November’s Dividend Calendar: The Hidden Opportunities Singapore Investors Are Missing

Don't miss these crucial ex-dividend dates in November

Most investors chase yield. Smart investors chase sustainable yield. November 2025 brings 29 dividend-paying Singapore stocks to the table, but only a handful deserve your attention.

The challenge? Spotting diamonds among ordinary pebbles. High yields can mask troubled businesses, while modest payouts might signal rock-solid fundamentals. The key is understanding what each dividend truly represents about a company’s financial health.

In This Article:

• The Big Picture: What November Reveals

• My November Watchlist: Four Stocks Worth Your Attention

• Lum Chang Holdings: Riding the Construction Wave

• GuocoLand: Property Developer with Patience Required

• Micro-Mechanics: Semiconductor Dividend Machine

• Mapletree Pan Asia Commercial Trust: The REIT Anchor

• The Ones to Watch (But Maybe Skip)

• The Overlooked November Picks: High Risk, High Reward

• Lum Chang Creations (Yield: Speculative)

• Ossia International (Yield: 4.19%)

• Ellipsiz (Yield: 3.45%)

• What This Dividend Calendar Really Tells Us

• How to Approach November Dividends

• The CPF/SRS Angle Most People Miss

• Key Risks Every Dividend Investor Must Know

• November Dividend Action Plan

• The Bottom LineThe Big Picture: What November Reveals

Singapore’s dividend landscape shows fascinating dynamics this November. Construction stocks are riding a multi-year boom fueled by public infrastructure projects. REITs benefit from falling interest costs as financing expenses decline. And select industrial players continue their steady march forward.

But here’s what most analysts won’t tell you: dividend yield alone is a terrible metric. A 4% yield from a declining business is worse than 2% from a growing one. Context matters.

My November Watchlist: Four Stocks Worth Your Attention

After analyzing all 29 November dividend payers, four names stand out for different reasons. These picks balance yield, growth potential, and risk profiles suitable for income-focused Singaporean investors.

Lum Chang Holdings: Riding the Construction Wave

Lum Chang represents the most compelling construction play in November’s dividend roster. The stock has delivered a stunning 69.6% total return year-to-date, crushing the STI’s 21.1% gain.

Why it works: Singapore’s construction sector faces a multi-year upswing. The Building and Construction Authority forecasts $47-53 billion in contracts for 2025 alone. Lum Chang’s A1-grade contractor status positions it perfectly to capture major projects like Changi Terminal 5, MRT extensions, and public housing developments.

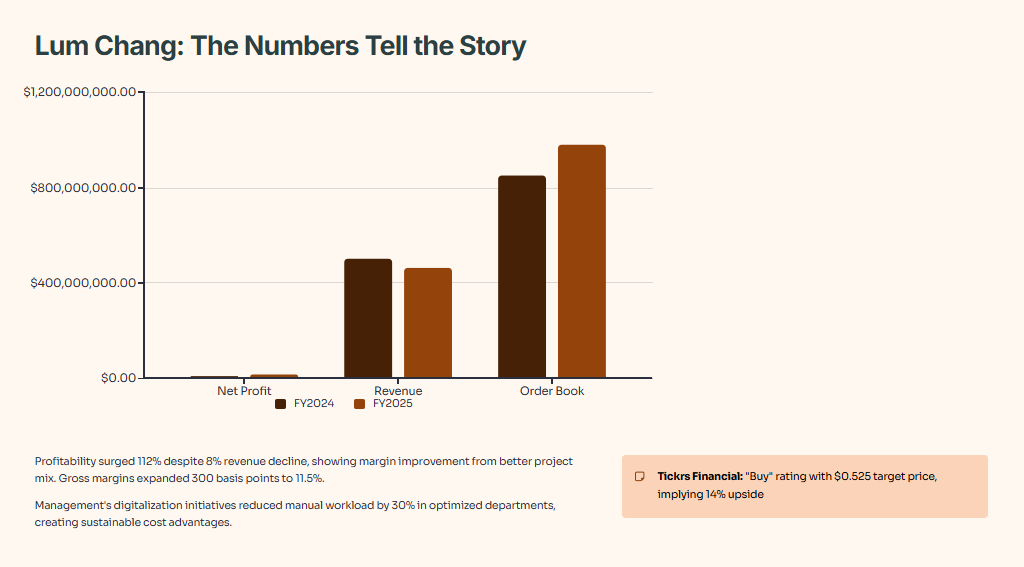

The numbers tell the story. Full-year FY2025 net profit surged 112% to $15.6 million, while gross margins expanded by 300 basis points to 11.5%. Management’s digitalization initiatives reduced manual workload by 30% in optimized departments, creating sustainable cost advantages.

