Mapletree Industrial Trust: 3 Good and 3 Red Flag

Like a fully paid-up 5-room HDB with no pocket money—safe house, but your cai fan getting more expensive.

You are sitting at your neighbourhood kopitiam. You stare at your shrinking paycheck and the ever-rising cost of your morning kopi peng. The Straits Times Index is hovering around the 5,000 mark as it continues the psychological battle for that resistance level. Everyone around you is hunting desperately for yield to beat the inflation creep.

Then you look at Mapletree Industrial Trust. It flaunts a very attractive headline forward yield. And let’s be honest, the bulls are not wrong to be drawn to it. But here is the uncomfortable truth: a high yield is only as good as the cash flow defending it. We need to strip away the market noise. We need to run the forensic math.

In This Article:

The Financial Snapshot

The 3 Good

Good 1: Resilience and Pricing Power in the Singapore Portfolio

Good 2: Institutional Grade Credit Stability

Good 3: The Successful Data Center Pivot

The 3 Red Flags

Red Flag 1: Imminent Revenue Churn in North America

Red Flag 2: Structural DPU Compression from the Debt Wall

Red Flag 3: Divestment-Induced Income Vacuum and NAV Erosion

The Singaporean Context

The Weighing Scale

InvestingPro Reality Check

The Verdict

About Iggy & the Elite Investors

The Crash Wasn’t a Surprise. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided before the opening bell — not after the damage is done. The red flags are always there. The question is whether you had the forensic framework to read them in time.

Iggy’s Elite Investors didn’t chase the headline yield. They had the full forensic breakdown — the gearing ratios, the occupancy gaps, the debt overhang — before the market opened and before the price moved. Zero-day reports, the complete “Red Zone” watchlist, and institutional-grade cheatsheets that flag the landmines disguised as opportunities.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

