Is Your Stock Yield Actually Safe vs. 4.0% CPF? (Forensic Audit Lesson)

Why the Real Opportunity (and Risk) Is in Singapore Small Caps

Your phone buzzes with the same screenshot in three different WhatsApp chats: STI 5,000. The caption is always some version of “Finally 🚀” or “Next stop 6,000?”. Friends who sat out the last decade are suddenly asking if they’re “too late to get in”. The narrative is clear – Singapore’s market has broken its psychological ceiling.

But here is the uncomfortable truth: at 5,000 points, the STI is no longer where the real story is. The blue‑chip rally is already on every kopitiam table; the genuine multi‑bagger potential – and the nastiest traps – are hiding in the small‑cap corner of the market that nobody is screenshotting.

For the headlines, this is a celebration of Singapore’s resilience. For retirees who treat their CPF Special Account like a fortress rather than a playground, this milestone should be a rotation question: which small caps actually deserve to come off the watchlist and into the portfolio, and which ones are just “cheap” for a reason?

This is exactly why our community exists. We are now a group of over 6,000 free subscribers and, more importantly, a high-conviction core of 170+ Elite Members who refuse to be blinded by the glare of the STI’s record highs. We don’t look at the 5,000 mark as a trophy; we look at it as a forensic boundary. If you want to navigate this shift without losing your “Sleep-at-Night” (SAN) score, you need to stop looking at the index and start looking at the balance sheets of the companies the index left behind.

In This Article:

The Masterclass: The “Mixed Rice” Mechanics of Small-Cap Growth

Step 1: The Health Check (Balance Sheet and Solvency)

The Forensic Audit of Micro-Mechanics (5DD) and Kimly (1D0)

Step 2: The Wealth Check (Cash Flow and Yield)

The Forensic Yield Spread Audit

Step 3: The Price Check (Valuation and Peers)

The Peer Valuation Gap

Step 4: The Future Check (Scenarios and Fair Value)

