SGX Alert: Stop Buying These 3 Stocks on Dec 22

Three stocks enter. Three stocks leave. On 22 December, passive flows will force price moves—here is your playbook to exploit the volatility.

The Singapore stock market just got smaller in one tier and slightly richer in another. On 9 December, SGX Indices announced the quarterly rebalancing of the iEdge Singapore Next 50, effective 22 December 2025.

If you are a casual observer, you might ignore this. You might think, “I only care about the STI.” But if you manage your own capital, ignoring this rebalance is a mistake. This index is the waiting room for the STI. It is where liquidity builds or dies. And when the index changes, passive funds are forced to move money—creating artificial supply and demand that has nothing to do with earnings and everything to do with mechanics.

Iggy’s Insight:

Most retail investors treat index announcements as “Buy” signals. That is the quickest way to lose money. By the time you read the headline, the algorithm bots have already front-run the trade. The real opportunity isn’t chasing the entrance; it’s waiting for the liquidity gap to settle. We are looking for mispricing, not popularity.

In This Article:

• The Mechanics: Why Flows Matter More Than Fundamentals

• The Three Companies Moving In

• The Three Companies Moving Out

• The Valuation Reality Check

• The “Next 50” Playbook

• Bottom Line

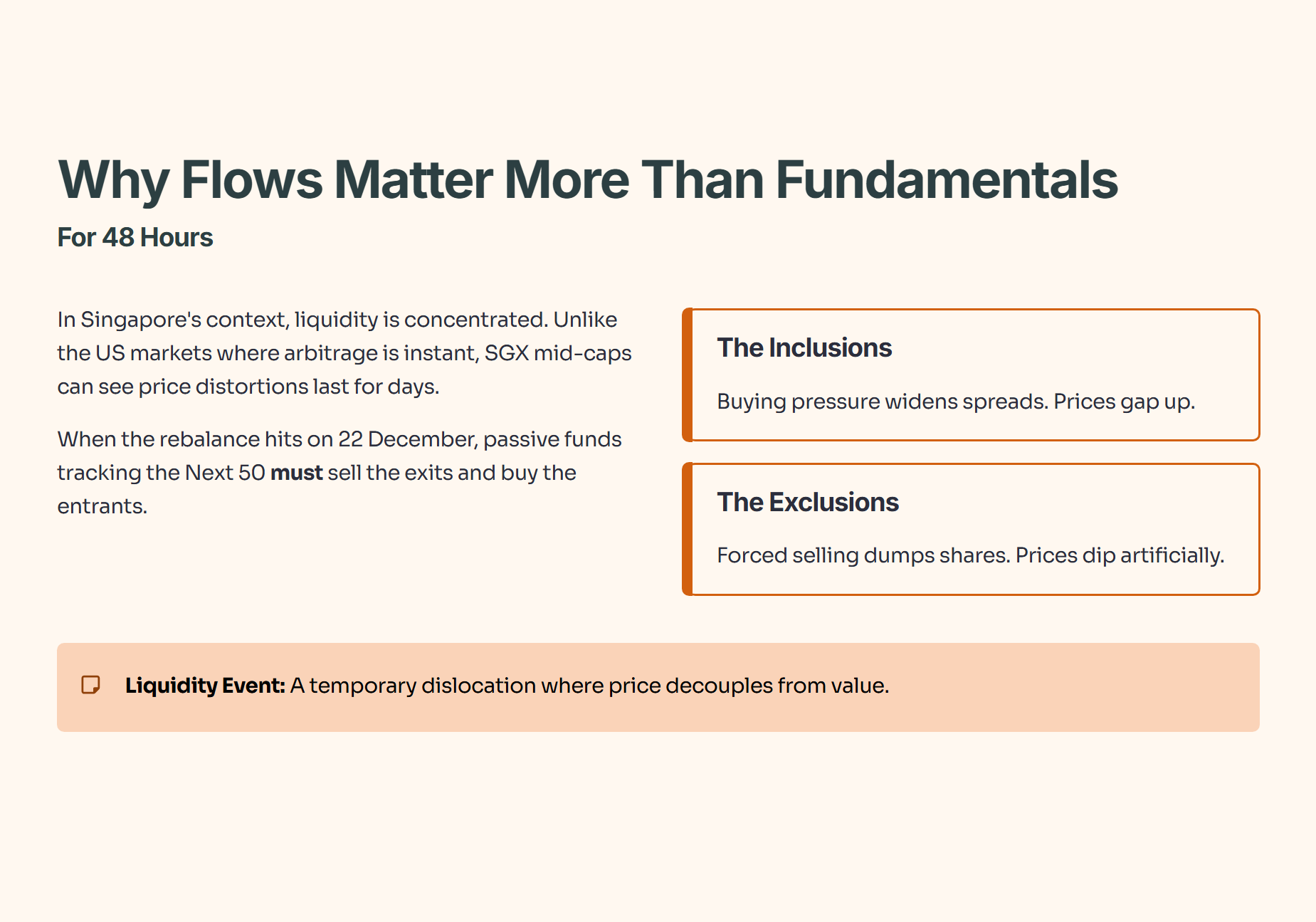

The Mechanics: Why Flows Matter More Than Fundamentals (For 48 Hours)

In Singapore’s context, liquidity is concentrated. Unlike the US markets where arbitrage is instant, SGX mid-caps can see price distortions last for days.

