Member Portfolio Audit | Principal (Age 60+) | Goal: Balanced

The 'Principal' portfolio puts 28% of your money into banks at their peak, while locking up critical retirement savings in property holdings that are trading well above what they are actually worth.

A New Submission for Iggy’s Portfolio Health Check

Another submission has come in for Iggy’s Portfolio Health Check — and this one is worth sitting with carefully. Principal, you are in your sixties, retired or retiring soon, and you have built what looks on the surface like a balanced portfolio. Banks for income. Property for stability. Industrial exposure for diversification. It is a familiar architecture for a Singaporean investor of your generation, and on the face of it, it makes sense.

But a forensic audit does not look at the face of it.

This portfolio is built for growth investors on one side and retirees on the other — and right now it is not fully serving either. The bank layer is doing real work. The property layer is not. And the gap between those two halves is wider than the headline numbers suggest.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips — the interest coverage, the gearing, the free cash flow sustainability — so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

In This Article:

Member profile

Portfolio health dashboard

Individual holding analysis

The valuation reality check

Dividend trajectory

Peer comparison

The strategic summary

Three strategic considerations

Iggy’s portfolio classification

The Member Profile

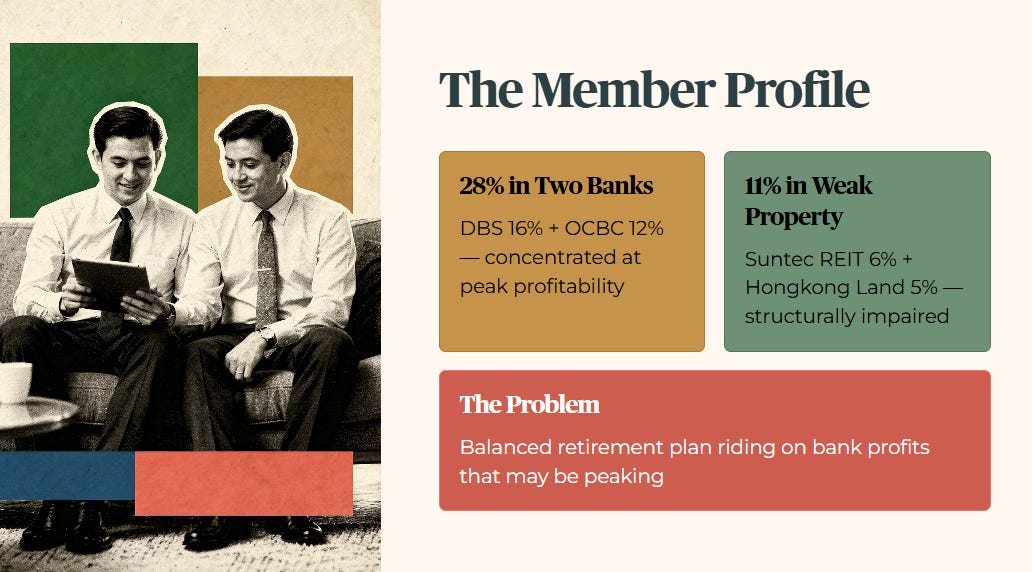

Principal, you are in your sixties and retired or retiring soon. You want a balanced mix: some growth, some regular cash payouts. You are willing to accept some ups and downs in your portfolio value.

But here is the problem. You have put 28% of your total capital into just two Singapore banks, DBS at 16% and OCBC at 12%. At the same time, you have locked 11% of your wealth into property-linked holdings that are structurally weak: Suntec REIT at 6% and Hongkong Land at 5%. This combination means your balanced retirement plan is riding on bank profits that may be peaking, while your property holdings are dragging your net worth down because you bought them at prices that were too high.

For a retiree in their sixties, this is not a theoretical risk. It is a live drag on the capital you need to fund the next twenty years.