The Bottom Line: My Forensic Stance

InvestingPro Reality Check

Iggy's VerdictAbout Iggy & the Elite 170

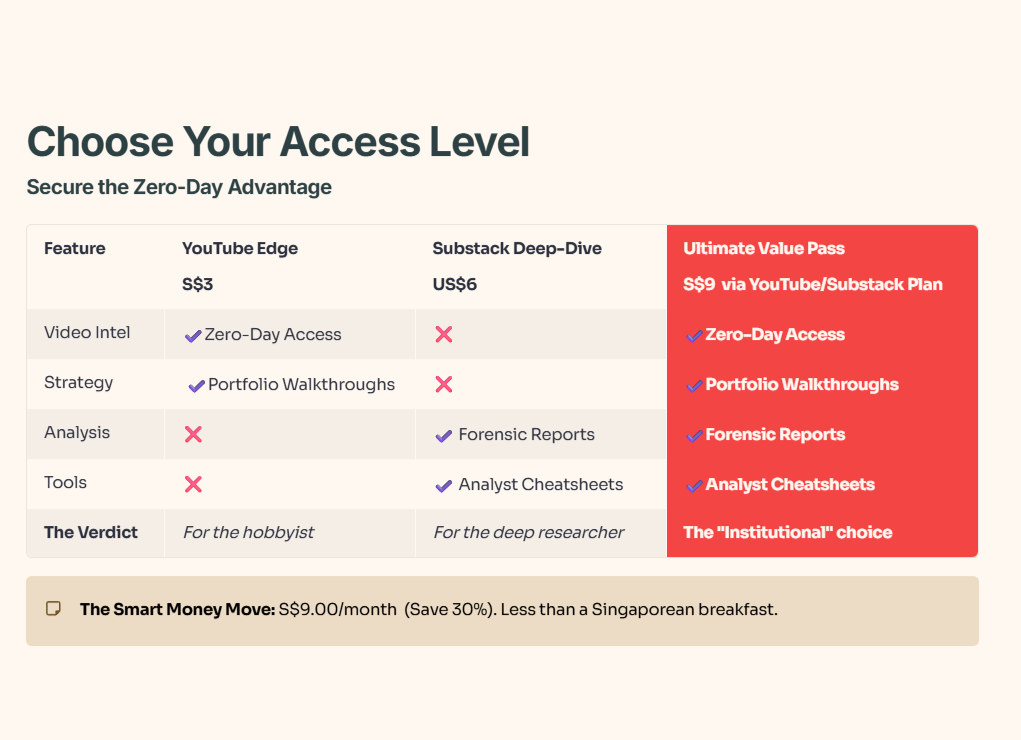

In the Singapore market, the gap between a smart entry and becoming someone else’s exit liquidity can be as little as 48 hours. That’s the cost of informational lag.

Free subscribers get my analysis up to 14 days later. The Elite 170 get it the moment it’s ready.

Your Edge: The S$9 Ultimate Value Pass bundles zero-day video intel, forensic reports, and analyst cheatsheets into one institutional-grade feed — for less than a Singaporean breakfast.

The Small‑Cap Masterclass: The “Mixed Rice” Mechanics of Growth in a 5,000‑Point Market

Think of the Singapore market like your favorite Cai Fan (mixed rice) stall in a Jurong West hawker centre. The “Big Three” banks and the massive REITs are the premium dishes—the steamed pomfret or the salted egg pork ribs. They are reliable, they look good on the plate, but they are expensive, and everyone knows exactly what they are getting. In a 5,000-point market, these premium dishes have already been priced for perfection.

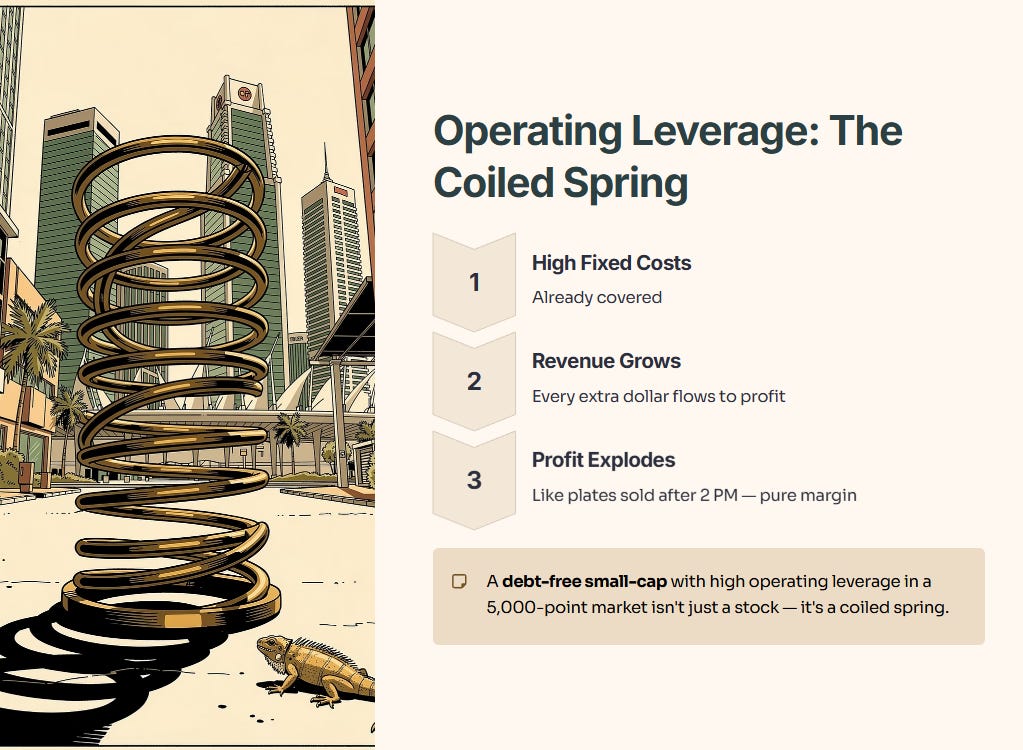

The small-cap segment, however, is like the hidden vegetable dishes or the humble “tau kwa” that the uncle tucked away at the back. Most people ignore them because they aren’t flashy. But for the forensic investor, these are the items that determine whether your “meal” (your portfolio) offers actual value. In the context of 2026, the primary financial driver isn’t just “growth”—it is operating leverage.