When the rebalance hits on 22 December, passive funds tracking the Next 50 must sell the exits and buy the entrants.

The Inclusions: Buying pressure widens spreads. Prices gap up.

The Exclusions: Forced selling dumps shares. Prices dip artificially.

This creates a “Liquidity Event.” It is a temporary dislocation where price decouples from value.

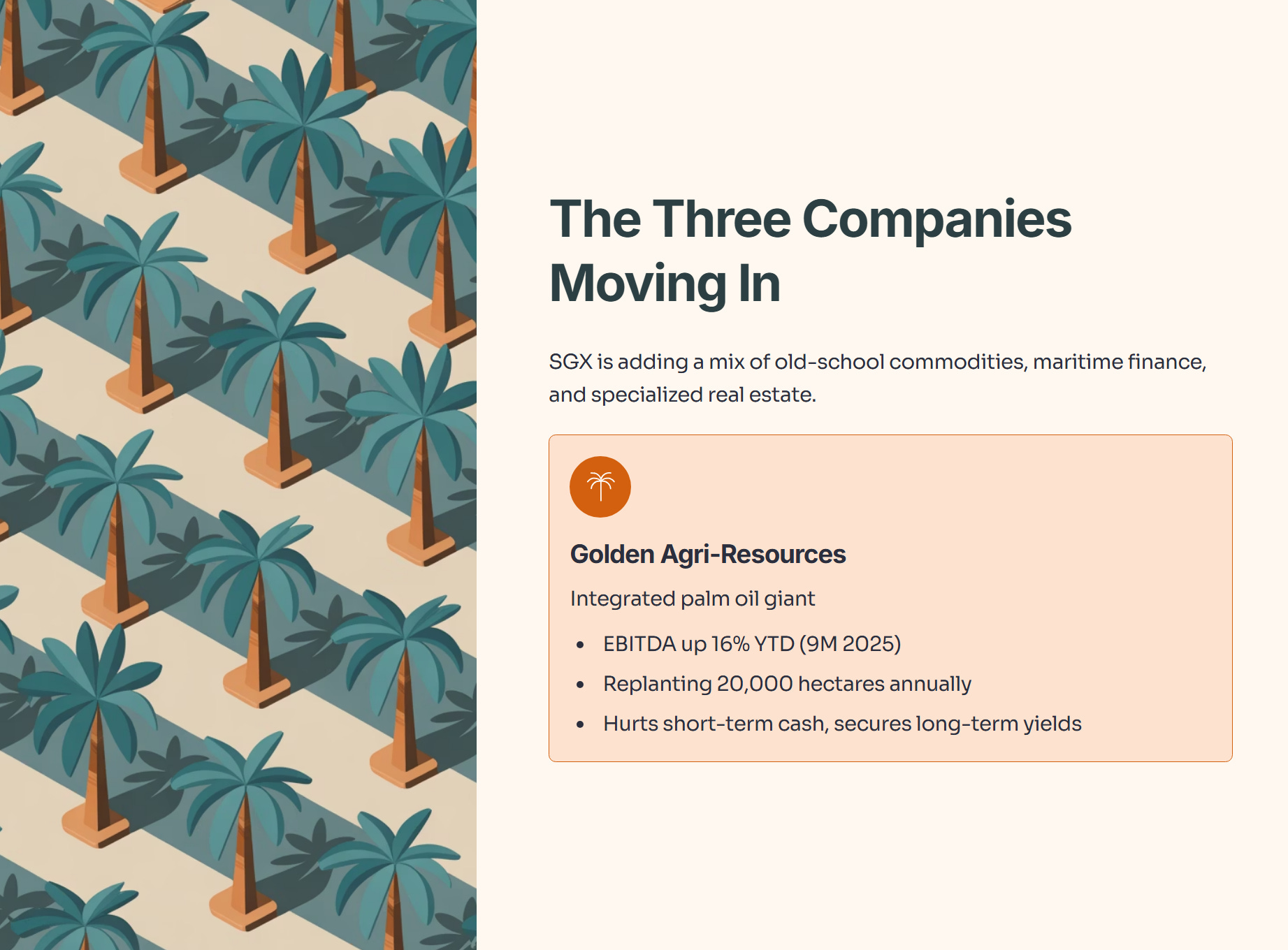

The Three Companies Moving In

SGX is adding a mix of old-school commodities, maritime finance, and specialized real estate.

