Mapletree Logistics Trust 3Q FY25/26: Value Trap or Mispriced Income Play in 2026?

DPU is down 9.3% to 1.816 cents, yet the “Smart Money” models see an 8.8% upside. Here is the disconnect.

The Mapletree Logistics Trust (SGX: M44U) 3Q FY25/26 report dropped two days ago (Jan 26), and the market reaction has been… silent. The stock is hovering at S$1.37.

[Here’s the 3Q FY25/26 Report]

If you just read the headlines, it looks ugly: Revenue down, NPI down, DPU down. But if you look at the InvestingPro models I use, we are staring at a potential mispricing.

Let’s strip away the “Resilient Performance” corporate fluff and look at the raw numbers.

In This Article:

The DPU Pain Point Financial Highlights

The China Turnaround Story Portfolio Operations

The Debt Wall and Liquidity Balance Sheet

InvestingPro Reality Check

Iggy's Verdict🦎 About Iggy the Investing Iguana

Welcome to the Iguana Pit! If you’re new here, I’m Iggy: your guide through the dense jungle of the Singapore markets. My mission is simple: to spot the predators before they spot your portfolio.

We are now 5,800+ subscribers strong across YouTube and Substack, focusing purely on the data-driven alpha that mainstream media misses.

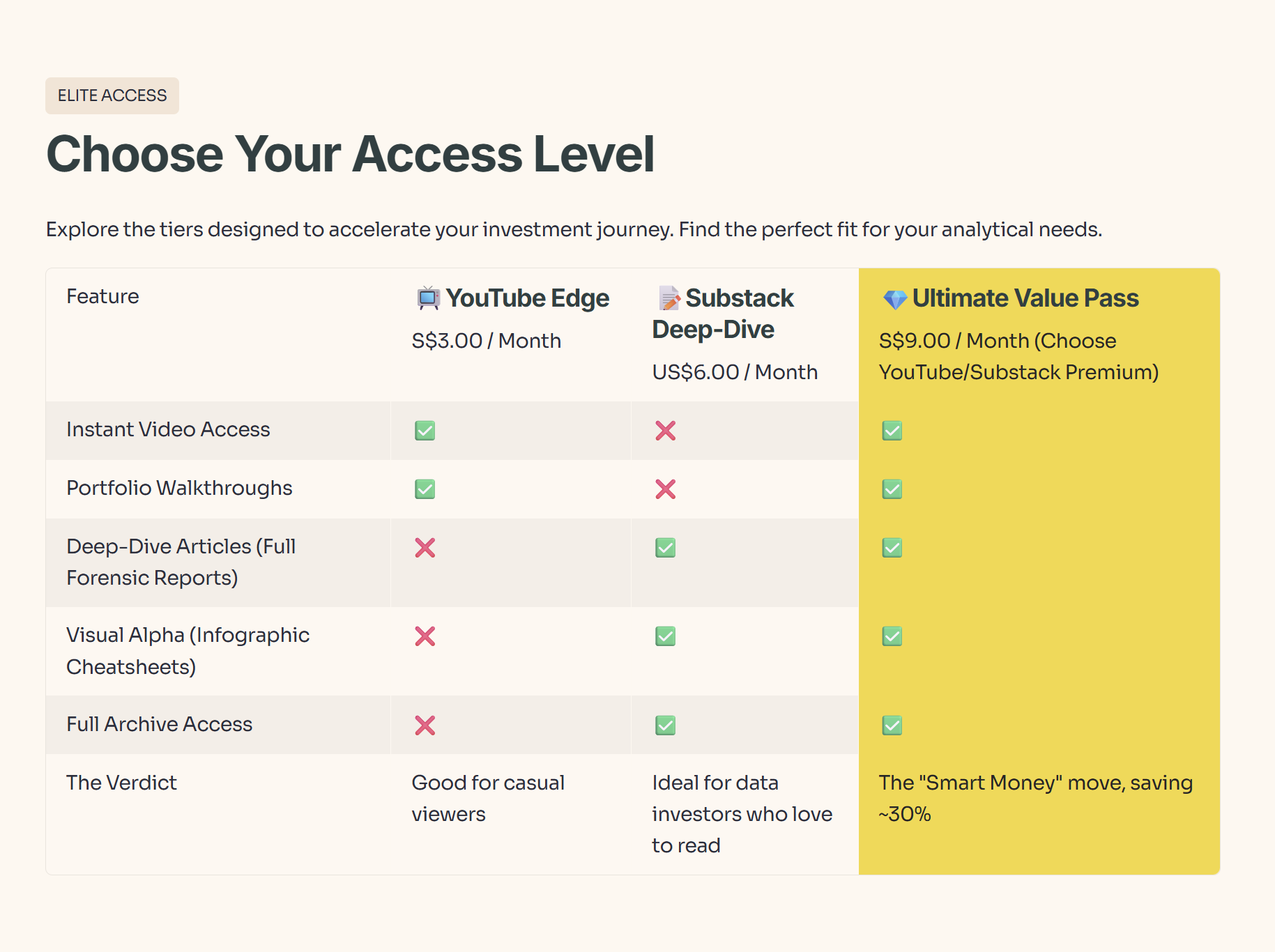

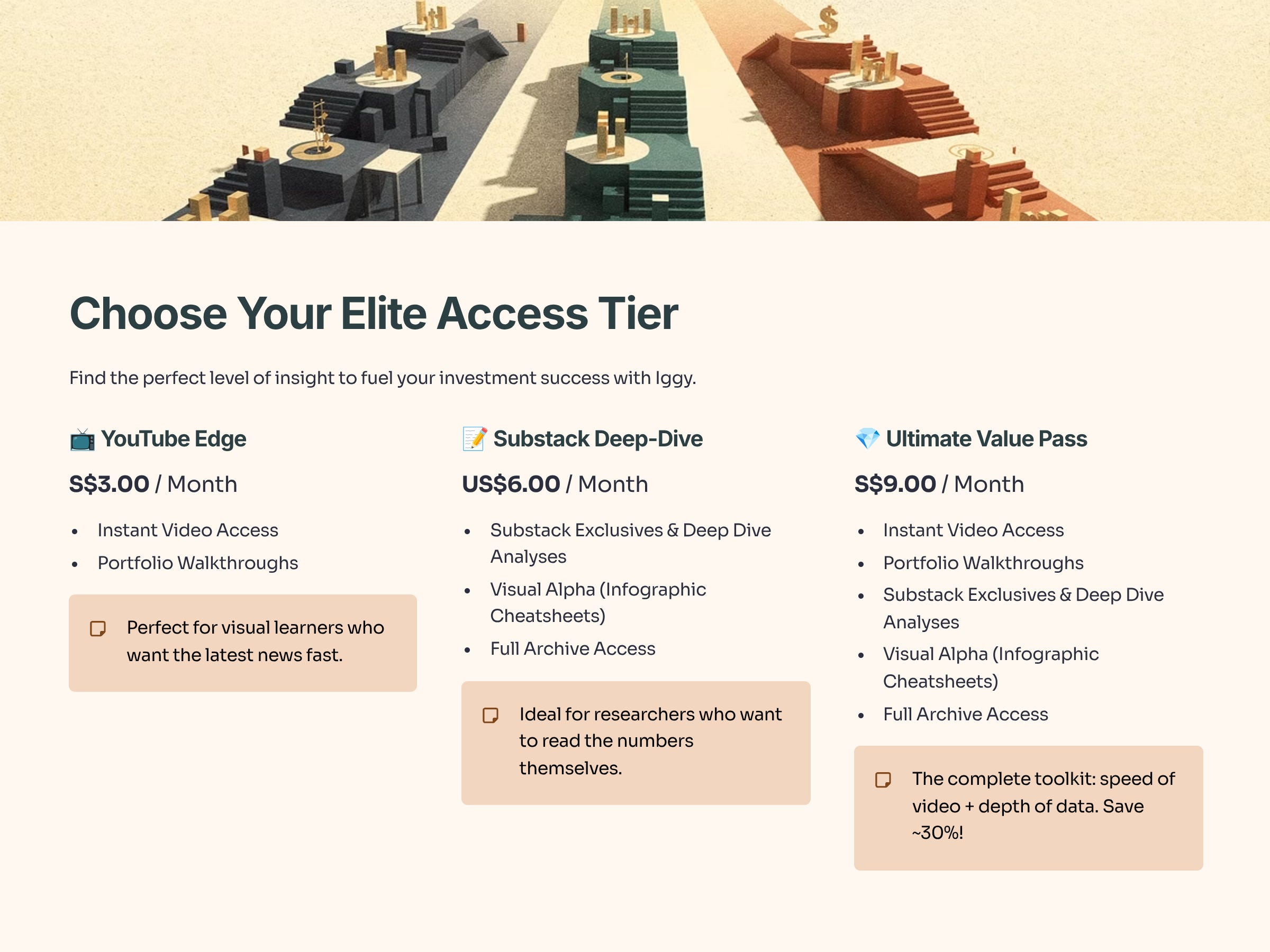

🚀 Join the “Elite 150” Inner Circle

Real alpha is found behind the velvet rope. Stop following the herd and start following the data with our 150+ paid members.

📺 The YouTube Edge (S$3/mo): Beat the Delay.

Instant Access: Watch new videos the moment they drop.

The Free Tier Trap: Free subscribers wait up to 14 days to see the same video. (By then, the news is old and the trade is gone).

📝 The Substack Deep-Dive (US$6/mo): Unlock the Vault.

Zero Paywalls: Read the full “Deep Dive” articles and “Substack Exclusive” articles found only on Substack.

Visual Alpha: Download exclusive Infographic Cheatsheets not available to free readers.

💎 The Ultimate Value Pass (S$9/mo): (BEST VALUE)

Get It All: Paid via YouTube, this bundle grants you Instant Video Access AND Full Substack Access.

The Math: You save ~30% compared to buying them separately. It’s the “Smart Money” move.

Why wait 2 weeks for old news? Get the data while it’s fresh. 👉 Join Here: https://www.youtube.com/@InvestingIguana/membership