Operating leverage is a simple concept that many miss. When a small company has high fixed costs but starts growing its revenue, every extra dollar of sales doesn’t just add a dollar to the profit; it flows straight to the bottom line because the costs are already covered. It’s like a chicken rice seller who has already paid for his stall rent and his assistant; every plate sold after 2:00 PM is almost pure profit. If you find a debt-free small-cap with high operating leverage in a 5,000-point market, you aren’t just buying a stock; you are buying a coiled spring.

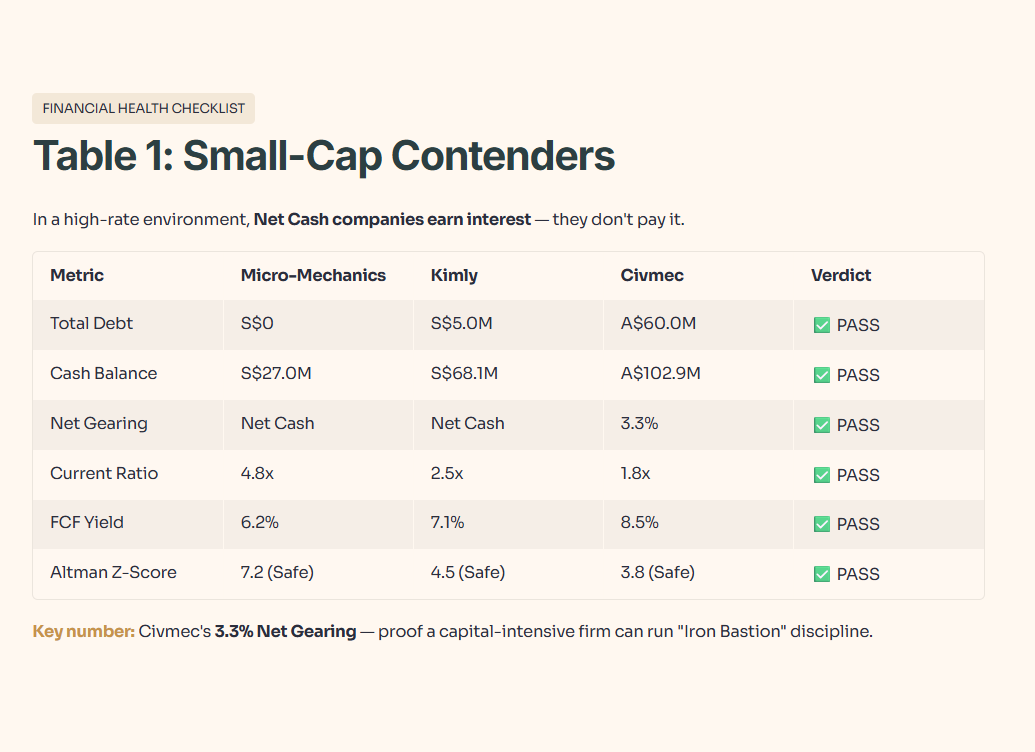

Step 1: The Health Check (Balance Sheet and Solvency)

