I Ran OCBC's BUY Call on UOB Through My Forensic Screen. Here Is What They Missed | EP1601🦖

UOB earns a Zone 3 Conditional — which means the dividend is safe, but the capital growth story is a 2030 promise, not a 2026 delivery.

Management is guiding for a 2026 Net Interest Margin as low as 1.75%. That is a sharp drop from the 2.03% high just two years ago. If you are relying on bank dividends to fund your retirement drawdown, this compression hits your safety margin directly.

Today, I am auditing whether OCBC’s new BUY call on UOB actually survives my forensic screen.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips — the interest coverage, the gearing, the free cash flow sustainability — so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

In This Article:

The health check solvency

Financial health checklist

How Iggy rates every stock

The wealth check yield and cash flow

The price check valuation

Analyst audit the loan book and the war

The forensic gap Iggy vs OCBC

The bottom line forensic stance

Iggy’s forensic disclaimer

THE HEALTH CHECK (Solvency)

The core lending engine is slowing down. But the wealth management pivot is starting to pick up the slack. Net profit of S$1,437m beat the consensus estimate. However, the underlying income streams are shifting. That requires a closer look at the balance sheet stability.

Financial Health Checklist

How Iggy Rates Every Stock

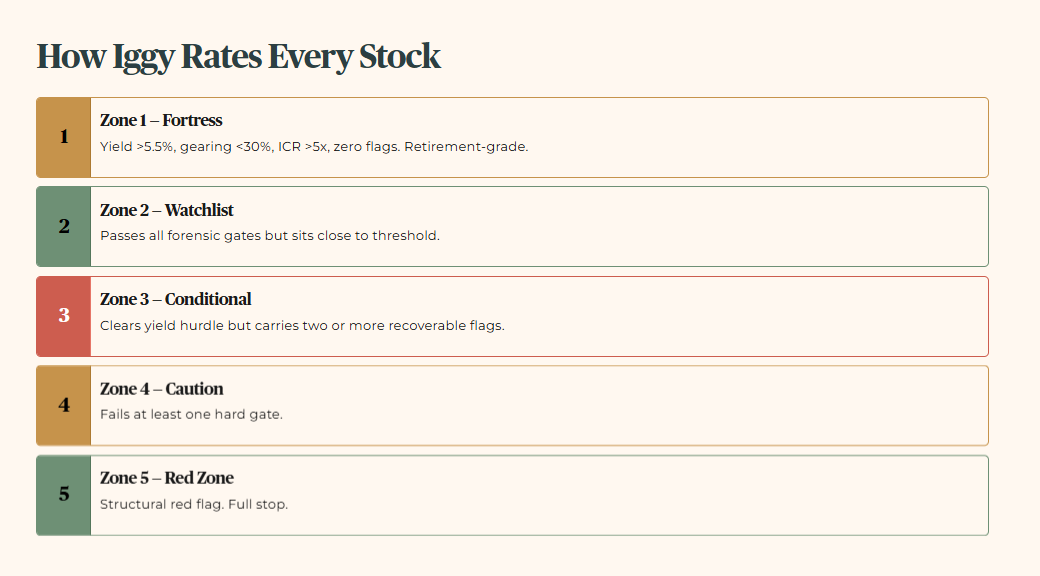

Every stock I track is assigned a Forensic Zone. That is a structured rating based on yield, gearing, interest coverage, and balance sheet flags. There are five zones. Zone 1 Fortress is retirement-grade: yield above 5.5%, gearing below 30%, interest coverage ratio (ICR) above 5x, and zero structural flags. Zone 2 Watchlist passes all forensic gates but sits close to threshold. Zone 3 Conditional clears the yield hurdle but carries two or more recoverable flags. Zone 4 Caution fails at least one hard gate. Zone 5 Red Zone carries a structural red flag, full stop. Elite Investors receive the full forensic rationale, soft flag breakdown, and zone trajectory commentary for every stock I cover.