🦎 Iggy’s Insight Block 1

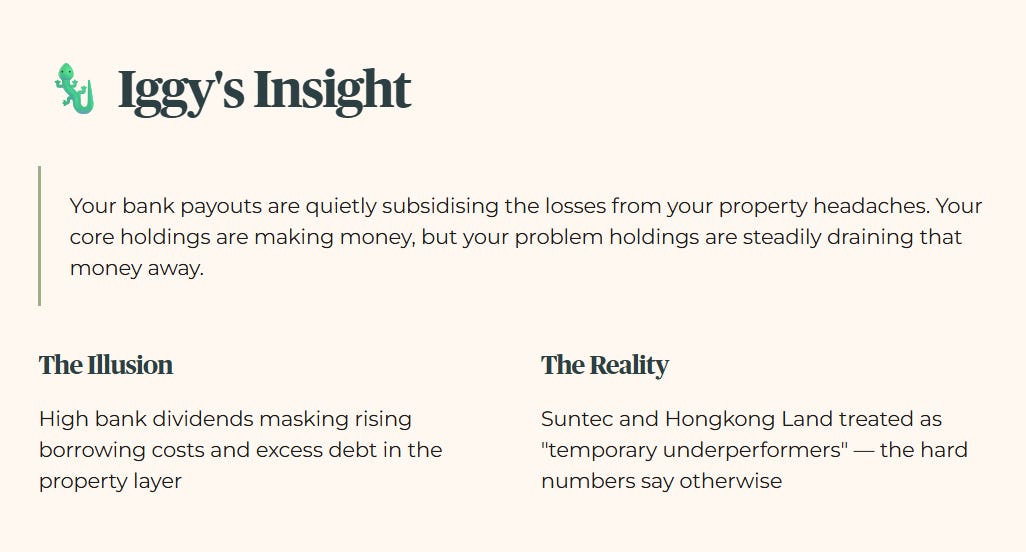

Principal, your portfolio tracking is hiding a serious mismatch between how much risk you think you are taking and how much you are actually taking. You are relying on Singapore’s big banks to deliver the growth and income you need. And you are treating Suntec REIT and Hongkong Land as temporary underperformers that will eventually recover on their own. The hard numbers tell a more urgent story. Your high bank dividends are masking real problems: rising borrowing costs and too much debt in your property layer.

The truth is this: your bank payouts are quietly subsidising the losses from your property headaches. Your core holdings are making money, but your problem holdings are steadily draining that money away.

The Safety Stress Test

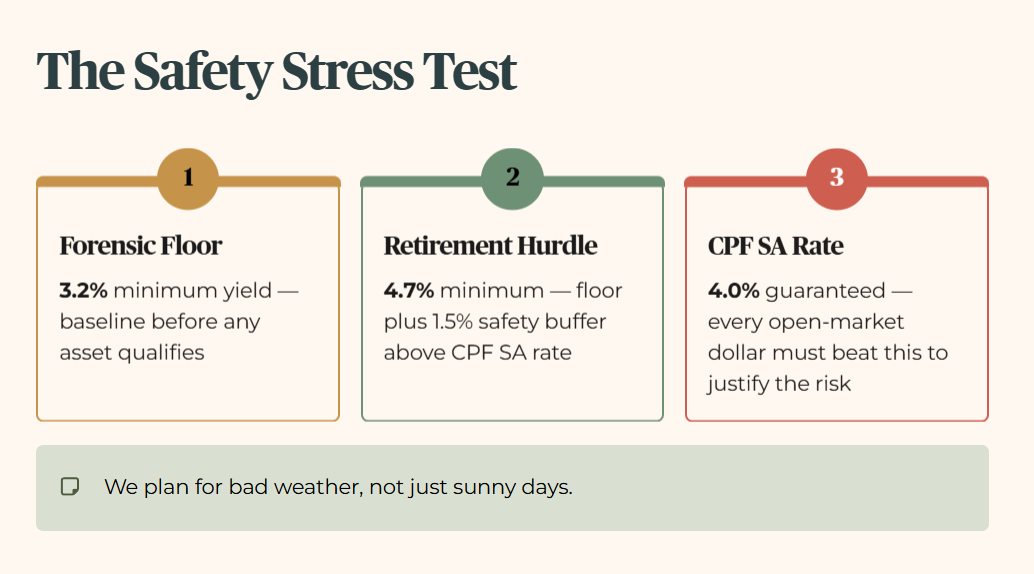

To check whether your portfolio can reliably fund a balanced retirement, I have audited your five largest holdings against my forensic tracking standards. The forensic floor, which is my minimum acceptable yield of 3.2%, is the baseline I require before any asset qualifies for consideration. The minimum yield I want to see in a retirement portfolio is 4.7%. That is the 3.2% floor plus an extra 1.5% as a safety buffer above the CPF SA guaranteed rate of 4.0%. Every dollar you put into the open market is exposed to gearing risk, distribution cuts, and price volatility. The 4.7% hurdle is the minimum that exposure must earn to justify the risk.