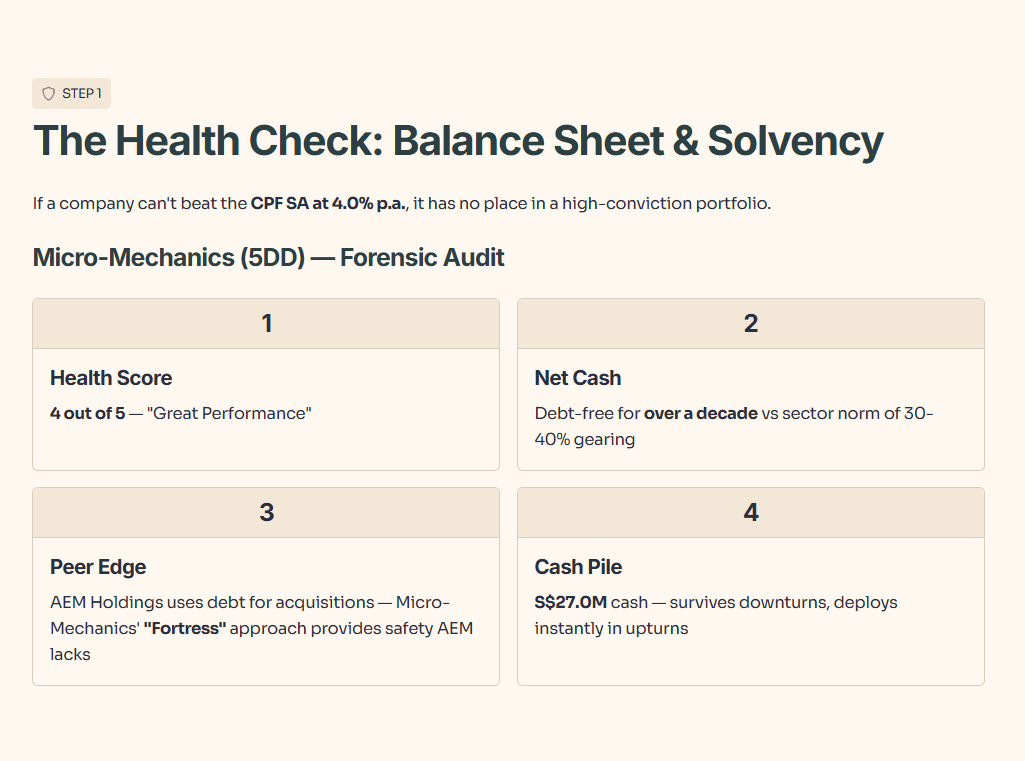

Is this company an Iron Bastion or a house of cards? For the retiree, the 4.0% p.a. interest in the CPF Special Account is the risk-free floor of any strategy. If a company’s financial health cannot convincingly beat the safety of the CPF SA, it has no place in a high-conviction portfolio. We begin our audit with the most critical pillar: Solvency.

The Forensic Audit of Micro-Mechanics (5DD) and Kimly (1D0)

We start with Micro-Mechanics (5DD).

Layer 1 (Raw Fact): Micro-Mechanics currently maintains a "Great Performance" score of 4 out of 5 for overall financial health.

Layer 2 (Historical Benchmark): This “Net Cash” position is a persistent trait; the company has maintained a debt-free status for over a decade, which is significantly superior to the semiconductor sector norm where gearing often sits at 30-40%.

Layer 3 (Peer Context): Compare this to AEM Holdings, which has historically utilized debt to fund acquisitions. Micro-Mechanics’ “Fortress” approach provides a safety margin that AEM lacks during cyclical downturns.

Layer 4 (Forward Scenario): If the semiconductor market slows by 10%, Micro-Mechanics can survive indefinitely without interest expense pressure. If it grows by 10%, that S$27.0 million cash pile can be deployed for immediate capacity expansion.

Layer 5 (Wallet Impact): For a Singaporean investor aged 55+, this means your principal is protected by a literal pile of cash. It mirrors the stability of the CPF BRS ($110,200)—it is money that is there, regardless of market sentiment.