Lum Chang declares a 2.17% dividend yield with November 5th as the ex-dividend date. The improved payout ratio reflects management’s confidence in sustained earnings power. Tickrs Financial assigns a “buy” rating with a $0.525 target price, implying 14% upside from current levels.

Lum Chang’s profitability surge despite revenue decline shows margin improvement from better project mix and cost control

The risk? Construction cycles turn. Labor shortages could pressure margins. Execution mishaps on large projects hurt contractors fast. But with a net-cash balance sheet and visible multi-year pipeline, Lum Chang offers growth and income.

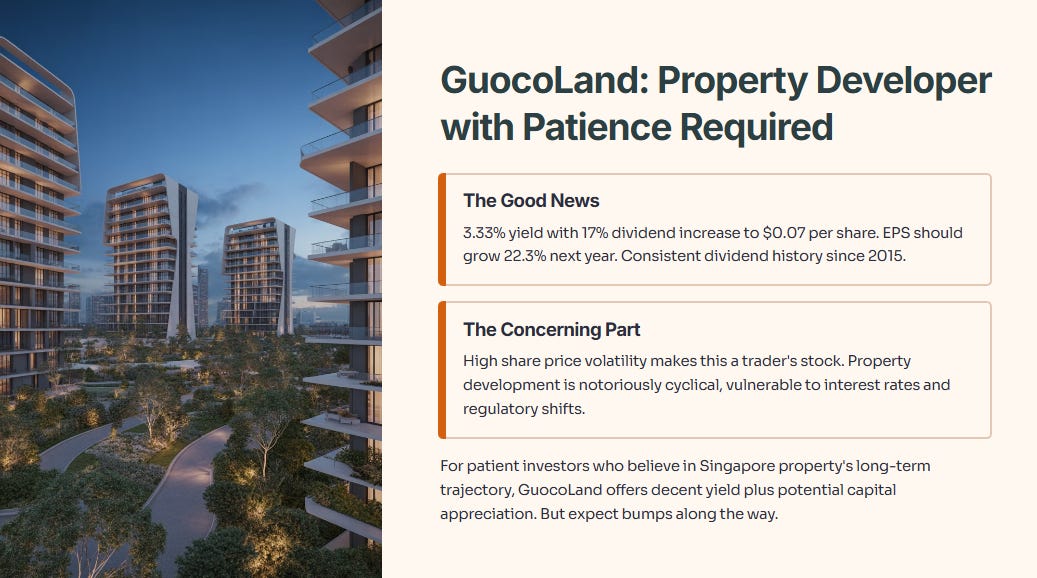

GuocoLand: Property Developer with Patience Required

GuocoLand splits opinion. The 3.33% yield looks attractive, and the company just increased dividends by 17% to $0.07 per share for November 4th payment. But dig deeper and you’ll find complexity.

The good news: earnings per share should grow 22.3% next year. The payout ratio sits at 71% of earnings, leaving room for flexibility. GuocoLand maintains consistent dividend history since 2015, though growth has been modest at 1.8% annually.

The concerning part: share price volatility makes this a trader’s stock more than an income play. The company operates in property development, a notoriously cyclical sector vulnerable to interest rate changes and regulatory shifts.

For patient investors who believe in Singapore property’s long-term trajectory, GuocoLand offers decent yield plus potential capital appreciation. But expect bumps along the way.

