Leong Guan IPO: The <50% Efficiency Warning

The noodle maker’s debut was tasty, but for durable returns, we need to see the “ingredients” first.

If you’re new here, welcome—The Investing Iguana just hit 1.3 million reads and 65,000 likes. We’re thrilled to welcome our growing community of over 48 YouTube Premium subscribers and 22 paid Substack members. We landed 8th in Tiger Brokers’ 2024 Influential Tigers ranking. Since October 2025, I’ve produced over 1,200 videos and more than 600,000 watch hours. If you want deeper context and a sharper edge in Singapore’s markets, you’re right where you need to be.

Is the Drought Finally Over?

Singapore’s IPO market has been quieter than a library on a Sunday morning. It has been silent. It has been dry. So, when a company like Leong Guan listed on the SGX Catalist board and immediately popped above its offer price, heads turned. People woke up. The noodle manufacturer listed at 23 cents and closed its debut day higher, sitting roughly around 24.5 cents.

In a market starved for action, it is tempting to chase the only thing moving. You see green on the screen, and you want to be part of it. But here is the problem, and I need you to listen closely. A listing pop driven by a low number of available shares is very different from real price growth driven by solid earnings.

So, is this a trap? Is this the start of a new bull run for small companies? Or is this a classic case where retail investors rush in, only to get stuck holding the bag months later? The stakes are real. We are talking about the risk of getting stuck with a stock you can’t sell in a portfolio meant for your safety or retirement.

We need to look past the hype. We need to look past the first-day excitement. Because the noodle maker’s debut was tasty, sure. But for long-term returns, we need to inspect the ingredients first.

In This Article:

• The Deep Dive: Anatomy of the Listing

• Data Check: The IPO “Blind Spot”