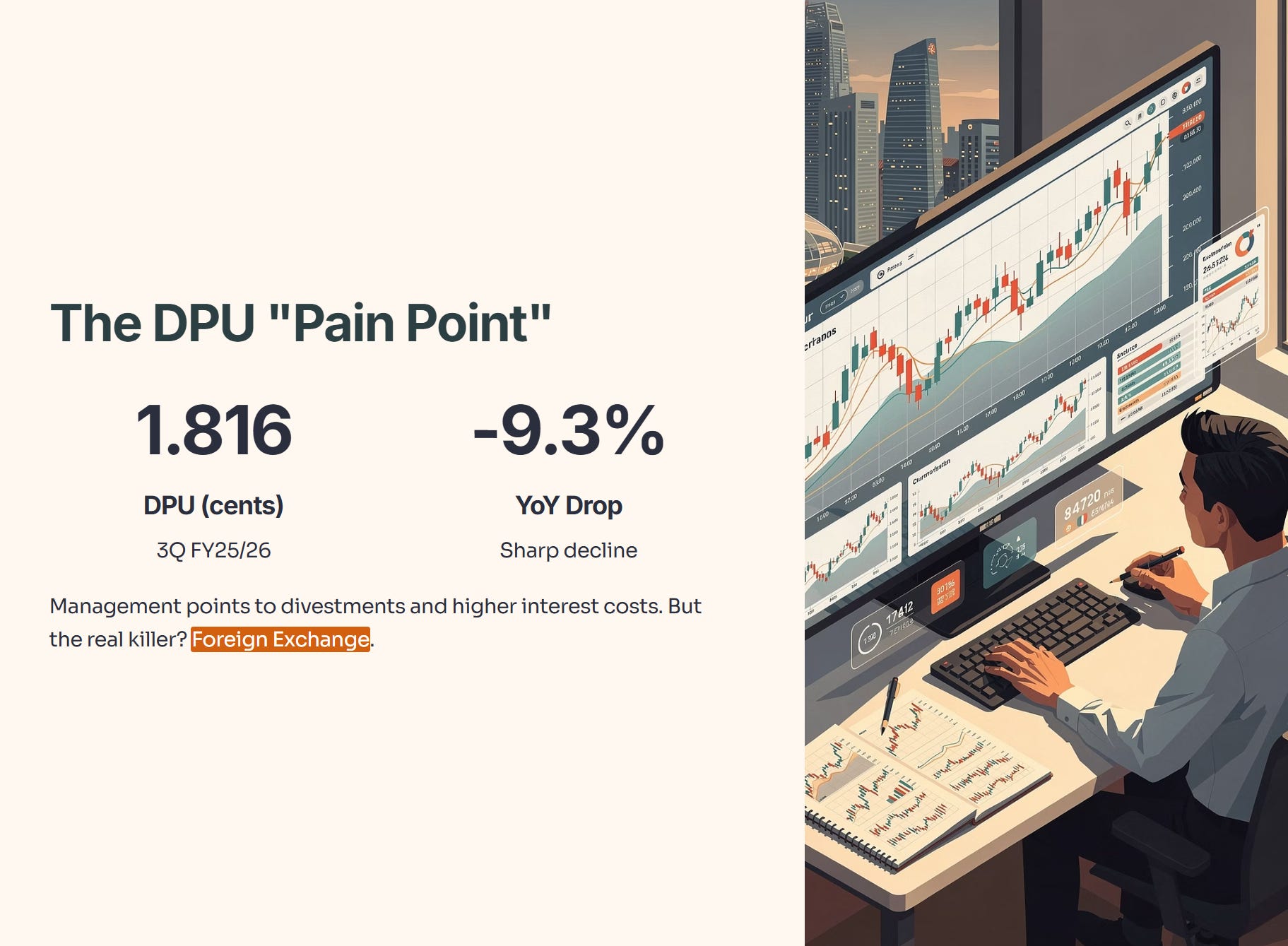

1. The DPU “Pain Point” (Financial Highlights)

The Headline: DPU for 3Q FY25/26 fell to 1.816 cents, a sharp 9.3% drop year-on-year.

The Iggy Analysis:

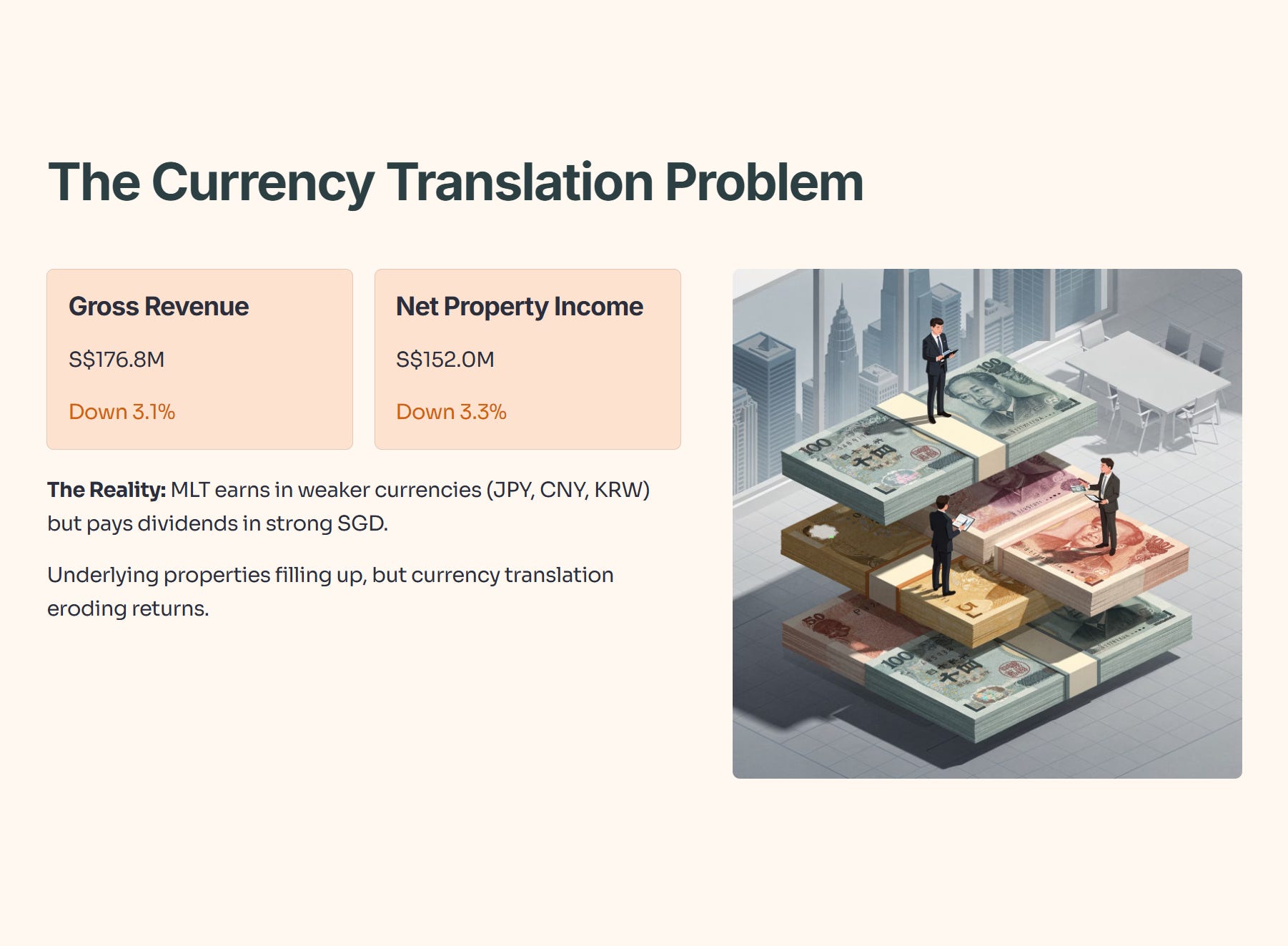

Why is the dividend shrinking? Management will point to “divestments” (selling old assets) and “higher interest costs.” That is true, but the real killer here is FX (Foreign Exchange).

MLT earns income in weaker currencies (Japanese Yen, Chinese Yuan, Korean Won) but pays you in a very strong Singapore Dollar.

Gross Revenue: S$176.8M (down 3.1%)

Net Property Income (NPI): S$152.0M (down 3.3%)

The Takeaway: The underlying properties are actually filling up (see below), but the currency translation is eating your lunch. Until the SGD weakens or regional currencies rebound, this “optical shrinkage” will persist.

2. The China “Turnaround” Story? (Portfolio Operations)

The Data:

Portfolio Occupancy: 96.4% (Up from 96.1% in Q2).

China Rental Reversions: -3.0%.

The Interpretation:

Wait, why am I highlighting a negative -3.0% number? Because context is King.

A year ago, China rental reversions were terrible (double-digit negative). Last quarter was also painful. A -3.0% reversion suggests the bleeding in China is finally clotting. It’s not “growth” yet, but it’s “stabilization.”

If you are holding MLT, you are betting on China not getting worse. This metric confirms that thesis for now.