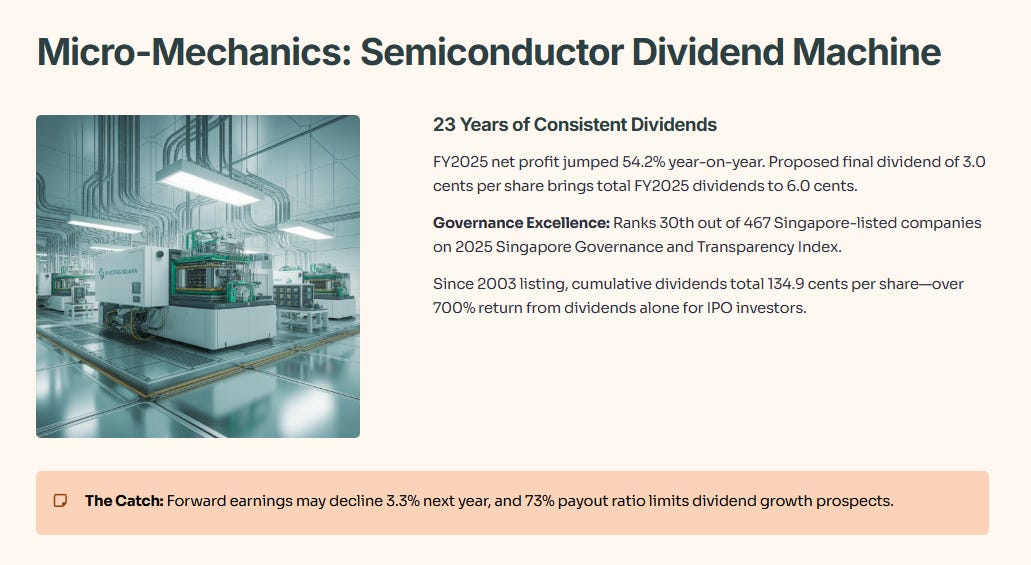

Micro-Mechanics: Semiconductor Dividend Machine

Here’s a name most retail investors miss. Micro-Mechanics operates in semiconductor equipment manufacturing, paying dividends consistently for 23 years. The November 6th ex-dividend brings a 1.71% partial payout.

Recent results impress. FY2025 net profit jumped 54.2% year-on-year, driven by precision manufacturing demand. The company proposed a final dividend of 3.0 cents per share, bringing total FY2025 dividends to 6.0 cents.

The standout feature? Governance excellence. Micro-Mechanics ranks 30th out of 467 Singapore-listed companies on the 2025 Singapore Governance and Transparency Index. Since listing in 2003, cumulative dividends total 134.9 cents per share—over 700% return from dividends alone for IPO investors.

The catch: forward earnings may decline 3.3% next year, and the payout ratio hovers near 73%. This limits dividend growth prospects. Still, for investors seeking exposure to semiconductor sector recovery with income, Micro-Mechanics deserves consideration.

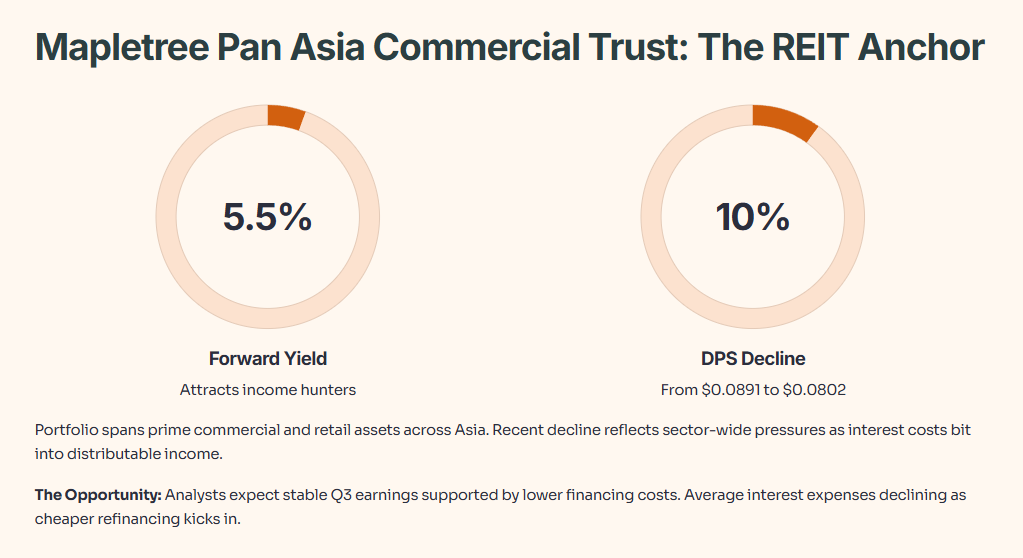

Mapletree Pan Asia Commercial Trust: The REIT Anchor

REITs dominate high-yield investing in Singapore, and Mapletree Pan Asia Commercial Trust exemplifies why. The 5.5% forward yield attracts income hunters, though November’s distribution represents just 0.3% and 1.05% across two separate payouts.