For this audit I use the conservative 3.2% floor as the stress-test buffer. We plan for bad weather, not just sunny days.

To understand better Iggy’s Forensic Filters and Why I insist on 4.7%, 3.2% etc, check out this post.

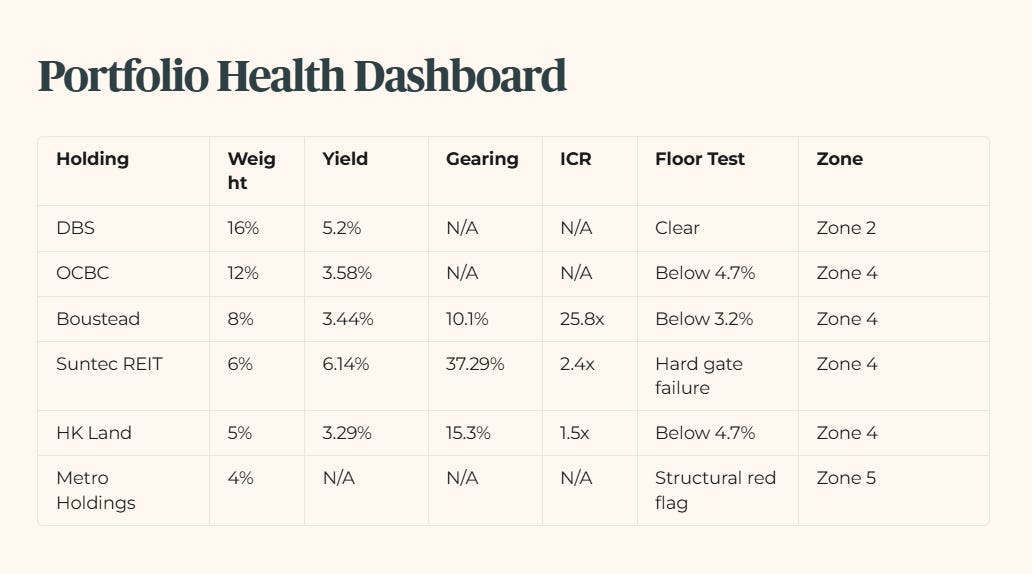

Portfolio Health Dashboard

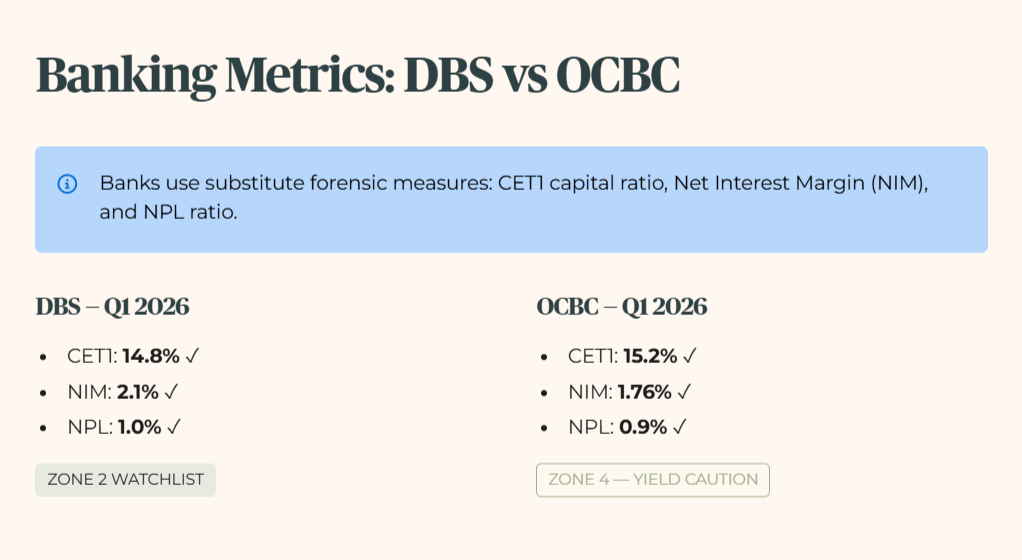

Note on DBS and OCBC: Gearing and ICR are not applicable to banking entities. Singapore banks fund their lending operations through customer deposits, which makes conventional debt-to-asset gearing meaningless as a safety metric. For banking entities, Iggy applies three substitute measures: CET1 capital ratio for balance sheet safety, net interest margin (NIM) for lending profitability, and non-performing loan (NPL) ratio for asset quality.

