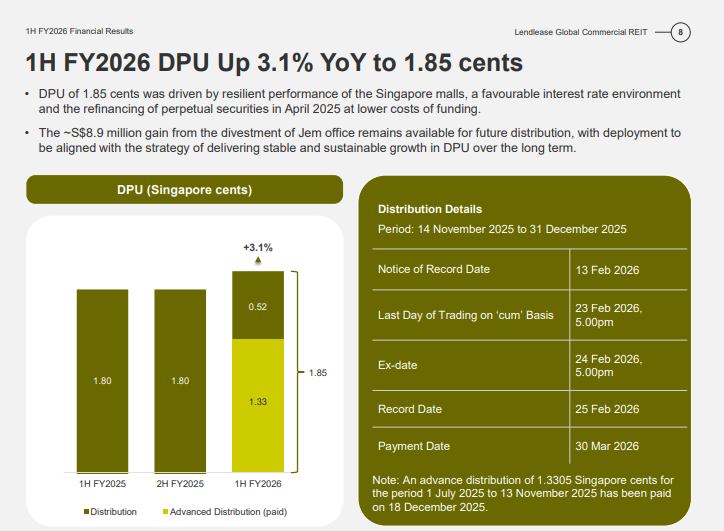

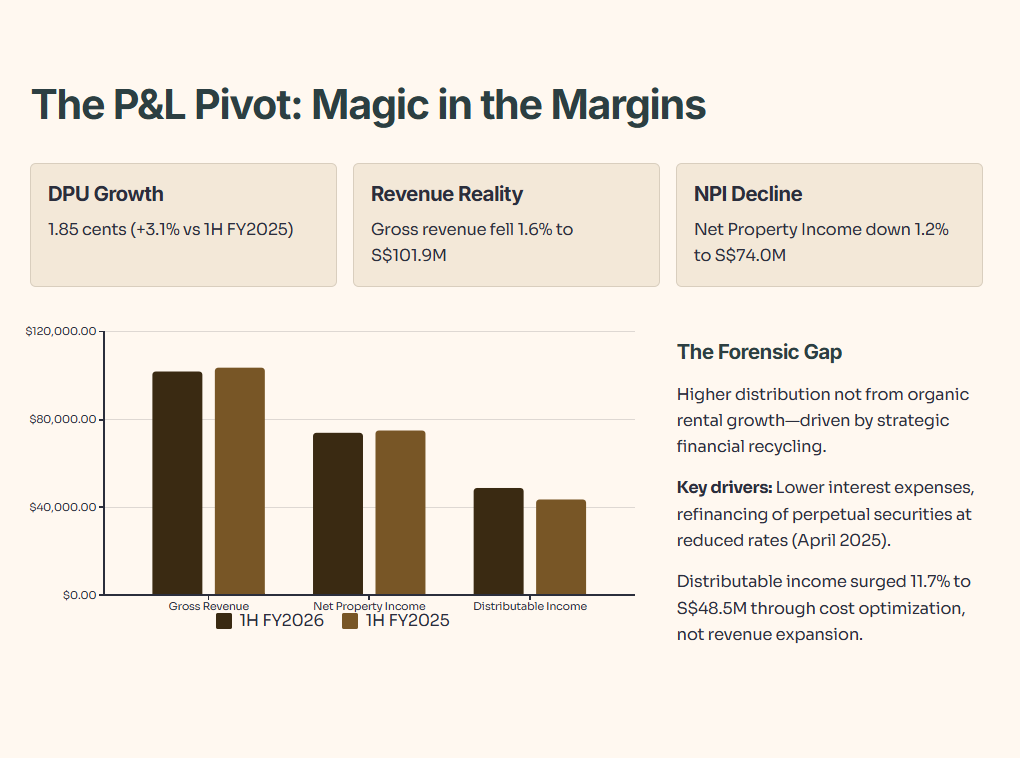

(Ref: Slide 4, 7, 8) The P&L Pivot: Magic in the Margins

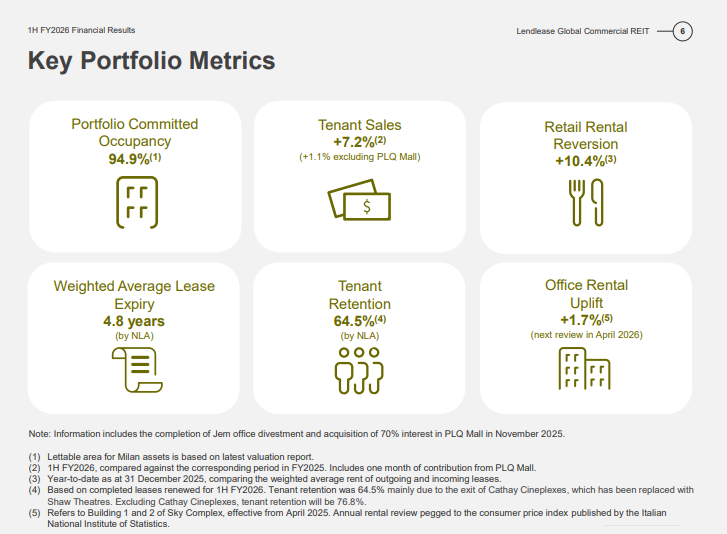

Management has delivered a Distribution Per Unit (DPU) of 1.85 cents for 1H FY2026, which is a 3.1% increase over the 1.80 cents paid in 1H FY2025. However, the “Forensic Gap” appears in the top line. Gross revenue actually fell 1.6% to S$101.9 million, and Net Property Income (NPI) dipped 1.2% to S$74.0 million. This retreat was primarily due to the strategic divestment of the Jem office and a vacancy period following the exit of Cathay Cineplexes. The “Wallet Impact” here is that the higher distribution is not primarily a function of organic rental growth; rather, it is a result of strategic financial recycling. Specifically, lower interest expenses and the refinancing of perpetual securities at lower coupon rates in April 2025 provided the lift needed to boost distributable income by 11.7% to S$48.5 million.

