LHN Limited: 3 Reasons to Be Excited and 3 Forensic Red Flags (The Honest Audit)

A shrinking yield meets an aggressive asset-light pivot as a traditional landlord attempts a high-wire balancing act.

Welcome back to the forensic lab, Iggy’s Elite Investors.

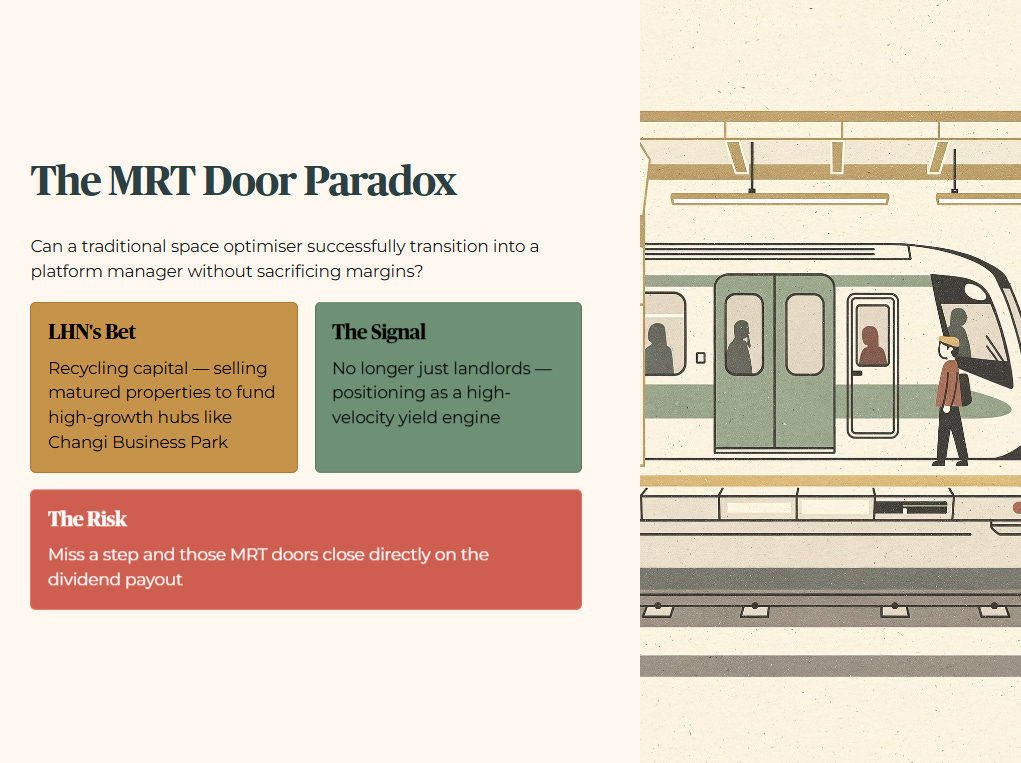

The physical tension in the Singapore mid-cap space right now is centred on one fundamental question. Can a traditional space optimiser successfully transition into a platform manager without sacrificing its margins and punishing its shareholders? LHN Limited (SGX: 41O) is currently attempting exactly this high-wire act, and the market is watching closely.

Think of it as the MRT Door Paradox. In Singapore, when the MRT doors are flashing red and closing, you have a split-second decision to make. Do you sprint and risk getting wedged between the heavy doors, or do you stand back, wait for the next train, and accept being late for work? LHN is sprinting. By recycling capital — selling matured properties to fund high-growth hubs like Changi Business Park — management is signalling they are no longer just landlords. They want to be a high-velocity yield engine.