• What to Monitor Next: The Margin Squeeze

• The Investor’s Playbook

• Iggy’s Verdict

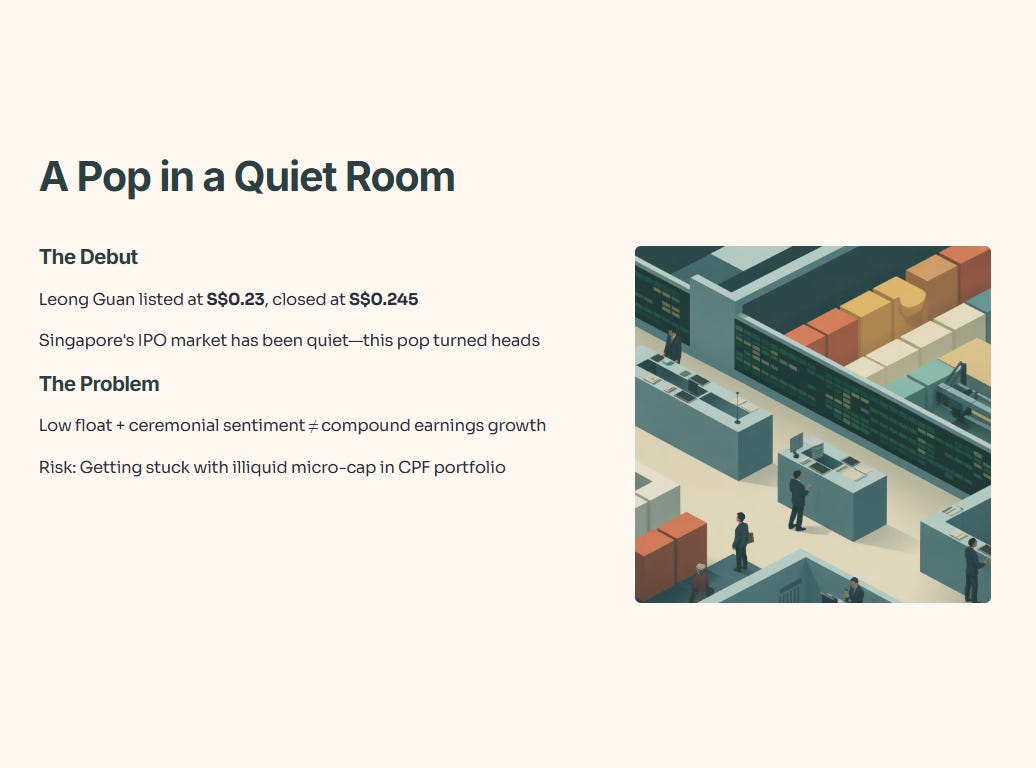

The Hook: A Pop in a Quiet Room

Singapore’s IPO market has been quieter than a library on a Sunday morning, so when Leong Guan (SGX: Catalist) lists and immediately pops above its offer price, heads turn. The noodle manufacturer listed at S$0.23 and closed its debut day higher at roughly S$0.245.

In a market starved for action, it’s tempting to chase the only thing that’s moving. But here is the problem: A listing pop driven by low float and “ceremonial” sentiment is very different from a price appreciation driven by compound earnings growth. The stakes? Getting stuck with an illiquid micro-cap in a CPF portfolio that was meant for safety.

The Deep Dive: Anatomy of the Listing

Let’s strip away the excitement and look at the mechanics of this listing. This isn’t just about noodles; it’s about market structure.

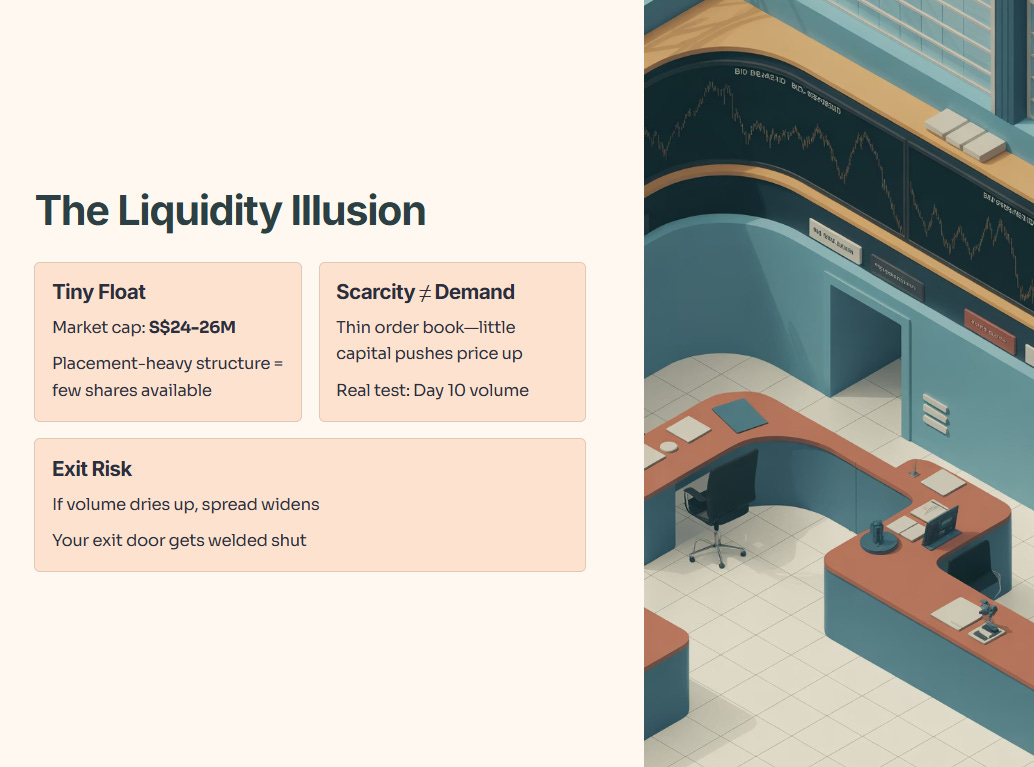

1. The Liquidity Illusion

The stock opened at S$0.245, a premium to its S$0.23 offer. Why? Because the float is tiny. With a post-IPO market cap estimated around S$24–26 million and a placement-heavy structure, there simply aren’t many shares floating around for retail traders on Day 1.