1. Golden Agri-Resources (GAR)

This is the heavyweight. GAR is an integrated palm oil giant—upstream plantations, refineries, and biodiesel.

The Data: EBITDA is up 16% YTD (9M 2025).

The Context: They are replanting 20,000 hectares annually. This hurts short-term cash flow but secures long-term yields.

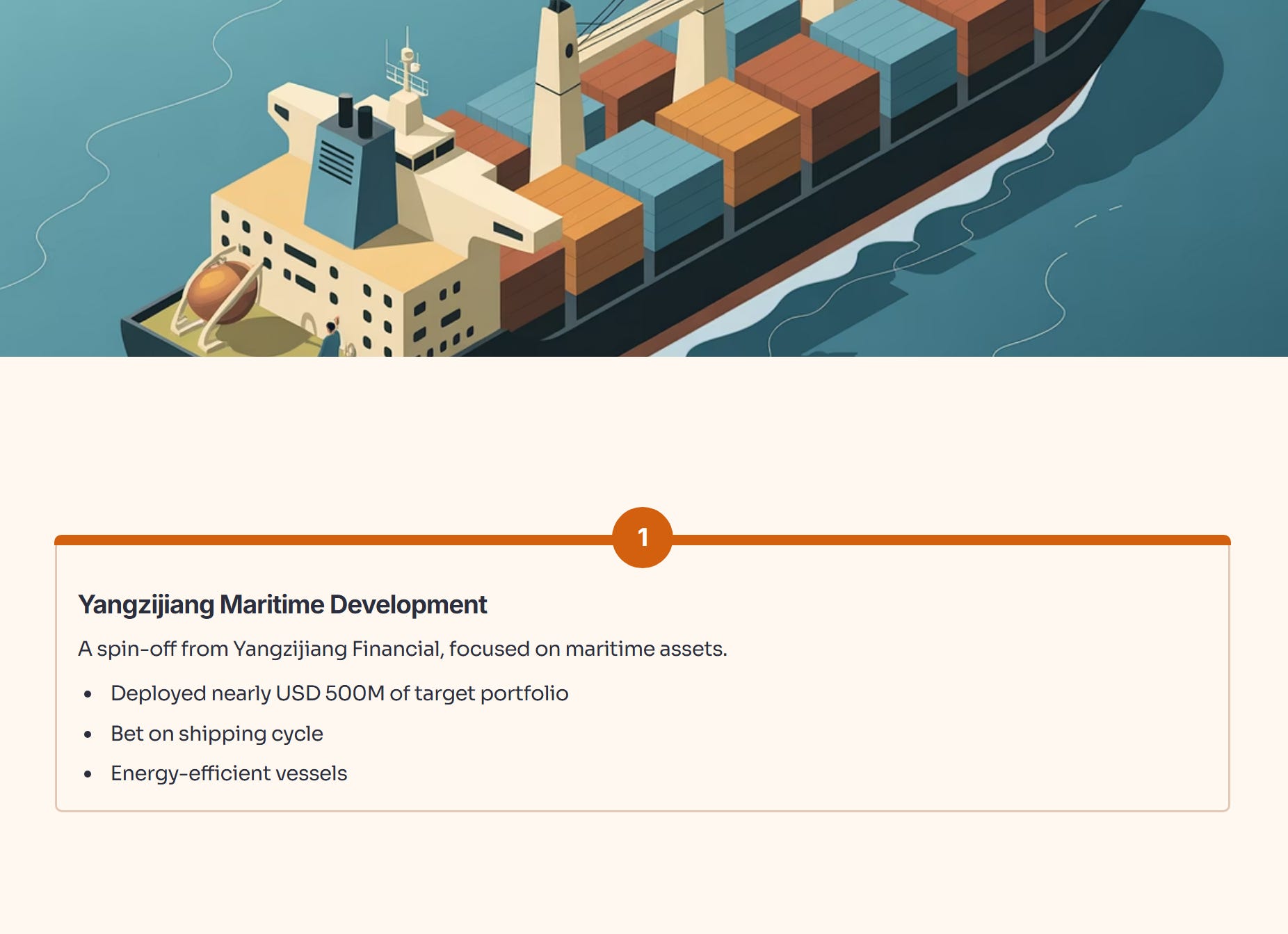

2. Yangzijiang Maritime Development (YZJ)

A spin-off from Yangzijiang Financial, focused on maritime assets. They have deployed nearly USD 500M of their target portfolio.

The Angle: This is a bet on the shipping cycle and energy-efficient vessels.