👉 Secure Your Seat in Iggy’s Elite Investors Here

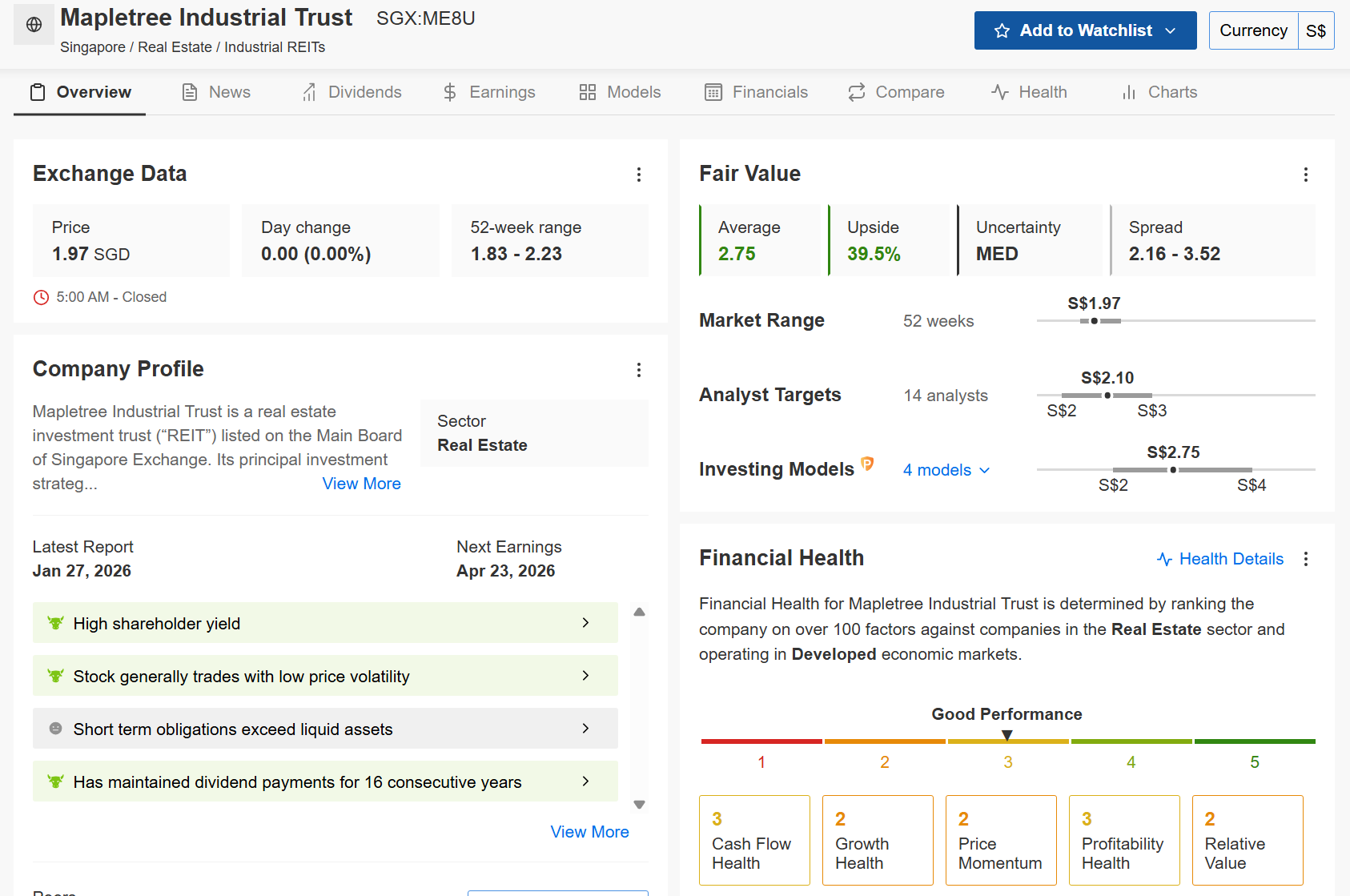

The Financial Snapshot (The Baseline)

Before we debate the future, we must establish the hard reality of the present. Mapletree Industrial Trust recently released its post-January 2026 earnings. The numbers present a fascinating contradiction between balance sheet strength and income statement weakness.