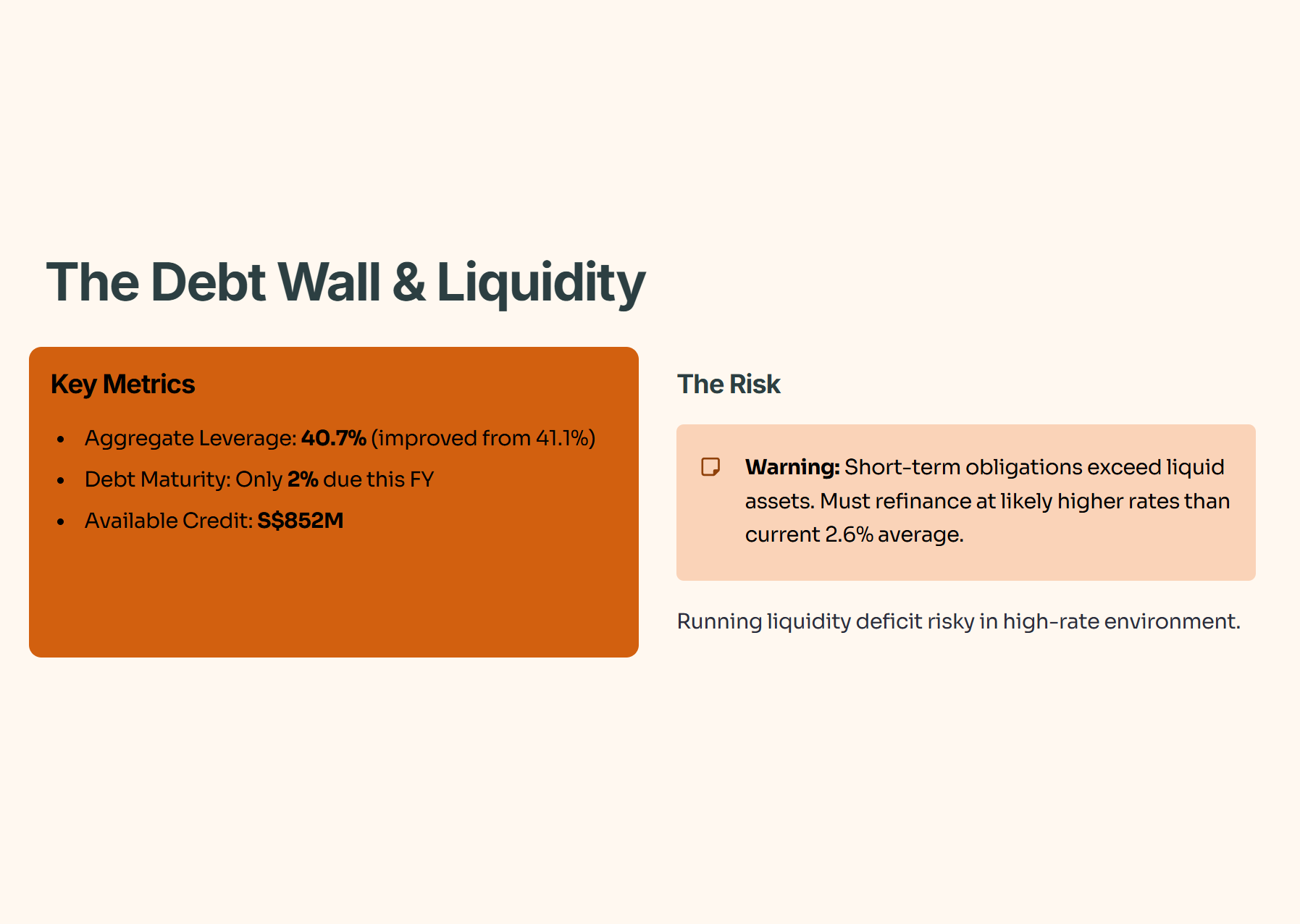

3. The Debt Wall & Liquidity (Balance Sheet)

The Data:

Aggregate Leverage: 40.7% (Slight improvement from 41.1%).

Debt Maturity: Only 2% of debt is due for the rest of this financial year.

Note: Premium members use code INVESTINGIGUANA for 55% OFF InvestingPro to run these health checks on your own portfolio.

The Risk:

Iggy’s Take:

Look at the InvestingPro screenshot I shared above. It flashes a warning: “Short term obligations exceed liquid assets.”

While MLT has credit facilities to cover this (approx. S$852M available), running a liquidity deficit is risky in a high-rate environment. They must refinance, and they will likely refinance at rates higher than their historical average (which is currently a low 2.6%).