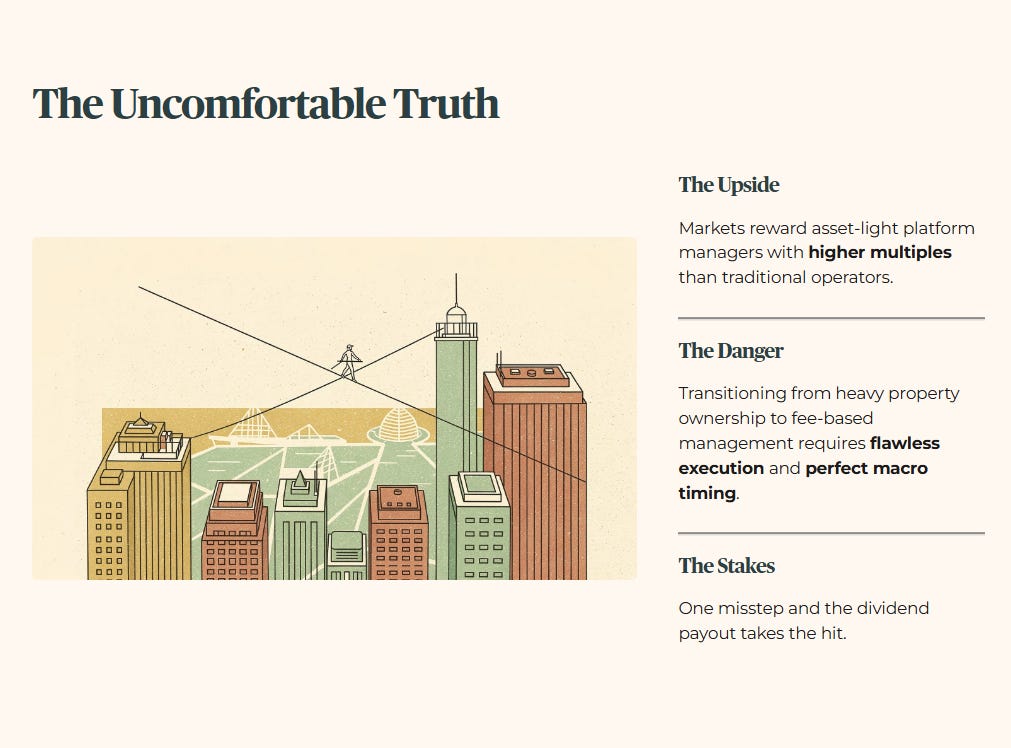

And let us be honest, they are not wrong to attempt this. The broader market historically rewards asset-light platform managers with higher multiples than traditional brick-and-mortar operators. But here is the uncomfortable truth: transitioning from heavy property ownership to fee-based management is notoriously difficult. It requires flawless operational execution and perfect macroeconomic timing. If they miss a step, those MRT doors will close directly on their dividend payout.

Let us dive straight into the forensic data.

In This Article:

The Financial Snapshot (The Baseline)

Financial Health Checklist

Iggy's Insight

Good 1: The Coliwoo Occupancy Fortress (96.5%)

Good 2: The Changi Business Park Strategic Moat

Good 3: The Facilities Management (FM) Multiplier

Red Flag 1: The Work+Store Occupancy Drop

Red Flag 2: The Debt Wall vs. S$101M Commitment

Red Flag 3: The Asset-Light Valuation Trap

The Singaporean Context (The Iggy Stress-Test)

