OCBC Says the IPO Bar Just Got Higher. Here's What That Actually Means

The math behind OCBC's IPO warning, and what it means for your REIT income.

I used to think a new listing on the Singapore Exchange was close to a sure thing for a retirement portfolio. Get an allocation, watch it pop on debut, move on. That instinct is getting harder to justify, and OCBC’s mid-year outlook briefing gave me a clear reason why.

Why New Listings Are Suddenly a Harder Sell

Industrials Up, REITs Under Pressure

The 15 Names OCBC Is Backing

The Window Is Already Open

The Bottom Line

Why New Listings Are Suddenly a Harder Sell

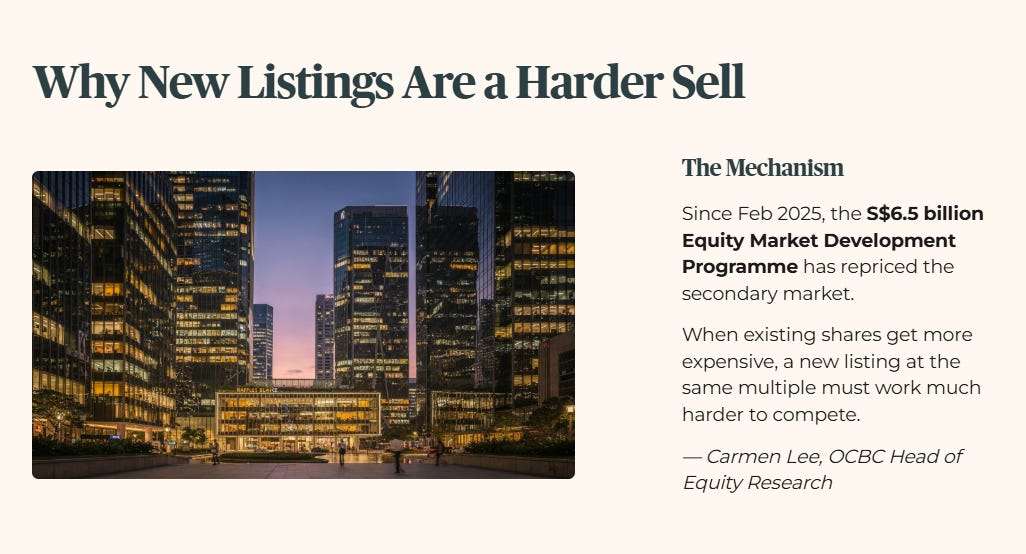

Here’s the mechanism, in plain terms. Since February 2025, the S$6.5 billion Equity Market Development Programme has been pumping capital support into local shares. Carmen Lee, OCBC’s head of equity research, made the point that this has quietly repriced the secondary market, meaning the shares of companies already listed and trading every day. When those get more expensive, a new listing pricing itself at the same multiple has to work a lot harder to pull my money away from something already proven and already paying a dividend.

Ada Lim on the same research team put a number to it: unless a new listing can show projected earnings growth of at least 20 per cent, justifying an average-market valuation becomes a tough sell. So a new issuer is really left with two options. Either come in noticeably cheaper than its peers, or bring a growth story specific enough to survive scrutiny. A familiar brand name on its own doesn’t do it any more, and JustCo’s debut earlier this year is the example OCBC pointed to: plenty of attention at listing, lacklustre share price since.

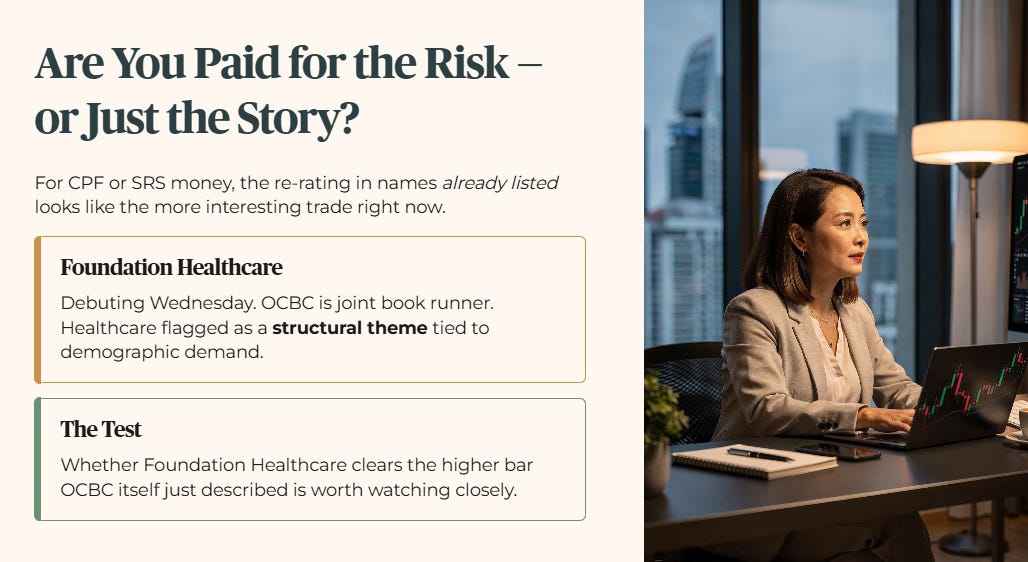

I keep coming back to a simple question here. If I’m managing CPF or SRS money and chasing the excitement of a new IPO, am I actually getting compensated for that risk, or am I just paying for the story?

