Mapletree Industrial: Buy The Dip or Sell Everything? (My Verdict)

Revenue is down, DPU has dropped 5.6%, and the payout ratio has breached 100%. Is this a buying opportunity, or is the “Industrial Darling” thesis broken?

If you rely on your CDP account for passive income—specifically using your CPF or SRS funds—the latest report from Mapletree Industrial Trust (MIT) likely felt like a cold shower.

For the last decade, MIT has been the “sleep well at night” stock. It was the boring, reliable proxy for Singapore’s industrial stability. But the latest half-year results (1H FY2025/26) have shattered that calm. Distributions are down, vacancies in the US are rising, and—most concerningly—the trust is currently paying out more cash than it is generating from operations.

The question on every Singaporean investor’s mind is simple: Is this a temporary stumble due to a strategic pivot, or is it a structural decline that threatens your long-term capital?

This report cuts through the management jargon to look at the mechanics of the dividend cut.

In This Article:

• The Financial Health Check: The “100% Rule”

• The Operating Momentum: The “Three-Pronged” Drag

• Iggy’s Analysis: The Good vs. The Ugly

• Iggy’s Insights: The “Alpha” Verdict

• My Verdict: HOLD (Do Not Average Down Yet)

• A Sound Conclusion: The Investor’s RoadmapThe Financial Health Check: The “100% Rule”

Let’s look at the cold hard numbers. On the surface, the valuation looks reasonable. But when you look under the hood at the Payout Ratio, the engine is overheating.

The “So What?” for Investors:

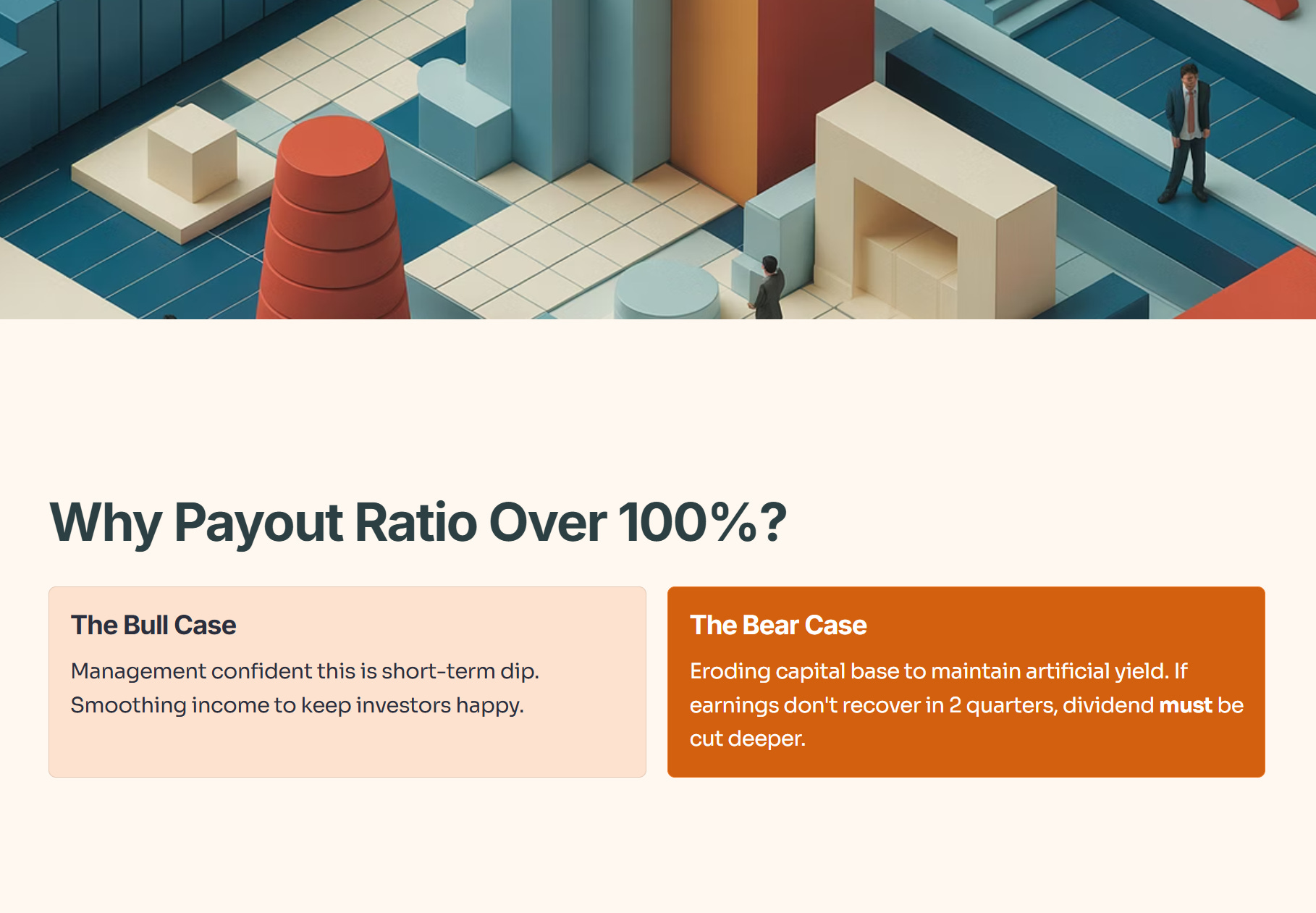

Why is the Payout Ratio over 100%? This usually happens when a REIT uses “capital distributions”—often from the proceeds of selling properties (divestments)—to “top up” the dividend.

The Bull Case: Management is confident this is a short-term dip, so they are smoothing income to keep investors happy.

The Bear Case: They are eroding their capital base to maintain an artificial yield. If earnings don’t recover in 2 quarters, the dividend must be cut deeper.