Iggy's Insight

The Weighing Scale

Profile Match

LHN Limited: Forensic Stance — Watchlist Trigger

Peer Comparison & Valuation Table

Iggy's Conclusion

InvestingPro Reality Check

The Verdict

About Iggy & the Elite Investors

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

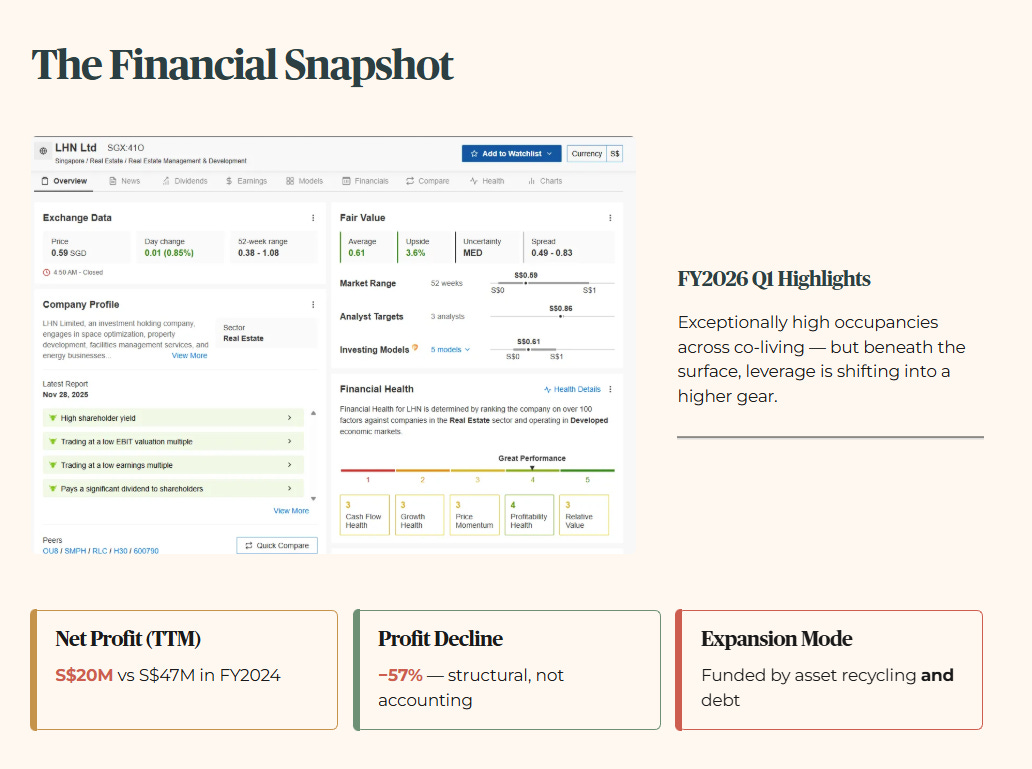

The Financial Snapshot (The Baseline)

Before we debate the forward-looking narrative, we must anchor ourselves entirely to the raw, verified data. In their FY2026 Q1 update, LHN reported exceptionally high occupancies across their core co-living segments, but beneath the glossy surface, the leverage dynamics are shifting into a higher gear. We are observing an aggressive expansion phase funded by a complex mix of asset recycling and debt. Net profit has declined sharply — from S$47M in FY2024 to S$20M in the trailing twelve months to September 2025, a 57% contraction that the headline occupancy figures do not reveal.

“Don’t overpay for the hype. See the math behind the momentum.” .....Use the Fair Value models I use in every video. Code INVESTINGIGUANA gets you 50% off the world’s most powerful stock screener.

🦎 [Spot Undervalued Gems Here]