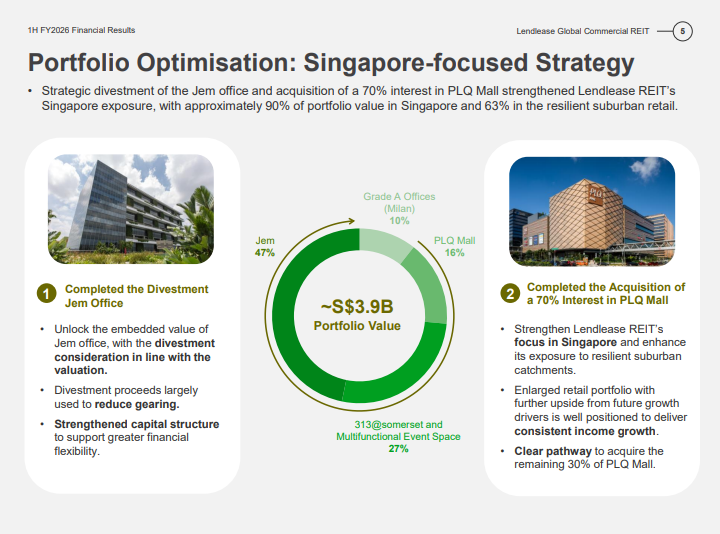

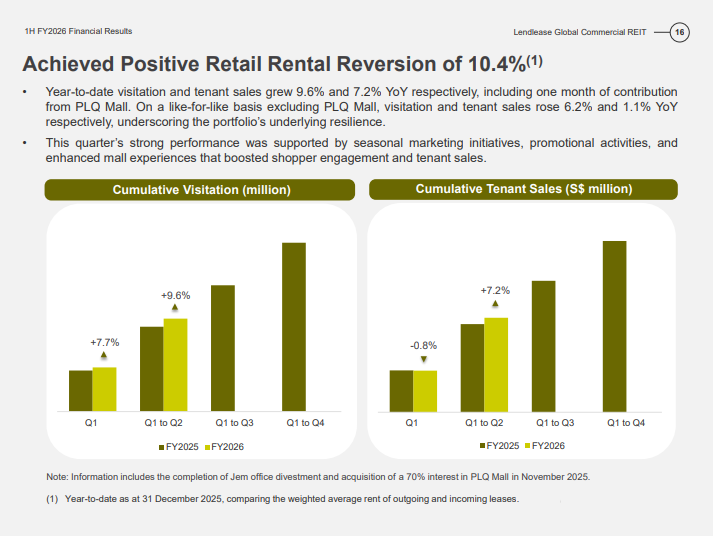

(Ref: Slide 5, 6, 16) Portfolio Reshuffle: Trading Stability for Retail Beta

The strategic shift to a Singapore-focused titan is now nearly complete, with approximately 90% of the S$3.9 billion portfolio value now anchored locally. By divesting the Jem office and acquiring a 70% interest in PLQ Mall, the REIT has leaned heavily into the resilient suburban retail segment, which now makes up 63% of the asset class mix. Retail rental reversion remains a highlight at 10.4%, supported by strong tenant sales which rose 7.2% year-on-year. However, when you remove the new PLQ contribution, like-for-like tenant sales growth was a mere 1.1%. This suggests that organic growth velocity is moderating, and the REIT is increasingly reliant on acquisitions and asset reconfiguration—such as the works currently underway at PLQ Mall—to sustain future rent uplifts.