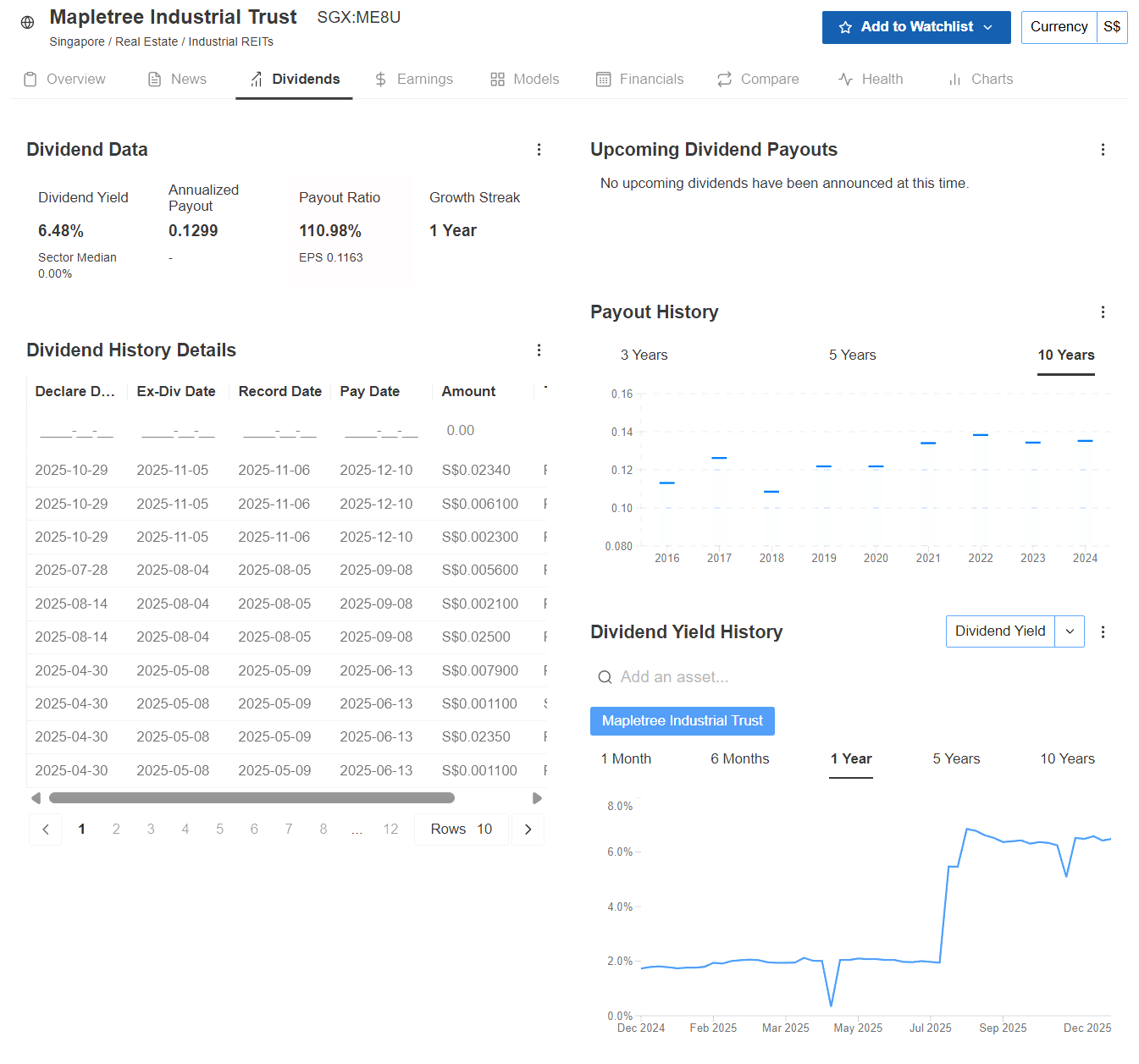

Chart: MIT’s 10-Year Payout History. Notice the dip in the latest bar? This is the DPU cut everyone is worried about. Source: InvestingPro (Use code INVESTINGIGUANA for up to 50% off).

Iggy’s Insights

Look at the bar chart above. See that small dip on the far right? That represents the recent DPU cut. Now, zoom out. Look at the steady climb over the last 10 years. Does this one small dip look like a crisis, or just a speed bump in a long-term uptrend? InvestingPro data shows the yield is still a healthy 6.48% (top left), which is well above the sector median.