Right now the re-rating happening quietly in names I already own or could already buy looks like the more interesting trade, not the flashy new one.

Foundation Healthcare is set to test this directly, debuting on Wednesday with OCBC itself as one of the joint book runners, meaning one of the banks helping underwrite and place the shares. Carmen Lee flagged healthcare and biotech as a structural theme OCBC expects to matter more over the next few years, tied to demographic demand that isn’t going away. Whether Foundation Healthcare clears the higher bar OCBC itself just described is going to be worth watching.

Industrials Up, REITs Under Pressure

OCBC stays overweight on Singapore equities for the second half of 2026, arguing valuations are still reasonable even after the Straits Times Index’s run-up, and that Singapore’s defensiveness and a firm SGD dollar are doing real work as a buffer against global inflation worries and geopolitical noise.

Industrials are where the research team sounds most enthusiastic. Ada Lim called out the sector, now the third-largest slice of the local market, as offering real exposure to the AI infrastructure buildout globally, plus a supportive backdrop from developments in the Middle East for some of the larger local industrial names. Their advice is to stay selective rather than buy the sector broadly.

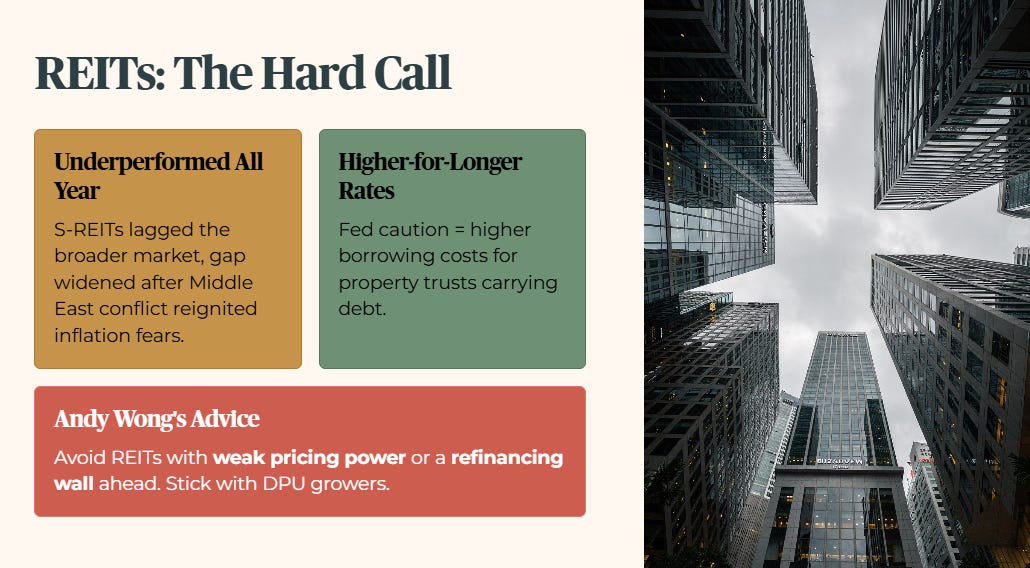

REITs are the other side of that coin, and this is the one that hits closer to home for a lot of us relying on distributions to top up retirement income. Andy Wong, senior equity research analyst at OCBC, pointed out that Singapore REITs have underperformed the broader market all year, and that gap widened after the Middle East conflict pushed inflation worries back up and made the US Federal Reserve more cautious about cutting rates. Higher-for-longer rates mean higher borrowing costs for property trusts carrying debt. His advice is to avoid REITs with weak pricing power or a refinancing wall coming up, and stick with the ones that can still grow their distribution per unit, the actual payout to unitholders, despite the rate backdrop.

That’s frustrating to sit with if REIT income is part of your plan, mine included. The honest question is whether the strongest property managers can out-earn the higher cost of debt, or whether the easy years of REIT growth are simply behind us for this cycle. I don’t think anyone, including OCBC, has a clean answer yet.

The 15 Names OCBC Is Backing

OCBC’s preferred picks skip the local banks entirely, reasoning that the banks have already had their run and the better relative upside sits elsewhere. Modelled upside across the list ranges from 12.7 to 52.2 per cent. The names:

The modelled upside range is where the real forensic work begins, and the next section walks through how those upside figures and names stack up against Iggy’s yield, gearing and coverage thresholds for CPF and SRS money.