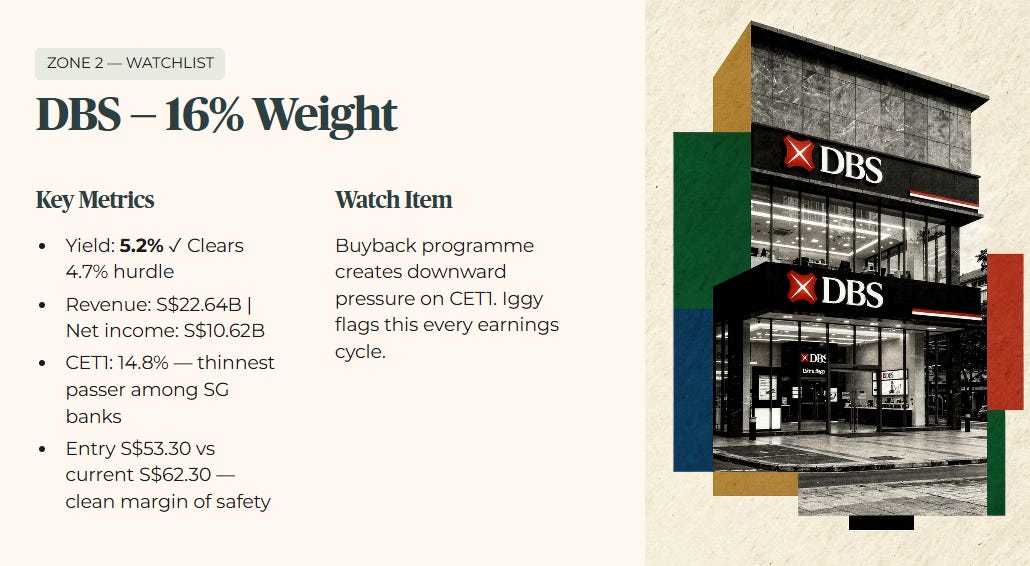

DBS Q1 2026: CET1 14.8%, NIM 2.1%, NPL 1.0%. All forensic thresholds clear. Zone 2 Watchlist.

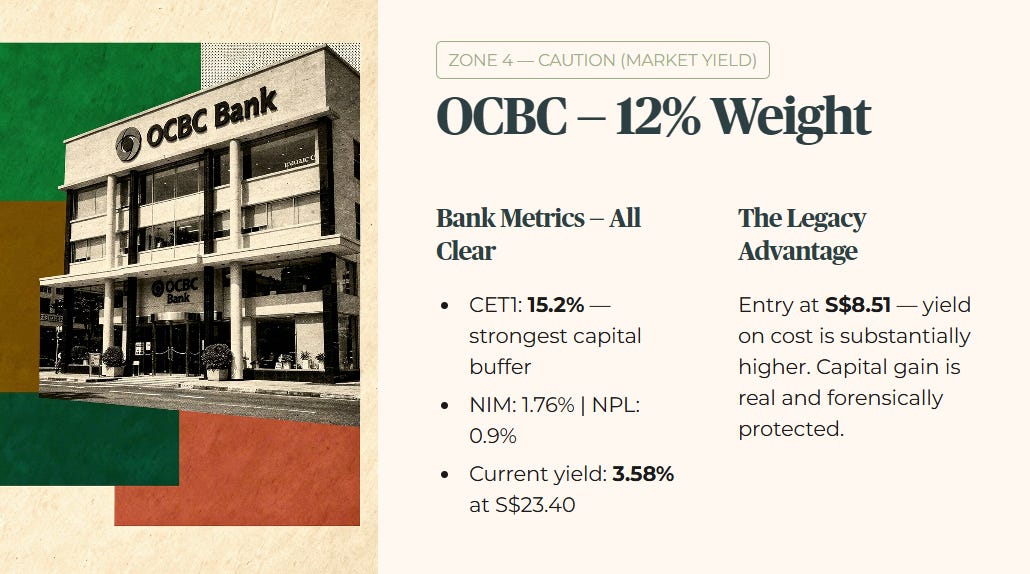

OCBC Q1 2026: CET1 15.2%, NIM 1.76%, NPL 0.9%. All forensic thresholds clear on bank metrics. Zone 4 Caution on current market yield — see Legacy Hold section below.