The REIT’s portfolio spans prime commercial and retail assets across Asia. Recent performance shows dividend per share of $0.0802 in 2025, down 10% from 2024’s $0.0891. This decline reflects sector-wide pressures as interest costs bit into distributable income.

But here’s the opportunity: analysts expect Singapore REITs to deliver stable Q3 earnings supported by lower financing costs. Average interest expenses are declining as cheaper refinancing kicks in. For REITs with high floating-rate debt exposure, savings flow directly to distribution per unit.

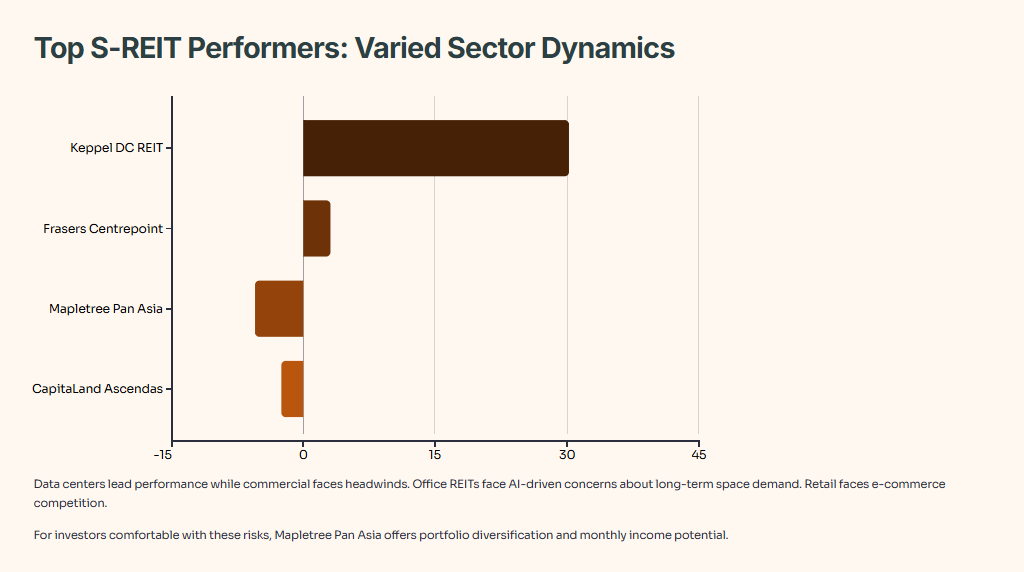

Top S-REIT performers show varied sector dynamics, with data centers leading and industrial facing headwinds

The risk with REITs centers on interest rate volatility and occupancy pressures. Office REITs face AI-driven concerns about long-term space demand. Retail faces e-commerce competition. But for investors comfortable with these risks, Mapletree Pan Asia offers portfolio diversification and monthly income potential.