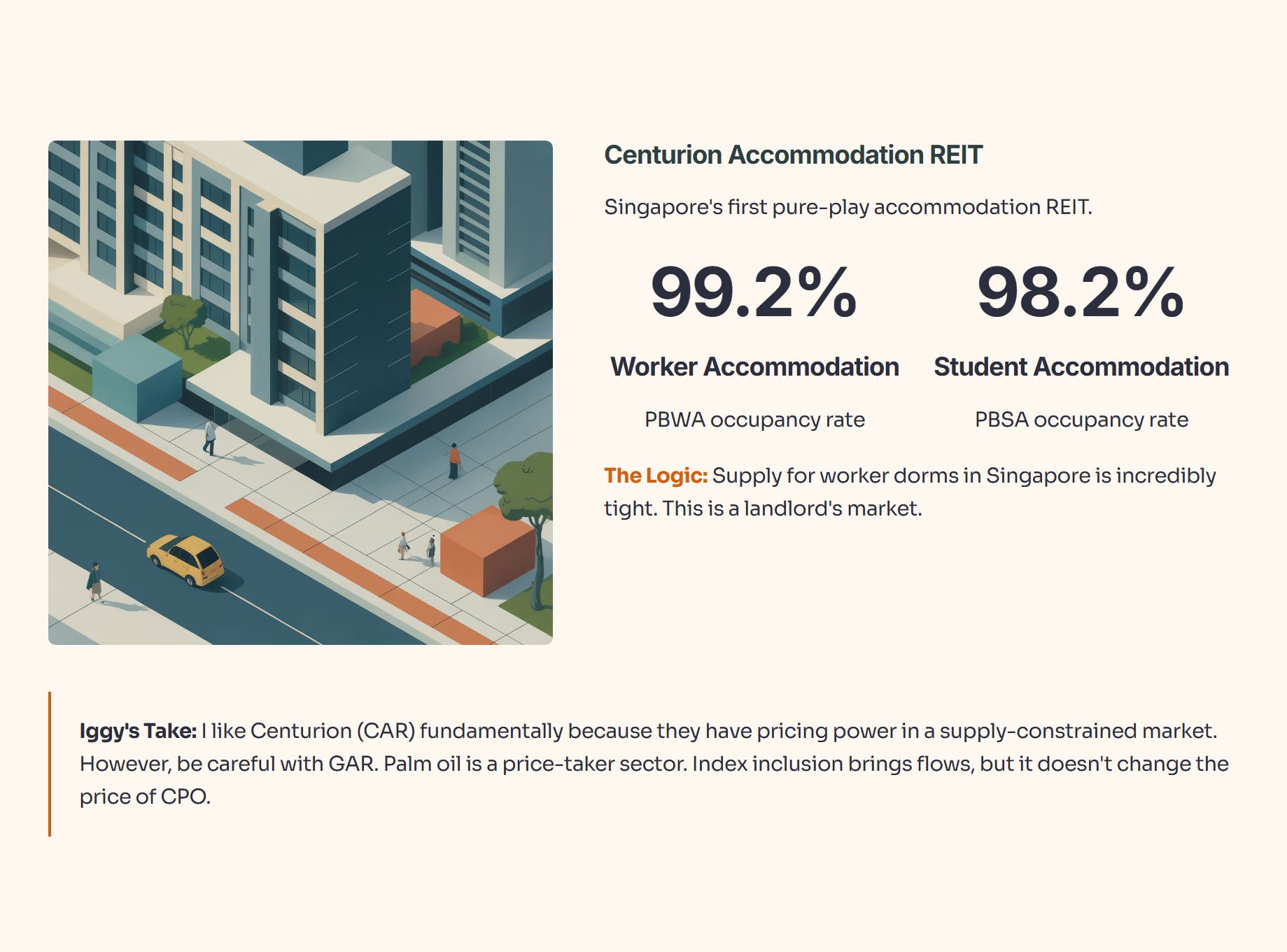

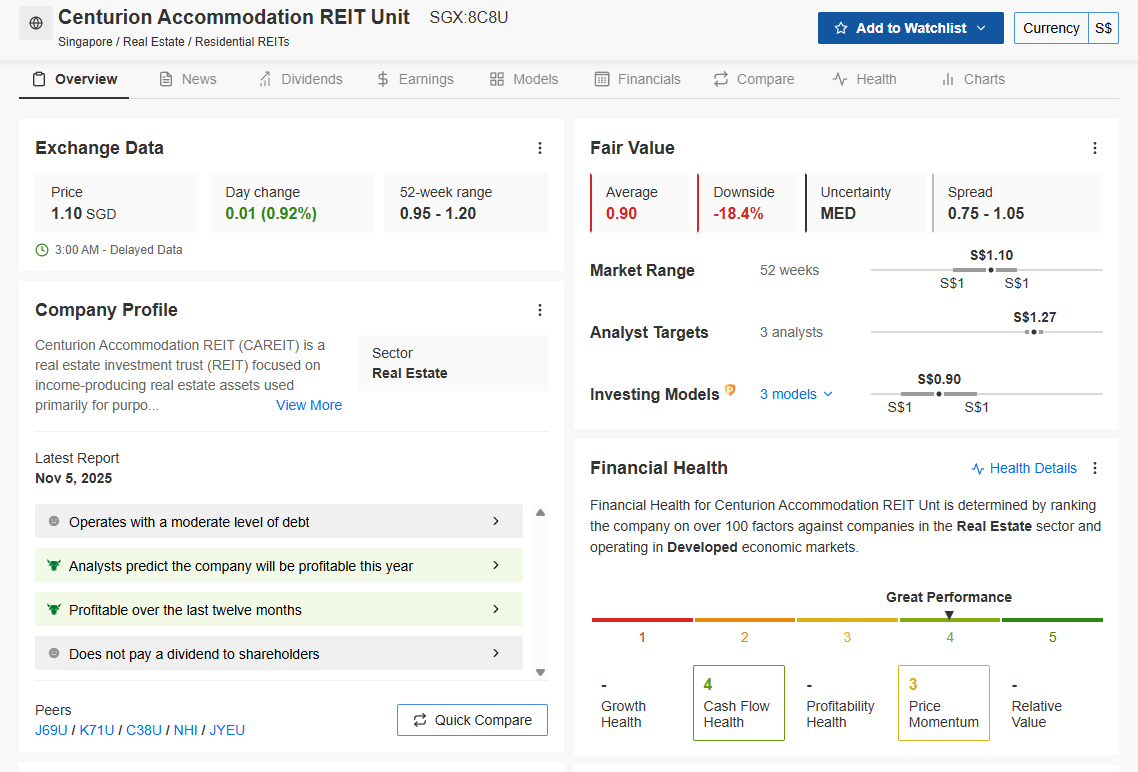

3. Centurion Accommodation REIT (CAR)

Singapore’s first pure-play accommodation REIT.

The Moat: 99.2% occupancy in Worker Accommodation (PBWA) and 98.2% in Student Accommodation (PBSA).

The Logic: Supply for worker dorms in Singapore is incredibly tight. This is a landlord’s market.

Iggy’s Take:

I like Centurion (CAR) fundamentally because they have pricing power in a supply-constrained market. However, be careful with GAR. Palm oil is a price-taker sector. Index inclusion brings flows, but it doesn’t change the price of Crude Palm Oil (CPO). Do not confuse a liquidity event with a change in business quality.