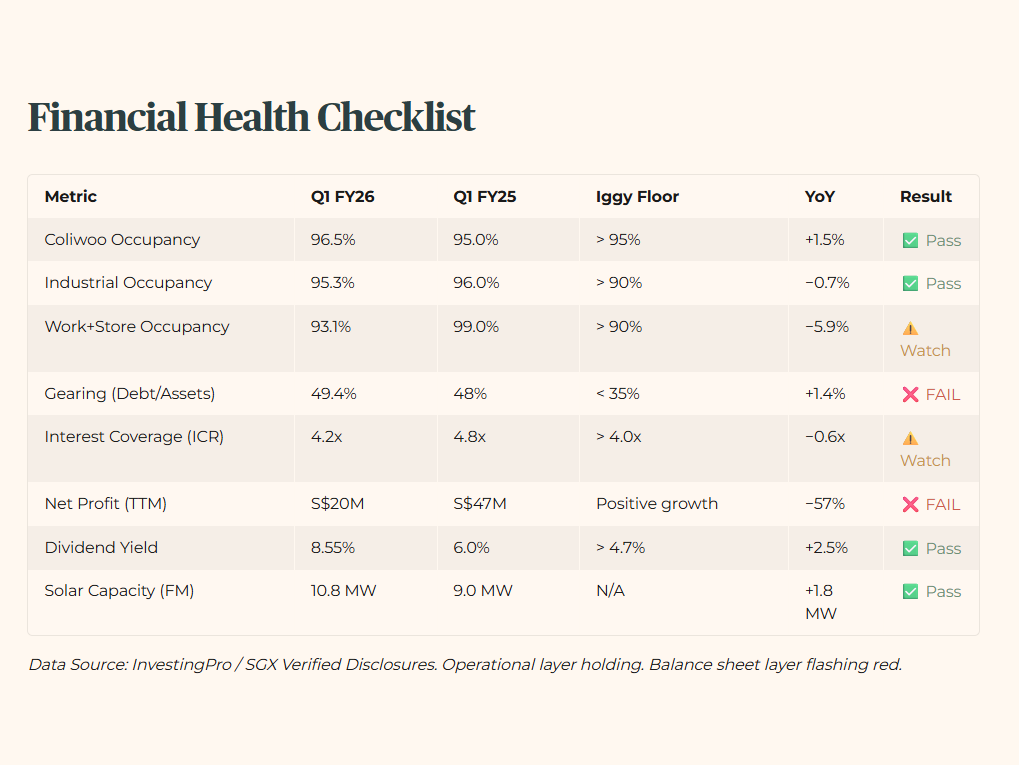

Financial Health Checklist

Data Source: InvestingPro / SGX Verified Disclosures.

The checklist tells a split story. The operational layer — occupancy, ICR, yield — is holding. The balance sheet layer — gearing and profit trajectory — is flashing red. At 49.4% debt-to-assets, LHN is operating well above our forensic ceiling, and the 57% profit decline confirms this is not a temporary accounting artefact. This is structural margin compression playing out in real time.