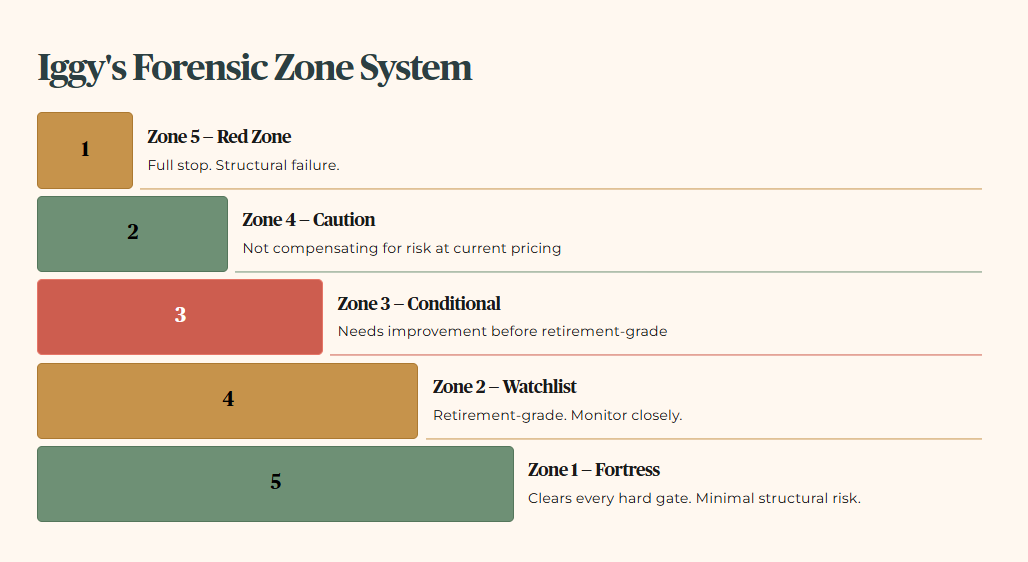

How Iggy Rates Every Stock

Iggy’s Forensic Zone system runs from Zone 1 Fortress to Zone 5 Red Zone. Zone 1 and Zone 2 are retirement-grade holdings — assets that clear every hard gate and carry minimal structural risk. Zone 3 is conditional — something needs to improve before it belongs in a retirement portfolio. Zone 4 is caution territory — the asset is not compensating you adequately for the risk at current pricing. Zone 5 is a full stop. The hard gates are yield, balance sheet strength, and debt serviceability. A single hard gate failure drops a stock to Zone 4 minimum, regardless of how good the other numbers look.

Individual Holding Analysis

DBS (Weight: 16% | Average Buy Price: S$53.30)

DBS pays 5.2% on its current share price. The bank has reported trailing twelve-month revenue of S$22.64 billion and net income of S$10.62 billion. On the banking forensic framework, CET1 sits at 14.8%, placing DBS in the Zone 2 band on capital adequacy. NIM of 2.1% and NPL of 1.0% carry zero soft flags.

Your entry price of S$53.30 sits below the current market price, giving you a clean margin of safety on your cost base. For a retiree in your sixties, this holding clears the 4.7% minimum yield and delivers meaningful cash payouts that anchor your retirement income.

One watch item: DBS CET1 at 14.8% is the thinnest passer among the three Singapore banks. The ongoing buyback programme and capital return distributions create downward pressure on that ratio. Iggy will flag this at every earnings cycle.

Iggy’s Forensic Zone: Zone 2 — Watchlist

OCBC (Weight: 12% | Average Buy Price: S$8.51)

OCBC pays 3.58% on its current share price of S$23.40. On bank forensic metrics, CET1 sits at 15.2%, NIM at 1.76%, and NPL at 0.9% — all clear.