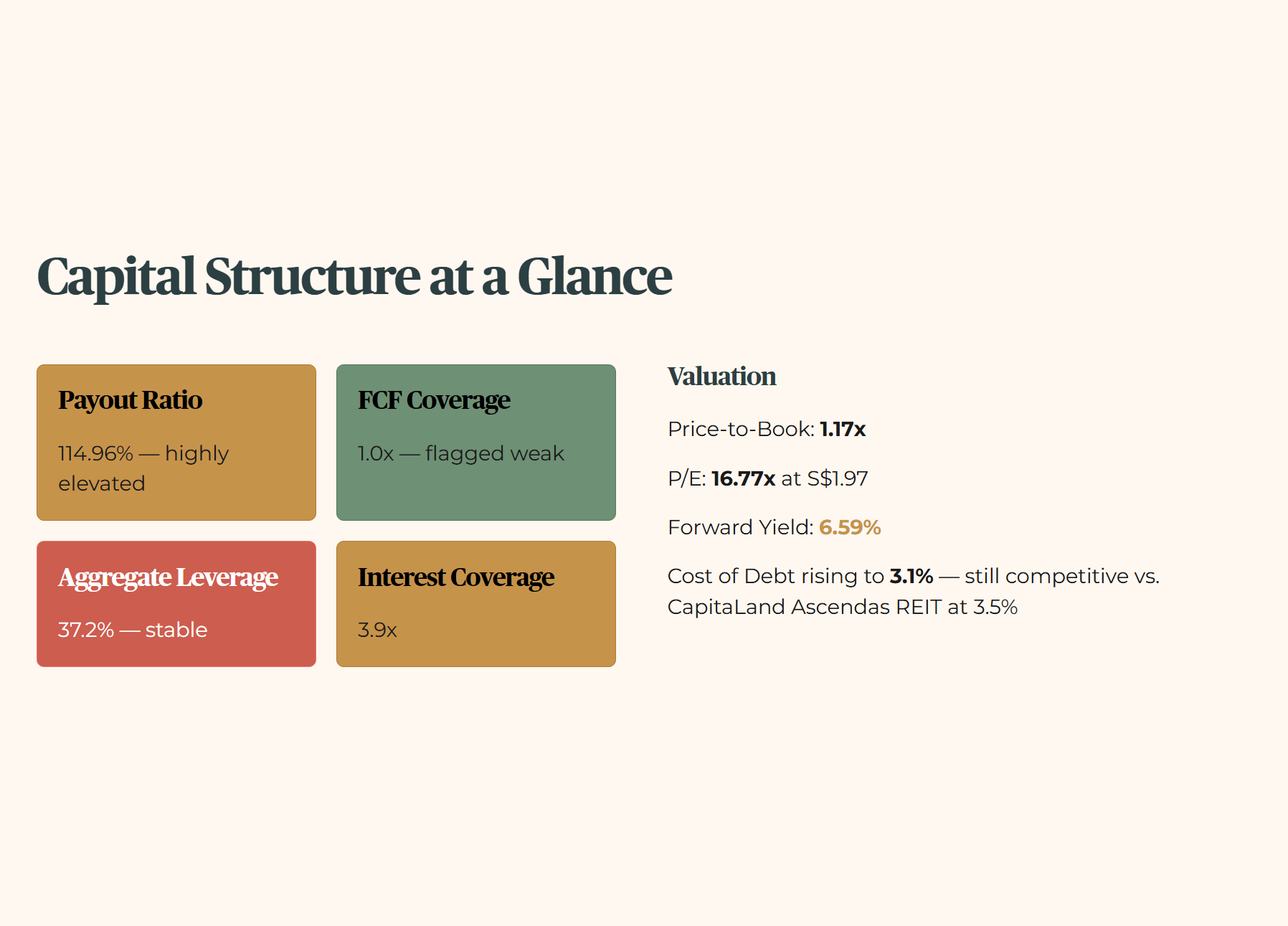

The numbers confirm what the headline yield was hiding. Gross Revenue sits at S$163.13 million, representing an 8.0% year-on-year decline. Net Property Income mirrors this pain, falling 7.8% to S$122.83 million. The EBITDA Margin remains functional at 66.8%, but the Free Cash Flow of S$447.71 million is contracting. This squeeze flows directly down to the Distribution Per Unit, which has tumbled 7.0% to 3.17 cents.

Consequently, the Payout Ratio has ballooned to a highly elevated 114.96%, backed by a free cash flow coverage flagged as weak at a mere 1.0x. Yet, the capital structure remains robust. Aggregate Leverage is managed at 37.2%, barely shifting from the prior 37.3%.

The Interest Coverage Ratio stands at 3.9x. The Cost of Debt is rising slightly to 3.1%, but remains competitive against peers like CapitaLand Ascendas REIT at 3.5%. Valuation-wise, the Price-to-Book Ratio is elevated at 1.17x, while the Price-to-Earnings ratio sits at 16.77x based on the latest S$1.97 pricing. And sitting on top of all that is the number everyone’s eyes land on first: a 6.59% forward yield.