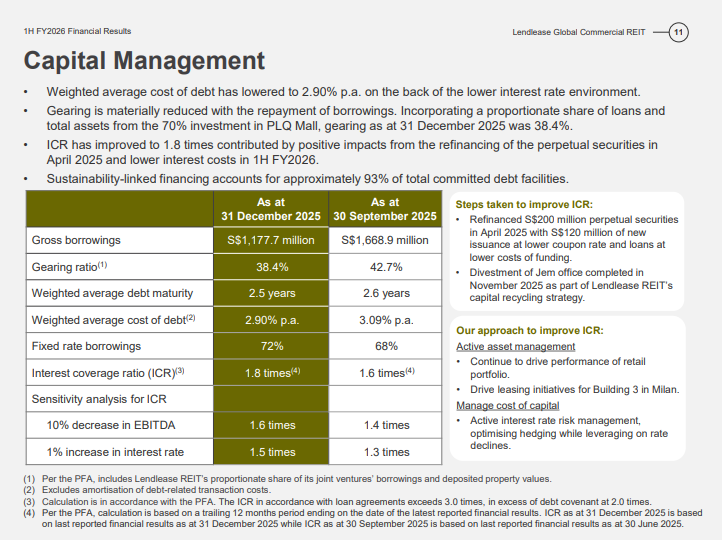

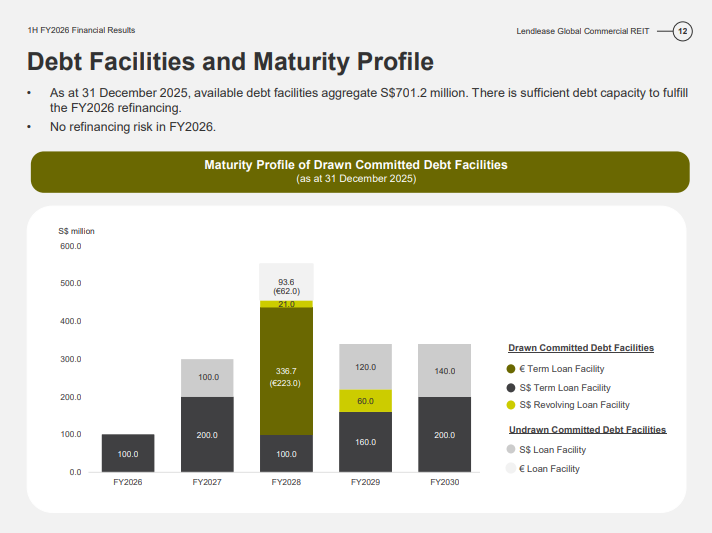

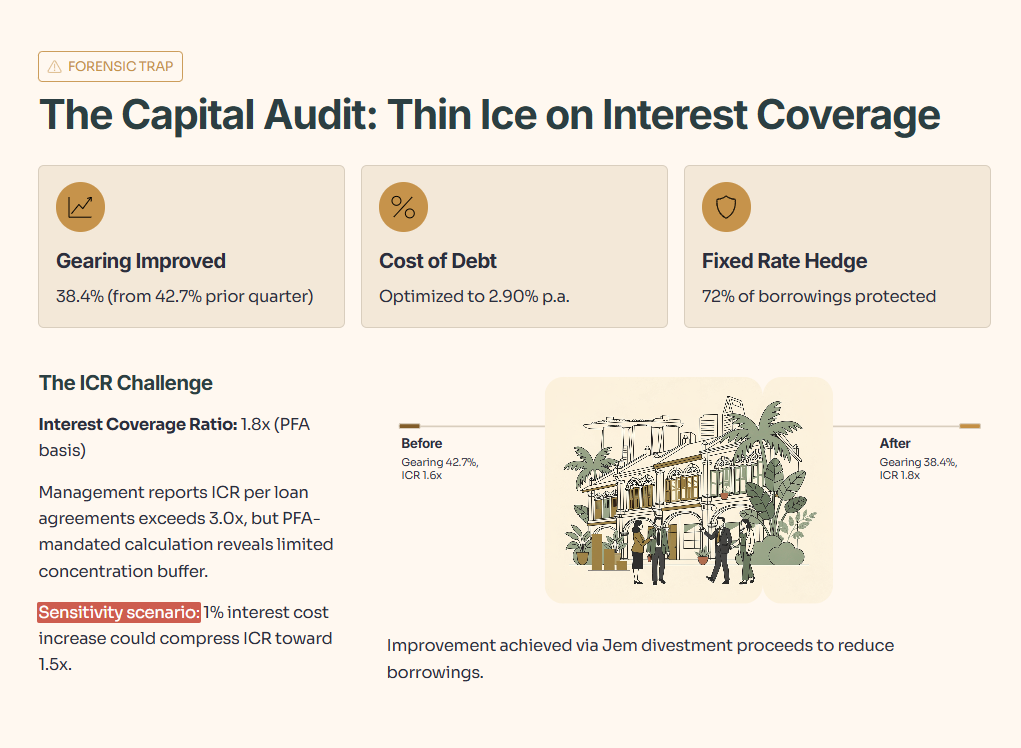

(Ref: Slide 11, 12) The Capital Audit: Thin Ice on Interest Coverage

We must audit the “Iron Bastion” of the balance sheet. Management successfully lowered the gearing ratio to 38.4% from the 42.7% seen in the previous quarter, largely by using Jem divestment proceeds to prune borrowings. The weighted average cost of debt has also been optimized down to 2.90% per annum. Despite these efforts, the Interest Coverage Ratio (ICR) remains a “Forensic Trap” at 1.8 times. While management notes that the ICR per loan agreements exceeds 3.0 times, the PFA-mandated calculation of 1.8x leaves a limited “Concentration Buffer” for our SAN Score calculation. In a hypothetical scenario where interest costs rise by 1%, the mathematical sensitivity suggests the ICR could compress toward 1.5 times.

The “Reality Check” (InvestingPro Analysis)

“The dividend story looks fine on the slides—but the institutional fair value model is flashing a number so extreme it changes how you should think about this REIT’s ‘safety’ overnight.”