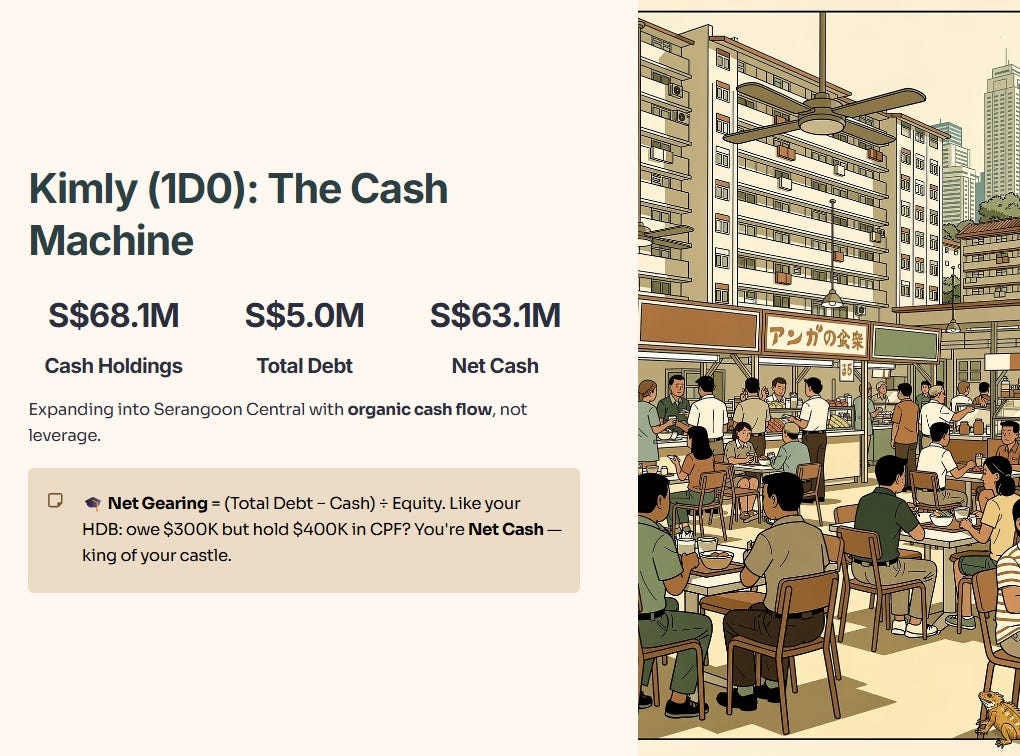

Next, we look at Kimly Limited (1D0). The raw fact is that Kimly holds S$68.1 million in cash against only S$5.0 million in debt. This gives them a net cash position of S$63.1 million. Historically, this is an improvement from their 2023 levels, showing that even as they expand into places like Serangoon Central, they are doing it with organic cash flow, not leverage.

🎓 Educational Note: Net Gearing Ratio

Let’s define that term for a second. Net Gearing is simply the measure of a company’s total debt minus its cash, divided by its total equity. Think of it like your HDB mortgage. If you owe the bank $300,000 but you have $400,000 sitting in your CPF and savings, you are “Net Cash.” You are the king of your own castle. If you owe $300,000 but only have $10,000 in the bank, your gearing is high and your “Sleep-at-Night” score is low.

So what does this mean for you? It means in a high-interest-rate environment, a Net Cash company doesn’t care if the Fed raises rates. They are the ones earning interest, not paying it.

Table 1: Financial Health Checklist (Small-Cap Contenders)

The number that matters most here is the Net Gearing of 3.3% for Civmec, because it proves that even a capital-intensive engineering firm can operate with “Iron Bastion” discipline if the management is competent.

🦎 Iggy’s Insight: In this 5,000-point STI environment, everyone is talking about “blue-chip stability,” but they are ignoring the debt these giants carry. My forensic stance is that a debt-free small-cap like Micro-Mechanics is actually a safer “Fortress” than a highly-geared blue chip. If the macro environment pivots and rates stay higher for longer, the company with the cash pile becomes the predator, while the company with the debt becomes the prey. It’s the difference between owning the coffee shop and just working there. Punchline: In a market of over-leveraged giants, the debt-free dwarf is the only one who doesn’t need to ask permission to grow.

Punchline: In a market of over-leveraged giants, the debt-free dwarf is the only one who doesn’t need to ask permission to grow.