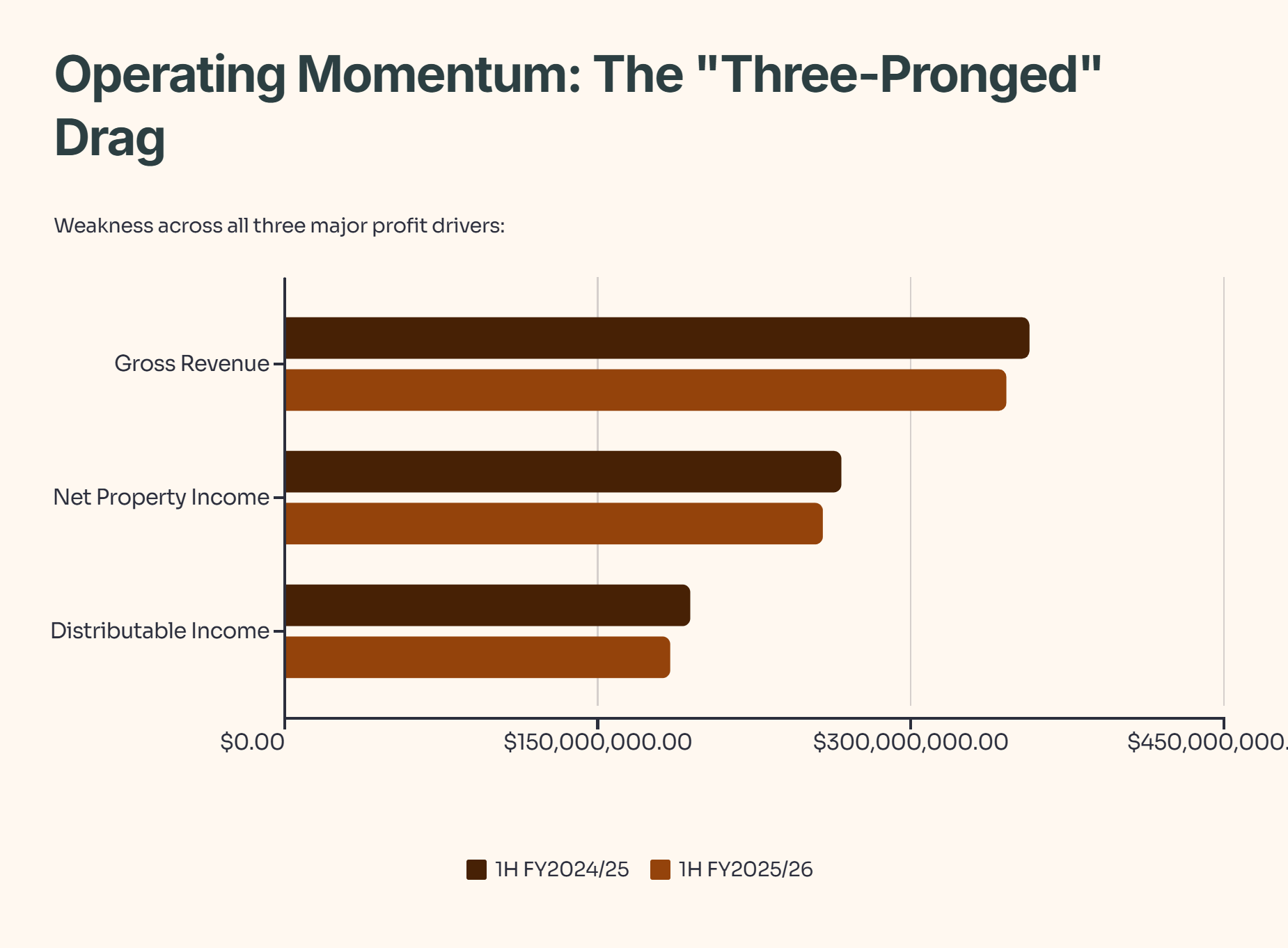

The Operating Momentum: The “Three-Pronged” Drag

We look at momentum to see if the bleeding is stopping. Unfortunately, the trend for the first half of the financial year shows weakness across all three major profit drivers.

Iggy’s Analysis: The Good vs. The Ugly

This isn’t a failing company. It is a blue-chip company attempting a difficult acrobatic maneuver: pivoting from “Old Industrial” to “New Tech” while the macro-economic winds are blowing against them.

The 3 Good: The Future Engine

The Japan “Safe Haven”: While the US struggles, MIT’s acquisition in Tokyo and the Osaka data centre (fit-out completed May 2025) are bright spots. Japan offers a unique environment: extremely low borrowing costs and stable, long-term tenants. This geographic diversification is saving the portfolio from a steeper drop.

Asset Recycling Discipline: MIT sold three older Singapore industrial properties (Tangent logistics, etc.). While this caused the immediate revenue dip, it is the correct long-term move. You do not want to hold decaying 30-year leasehold assets; you want to trade them for freehold data centres. It hurts now, but it builds value for later.

The “Boring” Singapore Core: The 83 properties in Singapore are the anchor. Flatted factories and business parks are not sexy, but they have high retention rates. This “boring” core is effectively subsidizing the “exciting” but volatile US expansion.

The 3 Red Flags: The Structural Drag

The US Office/Data Centre Trap: The North American portfolio is the primary culprit. We are seeing tenant non-renewals. In the US, when a tenant leaves a Data Centre or office park, the “switching costs” are high, meaning it takes a long time and high CAPEX (incentives) to lure a new tenant in.

The Strong Singdollar (Forex Pain): This is the hidden killer for Singaporean investors holding global REITs. As the SGD strengthens against the USD, every US Dollar of profit MIT earns is worth less when converted back to SGD for your dividend. You are losing money simply because the Singdollar is strong.

The “Higher for Longer” hangover: MIT’s average cost of debt is creeping up. Even with rate cuts on the horizon, refinancing old cheap loans (at 1-2%) with new loans (at 3-4%) will continue to compress margins for at least another 12 months.

Iggy’s Insights: The “Alpha” Verdict

Most analysts will simply tell you to “buy the dip” because it’s a Mapletree REIT. I believe we need to be more nuanced.