THE WEALTH CHECK (Yield and Cash Flow)

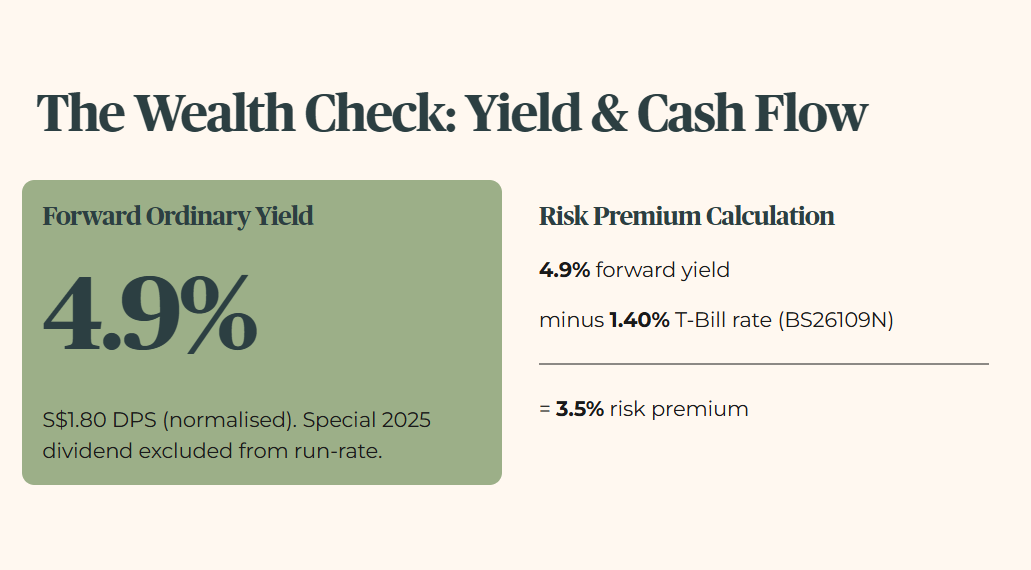

For a retail investor, the dividend is the only truth that matters. OCBC is projecting a normalised dividend per share of S$1.80 per year. That equates to a forward ordinary yield of 4.9% at current levels. Note: this figure reflects the recurring forward ordinary dividend only. The 2025 special dividend is excluded from this base and should not be used as the run-rate income assumption.

The calculation is straightforward. 4.9% forward ordinary yield minus 1.40% (BS26109N, current T-Bill rate from the Iggy Macro Dashboard) equals a risk premium of 3.5%.