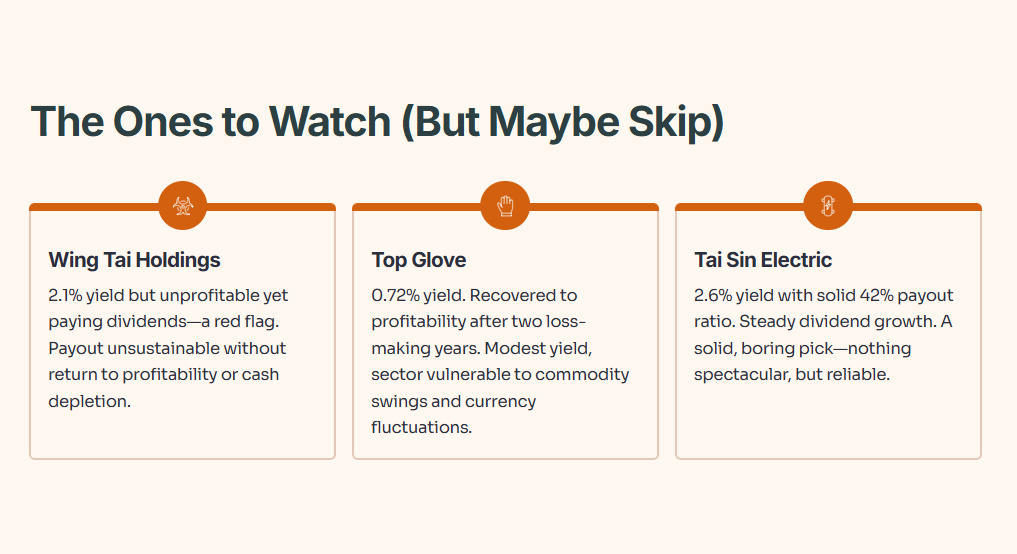

The Ones to Watch (But Maybe Skip)

Several November payers deserve mention but don’t make my top picks:

Wing Tai Holdings pays 2.1% yield but shows concerning fundamentals. The company is unprofitable yet continues paying dividends—a red flag. The payout is unsustainable without either return to profitability or cash reserve depletion.

Top Glove recovered to profitability after two loss-making years, paying 0.72% yield. The Malaysian glove maker benefits from improved demand and cost management. But the yield is modest, and the sector remains vulnerable to commodity price swings and currency fluctuations.

Tai Sin Electric offers 2.6% yield with solid earnings coverage at 42% payout ratio. The electrical equipment distributor shows steady dividend growth over time. It’s a solid, boring pick—nothing spectacular, but reliable.

The Overlooked November Picks: High Risk, High Reward

For aggressive income investors willing to venture into smaller caps, November offers intriguing options:

Lum Chang Creations (Yield: Speculative) This is the high-risk, “story stock” offspring of the more stable Lum Chang Holdings. Spun off to focus on the sexy, high-margin niche of urban revitalization and heritage conservation, LCC is a pure bet on a narrative.

The Bull Case: This is a direct play on Singapore’s multi-year, government-backed revitalization boom. The company has a robust order book and has promised a dividend payout ratio of at least 30% for FY2025-2026.

The “Iguana” Take (The Risk): This is not a dividend stock; it’s a dividend promise. As a new spin-off, it has no payment track record. More importantly, its “niche” is inherently “lumpy.” Revenue won’t be a smooth, quarterly stream but will arrive in large, inconsistent chunks as major projects are completed. You are betting that management can 1) constantly win these specialized contracts and 2) will actually follow through on the payout policy. This is a speculative venture, not a reliable income source.

Ossia International (Yield: 4.19%) On the surface, a 4.19% yield from a distributor of known brands like Tumi and Columbia looks tempting. But this is a classic “due diligence required” stock. Ossia operates as a holding company with the majority of its revenue coming from Taiwan, not Singapore. This makes it opaque for local investors to analyze. Worse, public data on its dividend history is conflicting, a major red flag. This high yield might be a siren’s call for a business facing low-visibility retail headwinds in an overseas market. It’s a bet on management, not a clear-cut dividend play.

Ellipsiz (Yield: 3.45%) This is not an “electronics manufacturing” stock; it’s a “special situations” play. Ellipsiz is a diversified holding company whose segments include semiconductor equipment distribution, property investment, and... egg production. This lack of focus makes it incredibly difficult to value. Recent profit guidance was positive, but this was driven by a one-off gain from selling an asset, not a surge in core operations. Furthermore, the dividend is not well covered by free cash flow. Buying this for the 3.45% yield is missing the point—you’re not investing, you’re speculating that management can successfully unlock value from its bizarre collection of assets. This is for speculators only.

What This Dividend Calendar Really Tells Us

November’s dividend roster reveals three key themes:

Construction dominance: Multiple construction-related names appear, reflecting sector strength. This validates the multi-year infrastructure spending cycle. But remember: cycles peak. Position sizing matters.

REIT resilience: Lower financing costs are breathing life back into REITs after years of interest rate pain. The sector offers immediate income but limited growth. Suitable for retirees and income-focused portfolios.

Industrial variability: Industrial stocks show mixed results. Winners like Micro-Mechanics benefit from secular growth trends (semiconductors). Losers face structural headwinds (traditional manufacturing, shipbuilding).

How to Approach November Dividends