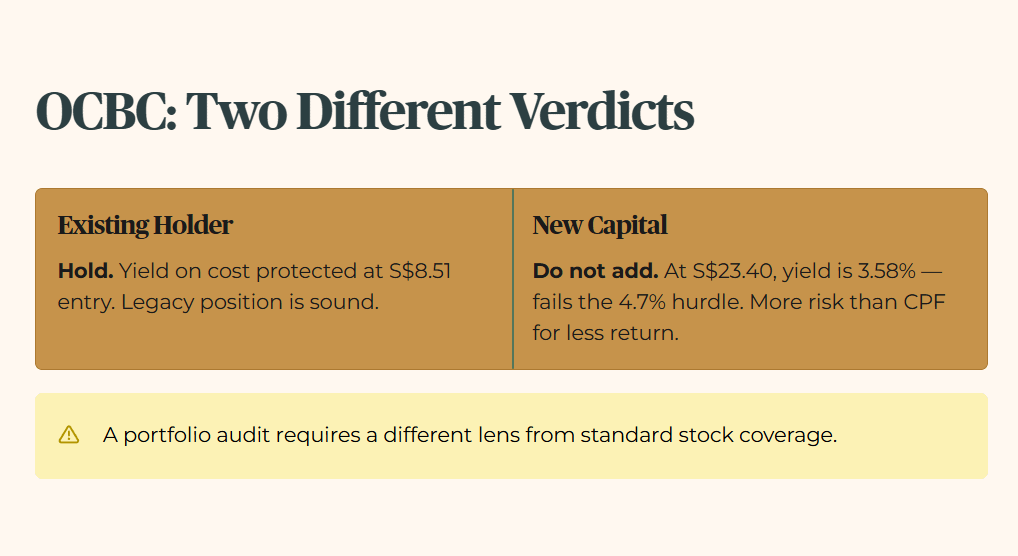

Here is where a portfolio audit requires a different lens from a standard stock coverage piece.

Your entry price of S$8.51 is exceptional. On that cost base, your personal yield is substantially higher than the 3.58% the market currently prices. That entry is forensically protected and the capital gain embedded in your position is real.

But the zone assignment reflects what OCBC offers a buyer at today’s price — because that is the honest forensic question for any dollar you consider adding. At S$23.40, the yield is 3.58%. That fails my 4.7% minimum yield hurdle. A new buyer at today’s price is accepting more risk than CPF for less return. That is a Zone 4 decision.

The verdict for your existing holding is different from the verdict for new capital. Hold your legacy position — your yield on cost is protected. Do not add at current market pricing until the yield clears 4.7%.

Iggy’s Forensic Zone: Zone 4 — Caution (current market yield). Legacy holding: yield on cost protected at entry price of S$8.51.

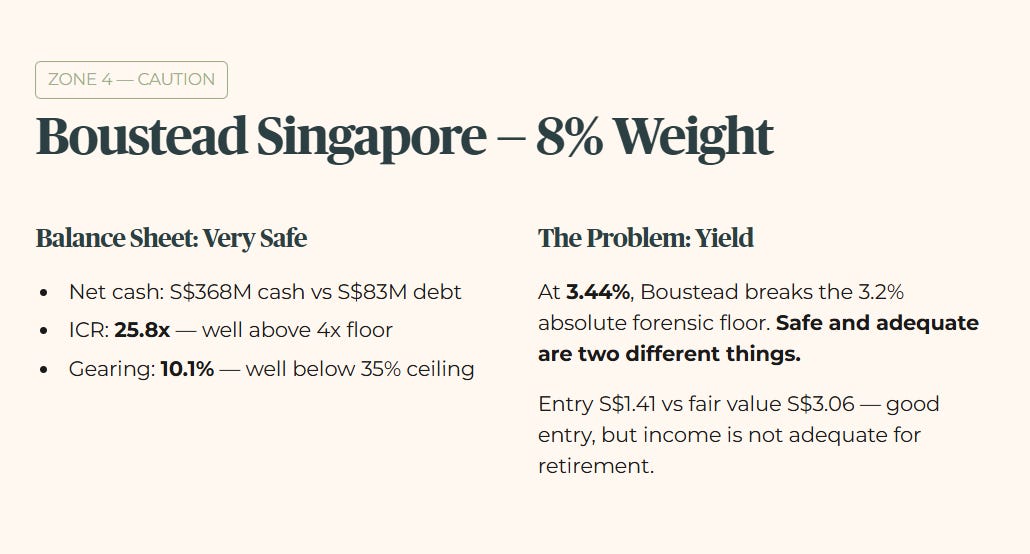

Boustead Singapore (Weight: 8% | Average Buy Price: S$1.41)

Boustead pays 3.44% on its current share price of S$2.23. The company carries S$83 million in debt against S$368 million in cash, giving it a net cash position that makes its balance sheet very safe. The interest coverage ratio, which measures how many times a company’s operating profit covers its interest payments, sits at 25.8x — comfortably above my 4x forensic floor. Gearing at 10.1% is well below my 35% ceiling.