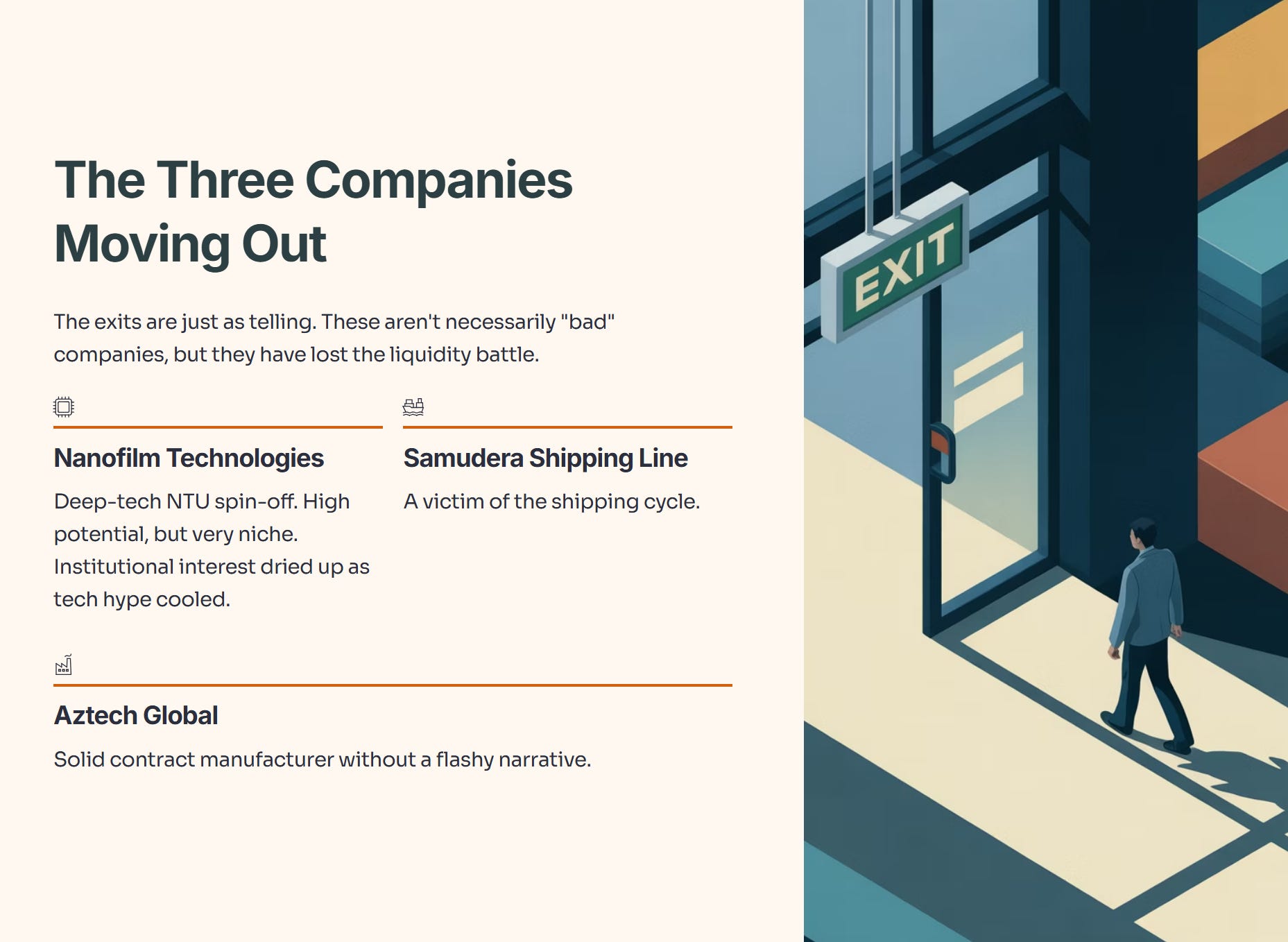

The Three Companies Moving Out

The exits are just as telling. These aren’t necessarily “bad” companies, but they have lost the liquidity battle.

Nanofilm Technologies (NFI): A deep-tech NTU spin-off. High potential, but very niche. Institutional interest has dried up as the “tech hype” cooled.

Samudera Shipping Line (SMDR): A victim of the shipping cycle.

Aztech Global (AZTECH): A solid contract manufacturer without a flashy narrative.