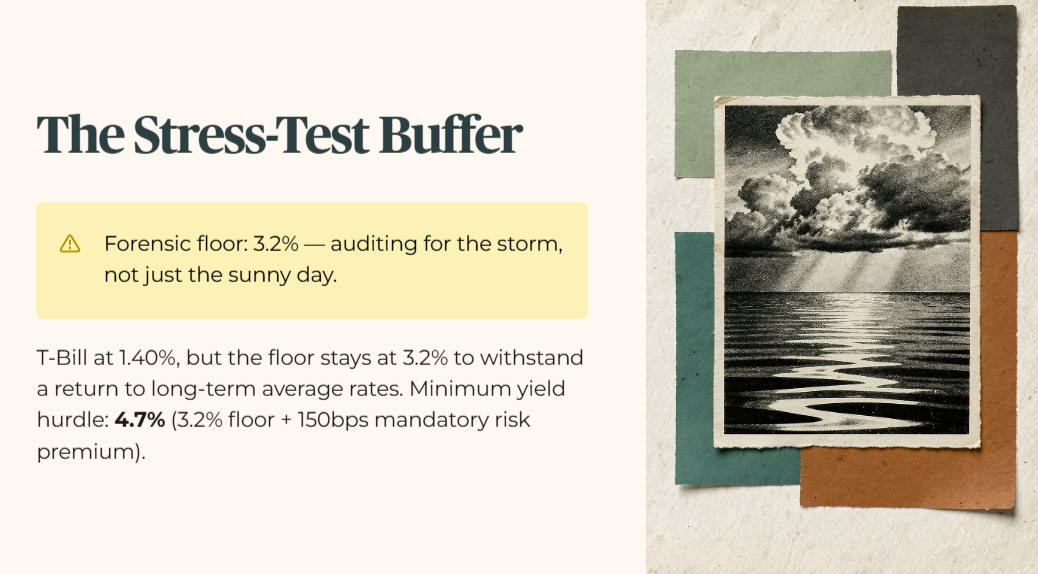

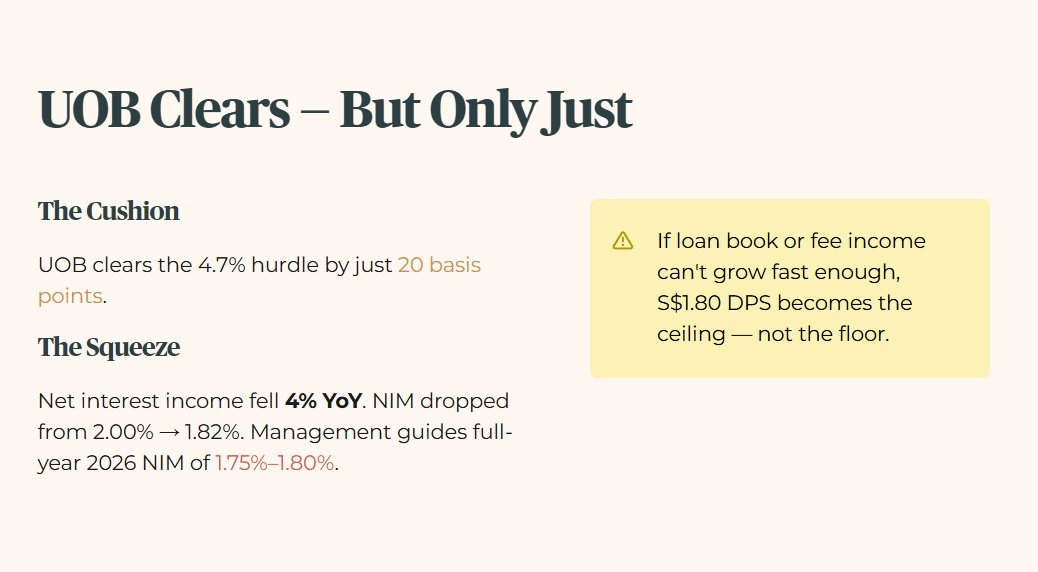

Note on the Stress-Test Buffer: For this audit, I apply a conservative forensic floor of 3.2%. We audit for the storm, not just the sunny day. The T-Bill sits at 1.40% (BS26109N). But I do not lower my standards to match a temporary market dip. My floor remains at 3.2% to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7%, which is the 3.2% floor plus 150 basis points of mandatory risk premium.

UOB currently clears this hurdle with a 20 basis point cushion. But we must look at the quality of that yield. Net interest income fell 4% year on year. The gap between what the bank earns on loans and what it pays for deposits is narrowing. This is the Net Interest Margin, or NIM. Think of it like the gross profit margin of a bank. When NIM falls from 2.00% to 1.82%, the bank has to work much harder just to stay in the same place.

Management has been very honest about the headwind. They expect NIM to settle between 1.75% and 1.80% for the full year 2026. If they cannot grow the loan book or fee income fast enough, that S$1.80 dividend starts to look like the ceiling rather than the floor.

THE PRICE CHECK (Valuation)

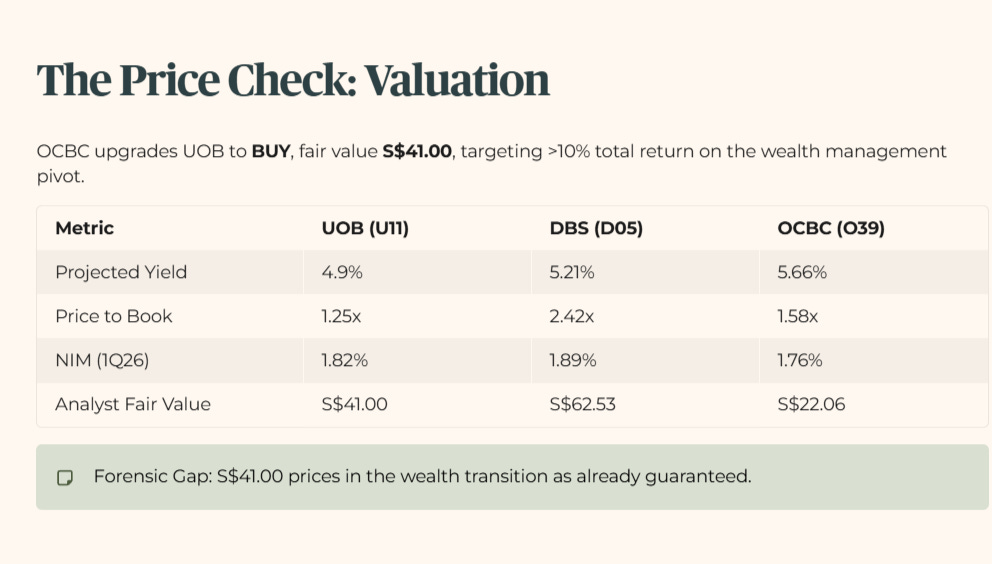

OCBC Research has upgraded UOB from Hold to BUY with a fair value of S$41.00. They are betting on a total return of more than 10%. That is driven largely by the bank’s pivot toward wealth management.