The problem is not the balance sheet. The problem is the yield. At 3.44%, Boustead breaks my 3.2% absolute forensic floor. For a retiree looking for income, holding something that pays less than a risk-free instrument outside CPF means your money is not working hard enough. The large cash pile keeps the dividend safe — but safe and adequate are two different things.

Your entry at S$1.41 against a current price of S$2.23 and a fair value of S$3.06 means your initial purchase captured deeply undervalued assets. That is a good entry. But the current yield does not clear the minimum income bar for a retirement portfolio.

Iggy’s Forensic Zone: Zone 4 — Caution

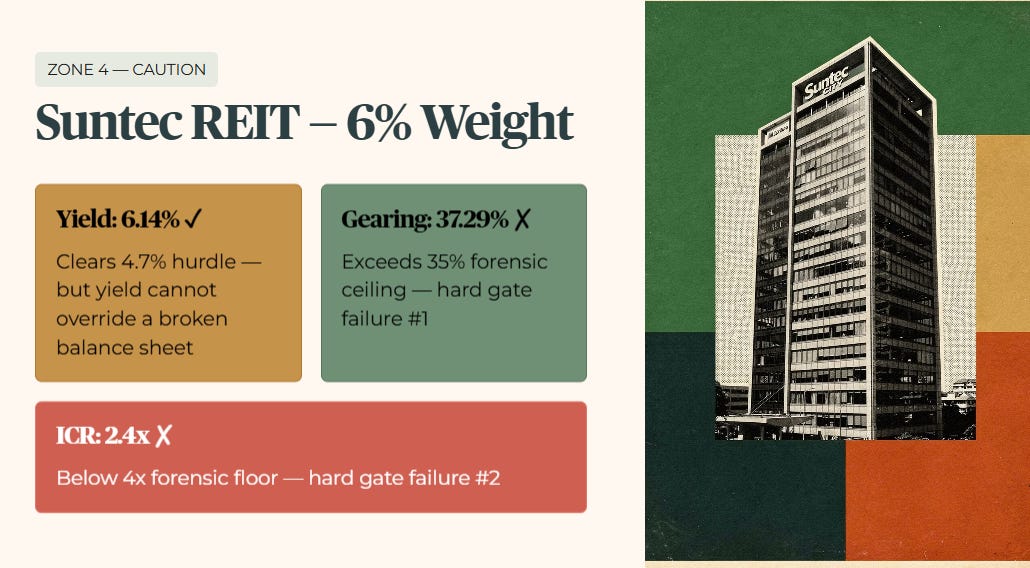

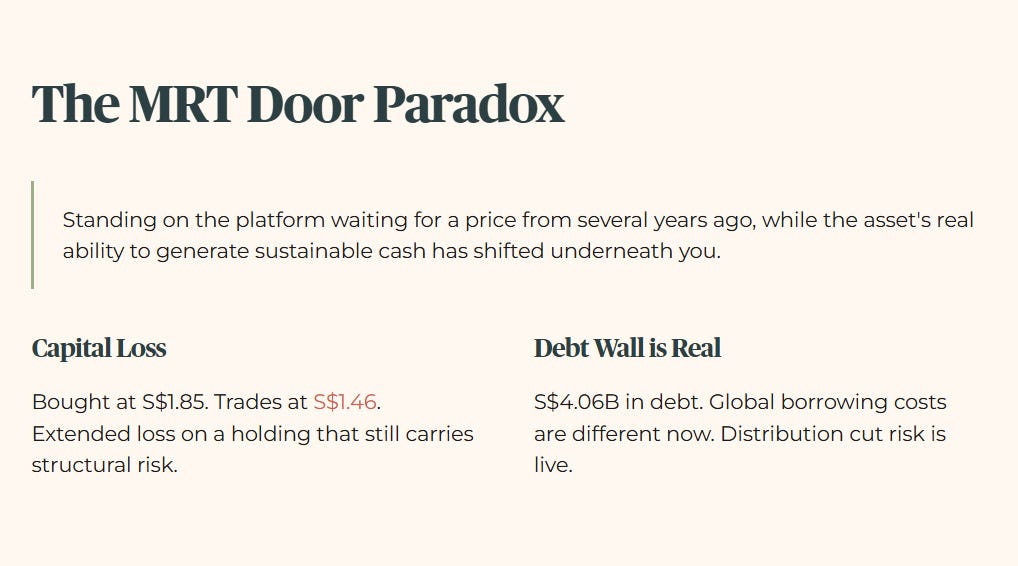

Suntec REIT (Weight: 6% | Average Buy Price: S$1.85)

Suntec REIT pays 6.14% on its current share price of S$1.46. It carries S$4.06 billion in debt against S$10.88 billion in assets, giving a gearing ratio, which is the proportion of the trust’s assets funded by debt, of 37.29%. That exceeds my 35% forensic ceiling — a hard gate failure. The interest coverage ratio at 2.4x falls below my 4x forensic floor — a second hard gate failure. Under Zone System V1.0, a single hard gate failure drops a stock to Zone 4 minimum. Two hard gate failures on the same name confirm it.

The 6.14% yield clears the 4.7% hurdle. But yield cannot override a broken balance sheet. The income looks attractive until the debt servicing cost rises and the distribution gets cut.

You bought at S$1.85. Today it trades at S$1.46. That is an extended capital loss on a holding that still carries structural risk. This is the MRT Door Paradox — standing on the platform waiting for a price from several years ago, while the asset’s real ability to generate sustainable cash has shifted underneath you. Global borrowing costs are different now. Suntec’s debt wall is real.

Iggy’s Forensic Zone: Zone 4 — Caution

Hongkong Land (Weight: 5% | Average Buy Price: US$10.02)

Hongkong Land pays 3.29% on its current share price of US$7.64. Revenue has dropped from a historical US$2.00 billion to US$1.45 billion. Net income has recovered to US$1.26 billion from previous non-cash losses, but is expected to compress again this year.