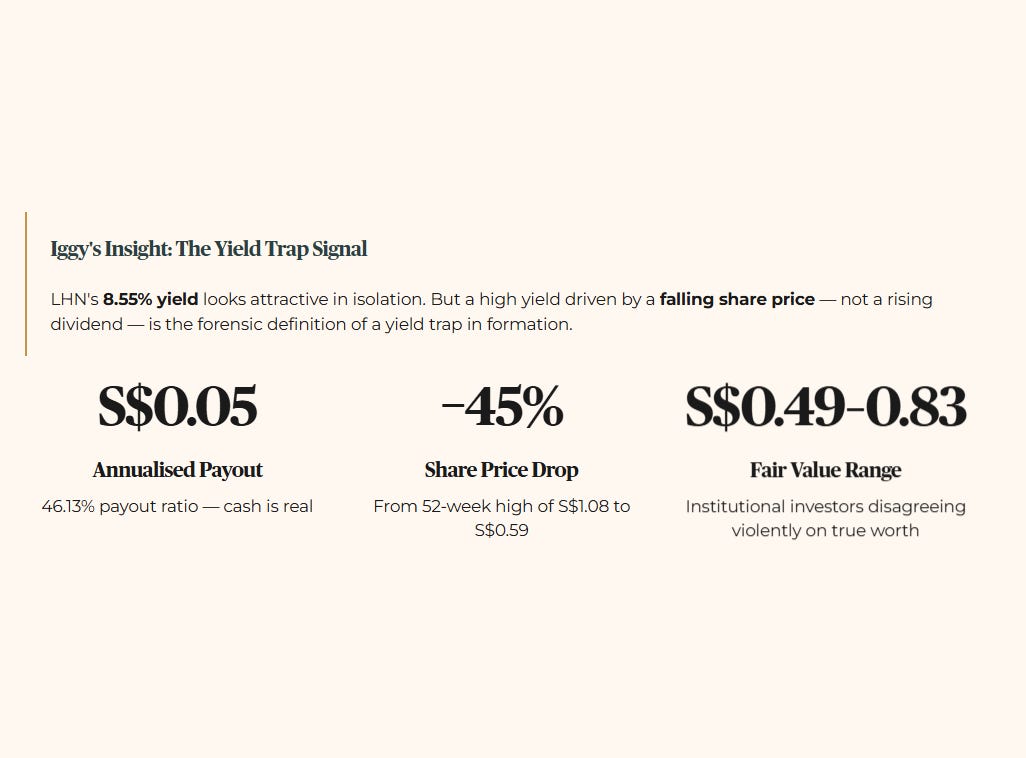

Iggy’s Insight LHN’s 8.55% yield looks attractive in isolation. But a high yield driven by a falling share price — not by a rising dividend — is the forensic definition of a yield trap in formation. The annualised payout is S$0.05, with a 46.13% payout ratio. The cash is real. But the share price has declined from a 52-week high of S$1.08 to S$0.59 — a 45% compression — and the market’s uncertainty band on fair value runs from S$0.49 to S$0.83. That range is the sound of institutional investors disagreeing violently about what this company is actually worth.

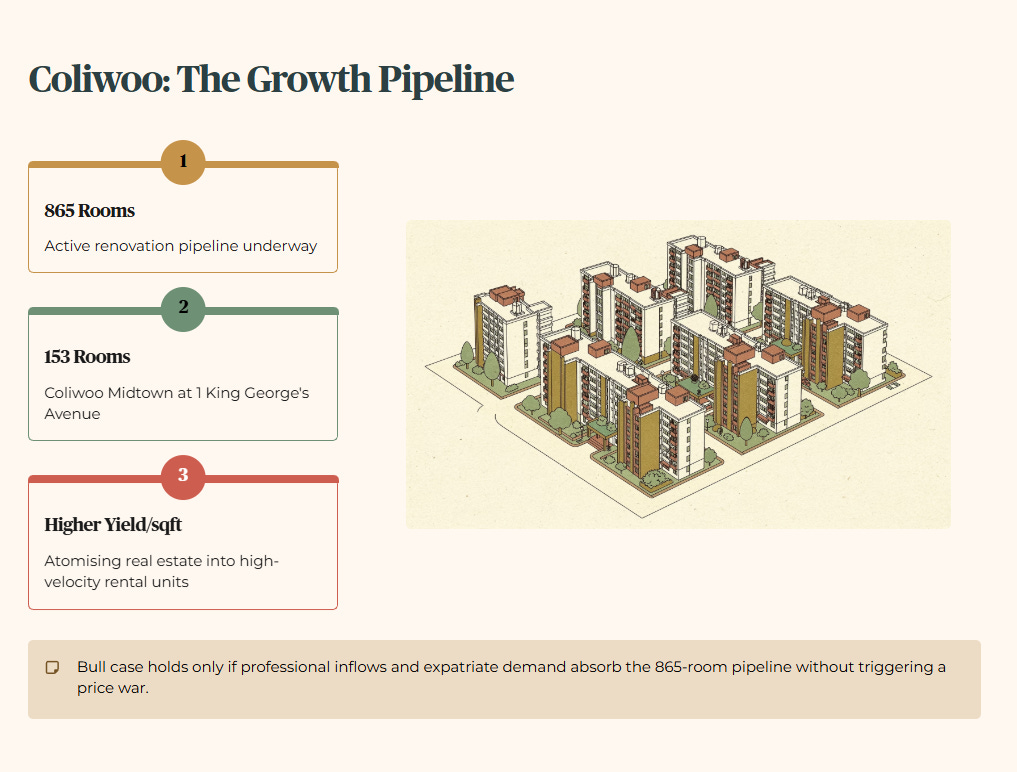

Good 1: The Coliwoo Occupancy Fortress (96.5%)

Co-living is no longer a niche, experimental housing alternative for young expatriates. It has evolved into the primary sanctuary for Singapore’s professional demographic. At 96.5% occupancy, the Coliwoo brand is operating at near-perfect efficiency.