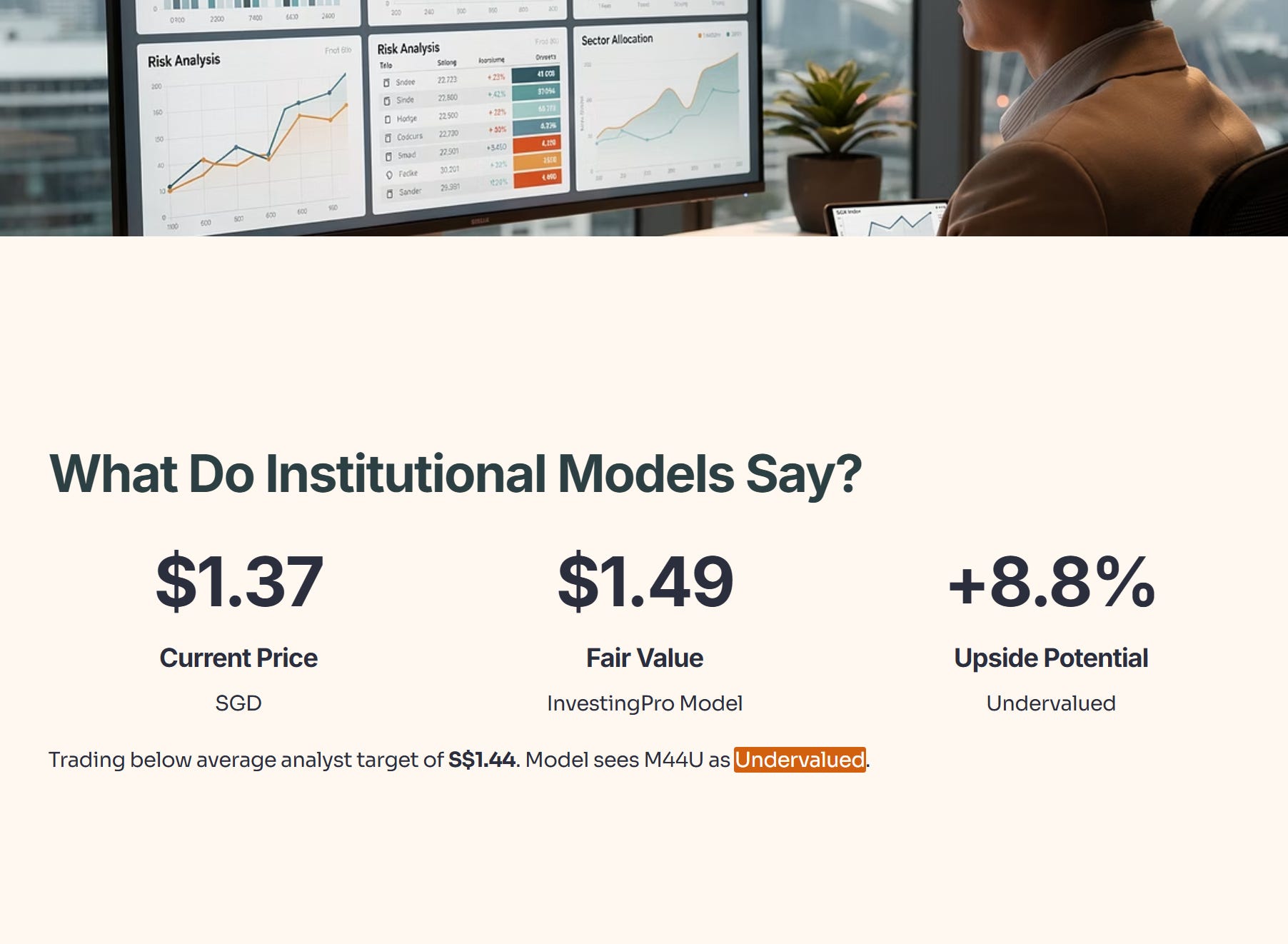

🛑 Reality Check: What do the Institutional Models Say?

The slides say “Stable,” but what does the math say? I ran M44U through the InvestingPro Fair Value Model to remove the emotion.

The Verdict:

Current Price: S$1.37

Fair Value: S$1.49

Upside: +8.8%

Iggy’s Analysis:

The model sees M44U as Undervalued. It is trading below the average analyst target of S$1.44.

However, look at the Financial Health Score on the right: 2/5 (Fair).

Specifically, Growth Health is 1/5. The algorithm hates the declining Revenue and DPU. This tells me MLT is a “Value Play,” not a “Growth Play.” You are buying S$1.00 of assets for S$0.90, but don’t expect that asset to grow fast.

The Iggy Scorecard: M44U (3Q FY25/26)