Peer Comparison Table

The Forensic Gap here is the difference between what the analyst thinks the bank is worth and what the raw financial data suggests. At a S$41.00 fair value, the market would be pricing UOB as if the wealth management transition is already a guaranteed success.

🦎 Iggy’s Insight

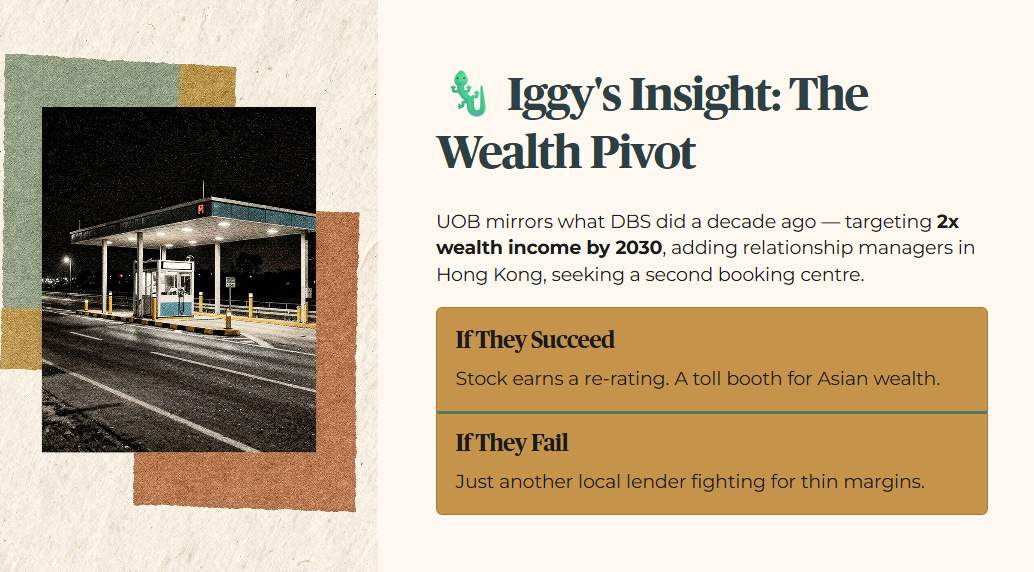

UOB is moving into a transition phase that mirrors what DBS did a decade ago. By targeting a doubling of wealth income by 2030, they are trying to reduce their reliance on the volatile interest rate cycle. That is why they are adding relationship managers in Hong Kong and looking for a second booking centre. They are building a toll booth for Asian wealth. If they succeed, the stock earns a re-rating. If they fail, they are just another local lender fighting for thin margins. The wealth pivot is the only story that matters now.