Iggy’s Insight:

Don’t mistake “scarcity” for “demand.” When a micro-cap lists with a small float, it takes very little capital to push the price up. This is a “thin” order book. The real test isn’t the listing day pop; it’s Day 10 volume. If volume dries up, that spread widens, and your exit door gets welded shut.

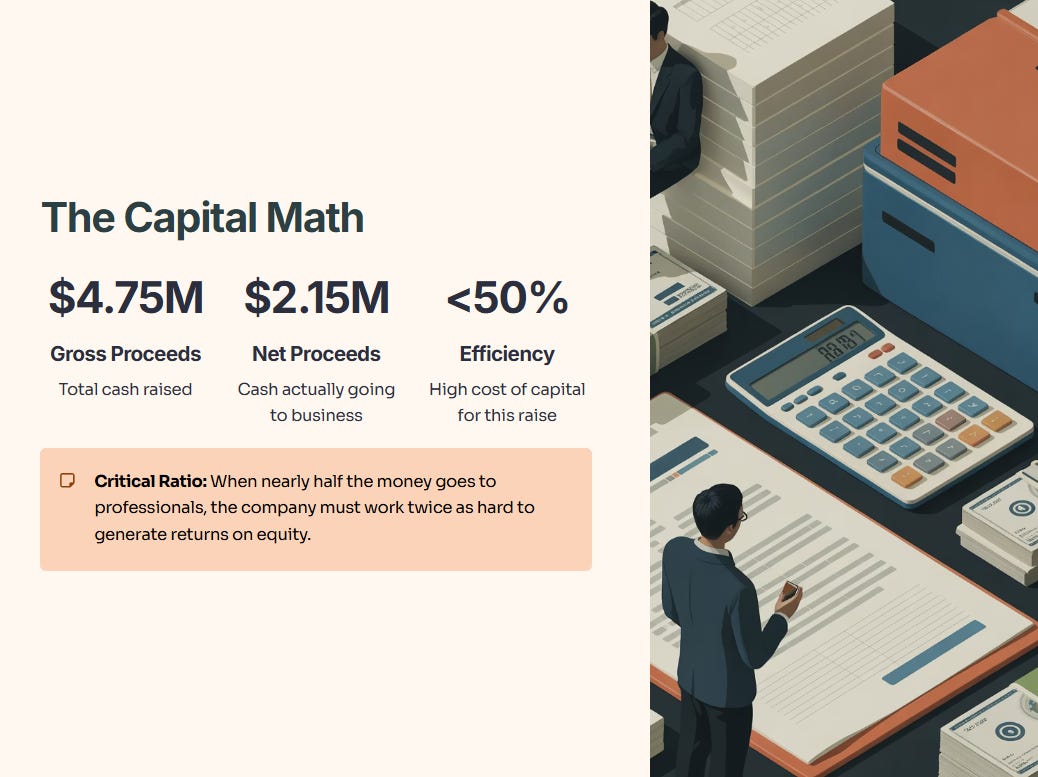

2. The Capital Math

Leong Guan raised roughly S$4.75 million gross. But after listing expenses, the **net proceeds** are only about S$2.15 million.

This is a critical ratio. When nearly half the money raised goes to paying the professionals (sponsors, lawyers, placement agents), the company has to work twice as hard to generate a return on that equity.

3. The Macro Tailwind

The timing was lucky. The Fed cut rates by 25bps this week (the third cut of 2025). This lowers the risk-free rate and generally pushes capital toward riskier assets like equities. However, a divided FOMC suggests the “easy money” taps aren’t opening fully yet.