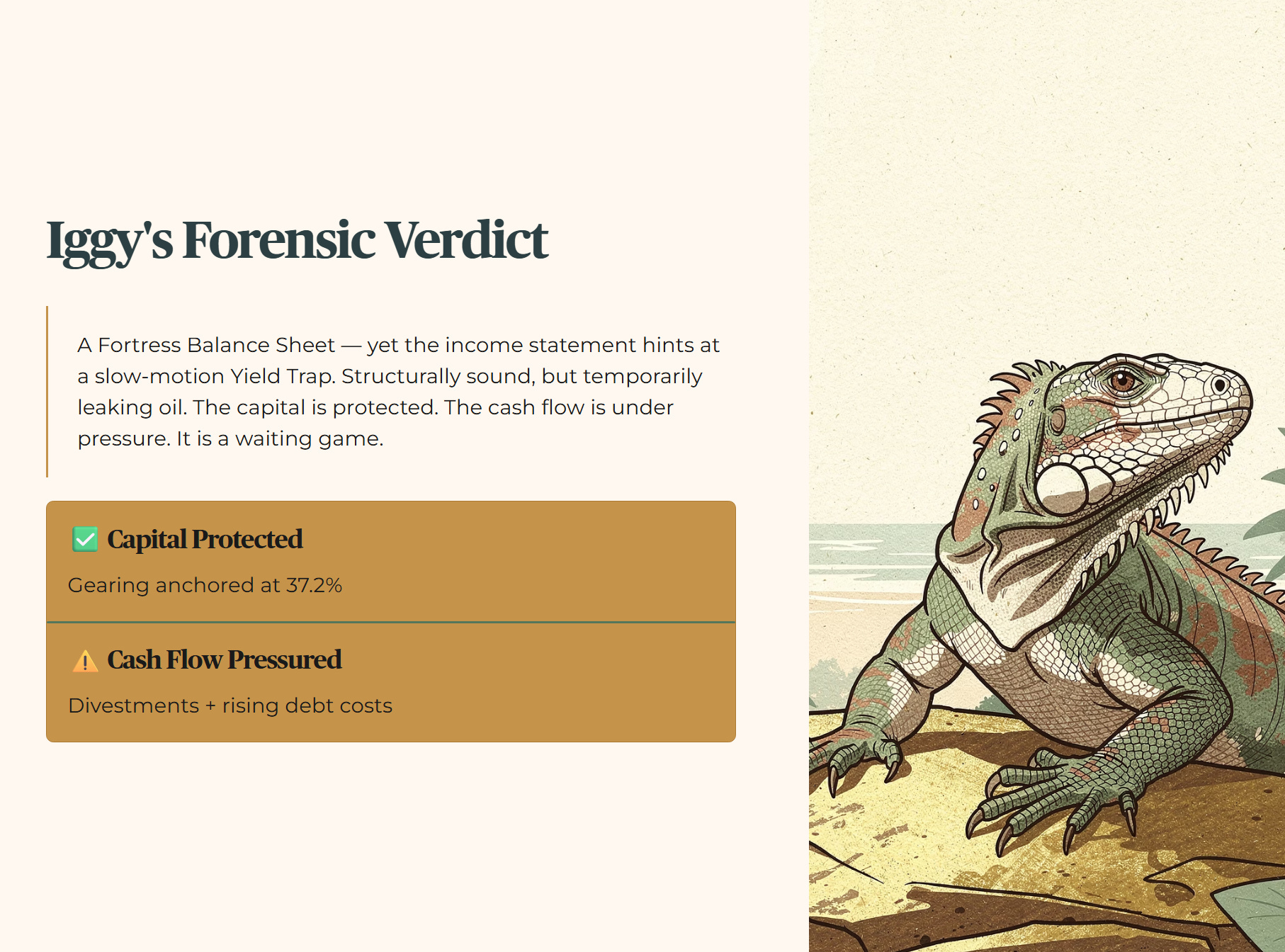

🦎 Iggy’s Insight: Mapletree Industrial Trust currently displays the classic hallmarks of a Fortress Balance Sheet, yet the income statement hints at a slow-motion Yield Trap. The gearing is comfortably anchored at 37.2%, giving it debt headroom compared to more highly leveraged peers.

However, the 7.0% drop in DPU and the weak free cash flow coverage tell a different story. You are buying a structurally sound vehicle that is temporarily leaking oil. The capital is protected, but the cash flow is under pressure from recent divestments and rising debt costs. The true forensic verdict? It is a waiting game.

The 3 Good (The Bull Case)

Good 1: Resilience and Pricing Power in the Singapore Portfolio

The raw fact here is undeniable. Mapletree Industrial Trust achieved a massive weighted average rental reversion of 7.1% across its Singapore properties in the third quarter. This is a sharp acceleration from the 6.2% reversion achieved just one quarter prior. It easily beats their own three-year historical average. Next, we apply peer context. Mapletree Logistics Trust only managed a positive rental reversion of 1.1% in the exact same economic window. The gap in pricing power is staggering.

“Don’t overpay for the hype. See the math behind the momentum.” .....Use the Fair Value models I use in every video. Code INVESTINGIGUANA gets you 50% off the world’s most powerful stock screener.

🦎 [Spot Undervalued Gems Here]

We run the numbers on the forward scenario. If these reversions hold above 7% while maintaining current occupancy, the income generated from Singapore will offset roughly half of the projected dividend declines from their North American struggles. So what does this mean for you? It means the core engine of this REIT is still firing on all cylinders. Wallet impact for a 50-plus Singaporean investor managing their CPF is significant. It provides a highly defensive floor.

🦎Iggy’s Insight: Think of it like a popular wet market stall. The owner raises the price of chicken by fifty cents, but the aunties still queue up every morning because the quality is unmatched. The tenant retention rate is an ironclad 86.9%. If you want to verify if this domestic growth is fully priced into the current valuation, you can run the intrinsic value models on InvestingPro using the discount code INVESTINGIGUANA.

Good 2: Institutional Grade Credit Stability

The raw fact is the official assignment of an “AA-” credit rating with a stable outlook by JCR and R&I as of their January 2026 earnings release. The historical benchmark shows they have maintained an aggregate leverage of 37.2%, which sits neatly below their five-year historical average. A gearing of 37.2% is superior to CapitaLand Ascendas REIT at 39.0% and safer than Mapletree Logistics Trust at 40.7%.

We pressure-test the forward scenario. The trust is sitting on S$500 to S$600 million in North American divestment proceeds. If they use this cash purely to repay debt, their leverage would plunge toward 31%. This creates massive dry powder for future acquisitions in Japan or Korea.

🦎Iggy’s Insight: So what does this mean for you? It means absolute capital preservation. Wallet impact for a retiree is peace of mind. This is a Fortress Balance Sheet. It is the financial equivalent of a fully paid-up 4-room HDB flat. You do not have to worry about the bank knocking on your door during a macro storm. The sponsor, Mapletree Investments, holds S$80.3 billion in assets and retains a 25.97% stake. They have skin in the game.