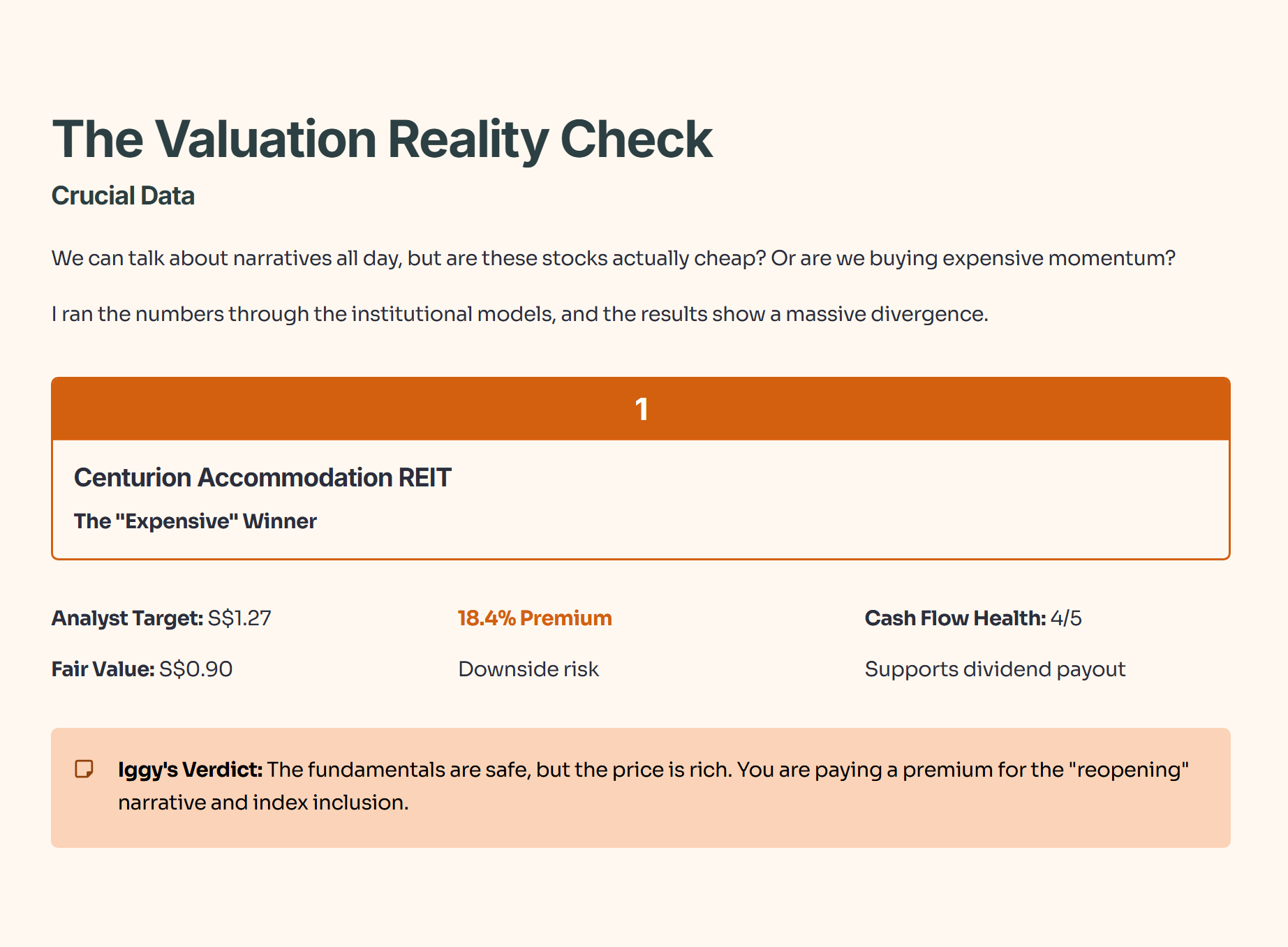

The Valuation Reality Check (Crucial Data)

We can talk about narratives all day, but are these stocks actually cheap? Or are we buying expensive momentum? I ran the numbers through the institutional models, and the results show a massive divergence.

I don’t just guess at valuations. I check the institutional models.

Source: InvestingPro (Data as of December 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

1. Centurion Accommodation REIT (The “Expensive” Winner)

The Warning: While analysts are bullish (Target: S$1.27), the quantitative Fair Value models tell a different story. The models peg the Fair Value at **S$0.90**, suggesting the stock is currently trading at an 18.4% premium (Downside risk).

The Health Score: The “Cash Flow Health” is excellent (4/5), which supports the dividend payout.

Iggy’s Verdict: The fundamentals are safe, but the price is rich. You are paying a premium for the “reopening” narrative and index inclusion.