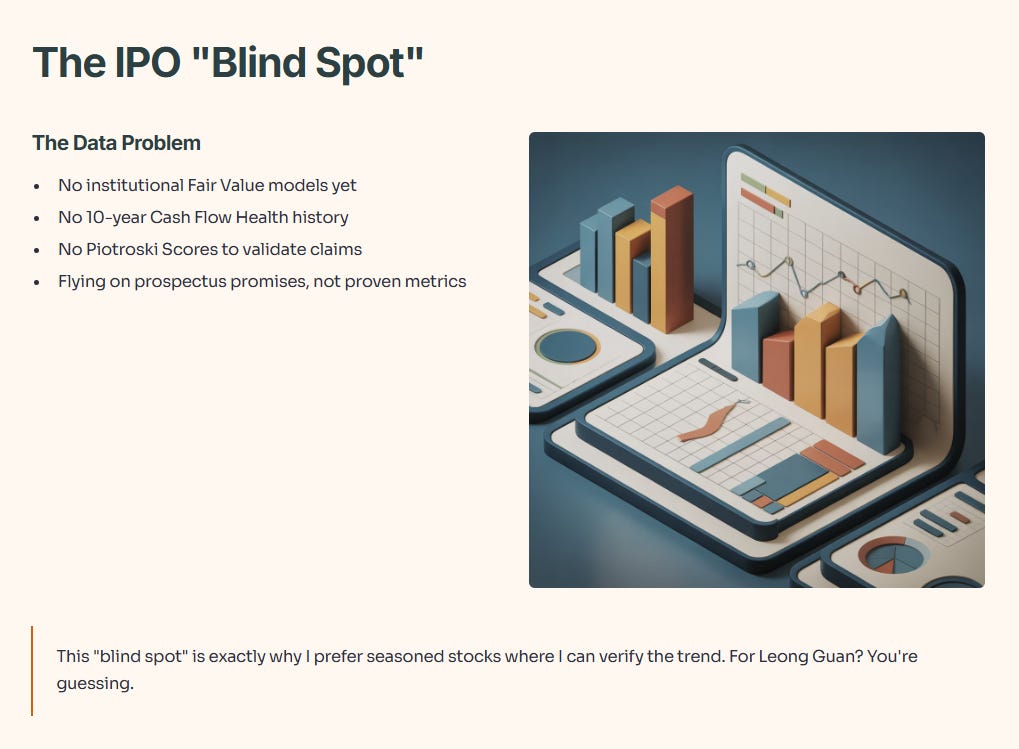

Data Check: The IPO “Blind Spot”

Usually, I run every stock analysis through InvestingPro to check the institutional Fair Value models and Financial Health scores.

But here is the trap with fresh IPOs: The data isn’t there yet.

Because Leong Guan is brand new to the board, the institutional models haven’t populated. We don’t have a 10-year history of Cash Flow Health or Piotroski Scores to validate their claims. We are flying on prospectus promises, not proven metrics.

Iggy’s Insight: This “blind spot” is exactly why I prefer seasoned stocks where I can verify the trend. For the rest of your portfolio (your DBS, your Genting, your REITs), you should be checking the Health Scores to ensure you aren’t holding a value trap. But for Leong Guan? You’re guessing.

Note: For your established holdings, you can use code INVESTINGIGUANA for up to 50% off InvestingPro to see the data that is available.

What to Monitor Next: The Margin Squeeze

The business model is simple: buy flour/soy, make noodles, sell noodles. But simple doesn’t mean easy.

Gross Margin Trend: This is the swing factor. Flour and energy costs are volatile. If input costs rise and Leong Guan can’t pass that on to customers (pricing power), their gross margins will compress.

Cash Conversion: Watch their inventory turns. Are they selling noodles faster than they are paying for flour? If not, that S$2.15 million in net proceeds will burn up just funding working capital.

Iggy’s Take:

Keep an eye on “Capex Creep.” They plan to use proceeds for manufacturing upgrades. In my experience with SGX manufacturing micro-caps, there is a risk that they spend money on new machines that don’t immediately result in higher sales. That leads to “stranded assets” and lower Return on Equity (ROE).

The Investor’s Playbook

So, what do we do? We don’t rely on hope. We rely on rules.