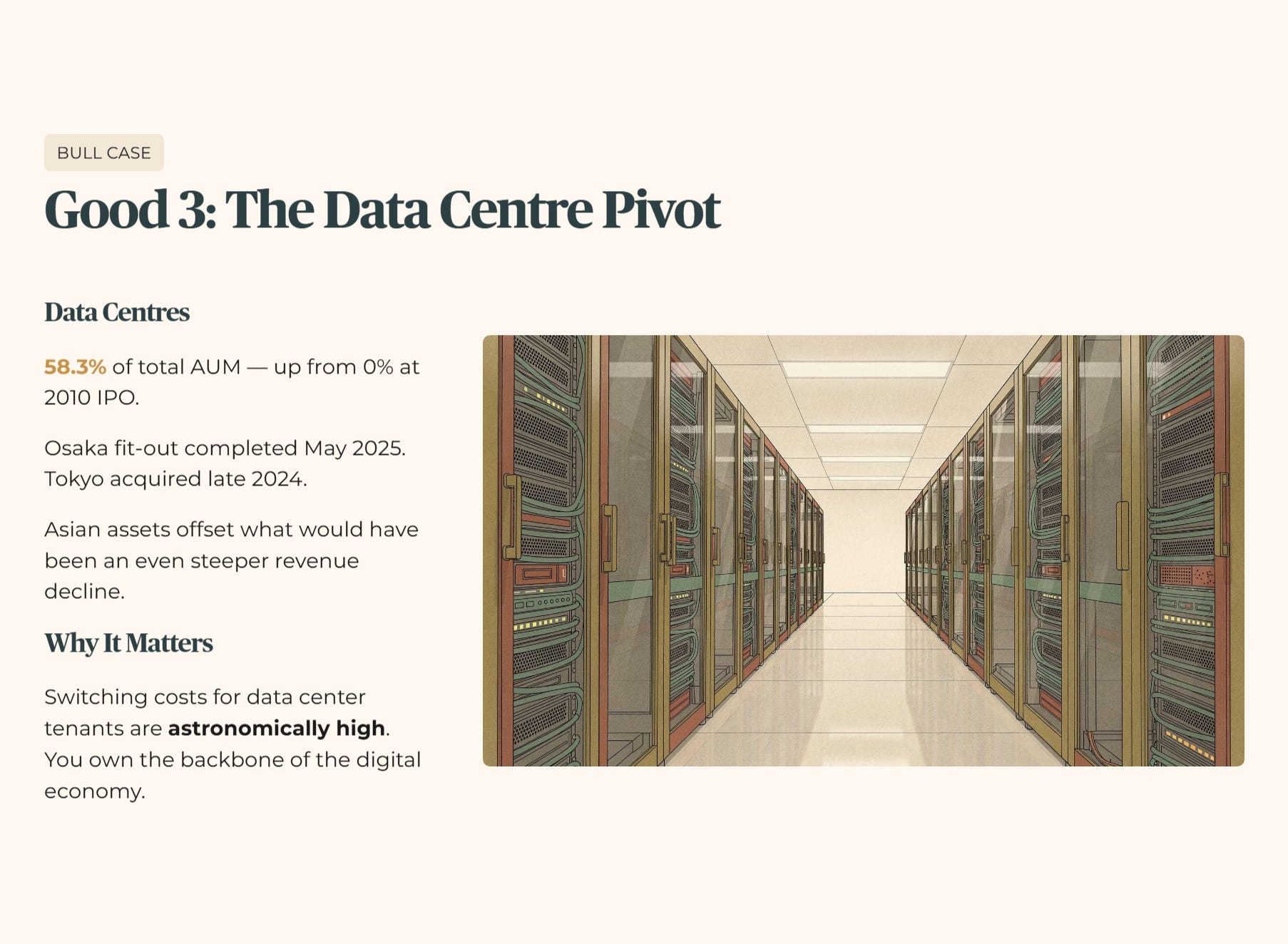

Good 3: The Successful Data Center Pivot

The raw fact is that Data Centres now make up a commanding 58.3% of their total Assets Under Management. At their 2010 IPO, they were entirely focused on Singapore flatted factories. They now possess a much higher exposure to specialized, sticky technology assets than many peers.

We run the numbers on the forward scenario. The completion of the Osaka Data Centre fit-out in May 2025 and the Tokyo acquisition in late 2024 are already doing the heavy lifting. These Asian assets provided the crucial revenue offsets to what would have been an even worse 8.0% gross revenue decline.

🦎Iggy’s Insight: So what does this mean for you? It means you own a piece of the digital economy’s backbone. Wallet impact is long-term future-proofing of your dividend stream. It is like owning the server room that every shop on the block now can’t function without. The switching costs for data center tenants are astronomically high.

“If all you see is the headline yield and the gearing ratio, you are missing the three specific red flags that will decide whether this becomes your sanctuary or your next regret.”

The 3 Red Flags (The Bear Case)