The raw fact is compelling. Coliwoo manages 3,200 active rooms across Singapore, maintaining a 96.5% occupancy rate. Historically, this performance smashes their trailing averages and proves that management can significantly scale their room count without diluting tenant demand. In peer context, traditional residential landlords and private condominium operators are fighting tooth and nail to maintain 90% occupancy amid a softening private rental market. Coliwoo is simply outperforming the traditional alternatives.

Looking forward, the growth engine remains fully throttled. They have 865 rooms in the active renovation pipeline, including the Coliwoo Midtown project at 1 King George’s Avenue, expected to add 153 rooms. By atomising traditional real estate into smaller, high-velocity rental units, they are extracting significantly higher yield per square foot. For the 50-plus Singaporean investor, this segment provides resilient, recurring cash flow that directly supports the corporate dividend payout.

Think of it exactly like the HDB BTO system. The wait times are so painfully long, and the open-market resale prices are so punitively high, that a massive cohort of young professionals is structurally locked out of homeownership. They urgently need high-quality, flexible housing. Coliwoo is standing right outside the MRT station, handing them the keys. It is a demographic tailwind that cannot be ignored.

This bull case holds only if Singaporean professional inflows and expatriate demand remain robust enough to absorb the incoming 865-room pipeline without triggering a price war.

(To verify whether this pipeline growth is currently priced into the market multiple, run the intrinsic value model on InvestingPro using discount code INVESTINGIGUANA.)

Good 2: The Changi Business Park Strategic Moat

The S$101 million acquisition at 2 Changi Business Park Ave 1 is a surgical strike. It is arguably the defining strategic move of their FY2026 playbook and fundamentally changes their operational footprint.

The raw fact is bold. LHN committed S$101 million to secure a hotel strata lot featuring more than 250 rooms in the heart of Changi Business Park. This ranks as one of the most aggressive single capital deployments the group has ever executed. Compared to SGX peers in the mid-cap space, most traditional property operators are playing defensive, hoarding cash, and shrinking their footprints. LHN is going on the offensive.

The forward scenario is significant. By securing this precinct, LHN is positioning itself as the primary housing provider for the upcoming Terminal 5 master construction wave. This is not a standard hospitality play. It is a logistics-adjacent worker housing strategy with a decade-long tailwind. The wallet impact is the high probability of locked-in, long-term corporate leases that bypass the daily volatility of the tourist market.

Changi Business Park is rapidly evolving into a self-sustaining economic node — a vital engine room for the eastern corridor. By planting a 250-room flag at its centre, LHN is building a toll bridge. Every major contractor working on T5 will require quality accommodation for their staff. LHN intends to collect that toll.

This bull case holds only if the T5 development timeline remains on schedule and corporate accommodation budgets do not contract materially.

Good 3: The Facilities Management (FM) Multiplier

While retail investors obsess over property acquisitions, the Facilities Management division is quietly building a cash flow floor that protects the entire enterprise.

In 1QFY2026, the FM subsidiary secured 14 new contracts and renewed 100 existing ones, serving 119 clients. They reached 10.8 MW of installed solar capacity. Free cash flow for the trailing twelve months to September 2025 came in at S$68M — recovering strongly from S$28M the prior year. This is not a secondary support function. It is a primary cash engine.

The forward scenario is driven by the energy transition. As more industrial landlords across Singapore are legislatively required to green their buildings, LHN’s FM division is positioned to capture those upgrade contracts. The recurring, service-based income stream acts as a forensic buffer, smoothing the lumpiness of traditional property development.

This is pure Kopitiam Logic. The FM division is the quiet neighbourhood minimart. It does not generate flashy headlines, but people buy bread and milk every day regardless of the macroeconomic weather. It prints cash consistently, providing the foundational stability the parent company needs to take bigger strategic risks elsewhere.

This bull case holds only if they can defend operating margins against rising foreign worker levies and labour shortages in the maintenance sector.

The numbers look powerful on the surface—but once you line up the three forensic red flags side by side, the 8.55% yield starts to look less like passive income and more like a warning label.