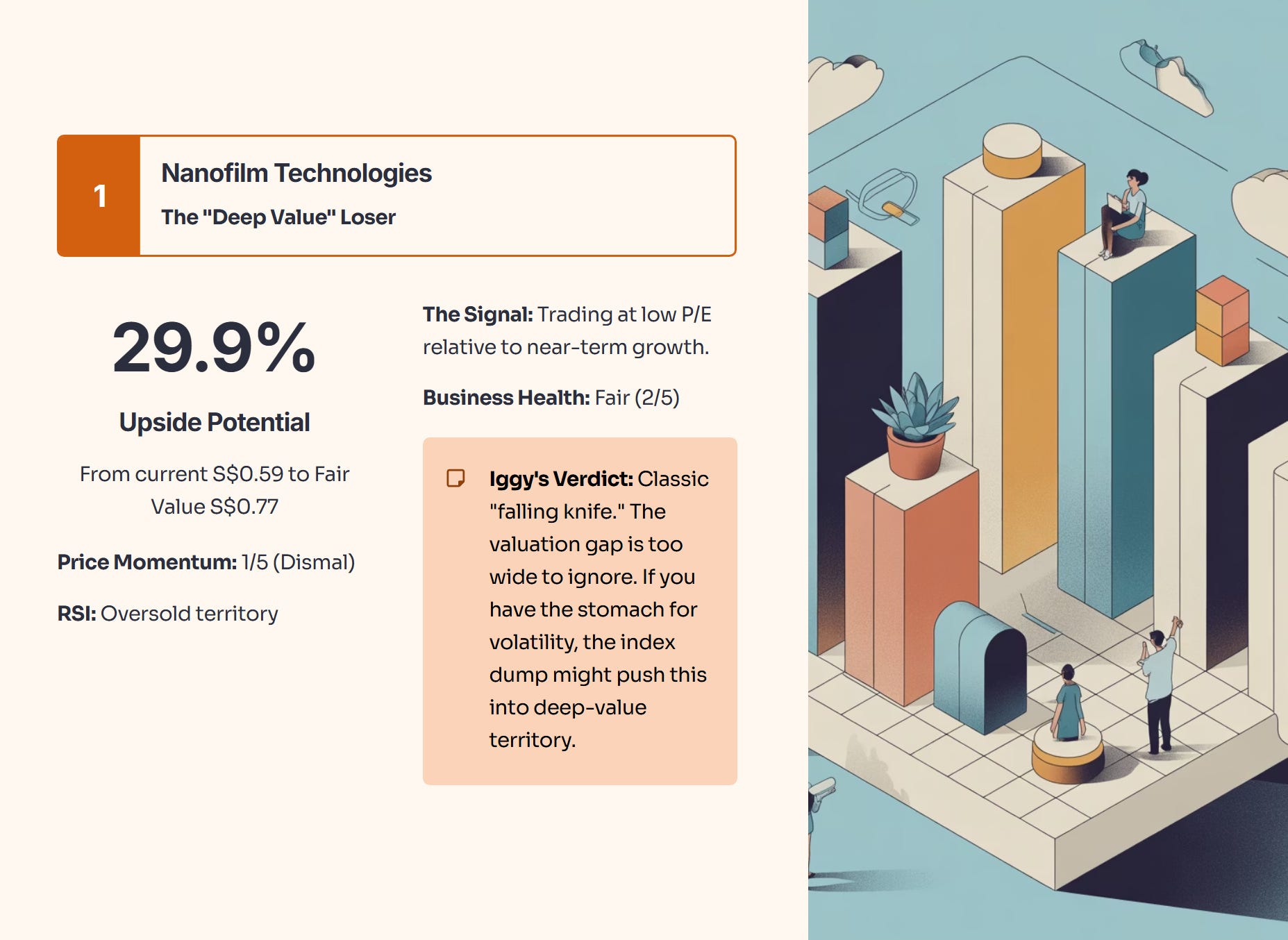

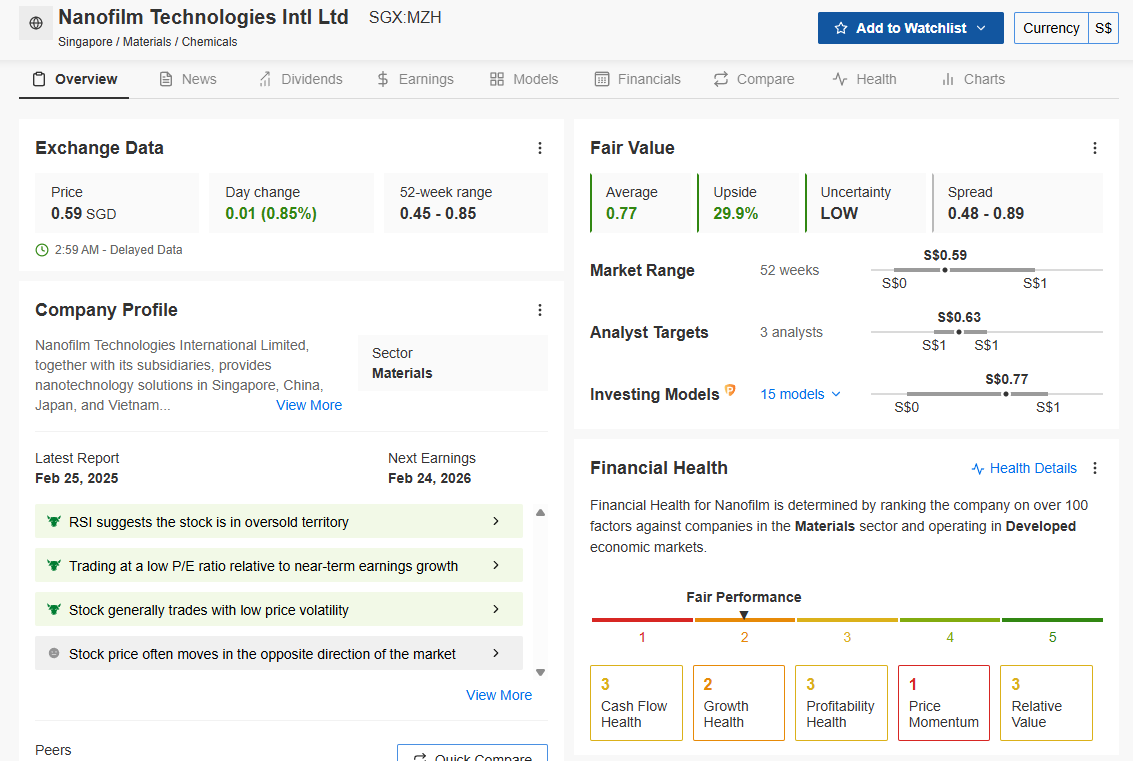

2. Nanofilm Technologies (The “Deep Value” Loser)

The Opportunity: The market hates this stock right now (Price Momentum is a dismal 1/5). However, the valuation is screaming “Bargain.” The models calculate a Fair Value of S$0.77, offering a massive 29.9% Upside from the current price of S$0.59.

The Signal: The RSI indicates the stock is in “oversold territory,” and it is trading at a low P/E relative to near-term growth.

Iggy’s Verdict: This is a classic “falling knife.” The business health is only “Fair” (2/5), but the valuation gap is too wide to ignore. If you have the stomach for volatility, the index dump might push this into deep-value territory.

The “Next 50” Playbook

So, how do we trade this using the data above?