At 3.29%, the yield fails my 4.7% minimum hurdle. A 10% drop in prime office leasing across the region would put direct pressure on its US$1.45 billion revenue base, which has already shrunk from US$2 billion in prior years. That would put its long dividend history at risk.

You bought at US$10.02. Today it trades at US$7.64. Your capital is frozen in an underperformer trading 45.6% above its InvestingPro fair value of US$6.88. Five percent of your retirement wealth is sitting in an asset with limited near-term upside and a yield that does not clear the forensic minimum.

Iggy’s Forensic Zone: Zone 4 — Caution

Metro Holdings (Weight: 4% | Average Buy Price: S$0.74)

Metro Holdings is the hardest conversation in this audit. You bought at S$0.74 in 2010. Today it trades at S$0.475. InvestingPro fair value is S$0.39. That means even at today’s depressed price, Metro is still trading 21.8% above fair value. The company reported annual net income of negative S$203.2 million. Your 25,000 shares are sitting in a stock that is losing money, trading above its forensic value, and offering no meaningful yield.

Long-term holding cannot fix a broken asset stack. Patience is a forensic virtue when the underlying business is sound. It is not a strategy when the business is structurally impaired.

Iggy’s Forensic Zone: Zone 5 — Red Zone

The Valuation Reality Check

Every holding in your portfolio carries two prices that matter: what you paid, and what the asset is actually worth today based on verified forensic fair value estimates from InvestingPro. The gap between those two numbers tells you whether your capital is working or whether it is stranded. A discount to fair value means you bought well and have a margin of safety underneath you. A premium to fair value means the market is pricing the asset above what the fundamentals support — and your capital is exposed to a correction that brings the price back to reality. For a retiree in your sixties, that distinction is not academic. Capital that corrects downward toward fair value is capital that cannot fund your retirement income in the meantime.

The valuation gap between what you paid and what each asset is actually worth on a 4.7% forensic yield standard is where this portfolio stops looking “balanced” and starts revealing the real capital at risk.