ANALYST AUDIT: THE LOAN BOOK AND THE WAR

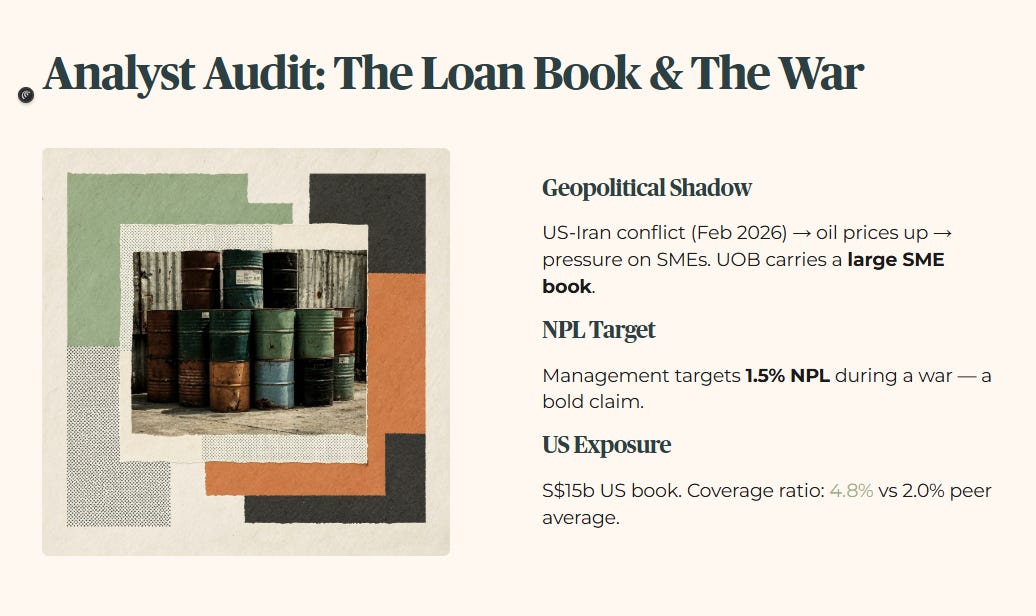

We cannot talk about UOB without talking about the geopolitical shadow. In February 2026, the US and Iran entered a period of heightened conflict. This usually sends oil prices up, which puts pressure on Small and Medium Enterprises (SMEs). UOB has a large SME book.

Management is targeting a Non-Performing Loan (NPL) ratio of 1.5%. An NPL is a loan where the borrower has stopped making payments. Keeping this at 1.5% during a war is a bold claim. They are also watching their US exposure of S$15b closely. Their coverage ratio for US loans is high at 4.8%. But a systemic property crash in the US would still leave a mark.

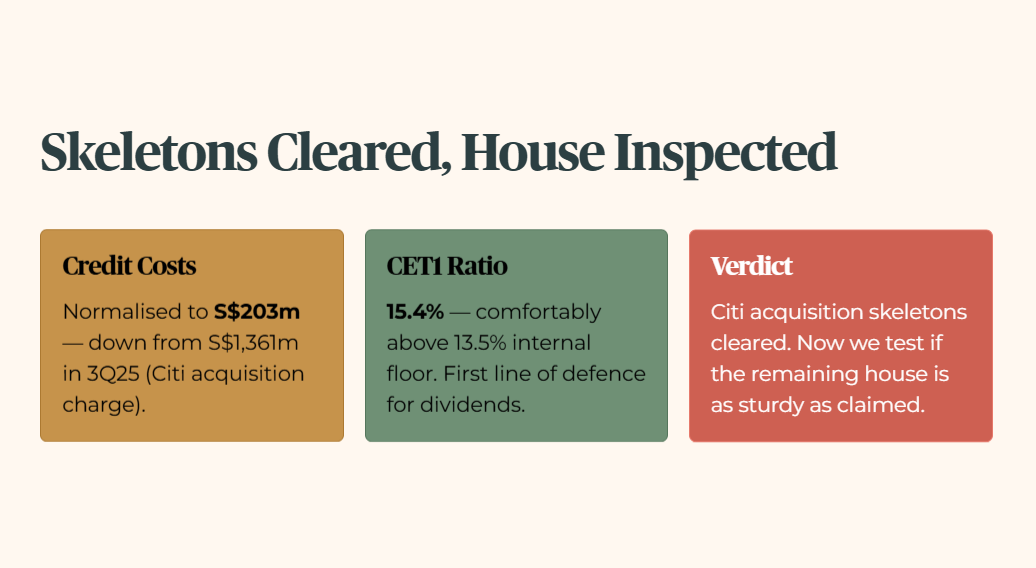

The credit costs have normalised to S$203m this quarter. That is a massive improvement from the S$1,361m charge they took in 3Q25. That charge was the primary reason the share price suffered last year. The Institutional Asian Uncle perspective here is simple. The bank has cleared the skeletons out of the closet from the Citi acquisition. Now we see if the remaining house is as sturdy as they say.

The CET1 ratio (the Common Equity Tier 1 capital ratio, which measures a bank’s core capital buffer against unexpected losses) sits at 15.4%. That is comfortably above my 13.5% internal floor and acts as a first line of defence for the dividend stream.

🦎 Iggy’s Insight

The market was spooked by that massive S$1.3b allowance charge in 2025. But the normalisation to S$203m suggests the worst of the credit stress is in the rearview mirror. Management is being cautious with their guidance because of the oil price risk to SMEs. But a 1.5% NPL target shows they still trust their underwriting. They have limited exposure to the Middle East, so the direct fallout from the war is contained. This is a management team that prefers to under-promise and over-deliver. The safety buffer is back in place.

THE FORENSIC GAP: IGGY VS. OCBC

This is the payoff section. OCBC has issued a BUY call. They see a recovery. I run a different set of rules.

The gap exists because analysts focus on the future potential of the 2030 wealth target, while my forensic screen is about what those three soft flags do to UOB’s risk-adjusted yield once you run them through the Zone 3 playbook.